LCD Driver IC Tester Market Insights

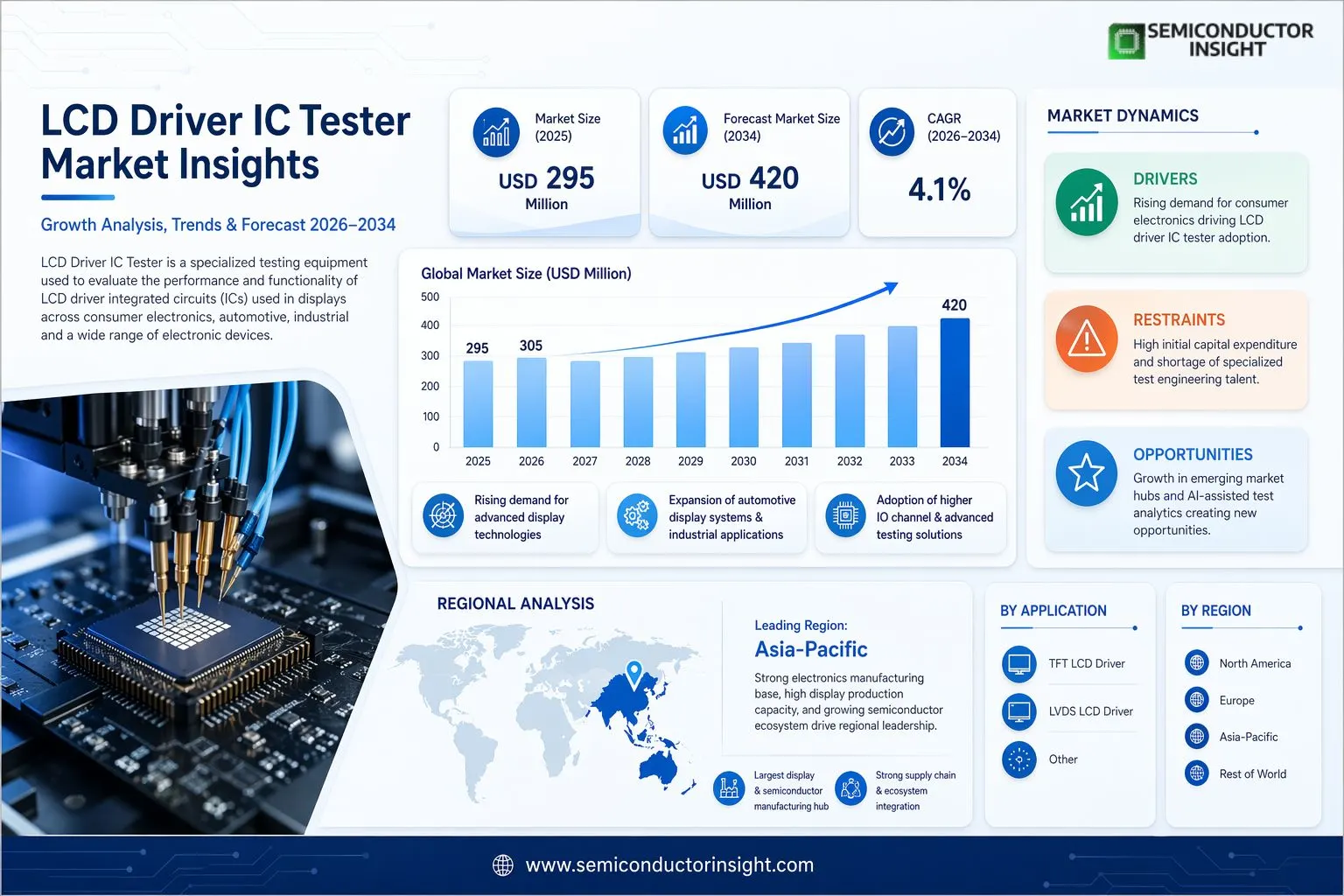

Global LCD Driver IC Tester market size was valued at USD 295 million in 2025. The market is projected to grow from USD 305 million in 2026 to USD 420 million by 2034, exhibiting a CAGR of 4.1% during the forecast period.

