MARKET INSIGHTS

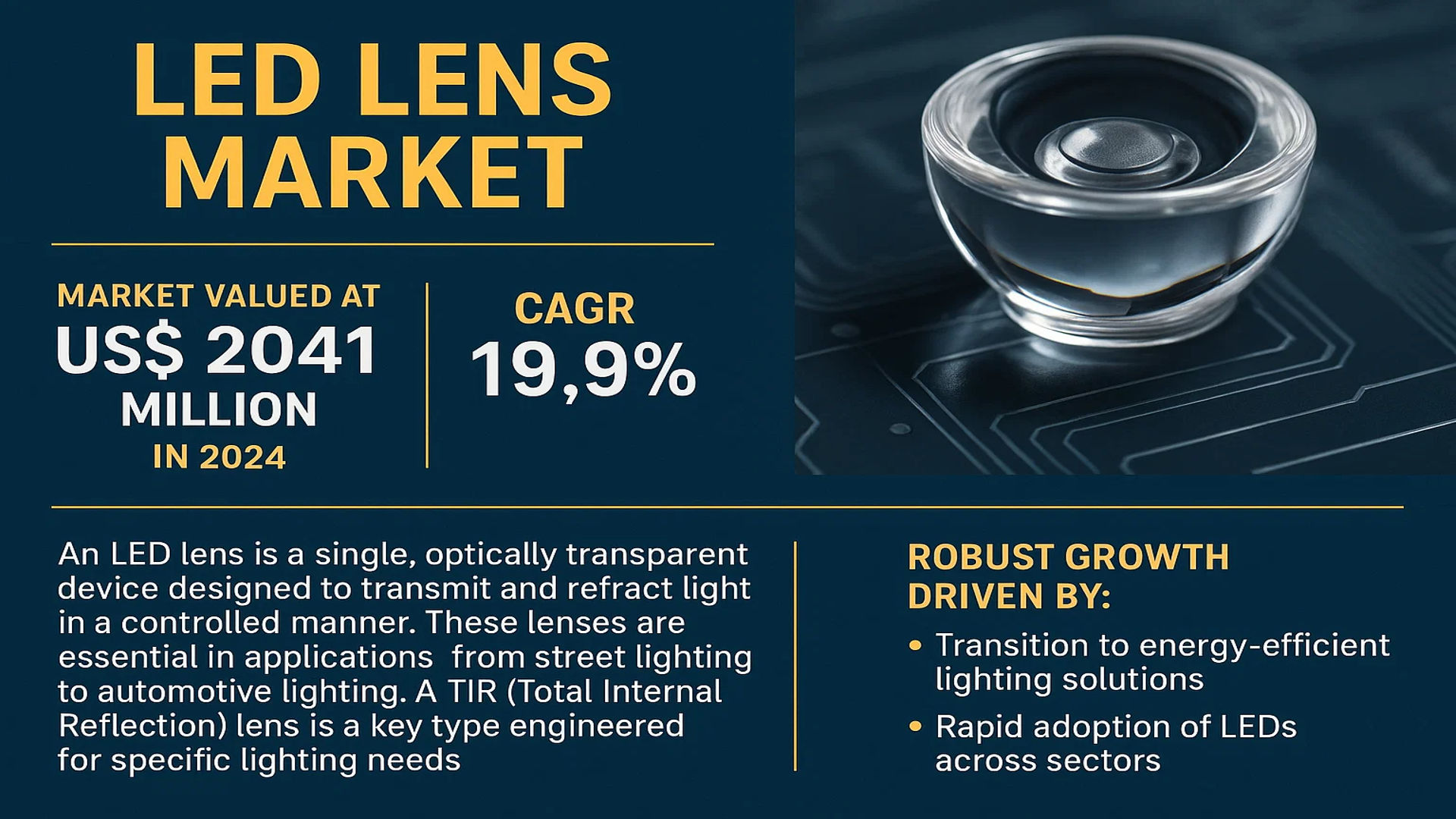

The global LED Lens Market was valued at 2041 million in 2024 and is projected to reach US$ 7078 million by 2032, at a CAGR of 19.9% during the forecast period.

