MARKET INSIGHTS

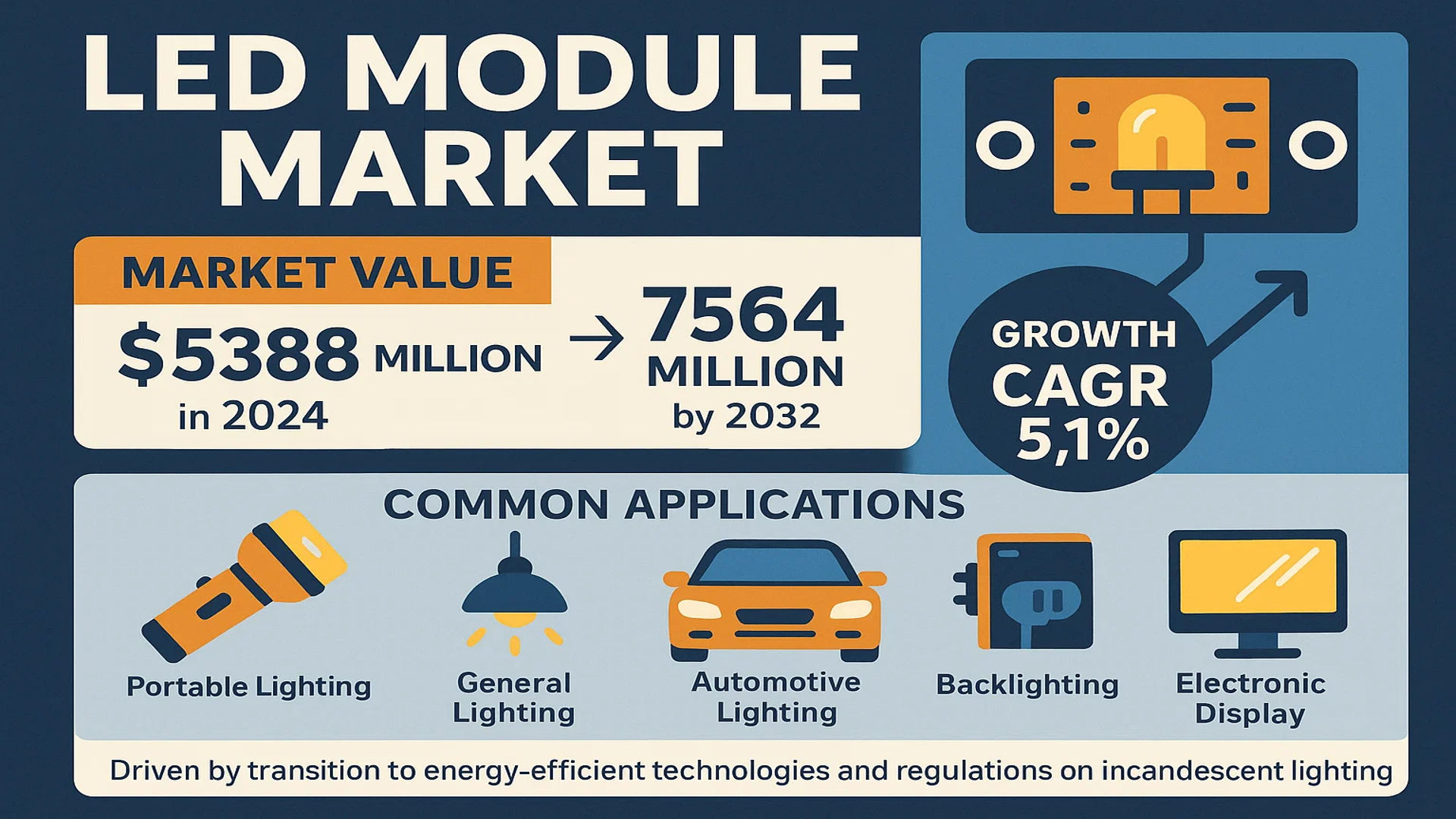

The global LED Module Market was valued at 5388 million in 2024 and is projected to reach US$ 7564 million by 2032, at a CAGR of 5.1% during the forecast period.

A Light Emitting Diode (LED) module is a self-contained, integrated device designed to function independently or interface with a compatible unit. These modules are fundamental components used to create highly energy-efficient, durable, and versatile lighting solutions. They consist of one or multiple LED bulbs housed within a fixture that either contains its own power system or connects to an external driver. Common applications span a wide spectrum, including portable lighting like flashlights and headlamps, residential and commercial general lighting, sophisticated automotive lighting systems, and essential backlighting for electronic displays.