An LCD Driver IC Tester is a specialized testing equipment used to evaluate the performance and functionality of LCD driver integrated circuits (ICs). LCD driver ICs are key components in displays, responsible for controlling the voltage and timing necessary to drive liquid crystal displays (LCDs). These ICs play a critical role in the proper functioning of displays across various applications, including smartphones, televisions, monitors, automotive dashboards, and a broad range of consumer and industrial electronic devices.

The market is witnessing steady growth driven by the expanding global demand for display-enabled devices and the rising complexity of LCD driver IC designs requiring more rigorous validation. The proliferation of TFT-LCD panels across automotive and consumer electronics sectors has further intensified the need for precise and reliable testing solutions. Furthermore, the growing adoption of advanced channel configurations, such as 256 IO and 512 IO channel testers, is enabling manufacturers to handle increasingly sophisticated driver IC architectures. Key players operating in Global LCD Driver IC Tester market include Teradyne, Cohu, Inc., Advantest, YTEC, King Long Technology, Wuhan Jingce Electronic Group, and HangZhou Speedcury Technology, among others, each contributing to a competitive and innovation-driven landscape.

MARKET DRIVERS

Rising Demand for Consumer Electronics Fueling LCD Driver IC Tester Adoption

Global proliferation of smartphones, tablets, wearables, and smart home displays has significantly amplified the need for rigorous quality assurance in display component manufacturing. As LCD panels continue to serve as a dominant display technology across mid-range consumer devices, manufacturers are investing in advanced testing infrastructure to ensure functional reliability. LCD Driver IC Tester market is benefiting directly from this upstream demand, as semiconductor fabs and display module assemblers require precise validation tools to confirm the electrical and functional integrity of driver ICs before integration into finished products.

Expansion of Automotive Display Systems Driving Testing Equipment Investment

Automotive OEMs and Tier-1 suppliers are increasingly integrating multi-zone LCD clusters, center-stack infotainment screens, and heads-up display systems into both electric and conventional vehicles. This shift toward digitized cockpit environments has elevated the criticality of LCD Driver IC performance validation, where failure can have direct safety implications. Manufacturers operating in the automotive display supply chain are consequently adopting specialized LCD Driver IC Tester solutions that meet stringent automotive-grade testing standards, including AEC-Q100 qualification requirements, thereby driving sustained market demand.

➤ The automotive display segment is emerging as one of the fastest-growing end-use verticals for LCD Driver IC Tester equipment, driven by rising in-vehicle screen proliferation and safety-critical performance requirements.

Industrial automation and medical device sectors are also contributing meaningfully to market growth. HMI panels, diagnostic imaging displays, and ruggedized control interfaces all rely on dependable LCD driver ICs, and the associated testing protocols must account for extended operational temperature ranges, vibration resistance, and long-term reliability. This broadening application base is encouraging test equipment vendors to develop more versatile and programmable LCD Driver IC Tester platforms capable of addressing multi-segment requirements within a single testing framework.

MARKET CHALLENGES

Technical Complexity of Testing Advanced Driver IC Architectures

As LCD Driver IC designs evolve to support higher resolutions, faster refresh rates, and lower power consumption profiles, the underlying test methodologies must keep pace. Modern driver ICs incorporate complex mixed-signal architectures combining analog voltage generation, digital timing controllers, and embedded memory elements. Developing test programs that thoroughly validate each functional block without compromising throughput or introducing measurement artifacts represents a significant engineering challenge for both test equipment developers and in-house testing teams. This complexity can extend development timelines and increase the cost per tested unit, particularly for smaller-volume specialty display applications.

Other Challenges

High Initial Capital Expenditure

Deploying production-grade LCD Driver IC Tester systems requires substantial upfront investment in both hardware platforms and application-specific test sockets, contactors, and load boards. For smaller display component manufacturers or contract test houses serving niche markets, this capital barrier can limit access to the most capable testing solutions, potentially resulting in reliance on older or less comprehensive test methodologies that may not fully address current driver IC feature sets.

Shortage of Specialized Test Engineering Talent

Operating and programming advanced LCD Driver IC Tester platforms demands expertise spanning analog circuit analysis, digital protocol validation, and display timing standards such as MIPI DBI and SPI interfaces. The availability of engineers with this precise combination of skills remains limited in many manufacturing regions, creating bottlenecks in test program development and qualification cycles. This talent gap can delay time-to-market for new display products and increase reliance on external test development services, adding cost and intellectual property exposure risks.

