Market Insights

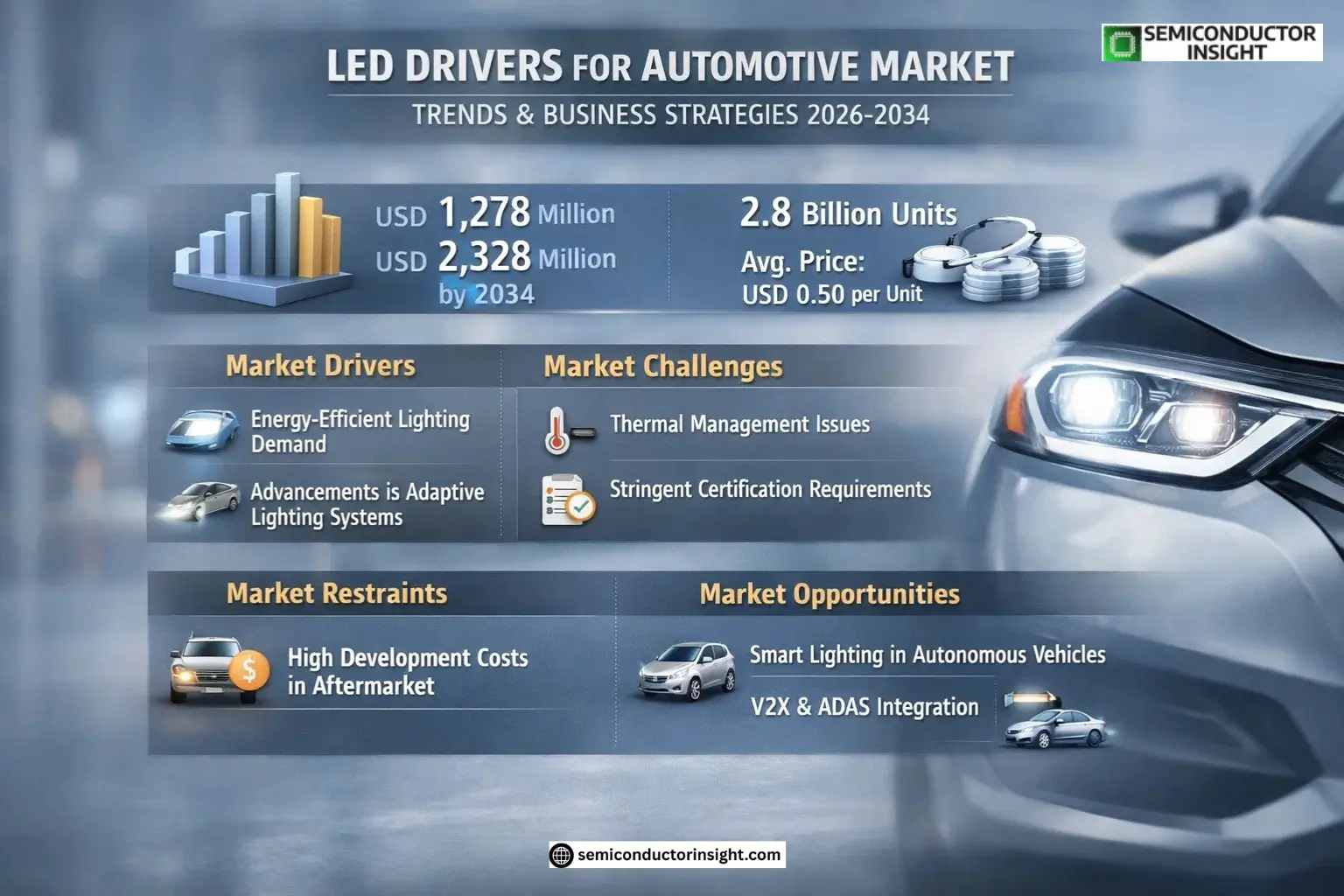

Global LED Drivers for Automotive Market was valued at USD 1,278 million in 2026 and is projected to reach USD 2,328 million by 2034, exhibiting a CAGR of 9.1% during the forecast period.

LED Drivers for Automotive are automotive-grade power management chips designed to precisely regulate current and voltage for various light-emitting diode loads in vehicles. These components enable stable operation, high conversion efficiency, and long-term reliability under wide temperature ranges and complex electrical environments, supporting the safety and consistency requirements of automotive lighting and related display applications. In 2026, production reached approximately 2.8 billion units, with an average price of USD 0.5 per unit.

The market growth is driven by increasing demand for energy-efficient lighting solutions in vehicles and advancements in adaptive headlight technologies. Furthermore, stricter regulatory standards on vehicle safety and energy consumption are accelerating adoption rates across passenger and commercial vehicle segments. Key industry players such as Infineon Technologies, Texas Instruments, and STMicroelectronics continue to innovate with multi-channel driver solutions that integrate diagnostics and thermal management features.