The market’s expansion is driven by the global transition towards energy-efficient technologies and stringent government regulations phasing out incandescent lighting. Furthermore, the declining cost of LED technology and its superior lifespan compared to traditional lighting are significant growth catalysts. The market is also characterized by a high degree of fragmentation; however, the top five manufacturers, including Osram and Philips Lighting, collectively hold a substantial share of approximately 30%. Geographically, China dominates as the largest market, accounting for nearly 30% of global consumption, followed closely by Europe.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Energy-Efficient Lighting Solutions to Propel Market Expansion

The global shift toward energy conservation and sustainability is significantly driving the LED module market. Governments worldwide are implementing stringent regulations phasing out inefficient lighting technologies while promoting LED adoption through subsidies and rebate programs. LED modules consume up to 80% less energy than traditional incandescent bulbs and approximately 40% less than fluorescent alternatives, making them the preferred choice for commercial, industrial, and residential applications. The continuous decline in LED prices, coupled with their extended lifespan exceeding 50,000 hours, has accelerated market penetration across all sectors. This energy efficiency trend is particularly prominent in emerging economies where rapid urbanization and infrastructure development are creating substantial demand for cost-effective lighting solutions.

Technological Advancements in Smart Lighting Systems to Accelerate Growth

Technological innovations in smart lighting and IoT integration are creating substantial growth opportunities for the LED module market. The development of connected lighting systems that incorporate sensors, wireless connectivity, and intelligent controls enables enhanced energy management, personalized lighting experiences, and data collection capabilities. These systems are increasingly being deployed in smart cities, commercial buildings, and residential applications, driving demand for advanced LED modules with integrated control circuitry. The integration of Li-Fi technology, which uses LED lights for data transmission, represents another innovative application expanding the market’s potential beyond conventional illumination purposes.

Growing Automotive Lighting Applications to Fuel Market Development

The automotive industry’s increasing adoption of LED lighting solutions is serving as a major growth driver for the LED module market. Automotive manufacturers are progressively incorporating LED modules in headlights, tail lights, interior lighting, and dashboard displays due to their superior energy efficiency, design flexibility, and enhanced safety features. The trend toward electric vehicles, which prioritize energy conservation to extend battery life, has further accelerated LED adoption in automotive applications. Additionally, regulatory mandates regarding vehicle safety and visibility standards are prompting automakers to upgrade their lighting systems, creating sustained demand for high-performance LED modules throughout the forecast period.

MARKET CHALLENGES

Intense Price Competition and Margin Pressures to Challenge Market Stability

The LED module market faces significant challenges from intense price competition and shrinking profit margins. The market has become increasingly commoditized, with numerous manufacturers competing primarily on price rather than technological differentiation. This price sensitivity is particularly pronounced in the general lighting segment, where customers often prioritize cost over advanced features. Manufacturing overcapacity in certain regions has exacerbated price pressures, leading to thinner margins across the value chain. While large-scale manufacturers benefit from economies of scale, smaller players struggle to maintain profitability, potentially leading to market consolidation and reduced innovation investment.

Other Challenges

Technical Standardization Issues

The lack of universal technical standards for LED modules creates compatibility challenges across different systems and applications. Variations in electrical characteristics, mechanical dimensions, and control protocols hinder interoperability between products from different manufacturers. This fragmentation complicates system design and installation while increasing costs for end-users who must ensure component compatibility. The absence of standardized testing methodologies also makes performance comparisons difficult, potentially undermining customer confidence in product claims and specifications.

Thermal Management Complexities

Effective thermal management remains a persistent technical challenge for high-power LED modules. Excessive heat generation can significantly reduce LED lifespan and light output while altering color characteristics. Designing efficient heat dissipation systems adds complexity and cost to module development, particularly for compact form factors required in modern lighting applications. These thermal considerations often necessitate advanced materials and sophisticated design approaches, creating barriers for manufacturers seeking to develop competitive products while maintaining performance reliability.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Component Shortages to Constrain Market Growth

The LED module market is experiencing constraints due to vulnerabilities in the global supply chain and periodic shortages of critical components. The industry’s reliance on specialized semiconductors, rare earth materials, and advanced substrates creates dependency on limited sourcing options. Geopolitical tensions and trade restrictions have disrupted supply chains, leading to production delays and increased material costs. These supply chain challenges are particularly impactful for manufacturers operating in regions with limited local sourcing options, forcing them to maintain higher inventory levels and absorb increased logistics expenses that ultimately affect market competitiveness and growth potential.

