MARKET INSIGHTS

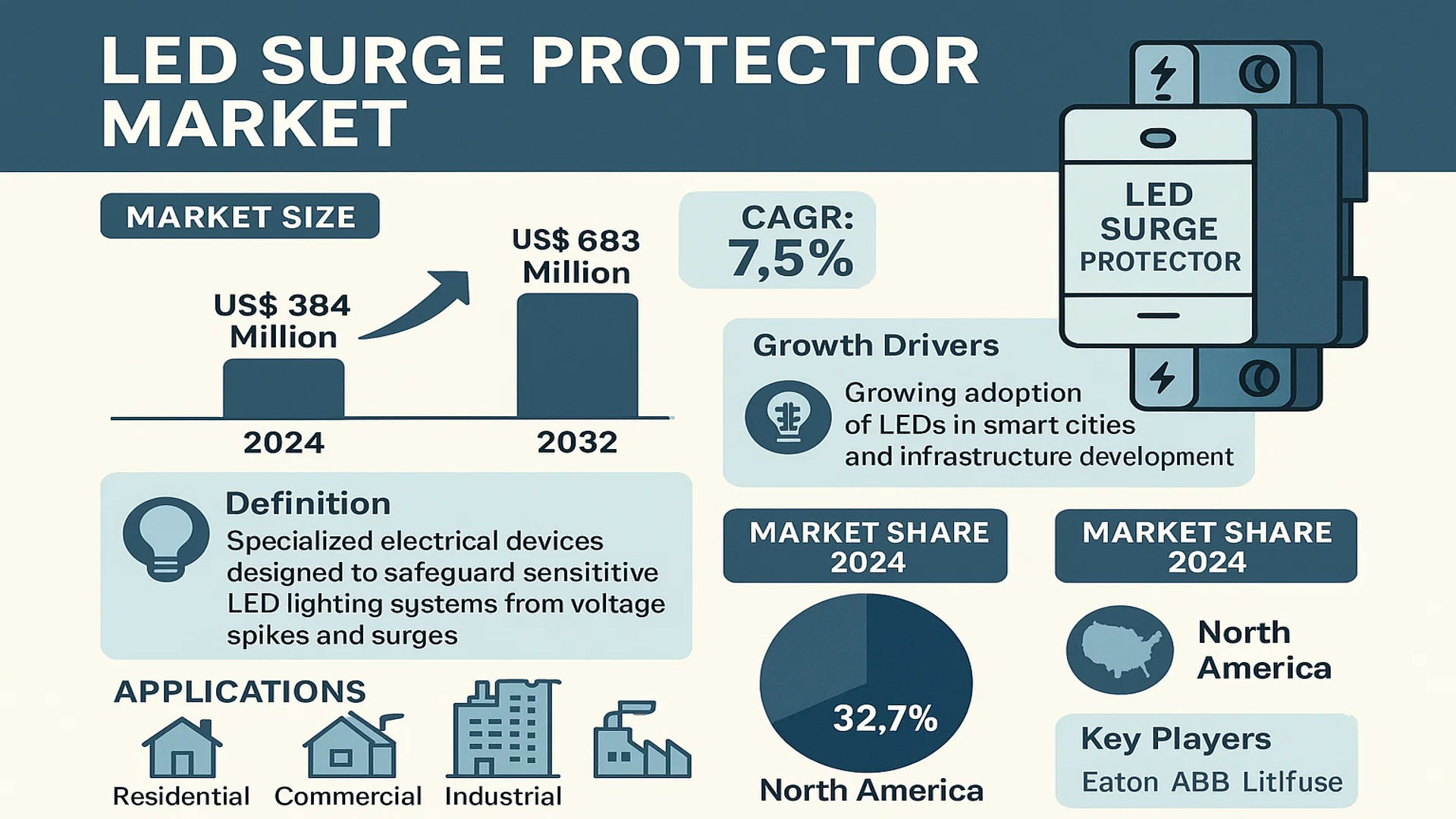

The global LED Surge Protector Market size was valued at US$ 384 million in 2024 and is projected to reach US$ 683 million by 2032, at a CAGR of 7.5% during the forecast period 2025-2032.

