MARKET INSIGHTS

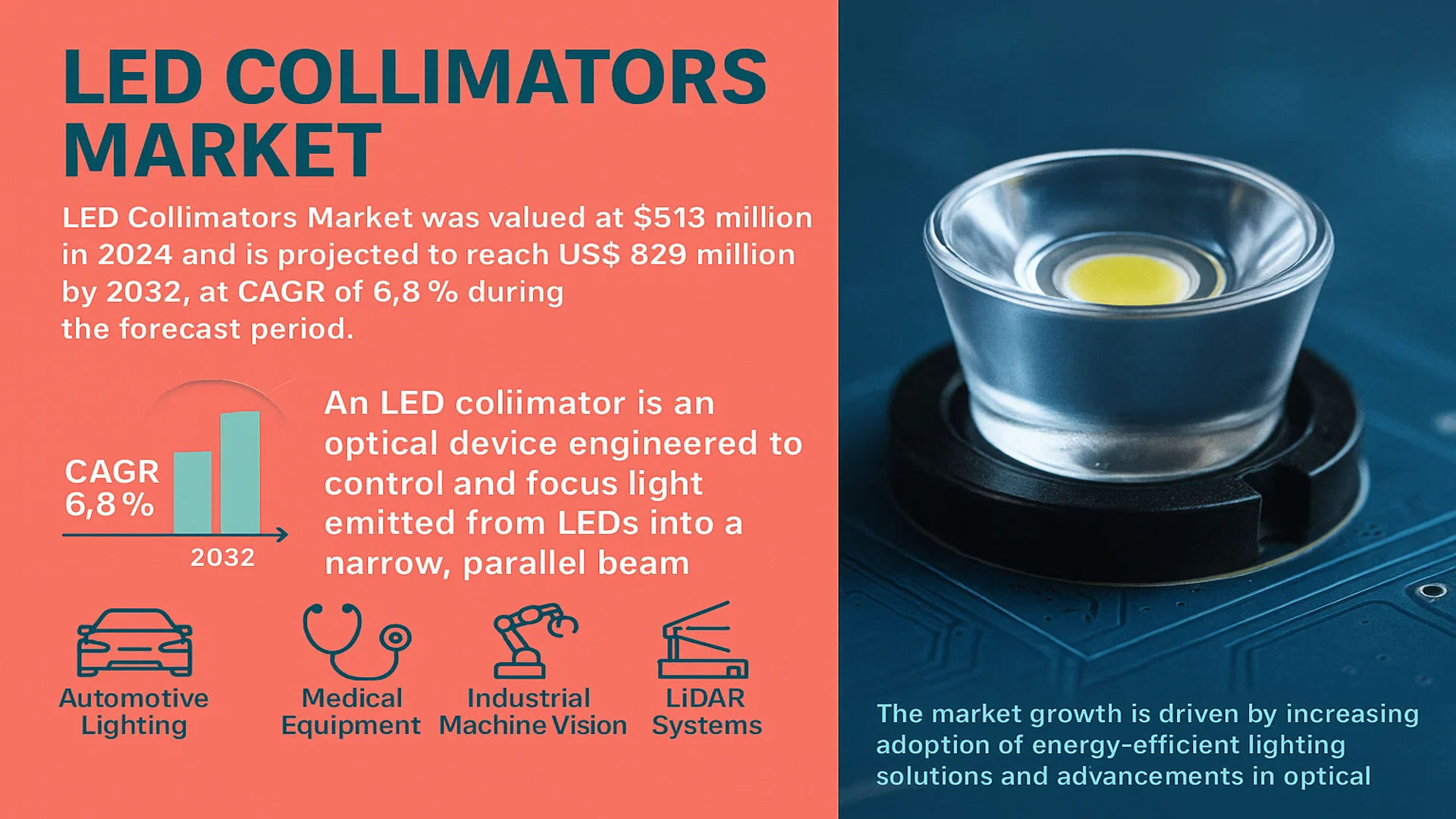

The global LED Collimators Market was valued at 513 million in 2024 and is projected to reach US$ 829 million by 2032, at a CAGR of 6.8% during the forecast period.

An LED collimator is an optical device engineered to control and focus light emitted from LEDs into a narrow, parallel beam. These components enhance light directionality by minimizing divergence, which improves efficiency and precision in applications requiring controlled illumination. LED collimators find extensive use across industries such as automotive lighting, medical equipment, industrial machine vision, LiDAR systems, and advanced display technologies.