An LED lens is a single, optically transparent device shaped and designed to allow the transmission and refraction of light to create a specific and controlled optical outcome. These lenses, which may consist of a single or multiple elements, are crucial for directing and focusing light from LEDs, thereby enhancing efficiency and performance in a wide variety of applications from street lighting to indoor and automotive lighting. A key type is the secondary optic, often referred to as a TIR (Total Internal Reflection) lens, which is engineered for optimal performance in specific lighting applications.

The market is experiencing robust growth driven by the global transition to energy-efficient lighting solutions and the rapid adoption of LEDs across multiple sectors. This expansion is further fueled by technological advancements in lens materials, such as PMMA and polycarbonate, which offer superior optical properties and durability. However, the market also faces challenges, including intense price competition and the technical complexity of designing lenses for increasingly specialized applications. Leading players such as Ledlink Optics, Carclo Optics, and Auer Lighting collectively hold a significant market share of approximately 18%, indicating a moderately concentrated competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Global Energy Efficiency Mandates Accelerate LED Adoption and Lens Market Expansion

Stringent global energy efficiency regulations are driving unprecedented adoption of LED lighting systems, subsequently fueling demand for precision optical components like LED lenses. Over 85 countries have implemented mandatory phase-outs of inefficient lighting technologies, creating a regulatory environment where LED technology becomes the default solution. The European Union’s Ecodesign Directive and similar regulations in North America and Asia-Pacific have accelerated this transition, with LED penetration in general lighting applications exceeding 60% globally as of 2024. LED lenses play a critical role in maximizing the efficiency of these systems, with high-quality optical components improving lumen output by 15-25% compared to standard solutions. This regulatory push creates a sustained demand environment where manufacturers must incorporate advanced optical solutions to meet efficiency standards, directly benefiting the LED lens market.

Automotive Lighting Revolution and Smart City Initiatives Drive Precision Optical Requirements

The automotive industry’s rapid transition to LED lighting systems represents a significant growth driver for precision lens manufacturers. Modern vehicles incorporate between 200-300 LEDs per vehicle for exterior and interior lighting applications, requiring specialized optical solutions for each function. Adaptive driving beams, dynamic turn signals, and sophisticated interior lighting systems demand precise beam control that only advanced LED lenses can provide. The global automotive LED market is projected to grow at approximately 8.5% annually, directly correlating to increased lens demand. Concurrently, smart city initiatives worldwide are driving infrastructure upgrades, with intelligent street lighting representing a $15 billion market opportunity. These systems require precisely controlled illumination patterns to minimize light pollution while ensuring safety, creating specialized demand for Total Internal Reflection (TIR) lenses and other advanced optical solutions that can achieve specific photometric distributions.

Technological Advancements in Material Science Enable New Application Frontiers

Breakthroughs in optical materials are expanding application possibilities for LED lenses across multiple industries. The development of high-temperature-resistant silicones and advanced polycarbonate blends enables lens operation in environments previously inaccessible to plastic optics. Automotive forward lighting applications now require materials capable of withstanding temperatures exceeding 135°C while maintaining optical clarity, driving innovation in material composition. In architectural lighting, UV-stable PMMA formulations allow for outdoor applications without yellowing or degradation. Recent material innovations have improved light transmission efficiency to 92-95% compared to traditional materials’ 88-90%, representing a significant performance enhancement. These material advancements coincide with manufacturing process improvements where injection molding techniques achieve surface finishes below 5nm Ra, enabling precise optical control previously only possible with glass elements.

MARKET RESTRAINTS

Raw Material Price Volatility and Supply Chain Constraints Impact Manufacturing Stability

The LED lens market faces significant challenges from raw material price fluctuations and supply chain disruptions affecting production costs and delivery timelines. Optical-grade polycarbonate and PMMA prices have experienced volatility ranging between 18-25% annually due to petrochemical market instability and production capacity constraints. Specialty optical silicones, essential for high-temperature applications, have seen even greater price variations exceeding 30% during supply-constrained periods. These cost pressures are particularly challenging for manufacturers operating in competitive market segments where pricing power is limited. Additionally, the specialized nature of optical-grade materials creates dependency on a limited number of global suppliers, creating vulnerability to geopolitical tensions and trade policy changes. The concentration of PMMA production capacity in specific regions creates logistical challenges and potential single points of failure in the supply chain.