MARKET RESTRAINTS

Gradual Market Transition Toward OLED and MicroLED Display Technologies

One of the structural restraints facing LCD Driver IC Tester market is the ongoing technological migration in the premium display segment toward OLED and, increasingly, MicroLED panel technologies. High-end smartphones, flagship televisions, and premium wearable devices are progressively shifting away from LCD architectures, which over the long term could moderate growth in demand for LCD-specific driver IC testing equipment in high-value consumer electronics manufacturing. While this transition is gradual and LCD technology retains strong positions in cost-sensitive segments, the directional shift is a factor that market participants must strategically account for in product roadmap planning.

Consolidation Among Display IC Manufacturers Limiting Tester Procurement Diversity

LCD Driver IC supply chain has experienced consolidation as larger semiconductor companies acquire or outcompete smaller specialized fabless design firms. This consolidation tends to concentrate purchasing decisions for test equipment among fewer, larger buyers with stronger negotiating leverage, compressing margins for tester vendors and intensifying competition on price rather than technical differentiation. Additionally, vertically integrated display manufacturers that design proprietary driver ICs internally may develop bespoke test solutions, reducing the addressable market for third-party LCD Driver IC Tester suppliers in certain segments.

MARKET OPPORTUNITIES

Growth in Emerging Market Display Manufacturing Hubs Creating New Demand Centers

Rapid expansion of display panel and semiconductor assembly capacity across Southeast Asia, including Vietnam, India, and Malaysia, is creating substantial new demand for LCD Driver IC Tester equipment. Government-backed initiatives to develop domestic electronics manufacturing ecosystems in these regions are attracting both global display brands and local component suppliers, many of which require complete in-line and final test infrastructure. This geographic diversification of manufacturing activity presents a meaningful commercial opportunity for tester vendors able to offer localized technical support, regional application engineering, and competitively priced entry-level to mid-range testing platforms.

Integration of AI-Assisted Test Analytics Enhancing Platform Value Proposition

The incorporation of machine learning algorithms into test data analysis workflows is opening a new dimension of value for LCD Driver IC Tester platforms. By analyzing parametric test results across large production volumes, AI-assisted analytics tools can identify process drift, predict yield loss events, and correlate test outcomes with upstream wafer fabrication variables. Tester vendors that embed these capabilities , or provide open data interfaces compatible with third-party analytics platforms , are well positioned to differentiate their offerings beyond raw test throughput metrics and command premium pricing in technically sophisticated customer segments.

The growing deployment of Internet of Things devices, smart retail displays, and digital signage infrastructure across commercial and public environments is sustaining baseline demand for cost-effective LCD display modules and, by extension, the driver ICs that power them. This broad IoT-linked application landscape ensures continued relevance for LCD Driver IC Tester solutions across a wide installed base of mid-tier display products. Vendors that develop scalable, modular tester architectures capable of efficiently addressing both high-volume commodity driver IC testing and lower-volume specialty application requirements will be well positioned to capture this diversified opportunity set.

LCD Driver IC Tester Market Trends

Rising Demand for Advanced Display Technologies Driving LCD Driver IC Tester Market

LCD Driver IC Tester market is witnessing consistent growth, largely driven by the accelerating demand for high-performance display technologies across consumer electronics, automotive, and industrial sectors. As LCD driver integrated circuits become increasingly sophisticated , managing precise voltage and timing signals across complex display panels , the need for rigorous, specialized testing equipment has grown in parallel. Manufacturers in LCD Driver IC Tester market are responding by developing testers capable of evaluating a broader range of electrical, functional, and performance parameters to meet evolving product specifications.

Other Trends

Expansion of Automotive Display Applications

One of the most prominent trends shaping LCD Driver IC Tester market is the rapid integration of advanced display systems in automotive environments. Modern vehicles increasingly feature digital dashboards, infotainment screens, and heads-up displays that rely on high-quality LCD driver ICs. This has created a notable uptick in demand for testers capable of validating driver ICs designed to operate reliably under temperature extremes and vibration conditions specific to automotive applications. Key players such as Teradyne, Advantest, and Cohu, Inc. have been actively developing solutions aligned with automotive-grade testing standards.