MARKET DRIVERS

Growing Demand for Energy-Efficient Lighting Solutions

The automotive industry’s shift toward energy-efficient lighting technologies is a primary driver for the LED drivers for automotive market. With LED lighting offering up to 80% higher energy efficiency compared to traditional halogen bulbs, automakers are rapidly adopting LED drivers to reduce vehicle power consumption. Regulatory pressures for lower emissions are further accelerating this transition, particularly in Europe and North America.

Advancements in Adaptive Lighting Systems

Intelligent lighting features like adaptive front-lighting systems (AFS) and matrix LED headlights require sophisticated LED drivers for precise control. These technologies enhance nighttime driving safety by automatically adjusting beam patterns, creating a USD 1.2 billion market segment growing at 11.4% annually. Premium automakers are leading adoption, with the technology now trickling down to mass-market vehicles.

Rising consumer preference for premium lighting features and OEM-standard daytime running lights (DRLs) in emerging markets is creating additional growth avenues for automotive LED driver manufacturers.

MARKET CHALLENGES

Thermal Management Complexities

LED drivers for automotive applications must operate reliably across extreme temperature ranges (-40°C to 105°C) while maintaining compact form factors. This requires advanced thermal design capabilities that add 15-20% to component costs compared to consumer-grade drivers, presenting engineering challenges for mass adoption.

Other Challenges

Stringent Automotive Certification Requirements

Compliance with AEC-Q100 qualification standards and ISO 26262 functional safety adds 6-9 months to development cycles. This creates barriers for new entrants in the LED drivers for automotive market.

MARKET RESTRAINTS

High Development Costs Limiting Aftermarket Adoption

Vehicle-specific integration requirements mean LED drivers for automotive applications often require custom development. This results in average unit costs 3-5 times higher than universal LED drivers, restricting adoption in the price-sensitive aftermarket segment which accounts for only 12% of current sales.

MARKET OPPORTUNITIES

Expansion of Smart Lighting in Autonomous Vehicles

The development of autonomous vehicles is creating demand for LED drivers with sophisticated communication capabilities. Future applications include vehicle-to-everything (V2X) lighting systems that project warnings to pedestrians, representing a potential USD 750 million market segment by 2030. Integration with LiDAR and camera systems for advanced driver assistance (ADAS) presents additional growth potential.

LED Drivers for Automotive Market Trends

Rising Demand for Advanced Automotive Lighting Systems

LED Drivers for Automotive Market is experiencing strong growth driven by increasing adoption of advanced lighting technologies in vehicles. With production reaching approximately 2.8 billion units in 2026 and an average price of USD 0.5 per unit, the sector shows significant expansion potential. Market revenue is projected to grow from USD 1,278 million in 2026 to USD 2,328 million by 2034, representing a 9.1% CAGR.

Other Trends

Electrification Driving Integration Requirements

Vehicle electrification trends are accelerating demand for highly integrated LED driver solutions that combine diagnostics, fault protection, and functional safety features. The industry is witnessing a shift toward multi-channel driver architectures capable of supporting intelligent lighting systems while maintaining a 45% average gross margin.

Regional Market Growth Patterns

Asia leads in market share for LED Drivers for Automotive, followed by Europe and North America. China’s strong position reflects both domestic vehicle production growth and the concentration of semiconductor manufacturers. Emerging markets show increased adoption rates as automotive lighting regulations tighten globally.

Technology Segmentation Developments

Product mix shows notable differentiation, with multi-channel drivers gaining share over single-channel variants. By drive type, buck LED drivers maintain dominance due to efficiency advantages, though boost drivers are growing faster in applications requiring higher voltage conversion.

Supplier Landscape Consolidation

Key players like Infineon, Texas Instruments, and NXP continue expanding their automotive-grade portfolios through both organic development and strategic acquisitions. The competitive landscape remains concentrated among semiconductor specialists with automotive qualification expertise, particularly for AEC-Q100 certified solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Positioning and Market Concentration in Automotive LED Driver Segment

LED Drivers for Automotive Market is dominated by established semiconductor manufacturers with specialized automotive-grade IC capabilities. Infineon Technologies and Texas Instruments lead the market with comprehensive portfolios covering single-channel and multi-channel solutions for exterior and interior lighting applications. These players benefit from vertical integration, AEC-Q100 certified production lines, and long-term supply agreements with major automakers. The top 5 companies collectively hold over 45% market share, with design wins in premium lighting systems of European and American OEMs.

Niche specialists like Nuvoton Technology and ROHM Semiconductor have gained traction through optimized solutions for Asian electric vehicle manufacturers, particularly in cost-sensitive segments. Emerging competition comes from analog IC vendors expanding into automotive, such as Analog Devices and Microchip, which are introducing integrated driver+controller solutions. Secondary players focus on regional OEM relationships or specific applications like adaptive headlights and ambient lighting modules.