LED surge protectors are specialized electrical devices designed to safeguard sensitive LED lighting systems from voltage spikes and transient surges. These components play a critical role in power conditioning, featuring technologies such as metal oxide varistors (MOVs), gas discharge tubes, and transient voltage suppression diodes. The product category includes both AC and DC surge protective devices, tailored for residential, commercial, and industrial applications.

Market growth is driven by increasing LED adoption across smart city projects and infrastructure development, coupled with rising awareness about electrical protection in mission-critical environments. While North America currently leads in market share (32.7% in 2024), the Asia-Pacific region shows the highest growth potential due to rapid urbanization. Key industry players like Eaton, ABB, and Littelfuse are expanding their product portfolios through technological innovations, such as DIN-rail mounted protectors and integrated monitoring solutions.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of LED Lighting Systems to Fuel Demand for Surge Protection

The global transition toward energy-efficient lighting solutions is accelerating the adoption of LED technology across residential, commercial, and industrial applications. LED luminaires now account for over 50% of the global lighting market, with projections indicating a continued growth trajectory. However, LEDs are inherently more sensitive to voltage fluctuations compared to traditional lighting systems. This vulnerability creates a critical need for robust surge protection solutions to prevent premature failure and ensure long-term reliability. The integration of surge protectors in LED installations has become a standard industry practice, particularly in regions prone to electrical disturbances.

Stringent Safety Regulations and Standards to Boost Market Growth

Governments and regulatory bodies worldwide are implementing stringent safety standards for electrical installations, including mandatory surge protection requirements. These regulations recognize the substantial financial losses caused by power surges, which can reach millions annually in damaged equipment and downtime. The International Electrotechnical Commission (IEC) and National Electrical Code (NEC) have established comprehensive guidelines for surge protective devices in lighting applications. Compliance with these standards is driving widespread adoption of LED surge protectors, particularly in commercial and industrial settings where liability and insurance considerations make protection mandatory.

Furthermore, the growing emphasis on smart city infrastructure projects is creating additional demand for protected LED lighting networks that can withstand electrical disturbances while maintaining continuous operation.

➤ For instance, major urban development projects now routinely specify Class II or Class III surge protection for all outdoor LED lighting installations to ensure long-term reliability.

Growing Awareness of IoT and Smart Lighting Vulnerabilities to Spur Market Expansion

The proliferation of IoT-enabled smart lighting systems is exposing new vulnerabilities in LED installations. Networked luminaires with sensitive control electronics require advanced surge protection to safeguard both power and data lines. Smart lighting deployments are projected to grow at an annual rate exceeding 20%, creating parallel demand for comprehensive protection solutions. This trend is particularly evident in commercial buildings implementing advanced lighting control systems, where surge protectors are becoming integral components of the lighting infrastructure rather than optional add-ons.

MARKET RESTRAINTS

Price Sensitivity in Emerging Markets to Limit Adoption Rates

While LED surge protectors offer clear technical benefits, their adoption faces challenges in price-sensitive markets. The additional cost of surge protection can increase total system costs by 15-20%, creating resistance in budget-conscious projects. This is particularly evident in developing regions where first-cost considerations often outweigh long-term operational benefits. Manufacturers face the challenge of delivering cost-effective solutions without compromising protection performance, requiring innovative design approaches and economies of scale.

Other Restraints

Lack of Standardization

The absence of universally accepted testing protocols for LED-specific surge protectors creates confusion in the market. Variations in testing methodologies between regions and certification bodies make it difficult for end-users to compare products directly. This lack of standardization can delay purchasing decisions and complicate specification processes for lighting designers and electrical engineers.

