MARKET INSIGHTS

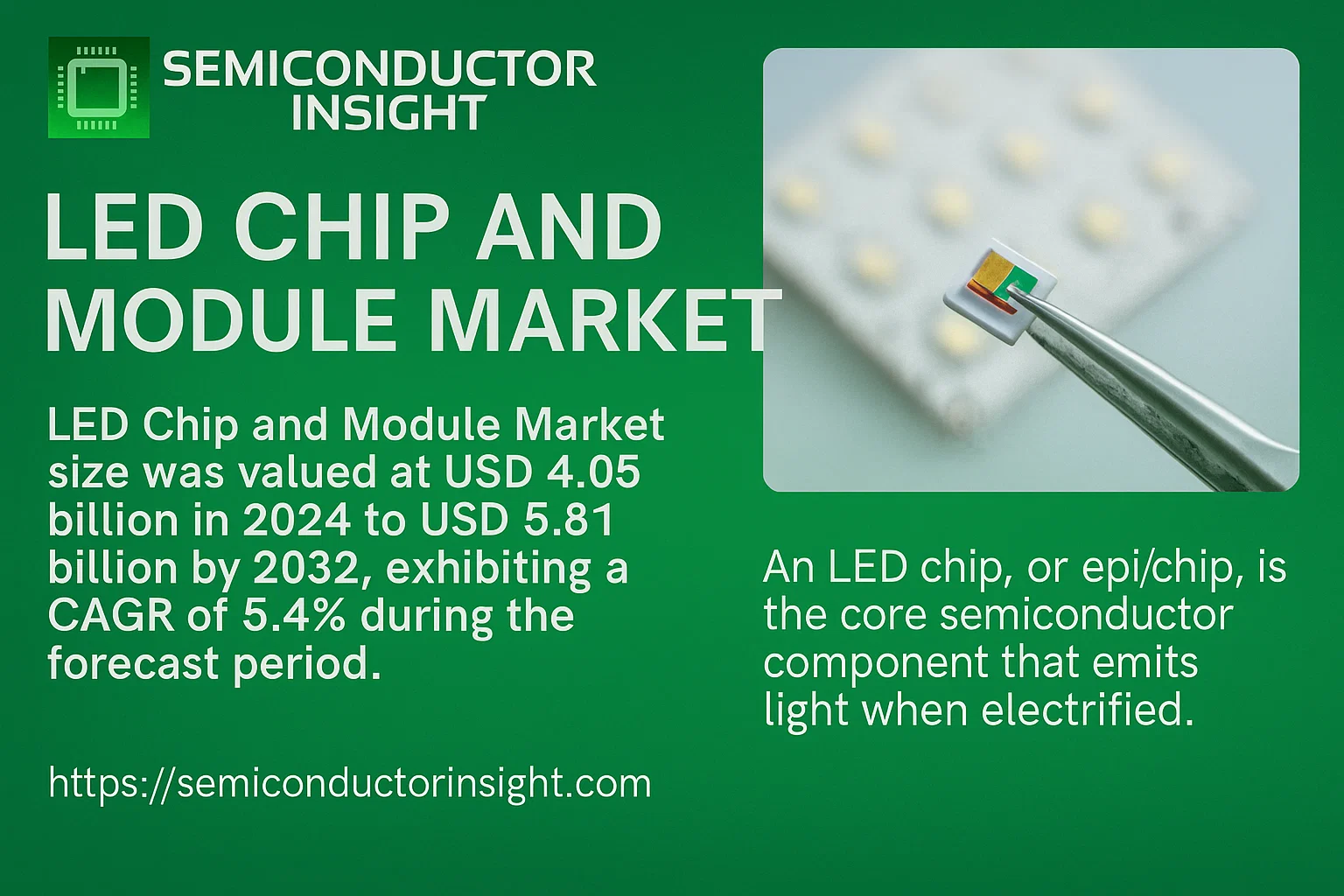

Global LED Chip and Module Market size was valued at USD 4.05 billion in 2024 to USD 5.81 billion by 2032, exhibiting a CAGR of 5.4% during the forecast period.