Technical Complexity in System Integration to Hinder Market Penetration

The technical complexity associated with integrating LED modules into existing lighting systems presents a significant restraint for market expansion. Many traditional lighting infrastructures were designed for conventional technologies and require substantial modification to accommodate LED modules effectively. This integration challenge is particularly evident in retrofit applications where compatibility issues, electrical characteristics mismatches, and physical form factor constraints create installation barriers. The need for specialized knowledge among installers and maintenance personnel further complicates adoption, especially in price-sensitive market segments where additional installation costs may deter potential customers from transitioning to LED technology.

Perceived Quality Variations and Performance Concerns to Limit Consumer Confidence

Market growth is restrained by perceived quality variations among LED module products and performance concerns among end-users. Inconsistent product quality across different manufacturers, particularly in the lower price segments, has created skepticism regarding longevity and reliability claims. Performance issues such as color shifting over time, lumen depreciation rates exceeding specifications, and premature failure in certain environmental conditions have affected consumer confidence. These quality perception challenges are particularly impactful in commercial and industrial applications where lighting system reliability directly impacts operational continuity and maintenance costs.

MARKET OPPORTUNITIES

Expansion in Horticulture and Agricultural Lighting to Create New Growth Avenues

The growing adoption of LED modules in horticulture and agricultural applications presents substantial growth opportunities. Controlled environment agriculture operations are increasingly utilizing specialized LED lighting systems to optimize plant growth, enhance crop yields, and reduce energy consumption. The ability to tailor light spectra for specific plant requirements enables precision agriculture techniques that improve productivity and resource efficiency. This application segment is experiencing rapid expansion as food security concerns and sustainable farming practices gain prominence globally, creating new revenue streams for LED module manufacturers developing agriculture-specific solutions.

Emerging Applications in Healthcare and Human-Centric Lighting to Drive Innovation

Healthcare applications and human-centric lighting systems represent promising growth opportunities for the LED module market. Medical facilities are adopting LED lighting for surgical applications, patient care environments, and diagnostic equipment due to their precise color rendering capabilities and minimal heat emission. The development of tunable white LED systems that mimic natural daylight patterns supports circadian rhythm regulation in healthcare settings, senior living facilities, and educational environments. This focus on lighting quality and biological impact rather than mere illumination is driving premium product development and creating value-added market segments with higher margins.

Infrastructure Development in Emerging Economies to Provide Substantial Market Potential

Rapid infrastructure development in emerging economies offers significant growth opportunities for the LED module market. Large-scale urbanization projects, transportation infrastructure development, and commercial construction activities in developing regions are driving substantial demand for energy-efficient lighting solutions. Government initiatives promoting smart city development and energy conservation are further accelerating LED adoption in public lighting, commercial buildings, and residential applications. These market dynamics create opportunities for both international manufacturers and local players to expand their presence in high-growth regions while developing products tailored to specific regional requirements and applications.

LED MODULE MARKET TRENDS

Smart and Connected Lighting Solutions Driving Market Evolution

The integration of smart technologies and Internet of Things (IoT) connectivity into LED modules represents a significant market trend, transforming traditional lighting into intelligent systems. These advanced modules now incorporate sensors, wireless communication capabilities, and microcontrollers that enable features such as remote control, automated dimming, color tuning, and energy usage monitoring. The global smart lighting market, which heavily relies on advanced LED modules, is projected to grow at a compound annual growth rate of over 20% through 2030, indicating substantial demand for these intelligent solutions. Furthermore, the adoption of Li-Fi technology, where LED modules transmit data through light waves, is creating new applications in indoor positioning systems and high-speed data transmission. This technological convergence is particularly prominent in commercial and industrial applications, where energy management and operational efficiency are paramount concerns for facility managers and building owners.

Other Trends

Sustainability and Energy Efficiency Regulations

Government regulations and environmental policies worldwide are accelerating the transition from traditional lighting to LED technology, creating sustained demand for high-quality LED modules. Numerous countries have implemented stringent energy efficiency standards and are phasing out incandescent and fluorescent lighting, with the European Union’s Ecodesign Directive and similar regulations in North America and Asia-Pacific driving market growth. The energy efficiency of LED modules, which can reduce energy consumption by up to 80% compared to conventional lighting solutions, aligns perfectly with global sustainability goals and corporate environmental initiatives. This regulatory push, combined with decreasing manufacturing costs and improved performance characteristics, has made LED modules the default choice for new installations and retrofitting projects across residential, commercial, and industrial sectors.