Shift Toward Higher IO Channel Configurations

Another significant trend in LCD Driver IC Tester market is the growing adoption of higher IO channel configurations. As display resolutions increase and driver IC architectures become more complex, testing equipment must support greater pin counts and parallel testing capabilities. The 512 IO Channel segment is gaining traction alongside the established 256 IO Channel segment, as manufacturers seek to reduce test time and improve throughput in high-volume production environments. This shift reflects a broader industry move toward cost-efficient, scalable testing infrastructure.

Asia-Pacific as the Dominant Regional Market

Asia-Pacific, led by China, Japan, and South Korea, continues to dominate LCD Driver IC Tester market. The concentration of display panel manufacturing and semiconductor fabrication in this region sustains strong local demand for testing equipment. Companies such as Wuhan Jingce Electronic Group and HangZhou Speedcury Technology are strengthening their regional presence, while global players expand partnerships with local supply chain stakeholders to maintain competitive positioning.

Integration of TFT and LVDS Testing Capabilities

LCD Driver IC Tester market is also being shaped by the growing requirement to test both TFT LCD Driver and LVDS LCD Driver ICs within unified testing platforms. As end-product designs evolve to support higher refresh rates and wider color gamuts, testers must accommodate diverse driver IC architectures within a single solution. This convergence trend is prompting manufacturers to invest in modular, software-configurable testing platforms that offer flexibility across multiple application segments, ultimately supporting more efficient validation workflows in fast-moving production environments.

COMPETITIVE LANDSCAPE

Key Industry Players

LCD Driver IC Tester Market , Competitive Dynamics and Leading Manufacturer Profiles

Global LCD Driver IC Tester market, valued at approximately USD 295 million in 2025 and projected to reach USD 372 million by 2032 at a CAGR of 3.5%, is characterized by a moderately consolidated competitive landscape. Teradyne, Advantest, and Cohu, Inc. collectively represent the most prominent tier of global competitors, leveraging decades of semiconductor test equipment expertise, broad product portfolios, and well-established distribution networks. These industry leaders have consistently invested in R&D to develop testers capable of addressing increasingly complex LCD driver IC architectures, including high-channel-count configurations such as 512 IO and 256 IO Channel platforms. Their global reach across North America, Europe, and Asia-Pacific , particularly in high-volume manufacturing hubs in China, Japan, South Korea, and Southeast Asia , reinforces their dominant revenue share. The top five players collectively accounted for a significant portion of global market revenue in 2025, underscoring the importance of scale, technological differentiation, and customer relationships in this specialized segment.

Beyond the top-tier incumbents, several regionally significant and niche players are actively shaping the competitive environment. Chinese manufacturers including Wuhan Jingce Electronic Group and HangZhou Speedcury Technology have gained considerable traction in the Asia-Pacific market, benefiting from proximity to major LCD panel and semiconductor fabrication ecosystems, competitive pricing, and growing domestic demand for display testing solutions. YTEC and King Long Technology also maintain meaningful market presence, particularly in serving LVDS LCD Driver and TFT LCD Driver testing applications. As original equipment manufacturers (OEMs) across automotive, consumer electronics, and industrial display segments demand higher test throughput and precision, competition among these players is intensifying around product innovation, after-sales support, and customization capabilities. Strategic mergers, acquisitions, and technology partnerships are expected to further reshape the competitive dynamics through the forecast period to 2032.

List of Key LCD Driver IC Tester Companies Profiled

- Teradyne

- Cohu, Inc.

- Advantest

- Wuhan Jingce Electronic Group

- YTEC

- King Long Technology

- HangZhou Speedcury Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

512 IO Channel testers represent the leading and fastest-growing type segment in LCD Driver IC Tester market, driven by the increasing complexity of modern display technologies.

|

| By Application |

|

TFT LCD Driver testing constitutes the dominant application segment, reflecting the widespread adoption of thin-film transistor display technology across a broad spectrum of consumer and industrial devices.

|

| By End User |

|

Semiconductor Manufacturers represent the primary end-user segment for LCD Driver IC Testers, as they bear direct responsibility for ensuring IC performance compliance before components reach downstream customers.

|

| By Testing Stage |

|

Package-Level Testing dominates the testing stage segmentation, serving as the most widely deployed stage across both high-volume consumer electronics and industrial manufacturing lines.

|

| By Automation Level |

|

Fully Automated Testers lead the automation level segment, reflecting the broader industry trend toward intelligent, high-throughput manufacturing environments across the semiconductor and electronics sectors.

|

Regional Analysis: LCD Driver IC Tester Market

Asia-Pacific

Asia-Pacific hosts an unparalleled density of LCD panel and semiconductor manufacturing facilities. The deeply integrated supply chains across China, Taiwan, South Korea, and Japan enable faster adoption of specialized LCD driver IC testing equipment, reducing lead times and accelerating product qualification cycles critical to competitive consumer electronics markets.