Installation Complexity

Proper integration of surge protectors into LED systems requires technical expertise that may not always be available. Incorrect installation can compromise protection effectiveness, leading to potential equipment failures despite the presence of surge protection devices. This technical barrier is particularly challenging for retrofit applications where existing electrical infrastructure may not be ideally suited for surge protector integration.

MARKET CHALLENGES

Balancing Protection Levels with Space Constraints in Compact LED Fixtures

The ongoing miniaturization of LED luminaires presents significant engineering challenges for surge protector manufacturers. Modern LED fixtures continue to shrink in size while increasing in luminous output, leaving limited space for protection components. Designing effective surge protection solutions that fit within these constrained form factors without compromising thermal performance or protection capabilities requires ongoing innovation. This challenge is particularly acute in architectural and decorative lighting applications where aesthetic considerations further limit available space.

Managing Expectations Regarding Protection Scope and Lifespan

A significant market challenge involves educating end-users about realistic performance expectations for surge protectors. While these devices effectively mitigate most transient threats, they cannot guarantee absolute protection against all possible electrical disturbances. Furthermore, surge protectors have finite lifespans that depend on exposure to electrical events, requiring periodic inspection and replacement. Communicating these operational realities while maintaining confidence in protection effectiveness represents an ongoing challenge for manufacturers and specifiers.

MARKET OPPORTUNITIES

Integration with Renewable Energy Systems to Create New Growth Avenues

The rapid expansion of solar-powered LED lighting systems presents significant opportunities for surge protector manufacturers. Off-grid and hybrid lighting installations are particularly vulnerable to voltage fluctuations and require specialized protection solutions. The global market for solar LED lighting is projected to maintain strong growth, creating corresponding demand for compatible surge protection technologies. This sector requires products that can handle the unique electrical characteristics of renewable energy systems while withstanding harsh environmental conditions.

Development of Smart Surge Protection Solutions for Next-Generation Lighting

The convergence of LED technology with IoT capabilities is driving innovation in intelligent surge protection systems. Next-generation products with condition monitoring, remote diagnostics, and predictive maintenance features are emerging to meet the demands of smart lighting networks. These advanced solutions can communicate protection status to building management systems, providing valuable operational data while optimizing maintenance schedules. The market for smart surge protectors is expected to grow significantly as lighting systems become increasingly connected and data-driven.

Additionally, the development of application-specific protection solutions for specialized LED installations such as horticultural lighting, UV disinfection systems, and high-bay industrial lighting represents an important growth opportunity for manufacturers focusing on niche applications.

LED SURGE PROTECTOR MARKET TRENDS

Increasing Demand for Energy-Efficient Lighting Solutions Drives Market Growth

The global shift toward energy-efficient lighting solutions, particularly LED technology, has significantly bolstered the demand for LED surge protectors. With LEDs being 80% more efficient than traditional incandescent bulbs, their adoption across residential, commercial, and industrial sectors is accelerating. However, LEDs are highly sensitive to voltage spikes, necessitating robust surge protection to mitigate costly replacements and operational downtime. The market is projected to grow at a CAGR of over 7% in the forecast period, driven by widespread LED adoption in smart cities and infrastructure projects. Additionally, regulatory mandates promoting energy conservation further amplify the demand for integrated surge protection solutions.

Other Trends

Advancements in Surge Protection Technology

The integration of smart monitoring features into LED surge protectors is revolutionizing the market. Modern devices now offer real-time voltage tracking, remote alerts, and automated shutdown mechanisms to prevent damage from transient surges. Innovations such as hybrid surge protection systems, combining gas discharge tubes with metal oxide varistors (MOVs), enhance durability and response times. Furthermore, the rise of modular surge protectors allows for scalable solutions tailored to large-scale LED installations, such as street lighting networks. This technological evolution aligns with the growing emphasis on predictive maintenance and IoT-driven lighting systems.