Miniaturization and High-Density Packaging Innovations

Technological advancements in miniaturization and high-density packaging are enabling the development of increasingly compact and powerful LED modules, particularly benefiting the backlighting and automotive lighting segments. Manufacturers are achieving higher lumen output per square millimeter through improved thermal management solutions and advanced packaging techniques such as Chip Scale Package (CSP) and flip-chip technology. The automotive sector especially benefits from these innovations, with premium vehicles incorporating sophisticated LED modules for adaptive headlights, dynamic turn signals, and ambient interior lighting. The global automotive LED market is experiencing robust growth, with projections indicating it will exceed 7 billion dollars by 2027, driven by consumer demand for enhanced safety features and aesthetic appeal. These compact, high-performance modules are also revolutionizing the display industry, enabling thinner televisions, monitors, and mobile devices with superior brightness and color reproduction.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global LED Module market exhibits a semi-consolidated competitive landscape, characterized by the presence of multinational giants, specialized medium-sized enterprises, and numerous smaller regional players. This dynamic is driven by the market’s valuation of $5.388 billion in 2024 and its projected growth to $7.564 billion by 2032, creating significant opportunities across diverse applications like general lighting, automotive, and backlighting. The top five manufacturers collectively command approximately 30% of the global market share, indicating a competitive environment where innovation and strategic positioning are paramount.

ams-OSRAM AG (formerly Osram) is a dominant force in the market, a position solidified through its extensive technological expertise in optoelectronics and a robust global distribution network spanning Europe, North America, and Asia-Pacific. Similarly, Signify N.V. (operating under the Philips Lighting brand) holds a significant market share, attributed to its strong brand recognition, comprehensive portfolio of connected lighting systems, and deep penetration in both the professional and consumer segments.

These leading companies are aggressively pursuing growth through continuous research and development, focusing on enhancing luminous efficacy, improving color rendering index (CRI), and developing smarter, IoT-enabled modules. Additionally, strategic mergers, acquisitions, and geographic expansions into high-growth regions, particularly Asia-Pacific, are key initiatives expected to further consolidate their market positions over the forecast period.

Meanwhile, other major players like Cree LED (part of SMART Global Holdings) and Seoul Semiconductor are strengthening their presence through significant investments in novel technologies such as WICOP (Wafer-level Integrated Chip on PCB) and nPola, which offer superior brightness and design flexibility. Companies such as Nichia Corporation and Samsung Electronics are also intensifying competition by leveraging their vertical integration capabilities and massive production scales to cater to the high-volume backlighting and automotive lighting sectors.

List of Key LED Module Companies Profiled

- ams-OSRAM AG (Austria)

- Signify N.V. (Philips Lighting) (Netherlands)

- Cree LED, Inc. (SMART Global Holdings) (U.S.)

- GE Lighting, A Savant Company (U.S.)

- Seoul Semiconductor Co., Ltd. (South Korea)

- Panasonic Corporation (Japan)

- Nichia Corporation (Japan)

- Lumileds Holding B.V. (Netherlands)

- Acuity Brands, Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- LG Innotek Co., Ltd. (South Korea)

- Eaton Corporation plc (Ireland)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Toyoda Gosei Co., Ltd. (Japan)

- OPPLE Lighting Co., Ltd. (China)

- Zhejiang Yankon Group Co., Ltd. (China)

- Edison Opto Corporation (Taiwan)

Segment Analysis:

By Type

Low Voltage LED Driver Module Segment Leads Due to High Demand in Consumer Electronics and Portable Lighting

The market is segmented based on type into:

- High Voltage LED Driver Module

- Low Voltage LED Driver Module

- Medium Voltage LED Driver Module

By Application

General Lighting Segment Dominates Owing to Widespread Adoption in Residential, Commercial, and Industrial Sectors

The market is segmented based on application into:

- General Lighting

- Automotive Lighting

- Backlighting

By End User

Residential and Commercial Sector Holds Largest Share Driven by Energy Efficiency Regulations and Smart City Initiatives

The market is segmented based on end user into:

- Residential

- Commercial

- Industrial

- Automotive

- Consumer Electronics

Regional Analysis: LED Module Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global LED Module market, accounting for approximately 50% of global consumption by volume. This dominance is primarily driven by China, which alone holds a market share of about 30%, making it the world’s largest single market. The region’s massive manufacturing base, extensive government-led infrastructure projects, and rapid urbanization are key growth drivers. Countries like China, India, Japan, and South Korea are hubs for both production and consumption, with significant demand stemming from the general lighting and backlighting sectors for consumer electronics. While cost-competitiveness remains a primary focus, leading to the prevalence of Low Voltage LED Driver Modules, there is a marked and accelerating shift towards higher-efficiency and smart lighting solutions, fueled by stringent national energy efficiency standards and growing environmental consciousness among consumers and governments alike.