The market growth is driven by increasing adoption of energy-efficient lighting solutions and advancements in optical technologies. While automotive applications dominate current usage, emerging sectors like augmented reality and smart displays present new opportunities. The U.S. currently holds the largest market share, though Asia-Pacific regions are experiencing accelerated growth due to expanding electronics manufacturing capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Energy-Efficient Lighting Solutions to Propel Market Growth

The global shift towards energy-efficient lighting solutions is a primary driver for the LED collimators market. LED technology, known for its high efficiency and long lifespan, has gained widespread adoption across multiple industries. Collimators enhance LED performance by optimizing light directionality and minimizing energy wastage through scattered light. Governments worldwide are implementing stringent regulations to phase out inefficient lighting systems, further accelerating demand. For instance, policies promoting LED adoption in street lighting and commercial buildings have increased the need for precision optical components like collimators to maximize energy savings.

Expansion of Automotive Lighting Applications to Boost Adoption

The automotive sector represents a significant growth area for LED collimators, particularly with the rising integration of advanced lighting systems in modern vehicles. Manufacturers are increasingly adopting LED-based headlights, daytime running lights, and interior lighting due to their superior brightness and efficiency. Collimators play a crucial role in shaping light beams for optimal visibility and safety compliance. The global automotive lighting market, valued at over $30 billion, continues to expand with advancements in adaptive driving beam (ADB) systems, where collimators help achieve precise light distribution. This trend is expected to persist with the growing production of electric vehicles, which prioritize energy-efficient components.

Additionally, the proliferation of LiDAR technology in autonomous vehicles is creating new opportunities for high-precision collimators. Modern LiDAR systems rely on precisely controlled light beams for accurate object detection, driving innovation in collimator design for specialized automotive applications.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Design Requirements Limit Market Penetration

Despite strong demand, the LED collimators market faces significant barriers due to high production costs and technical complexities. Precision manufacturing requirements for optical-grade materials like borosilicate glass and specialized polymers increase expenses. The process often involves advanced fabrication techniques such as diamond-point turning for achieving micron-level accuracy in surface profiles. These factors contribute to higher product costs, particularly for customized collimators designed for niche applications. Small and medium enterprises find it challenging to compete in this landscape dominated by established optical component manufacturers with specialized production capabilities.

Supply Chain Vulnerabilities Impact Product Availability

The global semiconductor shortage and disruptions in raw material supply chains have affected LED collimator production timelines and costs. Key materials like optical-grade silica and rare-earth elements used in advanced collimators face price volatility and geopolitical supply risks. Manufacturers must navigate these challenges while maintaining the stringent quality standards required for optical components. Recent trade restrictions on specialized glass and ceramic materials have further complicated sourcing strategies, potentially delaying product development cycles and constraining market growth in price-sensitive segments.

MARKET OPPORTUNITIES

Emerging Applications in Medical Technology Create New Growth Avenues

The healthcare sector presents substantial untapped potential for LED collimators, particularly in diagnostic and therapeutic applications. Advanced medical imaging systems, surgical lighting, and phototherapy devices increasingly incorporate LED-based solutions that require precise light control. The global medical lighting market is projected to maintain steady growth, driven by technological advancements and healthcare infrastructure development worldwide. Collimators enable uniform illumination and specific wavelength delivery critical for procedures like endoscopy and dermatological treatments. Additionally, the rising adoption of UV-C LED systems for sterilization applications creates demand for specialized collimators that optimize germicidal light distribution.

Integration with Smart Lighting Systems Opens Commercial Opportunities

The convergence of IoT technologies with lighting systems is transforming commercial and industrial applications of LED collimators. Smart buildings increasingly incorporate adaptive lighting solutions that dynamically adjust brightness and beam patterns based on occupancy and natural light conditions. These systems require advanced optical components to achieve precise light control while maintaining energy efficiency. The growing smart cities initiative across various countries further amplifies this opportunity, with intelligent street lighting projects driving demand for ruggedized, weather-resistant collimators capable of long-term outdoor performance.

MARKET CHALLENGES

Intense Competition from Alternative Lighting Technologies

While LED technology dominates many lighting applications, alternative light sources continue to challenge market growth in specific segments. Laser diodes, for instance, offer superior beam control in some industrial applications, potentially reducing the need for collimators. Organic LEDs (OLEDs) provide naturally diffused light that may reduce dependency on optical components for certain display applications. The rapid pace of innovation in lighting technologies creates a competitive landscape where collimator manufacturers must continually enhance their products to maintain relevance across evolving applications.