Expansion of Smart Infrastructure Fuels Market Opportunities

The rapid deployment of smart city initiatives worldwide is a key driver for the LED surge protector market. Governments and municipalities are investing heavily in intelligent lighting systems, which rely on uninterrupted LED performance. For instance, projects like Europe’s Smart Lighting Initiative prioritize resilient infrastructure, creating a surge in demand for high-grade protection devices. In parallel, the commercial sector—including retail spaces and offices—is increasingly adopting connected lighting systems, further propelling market growth. However, challenges such as high installation costs and limited awareness in emerging economies persist, necessitating targeted educational campaigns and cost-effective product innovations.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Expand Product Offerings to Capture Market Share

The global LED surge protector market features a competitive yet fragmented landscape, with a mix of established electrical component manufacturers and specialized surge protection providers. Littelfuse has emerged as a dominant player, leveraging its extensive expertise in circuit protection solutions and a strong distribution network across North America and Europe. The company accounted for a significant revenue share in 2024, driven by its advanced SPD (Surge Protection Device) technology tailored for LED lighting systems.

ABB and Eaton maintain robust market positions through their comprehensive power management portfolios and strategic focus on industrial applications. These companies have strengthened their offerings with integrated protection solutions that combine energy efficiency with advanced surge suppression capabilities. Their growth is further supported by increasing adoption in commercial and infrastructure projects where reliable LED lighting is critical.

The market has also seen notable activity from regional players expanding their global footprint. For instance, Phoenix Contact and Legrand have enhanced their product lines with modular surge protectors designed for both AC and DC LED applications. Meanwhile, DEHN continues to lead in technological innovation with its multi-stage protection systems that address complex transient voltage scenarios in LED installations.

Strategic collaborations and M&A activities are reshaping the competitive dynamics. Companies like Bourns and Citel are focusing on acquisitions to access new technologies and distribution channels, particularly in emerging markets where LED adoption is accelerating. Simultaneously, lighting giants Philips and OSRAM are integrating surge protection directly into their LED fixtures, creating new competitive pressures for standalone protector manufacturers.

List of Key LED Surge Protector Companies Profiled

- Littelfuse (U.S.)

- Citel (France)

- Bourns (U.S.)

- LSP International (U.S.)

- ABB (Switzerland)

- Eaton (Ireland)

- Phoenix Contact (Germany)

- Legrand (France)

- Inventronics (China)

- Philips (Netherlands)

- DEHN (Germany)

- Cirprotec (Spain)

- OBO (Germany)

- Hatch Lighting (U.S.)

- Satco (U.S.)

- Universal Lighting (U.S.)

- OSRAM (Germany)

Segment Analysis:

By Type

AC Surge Protective Devices Segment Dominates Due to Widespread Electrical Infrastructure Requirements

The market is segmented based on type into:

- AC Surge Protective Devices

- Subtypes: Single-phase, Three-phase, and others

- DC Surge Protective Devices

- Hybrid Surge Protectors

- Modular Surge Protection Units

- Others

By Application

Commercial Segment Leads Owing to High Adoption in Offices and Retail Spaces

The market is segmented based on application into:

- Residential

- Commercial

- Subtypes: Office buildings, Retail spaces, Hospitality, and others

- Industrial

- Subtypes: Manufacturing plants, Warehouses, and others

- Municipal/Public Infrastructure

By Protection Level

High Protection Grade Devices Preferred for Critical LED Installations

The market is segmented based on protection level into:

- Basic Protection (Up to 10kA)

- Medium Protection (10kA-40kA)

- High Protection (Above 40kA)

By Installation Type

Panel-mounted Devices Gain Traction for Centralized Protection Systems

The market is segmented based on installation type into:

- Plug-in Devices

- Hardwired Units

- Panel-mounted Devices

- DIN Rail-mounted Units

Regional Analysis: LED Surge Protector Market

Asia-Pacific

The Asia-Pacific region dominates the global LED surge protector market, driven by rapid urbanization and large-scale infrastructure development in countries like China and India. China holds the largest market share, accounting for over 40% of regional demand, due to government initiatives promoting LED lighting adoption and smart city projects. While cost sensitivity has slowed the penetration of high-end surge protection solutions in some markets, increasing awareness of power quality issues and the rising cost of LED replacement is accelerating adoption. Japan and South Korea lead in technological adoption, with stringent regulations for electrical safety in commercial and industrial applications.