Technical Complexity and Precision Manufacturing Requirements Create High Barriers to Entry

Manufacturing precision LED lenses requires sophisticated equipment and specialized expertise that creates significant barriers to market entry and expansion. Injection molding machines capable of producing optical-grade components represent investments ranging from $500,000 to over $2 million per unit, while metrology equipment for quality verification adds substantial additional capital requirements. The precision required for optical surfaces typically demands tolerances within ±5 microns and surface roughness specifications below 10nm Ra, necessitating climate-controlled manufacturing environments and highly skilled technicians. Maintaining consistent quality across production runs presents additional challenges, with yield rates for complex optical designs often initially below 60% before process optimization. This technical complexity is compounded by the extensive validation processes required by automotive and aerospace customers, where qualification periods can extend beyond 18 months and require investment in specialized testing equipment.

Intense Price Competition from Asian Manufacturers Squeezes Profit Margins

The market faces substantial pricing pressure from manufacturers in cost-competitive regions, particularly Chinese companies benefiting from government support and scaled production facilities. Asian manufacturers currently account for approximately 65% of global LED lens production by volume, leveraging lower labor costs and integrated supply chains to achieve significant cost advantages. This competitive landscape has driven average selling prices down by 7-9% annually over the past three years, compressing profit margins despite increasing technical requirements. The situation is particularly challenging for manufacturers serving price-sensitive market segments like general illumination, where customers often prioritize cost over optical performance. This pricing environment makes recouping investments in research and development increasingly difficult, potentially limiting innovation in the long term as companies focus on cost reduction rather than performance enhancement.

MARKET CHALLENGES

Rapid Technological Obsolescence and Short Product Life Cycles Challenge R&D Investment Recovery

The LED lens industry faces the significant challenge of rapidly evolving technology standards and shortening product life cycles that complicate investment recovery. LED technology improvements are occurring at a pace where product performance specifications become obsolete within 18-24 months, requiring continuous research and development investment. The transition from conventional LEDs to Micro-LED and Mini-LED technologies represents a particular challenge, as these emerging technologies require completely different optical approaches and manufacturing techniques. Developing lenses for these new platforms requires investment in new design software, prototyping capabilities, and production equipment, with individual development projects often exceeding $500,000 in costs. The rapid pace of change means that products frequently reach the end of their commercial life before companies can fully recoup these investments, creating financial pressure particularly for smaller manufacturers with limited resources.

Other Challenges

Intellectual Property Protection and Patent Infringement Risks

The optical design space faces ongoing challenges regarding intellectual property protection, with patent infringement cases increasing by approximately 40% over the past five years. Optical designs for specific applications often have narrow patent protection, creating legal uncertainties for manufacturers developing products for similar applications. The global nature of the market complicates enforcement, with different jurisdictions offering varying levels of protection. This environment creates significant legal costs for companies seeking to protect their designs, while simultaneously creating uncertainty regarding the freedom to operate for new product development.

Customization Demands and Small Batch Production Requirements

Market trends toward customization and application-specific solutions create manufacturing inefficiencies and cost challenges. Customers increasingly demand lenses tailored to specific photometric requirements, leading to production runs often limited to 5,000-50,000 units compared to standard product runs exceeding 500,000 units. These small batch sizes reduce manufacturing efficiency and increase per-unit costs due to frequent mold changes and process adjustments. The customization process itself requires extensive application engineering support, creating additional cost burdens that are difficult to pass through to customers in competitive market environments.

MARKET OPPORTUNITIES

Emerging Applications in Horticulture Lighting and UV Disinfection Create New Growth Vectors

The expanding applications of LED technology in specialized fields present substantial growth opportunities for lens manufacturers. Horticulture lighting represents a particularly promising segment, with the market projected to exceed $5 billion by 2028, requiring specialized optical solutions to optimize plant growth spectra. These applications demand precise light distribution patterns and specific wavelength management that only advanced optical systems can provide. Similarly, UV-C disinfection applications have created new market opportunities following increased focus on sanitation, with UV LED systems requiring specialized quartz lenses capable of transmitting ultraviolet wavelengths while withstanding degradation. The medical and healthcare sterilization market for UV LEDs is growing at over 20% annually, creating corresponding demand for specialized optical components. These emerging applications often command premium pricing and have less exposure to the cost pressures affecting general illumination markets.