An LED chip, or epi/chip, is the core semiconductor component that emits light when electrified. Its production involves epitaxy, a critical and capital-intensive process using MOCVD to deposit crystalline layers on a wafer, which is then diced into individual chips. An LED module, often called a light engine, integrates one or more LED packages with essential components like secondary optics, a heat sink, and an electrical driver on a printed circuit board (PCB) to create a functional lighting unit.

The market is experiencing steady growth driven by the global transition to energy-efficient lighting and supportive government regulations phasing out incandescent bulbs. Furthermore, rising adoption across key applications such as general lighting, automotive headlights, and backlighting for displays is contributing to market expansion. The competitive landscape is concentrated; for instance, the top four playersSan’an Opto, ETI, HC Semi Tek, and Lattice Power collectively hold 77% of the global market share. Europe currently leads as the largest consumption region, accounting for nearly 27% of the market.

MARKET DRIVERS

Global Push Towards Energy Efficiency

Stringent government regulations and policies worldwide, such as the EU’s Ecodesign Directive and energy labeling requirements, are phasing out inefficient lighting technologies. This regulatory push is a primary driver for the adoption of energy-efficient LED chips and modules. The superior lumens-per-watt performance of LEDs compared to traditional lighting solutions is leading to significant energy savings for commercial, industrial, and residential users.

Rising Demand in General Lighting and Automotive Applications

The transition to LED technology in general lighting remains a massive growth driver. Furthermore, the automotive industry is rapidly adopting LEDs for headlights, daytime running lights (DRLs), interior lighting, and advanced applications like adaptive driving beams. The demand for mini-LEDs and micro-LEDs for high-resolution displays in consumer electronics, including televisions, laptops, and augmented/virtual reality devices, is creating substantial market momentum.

➤ Global LED market is projected to grow at a CAGR of over 9% from 2024 to 2030, fueled by these expanding applications.

Technological advancements are also a key driver. Innovations in chip design, such as flip-chip LEDs and Chip-Scale Packaging (CSP), are improving performance, reliability, and thermal management, allowing for brighter and more compact lighting solutions.

MARKET CHALLENGES

Intense Price Competition and Margin Pressure

LED Chip and Module Market is highly competitive, characterized by the presence of numerous global and regional players. This leads to intense price competition, which squeezes profit margins for manufacturers. While material costs have stabilized, the pressure to reduce prices remains a significant challenge, particularly for standard, mass-produced components.

Other Challenges

Technological Complexity and High R&D Costs

Continuous innovation is required to stay competitive, necessitating substantial investments in research and development for next-generation technologies like micro-LEDs, which involve complex manufacturing processes and high initial capital expenditure.

Supply Chain Vulnerabilities

The industry relies on a global supply chain for raw materials (e.g., gallium nitride substrates, phosphors) and semiconductor components. Geopolitical tensions, trade disputes, and logistical disruptions can lead to supply shortages and price volatility, impacting production schedules and costs.

MARKET RESTRAINTS

Market Saturation in Mature Segments

The market for basic LED lighting in some developed regions is approaching saturation, leading to slower growth rates. The replacement cycle for LED products is also much longer than for traditional lighting, which limits repeat sales in the general lighting segment once market penetration is high.

Technical Limitations for High-End Applications

Despite advancements, technical challenges such as “droop” (efficiency loss at high current densities) and heat dissipation issues at extremely high brightness levels can restrain performance in demanding applications like high-power automotive headlights and ultra-high-brightness displays. The high cost and manufacturing yield issues associated with micro-LEDs also restrain their mass-market adoption.