Europe

Europe represents a mature and technologically advanced market for LED modules, characterized by strict regulatory frameworks such as the EU’s Ecodesign Directive and energy labeling requirements. These regulations aggressively phase out inefficient lighting, creating a sustained and high-value demand for innovative LED solutions. The market is driven by a strong emphasis on sustainability, quality, and smart city initiatives. Germany, France, and the U.K. are the largest national markets, with significant investments in retrofitting existing infrastructure with energy-efficient lighting. The demand is notably high for High Voltage LED Driver Modules and sophisticated modules integrated into smart home and building automation systems. Innovation, compliance with circular economy principles, and product longevity are the paramount market drivers, with leading European companies like Osram playing a crucial role.

North America

The North American market, led by the United States, is a significant and high-value region focused on technological innovation and quality. Growth is propelled by the ongoing modernization of commercial and industrial lighting infrastructure, the adoption of smart building technologies, and robust consumer demand for energy-efficient products. While federal energy standards (e.g., DOE regulations) set the baseline, state-level initiatives and utility rebate programs further accelerate the adoption of LED lighting. The market has a strong preference for reliable, high-performance modules, with significant activity in the automotive lighting sector as well. Major players like Cree and Acuity Brands have a strong foothold here. The region’s well-established distribution channels and high consumer purchasing power support the adoption of premium, feature-rich LED modules.

South America

The South American LED module market is in a growth phase, presenting nascent but tangible opportunities. Brazil and Argentina are the primary markets, driven by gradual infrastructure development and increasing awareness of energy savings. However, the market’s expansion is often tempered by economic volatility, currency fluctuations, and less stringent enforcement of energy efficiency standards compared to other regions. This economic sensitivity makes the market more receptive to cost-effective, Low Voltage LED Driver Modules, with price being a critical purchasing factor. While the adoption of advanced, smart lighting solutions is slower, the long-term potential is significant as urbanization continues and economic conditions stabilize, paving the way for future market maturation.

Middle East & Africa

The Middle East & Africa region is an emerging market with growth concentrated in specific nations, particularly the Gulf Cooperation Council (GCC) countries like the UAE, Saudi Arabia, and Israel. Growth is fueled by massive urban development projects, smart city initiatives (e.g., NEOM in Saudi Arabia), and the need for energy-efficient solutions in harsh climatic conditions. However, the broader regional market faces challenges, including infrastructure gaps, funding limitations, and varied levels of regulatory development. While there is a clear demand for durable and high-quality LED modules capable of withstanding extreme environments, the pace of adoption is uneven. The market holds considerable long-term potential, but its development is intrinsically linked to economic diversification plans and sustained infrastructure investment across the region.

Report Scope

This market research report provides a comprehensive analysis of the global LED Module market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Module Market?

-> LED Module Market was valued at 5388 million in 2024 and is projected to reach US$ 7564 million by 2032, at a CAGR of 5.1% during the forecast period.

Which key companies operate in Global LED Module Market?

-> Key players include Osram, Philips Lighting, Cree, GE Lighting, Seoul Semiconductor, Panasonic, Nichia, Samsung, LG Innotek, and Eaton, among others. The top five manufacturers hold a combined market share of approximately 30%.

What are the key growth drivers?

-> Key growth drivers include increasing demand for energy-efficient lighting solutions, rapid urbanization, government initiatives promoting LED adoption, and the expanding automotive lighting sector.

Which region dominates the market?

-> Asia-Pacific is the largest market, accounting for approximately 30% of global revenue, with China being the dominant country. Europe follows as the second-largest market with a share of about 20%.

What are the emerging trends?

-> Emerging trends include integration of smart lighting with IoT systems, development of human-centric lighting solutions, miniaturization of LED modules, and increasing adoption of UV-C LED modules for disinfection applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...