Integration with Smart Lighting Systems and IoT Connectivity Drives Value-Added Solutions

The convergence of lighting with Internet of Things (IoT) technologies creates opportunities for lens manufacturers to develop integrated solutions that command higher margins. Smart lighting systems require optical components that can accommodate sensors, communication modules, and other electronic components while maintaining photometric performance. This integration often requires custom optical designs that combine traditional illumination functions with light sensing, data transmission, and environmental monitoring capabilities. The global smart lighting market is expected to grow at a compound annual growth rate of 20% through 2030, creating substantial opportunities for manufacturers who can develop these integrated solutions. These systems typically sell at 2-3 times the price of conventional lighting solutions, providing better margin opportunities while requiring closer collaboration with lighting system manufacturers during the design process.

Advancements in Additive Manufacturing Enable Complex Geometries and Rapid Prototyping

Technological advancements in additive manufacturing are creating new opportunities for producing complex optical geometries that were previously impossible or economically unfeasible with traditional manufacturing methods. High-resolution 3D printing technologies now achieve surface finishes suitable for optical applications, enabling rapid prototyping of complex lens designs within days rather than weeks. This capability significantly reduces development time and cost for custom applications, making specialized solutions economically viable for smaller production runs. The ability to create freeform optical surfaces with additive manufacturing opens new possibilities for optical performance, particularly for applications requiring specific light distribution patterns that cannot be achieved with traditional rotationally symmetric designs. While currently limited to prototyping and low-volume production, continuing improvements in additive manufacturing technology are gradually expanding its application to medium-volume production scenarios.

LED LENS MARKET TRENDS

Advancements in Optical Design and Materials to Emerge as a Key Trend

The global LED lens market is experiencing a significant transformation driven by innovations in optical design and material science. While traditional materials like PMMA and Polycarbonate continue to dominate with approximately 65% market share collectively, newer materials such as advanced silicones and hybrid polymers are gaining traction for high-temperature applications, particularly in automotive lighting. The evolution towards Total Internal Reflection (TIR) lenses has revolutionized light control efficiency, achieving up to 92% optical efficiency in premium applications. This advancement is crucial because it enables manufacturers to achieve higher lumens per watt ratios, directly addressing the growing demand for energy-efficient lighting solutions across commercial and industrial sectors. Furthermore, the integration of micro-optical structures and freeform lens designs has enabled more precise beam control, reducing light pollution and improving uniformity in street lighting applications by up to 40% compared to conventional solutions.

Other Trends

Smart City Infrastructure Development

The global push toward smart city development is creating substantial opportunities for advanced LED lens systems. Urbanization projects worldwide are incorporating intelligent lighting systems that require sophisticated optical solutions for adaptive lighting, motion sensing, and data collection capabilities. Street lighting applications, which account for approximately 28% of the LED lens market, are increasingly incorporating lenses with integrated sensors and communication modules. This integration enables municipalities to implement dynamic lighting control systems that can reduce energy consumption by 30-50% while improving public safety through enhanced illumination patterns. The convergence of optical design with IoT connectivity represents a fundamental shift from simple illumination to multifunctional urban infrastructure, driving demand for lenses that can accommodate both lighting and data transmission functions within compact form factors.