MARKET OPPORTUNITIES

Expansion in Smart Lighting and IoT Integration

The integration of LED modules with sensors, connectivity chips, and smart controls is creating a significant growth avenue. The rise of smart homes, smart cities, and connected commercial buildings drives demand for intelligent LED lighting systems that offer energy management, data collection, and enhanced user experiences.

Emerging Applications in Horticulture and Health

There is growing adoption of specialized LED modules for horticultural lighting, enabling year-round, controlled-environment agriculture. Furthermore, research into human-centric lighting (HCL), which uses tunable LEDs to impact circadian rhythms and well-being, opens new markets in healthcare, offices, and residential settings.

Advancements in UV-C LED Technology

The development of UV-C LEDs for disinfection and purification applications presents a major opportunity. Demand surged post-pandemic for air, surface, and water sterilization in healthcare, public spaces, and consumer products, driving innovation and commercialization in this niche segment.

LED Chip and Module Market Trends

Sustained Market Growth Driven by Energy Efficiency Demands

Global LED Chip and Module Market is on a steady growth trajectory, with valuation projected to increase from over US$ 4 billion in 2024 to nearly US$ 5.8 billion by 2032, representing a compound annual growth rate of 5.4%. This expansion is primarily fueled by the global push for energy efficiency and the continued phase-out of traditional incandescent and fluorescent lighting. Government regulations and incentives promoting sustainable technologies are creating a robust demand environment across both consumer and industrial sectors.

Other Trends

Advancements in Chip and Module Manufacturing

The manufacturing process remains highly specialized, with the epitaxy stage being the most critical and capital-intensive. This process involves depositing epitaxial layers on a wafer substrate using Metal-Organic Chemical Vapor Deposition (MOCVD). The quality of the epi/chip, particularly its efficacy, varies significantly depending on the target application, such as general lighting, automotive, or backlighting. Module production then integrates these chips with essential components like secondary optics, heat sinks, and drivers onto a printed circuit board to create a complete light engine optimized for performance.

Market Consolidation and Regional Dynamics

The market structure is characterized by a high degree of concentration, with the top four playersSan’an Opto, ETI, HC SemiTek, and Lattice Powercollectively holding a dominant market share of approximately 77%. This consolidation highlights the significant barriers to entry posed by the technological expertise and capital investment required. Geographically, Europe stands as the largest consumption region, accounting for nearly 27% of the global market, driven by stringent energy regulations and high adoption rates of LED technology.

Application-Specific Segmentation and Future Outlook

The market is distinctly segmented by chip typeLateral, Vertical, and Flip Chipeach offering different performance characteristics for various applications. Key application areas include General Lighting, which represents the largest segment, followed by Automotive Lighting and Backlighting for displays. The analysis indicates that future growth will be closely tied to innovation in these application segments, with automotive lighting and smart, connected lighting systems presenting significant blue ocean opportunities for manufacturers who can meet the evolving technical and efficiency requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Dominated by a Few Vertically Integrated Giants

Global LED Chip and Module Market is characterized by a high concentration of power, with the top four playersSan’an Opto, ETI, HC SemiTek, and Lattice Powercollectively commanding approximately 77% of the market share by revenue. These companies are highly vertically integrated, controlling the critical and capital-intensive epitaxy process (using MOCVD technology) through to module (light engine) assembly. This control over the core manufacturing value chain, from wafer to finished component, provides significant economies of scale, technological advantages, and pricing power, creating high barriers to entry for new competitors. Europe stands as the largest consumption region, holding nearly 27% of the market, which further solidifies the global reach and strategic importance of these leading players.

Beyond the market leaders, the landscape includes several other significant players that compete effectively through technological specialization, strong regional presence, or focus on high-value application niches. Companies like Epistar, Osram, Seoul Semiconductor, and Cree (now part of SMTC) are renowned for their innovation in high-brightness and specialty LEDs for applications such as automotive lighting, display backlighting, and advanced general lighting. Other manufacturers, including Nichia, Samsung, and LG Innotek, leverage their vast corporate resources and technological expertise to maintain a strong foothold. These and other companies profiled below contribute to a dynamic and competitive environment, driving continuous advancements in efficacy, reliability, and cost-effectiveness across various LED types like Lateral, Vertical, and Flip Chips.