Thermal Management Requirements Constrain Design Flexibility

High-power LED applications generate significant heat that can degrade optical performance and reduce component lifespan. Collimators designed for these applications often require integrated thermal management solutions, increasing product complexity and cost. The need to maintain precise optical alignment under varying thermal conditions presents ongoing engineering challenges. As LEDs continue to achieve higher lumen outputs, thermal considerations will remain a critical factor in collimator design, particularly for automotive and industrial applications where reliability is paramount.

LED COLLIMATORS MARKET TRENDS

Rising Demand for High-Efficiency Lighting Solutions Drives LED Collimator Adoption

The global LED collimators market is experiencing robust growth, projected to expand from $513 million in 2024 to $829 million by 2032, reflecting a 6.8% CAGR. This surge is primarily driven by increasing demand for energy-efficient lighting solutions across automotive, medical, and industrial sectors. Automotive applications currently dominate, accounting for nearly 35% of market share, as manufacturers incorporate LED collimators to enhance headlight performance while meeting stringent energy regulations. In medical lighting, precision-focused collimators enable advanced surgical lighting systems, supporting the $12 billion medical device lighting market. The transition from conventional lighting to narrow-beam LED solutions is accelerating as manufacturers prioritize light uniformity and thermal management.

Other Trends

Advancements in Optical Design

Material science innovations are enabling thinner, more durable collimator lenses with 94-96% light transmission efficiency, compared to 88-90% in previous generations. Freeform optics now allow customized beam shaping for specialized applications like LiDAR systems, where collimator precision directly impacts scanning resolution. Meanwhile, hybrid polymer-glass composites reduce weight by 20-30% in automotive applications while maintaining high-temperature stability up to 120°C. These improvements are particularly crucial for emerging sectors such as augmented reality displays, where compact form factors require millimeter-scale collimation precision.

Regional Manufacturing Shifts Reshape Supply Chains

While China maintains dominance in LED component production with 60-65% global market share, manufacturers are establishing alternative supply chains to mitigate geopolitical risks. Southeast Asian facilities now produce 18-22% of mid-range collimators, focusing on automotive tier-2 suppliers. Meanwhile, North American reshoring initiatives have boosted local production by 8-10% annually since 2022, particularly for defense and aerospace-grade optical components requiring ITAR compliance. This geographical diversification coincides with tighter tolerances in industrial standards, where new ANSI/IESNA RP-16-05 specifications demand ±1° beam angle consistency for professional-grade luminaires.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Innovation and Strategic Expansions to Gain Market Share

The global LED collimators market features a dynamic competitive landscape characterized by both established manufacturers and emerging players. Ledlink Optics Inc. stands as a dominant force, known for its cutting-edge optical solutions and extensive applications in automotive and industrial lighting. The company holds a strong position due to its vertically integrated manufacturing capabilities and continuous R&D investments.

LEDIL Oy and Fraen Corporation also command substantial market shares, particularly in the narrow-beam and medium-beam collimator segments. Their growth stems from partnerships with high-power LED manufacturers and expansion into high-growth regions such as Asia-Pacific.

While some companies focus on enhancing product portfolios through innovation, others are adopting acquisition strategies to broaden their technological expertise. For instance, Carclo Technical Plastics has strengthened its position by acquiring smaller optical component manufacturers to expand its LED collimation solutions.

Meanwhile, Nichia Corporation and OSRAM Opto Semiconductors GmbH are integrating collimators directly into their LED packages, offering compact, high-performance lighting solutions. This vertical integration allows them to cater to industries requiring precision optics, such as medical devices and LiDAR systems.

List of Key LED Collimator Manufacturers

- Ledlink Optics Inc. (Taiwan)

- LEDIL Oy (Finland)

- Fraen Corporation (U.S.)

- Carclo Technical Plastics (U.K.)

- Nichia Corporation (Japan)

- OSRAM Opto Semiconductors GmbH (Germany)

- Dialight PLC (U.K.)

- Bivar Inc. (U.S.)