Automotive Lighting Revolution

Automotive lighting represents one of the fastest-growing segments within the LED lens market, projected to achieve a CAGR of approximately 22.3% through 2032. This growth is fueled by the automotive industry’s transition toward Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies, which require highly sophisticated lighting solutions. LED lenses for automotive applications are evolving beyond basic illumination to include adaptive front-lighting systems, dynamic bending lights, and high-resolution projection systems. The demand for premium polycarbonate and glass lenses with enhanced thermal stability has increased significantly, as these materials can withstand the rigorous environmental conditions required for automotive certification. Furthermore, the trend toward slimmer and more aerodynamic vehicle designs is pushing lens manufacturers to develop increasingly compact optical systems that deliver superior performance while meeting stringent space constraints. This has led to innovations in multi-functional lens arrays that combine several optical functions within single components, reducing assembly complexity while improving overall system reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Global Expansion Drive Market Leadership

The global LED lens market exhibits a semi-consolidated competitive structure, characterized by the presence of several established players alongside numerous specialized medium and small enterprises. Ledlink Optics, Carclo Optics, and Auer Lighting collectively command a significant portion of the market, holding an estimated 18% share in 2024. Their leadership is primarily attributed to extensive product portfolios, deep technical expertise in optical design—particularly in Total Internal Reflection (TIR) lenses—and a robust global distribution network that serves diverse applications from automotive lighting to architectural illumination.

LEDIL Oy and FRAEN Corporation are also pivotal contenders, recognized for their innovative solutions and strong foothold in the European and North American markets. These companies consistently focus on research and development to introduce lenses with higher efficiency and better thermal management, catering to the evolving demands of next-generation LED lighting systems. Their growth is further fueled by strategic partnerships with major LED manufacturers and lighting OEMs, ensuring a steady flow of advanced products into the market.

Furthermore, the competitive intensity is escalating as companies aggressively pursue geographical expansion and portfolio diversification. For instance, Asian-based players like ShenZhen Likeda Optical and HENGLI Optical are strengthening their production capabilities and cost-competitive offerings, thereby increasing their influence, particularly in the price-sensitive segments. This dynamic is prompting Western firms to enhance their operational efficiency and innovation cycles to maintain market relevance.

Meanwhile, other significant participants such as GAGGIONE (Lednlight) and Bicom Optics are cementing their positions through specialized, high-performance lenses for niche applications, including medical lighting and entertainment systems. Their strategy involves significant investment in custom solution development and securing intellectual property, which creates high entry barriers for new competitors and ensures sustained growth within their dedicated market niches.

List of Key LED Lens Companies Profiled

- Ledlink Optics (Taiwan)

- Carclo Optics (U.K.)

- Auer Lighting (Germany)

- LEDIL Oy (Finland)

- FRAEN Corporation (U.S.)

- GAGGIONE (Lednlight) (France)

- Bicom Optics (China)

- Darkoo Optics (China)

- Aether systems Inc (U.S.)

- B&M Optics Co., Ltd (China)

- ShenZhen Likeda Optical (China)

- HENGLI Optical (China)

- Brightlx Limited (China)

- Kunrui optical (China)

- FORTECH (China)

- Chun Kuang Optics (Taiwan)

- Wuxi Kinglux Glass Lens (China)

Segment Analysis:

By Type

PMMA LED Lens Segment Commands Significant Market Share Owing to its Superior Optical Clarity and Cost-Effectiveness

The market is segmented based on type into:

- Glass LED Lens

- PMMA LED Lens

- Polycarbonate (PC) LED Lens

- Others (Silicone, ABS, etc)

By Application

Street Lighting Segment Leads the Market Fueled by Global Infrastructure Development and Energy Efficiency Initiatives

The market is segmented based on application into:

- Street Lighting

- Commercial Lighting

- Architectural Lighting

- Indoor Lighting

- Automotive Lighting

- Others

By End User

Municipal and Government Bodies are Key End Users Due to Large-Scale Public Lighting Projects

The market is segmented based on end user into:

- Municipal and Government Bodies

- Commercial Enterprises

- Automotive Manufacturers

- Residential Consumers

- Others

Regional Analysis: LED Lens Market

Asia-Pacific

The Asia-Pacific region dominates the global LED Lens market, accounting for over 45% of total market share by volume. This leadership is primarily driven by China’s massive manufacturing ecosystem, which produces approximately 70% of the world’s LED components. The region benefits from extensive government-led infrastructure modernization projects, including China’s ongoing smart city initiatives and India’s National Street Lighting Programme, which has installed over 12 million LED street lights. While cost-effective PMMA lenses remain prevalent due to price sensitivity in emerging markets, there’s a noticeable shift toward higher-performance polycarbonate and specialized optical-grade materials. Major manufacturing hubs in Shenzhen, Guangzhou, and Taiwan continue to drive innovation while maintaining competitive production costs. The region’s automotive lighting sector is experiencing particularly strong growth, with leading manufacturers expanding production capacities to meet both domestic and international demand.