List of Key LED Chip and Module Companies Profiled

- Epistar

- San’an Opto

- Cree (Wolfspeed)

- OSRAM

- Samsung

- Toyoda Gosei

- Seoul Semiconductor

- Philips Lumileds

- ETI

- LG Innotek

- NiChia

- HC SemiTek

- Lextar

- Lattice Power

- OPTO-TECH

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Flip Chip technology is increasingly prominent due to its superior thermal management and enhanced light extraction efficiency, which are critical for high-power applications. This architecture allows for better reliability and a smaller footprint compared to traditional Lateral Chip designs, making it highly favored in advanced lighting solutions. The evolution towards Flip Chip reflects the industry’s drive for higher performance and miniaturization, although Lateral Chip remains important for cost-sensitive applications where the highest efficacy is not the primary driver. The transition is supported by ongoing manufacturing refinements that address initial yield challenges. |

| By Application |

|

General Lighting represents the core application segment, driven by the global transition from traditional lighting to energy-efficient LED solutions in residential, commercial, and industrial sectors. This demand is underpinned by continuous improvements in luminous efficacy, color quality, and lifespan, along with supportive regulatory policies. The market’s maturity fosters intense competition, pushing innovation in module design for better thermal management and driver integration. While Automotive Lighting is a high-growth niche with stringent performance requirements, and Backlighting faces saturation in certain display markets, General Lighting’s vast and diverse application base ensures its sustained leadership. |

| By End User |

|

Commercial & Industrial end users are the dominant force, driven by large-scale retrofitting projects and new construction that prioritize energy savings and operational longevity. This segment demands robust modules capable of extended operation in demanding environments, leading to innovations in heat dissipation and driver reliability. While the Residential segment is significant and benefits from smart lighting integration trends, its adoption cycle is typically slower. Automotive OEMs represent a highly specialized segment with rigorous quality and performance standards, but their volume is eclipsed by the broad-based demand from commercial infrastructure and industrial facilities worldwide. |

| By Performance Tier |

|

High Efficacy products are the leading segment, as they offer the optimal balance between performance improvements and cost considerations for the majority of lighting applications. This tier meets the growing demand for significant energy savings without the premium price associated with cutting-edge Ultra-High Efficacy chips, which are often reserved for specialized applications where maximum light output is critical. The Standard Efficacy segment remains relevant for cost-sensitive markets, but the industry’s trajectory is firmly oriented towards higher performance. Continual advancements in epitaxial growth and chip architecture are steadily pushing the performance boundaries, making higher efficacy levels more accessible. |

| By Integration Level |

|

Integrated Modules (Light Engines) are the leading segment, as they provide a complete, application-optimized solution that simplifies fixture manufacturing for lighting OEMs. These modules combine chips, optics, thermal management, and drivers into a single unit, offering superior performance consistency and reliability. While Discrete Chips offer design flexibility for specialized applications, they require significant engineering expertise from the fixture maker. Chip-on-Board technology is strong in high-lumen compact sources but is often incorporated within a broader module. The trend towards Integrated Modules reflects the market’s desire for plug-and-play solutions that accelerate time-to-market and ensure optimal performance. |

Regional Analysis: LED Chip and Module Market

Asia-Pacific

The region’s strength lies in its vertically integrated supply chains, from raw wafer production to final module assembly. This integration allows for tight quality control, reduced production lead times, and significant cost efficiencies, making it the primary global sourcing hub for LED components across various applications, from general lighting to backlight units.