North America

North America represents the second-largest market for LED surge protectors, with the U.S. contributing approximately 60% of regional revenue. Strict electrical safety standards set by UL and NEC, coupled with the high penetration of LED lighting in commercial buildings (estimated at over 80%), drive demand for premium surge protection solutions. The market is characterized by a strong preference for integrated protection systems rather than standalone devices. Recent grid modernization initiatives and increasing extreme weather events that cause power surges have further stimulated market growth across residential and industrial sectors.

Europe

Europe’s mature market shows steady growth, supported by EU directives on energy efficiency and the widespread replacement of conventional lighting with LEDs. Germany and France collectively account for nearly half of the regional market, with high adoption in industrial and commercial applications. The market emphasizes smart surge protection systems that integrate with building automation. Eastern European countries are emerging as growth hotspots due to infrastructure upgrades and increasing foreign investments in manufacturing facilities that require reliable power protection for sensitive LED lighting systems.

Middle East & Africa

This region exhibits the fastest growth potential, with GCC countries leading adoption due to massive infrastructure projects and smart city initiatives. The UAE and Saudi Arabia account for over 70% of regional demand, particularly for industrial-grade surge protectors used in oil & gas facilities and commercial complexes. However, market growth in other African nations is constrained by limited awareness and price sensitivity, though increasing electrification projects present long-term opportunities for basic surge protection solutions.

South America

The South American market remains relatively underdeveloped but shows gradual growth, primarily in Brazil and Argentina. Economic instability has slowed large-scale infrastructure investments, but the commercial sector, particularly retail and office spaces, demonstrates increasing demand for LED surge protectors. The lack of stringent regulations and low awareness in residential applications remain key challenges, though growing middle-class adoption of premium LED lighting solutions presents future opportunities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional LED Surge Protector markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global LED Surge Protector market was valued at US$ 384 million in 2024 and is projected to reach US$ 683 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (AC/DC Surge Protective Devices), application (Residential, Commercial, Industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S. market size estimated at USD 78.2 million in 2024), Europe, Asia-Pacific (China projected to reach USD 125.5 million by 2032), Latin America, and the Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants including Littelfuse, ABB, Eaton, Philips, and Legrand, covering their product portfolios, market shares (top 5 players held approximately 42% share in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies in surge protection, including smart monitoring capabilities and IoT integration in modern LED protection systems.

- Market Drivers & Restraints: Evaluation of factors such as growing LED adoption, increasing power quality concerns, and regulatory standards versus challenges like price sensitivity and counterfeit products.

- Stakeholder Analysis: Strategic insights for LED manufacturers, electrical component suppliers, contractors, and investors regarding market opportunities and supply chain dynamics.

Primary and secondary research methods are employed, including interviews with industry experts, manufacturer data, and verified market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Surge Protector Market?

-> LED Surge Protector Market size was valued at US$ 384 million in 2024 and is projected to reach US$ 683 million by 2032, at a CAGR of 7.5% during the forecast period 2025-2032.

Which key companies operate in Global LED Surge Protector Market?

-> Key players include Littelfuse, ABB, Eaton, Philips, Legrand, Citel, Bourns, and Phoenix Contact, among others.

What are the key growth drivers?

-> Key growth drivers include rising LED adoption, increasing power quality concerns, and stricter electrical safety regulations.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America currently holds the largest market share.

What are the emerging trends?

-> Emerging trends include smart surge protectors with remote monitoring, integrated protection for smart lighting systems, and miniaturization of components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...