Europe

Europe represents a sophisticated market characterized by stringent regulatory standards and high adoption of advanced optical technologies. The EU’s Energy Efficiency Directive and Ecodesign requirements have accelerated the transition to high-efficiency LED lighting systems, creating sustained demand for precision optical components. Germany stands as the regional technology leader, hosting several specialized lens manufacturers including Auer Lighting and LEDIL Oy, which focus on high-precision optical solutions for automotive and architectural applications. The market shows strong preference for premium materials like polycarbonate and specialized optical polymers that offer superior durability and optical performance. European manufacturers are increasingly investing in R&D for smart lighting applications and human-centric lighting solutions, driving demand for advanced lens designs that enable precise light control and distribution patterns.

North America

North America’s LED Lens market is characterized by technological innovation and high adoption rates of advanced lighting solutions. The region benefits from strong regulatory support through programs like Energy Star and DesignLights Consortium qualifications, which drive demand for high-performance optical components. The United States represents the largest sub-market, with significant investments in smart city infrastructure and commercial lighting retrofits. The market shows strong preference for durable polycarbonate lenses in outdoor applications and precision optical-grade materials in specialized sectors. Automotive lighting represents a growing segment, with major manufacturers integrating advanced adaptive driving beam systems requiring sophisticated lens arrays. Research institutions and manufacturers are collaborating on next-generation optical designs, particularly for horticultural lighting and UV-C disinfection applications, creating new market opportunities beyond traditional illumination.

South America

South America’s LED Lens market is experiencing gradual growth, primarily driven by infrastructure development projects and increasing energy efficiency awareness. Brazil represents the largest market in the region, with ongoing urban development projects and gradual adoption of LED technology in public lighting systems. The market remains price-sensitive, with PMMA lenses dominating due to their cost-effectiveness and adequate performance for basic applications. However, there’s growing interest in higher-quality optical solutions, particularly in the commercial and architectural lighting segments. Economic volatility and currency fluctuations continue to impact the adoption of advanced optical components, but government initiatives promoting energy efficiency are creating sustained demand for basic LED lighting systems. The region shows potential for growth in specialized applications, particularly in mining and industrial lighting where durability requirements drive demand for robust optical solutions.

Middle East & Africa

The Middle East & Africa region presents an emerging market with significant growth potential, particularly in infrastructure development projects. Gulf Cooperation Council countries, especially the UAE and Saudi Arabia, are leading the adoption of advanced lighting solutions through smart city initiatives and large-scale infrastructure projects. The market shows preference for durable optical materials capable of withstanding extreme environmental conditions, driving demand for high-quality polycarbonate and specialized glass lenses. Africa’s market development is more gradual, with basic PMMA lenses dominating due to cost considerations and developing infrastructure. However, urbanization projects and increasing electrification rates are creating opportunities for market expansion. The region’s unique environmental conditions, including high temperatures and dust exposure, are driving demand for specialized optical solutions with enhanced durability and maintenance-free operation characteristics.

Report Scope

This market research report provides a comprehensive analysis of the global and regional LED Lens markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Lens Market?

-> LED Lens Market was valued at 2041 million in 2024 and is projected to reach US$ 7078 million by 2032, at a CAGR of 19.9% during the forecast period.

Which key companies operate in Global LED Lens Market?

-> Key players include Ledlink Optics, Carclo Optics, Auer Lighting, LEDIL Oy, and FRAEN Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for energy-efficient lighting, urbanization, government regulations promoting LED adoption, and advancements in automotive lighting systems.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 45% of global revenue in 2024, driven by manufacturing hubs in China and increasing infrastructure development.

What are the emerging trends?

-> Emerging trends include miniaturization of lenses, development of smart lighting systems, integration of IoT in lighting solutions, and increased adoption of polycarbonate lenses for lightweight applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...