List of Key LED Drivers for Automotive Companies Profiled

- Infineon Technologies

- Texas Instruments

- NXP Semiconductors

- Renesas Electronics

- STMicroelectronics

- ROHM Semiconductor

- Analog Devices

- ON Semiconductor

- Microchip Technology

- Nuvoton Technology

- Maxim Integrated

- Diodes Incorporated

- Toshiba Electronic Devices

- Melexis

- Elmos Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi-channel drivers are gaining prominence in automotive applications due to:

|

| By Application |

|

Headlight applications dominate due to:

|

| By End User |

|

Premium vehicle segment drives innovation with:

|

| By Drive Type |

|

Boost converters are seeing fastest adoption due to:

|

| By Qualification |

|

AEC-Q100 qualified drivers are essential for:

|

Regional Analysis: LED Drivers for Automotive Market

Asia-Pacific benefits from vertical integration with LED chip manufacturers and automotive Tier-1 suppliers clustered in industrial corridors. This proximity reduces lead times for LED driver implementation in new vehicle models while maintaining cost competitiveness.

Strict vehicle lighting standards across Japan, China and Korea push automakers toward advanced LED driver solutions. Emerging markets are adopting UNECE regulations, creating standardized demand for compliant driver electronics throughout the region.

Regional automakers lead in implementing intelligent LED systems requiring programmable drivers. High demand for premium lighting features in mid-range vehicles creates unique opportunities for cost-optimized driver solutions with advanced functionality.

Growing EV production across China and Southeast Asia drives specialized LED driver development for electric platforms. New requirements for voltage stabilization and thermal management create additional technical challenges addressed by regional suppliers.

Europe

Europe maintains strong demand for high-performance LED drivers due to stringent automotive lighting regulations and premium vehicle concentration. German automakers lead in implementing adaptive LED systems requiring complex driver electronics. The region sees growing integration of LED drivers with vehicle communication networks for smart lighting functionality. Several EU directives promote energy-efficient lighting solutions, benefiting intelligent LED driver adoption. Established automotive supplier networks facilitate rapid technology transfer from luxury to mass-market segments.

North America

The North American market prioritizes rugged LED driver solutions capable of operating in extreme weather conditions. US and Canadian regulators emphasize glare reduction, pushing advanced driver-controlled beam shaping technologies. Significant R&D focuses on thermal management solutions for high-power LED arrays in trucks and SUVs. Regional automakers collaborate with semiconductor firms to develop application-specific driver ICs, creating differentiated product offerings.

South America

South America shows growing LED driver adoption driven by Brazilian vehicle safety regulations and Argentine aftermarket upgrades. Economic constraints favor cost-effective driver solutions with basic functionality over premium features. The region benefits from technology spillover from global automakers’ local production facilities, though adoption lags behind more developed markets.

Middle East & Africa

The MEA region experiences steady LED driver growth, primarily in Gulf Cooperation Council countries with luxury vehicle concentrations. Harsh environmental conditions necessitate robust driver designs with enhanced thermal protection. African markets show potential with gradual vehicle electrification and urbanization driving demand for modern lighting solutions, though infrastructure challenges persist.

Report Scope

This market research report provides a comprehensive analysis of the LED Drivers for Automotive Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of LED Drivers for Automotive Market?

-> LED Drivers for Automotive Market was valued at USD 1,278 million in 2026 and is projected to reach USD 2,328 million by 2034, exhibiting a CAGR of 9.1% during the forecast period.

What was the production volume of LED Drivers for Automotive in 2026?

-> Production reached approximately 2.8 billion units in 2026, with an average price of USD 0.5 per unit.

Which key companies operate in LED Drivers for Automotive Market?

-> Key players include Infineon Technologies, Texas Instruments, NXP, Renesas Electronics, STMicroelectronics, ROHM, Analog Devices, ON Semiconductor, Microchip, and Nuvoton Technology Corporation.

What are the key applications of LED Drivers for Automotive?

-> Major applications include headlights, taillights, daytime running lights, adaptive headlights, matrix lighting, ambient lighting, backlit displays, and indicator modules in passenger cars and commercial vehicles.

What are the key growth drivers for this market?

-> Growth is driven by rising vehicle electrification, increasing adoption of advanced lighting systems, regulatory requirements for lighting performance, and integration of intelligent, software-controlled lighting subsystems.

Which region dominates the LED Drivers for Automotive Market?

-> Asia holds significant market share, with key countries including China, Japan, South Korea, and India, due to strong automotive manufacturing presence.

What is the industry capacity utilization rate and gross margin?

-> In 2026, the industry capacity utilization rate was about 63%, with an average gross margin around 45%.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...