While China leads in volume, Japan and South Korea are centers for cutting-edge innovation. They pioneer developments in mini-LED and micro-LED technologies, which are critical for next-generation displays in smartphones, televisions, and augmented reality devices, giving the region a competitive edge in high-value market segments.

Supportive government policies, including subsidies for energy-efficient products and stringent regulations phasing out incandescent bulbs, have created a fertile ground for market growth. These policies not only stimulate local demand but also encourage local manufacturers to invest in advanced production capabilities and expand their global footprint.

The market’s dynamism is fueled by a wide array of applications. Beyond traditional lighting, demand is soaring from the automotive sector for adaptive headlights, the consumer electronics industry for display backlighting, and the horticulture sector for specialized grow lights, ensuring sustained and diversified growth drivers within the region.

North America

North America represents a significant and technologically advanced market for LED chips and modules, characterized by high adoption rates of energy-efficient solutions and a strong focus on innovation. The United States is the key driver, with stringent energy regulations and a mature infrastructure for smart city projects fueling demand for intelligent lighting systems. The presence of major automotive manufacturers and a robust consumer electronics industry creates substantial demand for high-performance LEDs used in automotive lighting and premium displays. The market is also influenced by a growing emphasis on human-centric lighting and connected IoT-enabled lighting solutions in commercial and residential buildings.

Europe

The European market is defined by its rigorous regulatory framework and early adoption of sustainability standards, which strongly favor LED technology. The region demonstrates high demand for high-quality, durable LED modules, particularly in the architectural, industrial, and outdoor lighting sectors. Countries like Germany and the Netherlands are hubs for horticultural lighting research, driving demand for specialized LED chips. The European automotive industry’s shift towards electric vehicles and advanced lighting systems, including matrix LED headlights, provides a steady stream of opportunities for module suppliers emphasizing quality and technological sophistication.

South America

The LED Chip and Module Market in South America is in a growth phase, propelled by increasing urbanization and infrastructure modernization projects, particularly in Brazil and Argentina. The primary demand originates from the general lighting segment as governments and businesses seek to reduce energy consumption. While the market is less technologically mature compared to other regions, it offers significant potential. Growth is tempered by economic volatility and a reliance on imported components, but local manufacturing initiatives are gradually emerging to cater to the expanding regional demand for basic to mid-range LED products.

Middle East & Africa

This region presents a market with high growth potential, largely driven by massive infrastructure development, urbanization megaprojects, and the need for energy conservation in Gulf Cooperation Council countries. The demand for LED modules is strong in outdoor lighting, architectural lighting, and retail applications. Africa’s market is emerging, with growth centered on off-grid solar-powered LED lighting solutions, addressing the need for electricity access. The market is price-sensitive, but there is a growing appreciation for quality and longevity, creating opportunities for suppliers who can balance cost-effectiveness with reliability.

Report Scope

This market research report provides a comprehensive analysis of the Global LED Chip and Module Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of LED Chip and Module Market?

-> LED Chip and Module Market size was valued at USD 4.05 billion in 2024 to USD 5.81 billion by 2032, exhibiting a CAGR of 5.4% during the forecast period.

Which key companies operate in LED Chip and Module Market?

-> Key players include Epistar, San’an Opto, Cree, OSRAM, Samsung, Toyoda Gosei, Seoul Semiconductor, Philips Lumileds, ETI, LG Innotek, NiChia, HC SemiTek, Lextar, Lattice Power, OPTO-TECH, Tyntek, Genesis Photonics, Formosa Epitaxy, Changelight, Aucksun, and TongFang.

What are the key segments of the LED Chip and Module Market?

-> The market is segmented by Type (Lateral Chip, Vertical Chip, Flip Chip) and by Application (General Lighting, Automotive Lighting, Backlighting).

Which region dominates the market?

-> Europe is the largest consumption region, holding a market share of nearly 27%.

What is the most critical step in LED manufacturing?

-> Creating the epitaxial layers is the most critical and capital-intensive step in LED manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...