- Lumileds Holding B.V. (Netherlands)

Segment Analysis:

By Type

Reflective LED Collimators Lead Market Share Due to Superior Beam Control and Efficiency

The market is segmented based on type into:

- Reflective LED Collimators

- Subtypes: Parabolic, Elliptical, and others

- Refractive LED Collimators

- TIR (Total Internal Reflection) Collimators

- Hybrid LED Collimators

- Others

By Application

Automotive Lighting Segment Holds Largest Revenue Share Due to Increasing Adoption in Headlights and Signal Systems

The market is segmented based on application into:

- Automotive Lighting

- Medical Devices

- Machine Vision

- Optical Instruments

- Display Technology

By End User

Consumer Electronics and Automotive OEMs Drive Market Growth

The market is segmented based on end user into:

- Automotive OEMs

- Consumer Electronics Manufacturers

- Medical Device Companies

- Industrial Equipment Manufacturers

- Research Institutes

Regional Analysis: LED Collimators Market

Asia-Pacific

The Asia-Pacific region dominates the LED collimators market, driven by rapid industrialization, urbanization, and significant investments in automotive and consumer electronics sectors. China leads the regional growth, contributing over 40% of the global demand due to its robust manufacturing ecosystem for LEDs and optical components. Countries like Japan and South Korea are also key players, fueled by advancements in automotive lighting and smart display technologies. The increasing adoption of LiDAR in autonomous vehicles and government initiatives supporting energy-efficient lighting solutions further propel the market. India presents substantial opportunities with its expanding infrastructure projects and rising demand for precision lighting in medical and industrial applications. However, price sensitivity remains a challenge, pushing manufacturers to balance cost and performance.

North America

North America is a high-growth region for LED collimators, with the U.S. accounting for the largest share. The market is driven by stringent regulations on energy efficiency, particularly in automotive and industrial lighting applications. The growing adoption of narrow beam collimators for medical devices, such as surgical lighting and diagnostic equipment, supports market expansion. Additionally, the U.S. defense sector leverages LED collimators for advanced optical systems, including LiDAR and targeting applications. Technological innovation and strong R&D investments in photonics and optoelectronics solidify North America as a leader in high-performance collimator solutions.

Europe

Europe’s LED collimators market is characterized by a strong emphasis on sustainability and precision engineering. The region benefits from strict regulations promoting energy-efficient lighting, particularly in automotive and architectural applications. Germany, France, and the UK are at the forefront, with increasing demand for collimators in automotive adaptive front-lighting systems (AFS) and machine vision technologies. The medical sector also contributes significantly, with rising use in endoscopy and laser-based treatments. Sustainability-driven policies and corporate investments in green technologies amplify the demand for high-efficiency collimators, though competition from Asia-Pacific suppliers remains a challenge.

South America

South America represents a developing market for LED collimators, with growth primarily concentrated in Brazil and Argentina. The automotive lighting segment is expanding due to rising vehicle production and modernization. However, the market faces hurdles such as economic instability and lower adoption rates of advanced optical technologies compared to other regions. Industrial applications, including machine vision and barcode scanning, present niche opportunities, but limited local manufacturing capabilities result in reliance on imports. Despite these challenges, gradual infrastructure improvements and urbanization signal long-term potential for market growth.

Middle East & Africa

The Middle East & Africa market for LED collimators is nascent but growing, driven by infrastructure projects and increasing focus on smart city initiatives. The UAE and Saudi Arabia lead the region in adopting high-performance lighting solutions for architectural and automotive applications. In Africa, South Africa shows emerging demand for LED collimators in industrial and medical sectors. However, market expansion is hampered by limited technical expertise and reliance on imported components. With rising investments in renewable energy and smart technologies, the region holds untapped potential for future development.

Report Scope

This market research report provides a comprehensive analysis of the global LED Collimators market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global LED Collimators market was valued at USD 513 million in 2024 and is projected to reach USD 829 million by 2032, growing at a CAGR of 6.8%.

- Segmentation Analysis: Detailed breakdown by product type (narrow beam, medium beam, wide beam), technology (reflector-based, lens-based), application (automotive lighting, medical devices, LiDAR, machine vision), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with significant growth expected in Asia-Pacific.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, including advanced optical materials, miniaturization, and integration with smart lighting systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Collimators Market?

-> LED Collimators Market was valued at 513 million in 2024 and is projected to reach US$ 829 million by 2032, at a CAGR of 6.8% during the forecast period.

Which key companies operate in Global LED Collimators Market?

-> Key players include Ledil Oy, Fraen Corporation, Carclo Optics, Ledlink Optics, and Auer Lighting, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient lighting, increasing adoption in automotive applications, and advancements in optical technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China’s manufacturing capabilities, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include hybrid collimator designs, smart lighting integration, and increasing use in LiDAR for autonomous vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...