National semiconductor strategies across China, South Korea, and Japan are channeling substantial resources into domestic IC design and fabrication capabilities. These policy-driven investments directly stimulate demand for LCD driver IC testing solutions, as newly established fabs and design centers require robust quality assurance and validation infrastructure to meet global performance benchmarks.

The region’s position as Global hub for smartphones, tablets, automotive displays, and industrial monitors creates persistent end-market pull for LCD driver IC testing. Continuous innovation in high-resolution and energy-efficient display technologies by regional OEMs demands next-generation tester platforms capable of validating increasingly complex driver ICs.

Beyond established semiconductor powerhouses, Southeast Asian economies including Vietnam, Malaysia, and India are emerging as significant electronics manufacturing destinations. As global supply chains diversify into these markets, demand for LCD driver IC testing infrastructure is expected to grow considerably, broadening the regional market base and creating new revenue opportunities through 2034.

North America

North America represents a mature and technologically sophisticated segment of LCD Driver IC Tester Market. The United States, in particular, is home to a number of leading semiconductor equipment companies, IC design firms, and display technology innovators that drive consistent demand for advanced testing solutions. While large-scale LCD panel manufacturing is relatively limited compared to Asia-Pacific, the region’s strength lies in high-value IC design, defense electronics, medical imaging systems, and automotive display applications , all of which require rigorous driver IC validation. The presence of well-established test and measurement companies fosters a culture of innovation in testing methodologies. Additionally, growing federal emphasis on domestic semiconductor production, bolstered by strategic policy initiatives, is expected to gradually expand the regional manufacturing base. Canada also contributes through its research institutions and emerging fabless IC design ecosystem. North America’s focus on precision, reliability, and compliance-driven quality standards continues to shape its distinct approach to LCD Driver IC Tester Market.

Europe

Europe occupies a prominent niche in LCD Driver IC Tester Market, characterized by its emphasis on automotive-grade display technologies, industrial automation systems, and high-reliability electronics. Germany, the Netherlands, and France are among the key contributors, housing globally recognized semiconductor equipment manufacturers and automotive electronics suppliers that demand stringent display driver IC testing. The region’s strong regulatory environment and commitment to quality certification standards drive adoption of advanced tester platforms capable of meeting exacting performance thresholds. European automotive OEMs, increasingly integrating sophisticated LCD-based instrument clusters, infotainment systems, and heads-up displays, represent a growing end-use segment for LCD driver ICs , and by extension, for testing equipment. The EU’s strategic focus on technological sovereignty and investments in semiconductor research further support regional market development. Europe’s market is expected to demonstrate steady, quality-driven growth throughout the 2026–2034 forecast horizon.

South America

South America remains a developing but gradually evolving participant in Global LCD Driver IC Tester Market. Brazil leads the regional landscape, supported by its established electronics manufacturing industry and a growing base of consumer electronics assembly operations, particularly in the Zona Franca de Manaus free trade zone. While the region currently lacks large-scale indigenous semiconductor fabrication, increasing imports of LCD-integrated devices and components are creating indirect demand for associated testing infrastructure. Local contract manufacturers and electronics distributors are progressively recognizing the importance of IC quality validation to compete in both domestic and export markets. Economic stabilization efforts and trade agreements are expected to attract incremental foreign investment into the region’s electronics sector. As regional awareness of quality standards grows and multinational electronics firms expand their South American footprints, LCD Driver IC Tester Market in this region is anticipated to gain measured momentum over the forecast period.

Middle East & Africa

The Middle East and Africa region represents an nascent but strategically interesting frontier for LCD Driver IC Tester Market. While the region does not currently host a significant volume of semiconductor or LCD manufacturing activity, its rapid urbanization, expanding telecommunications infrastructure, and growing consumer electronics adoption are collectively stimulating downstream demand for LCD-integrated devices. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are increasingly positioning themselves as regional technology and innovation hubs, drawing investment in electronics assembly and distribution. Government-led smart city initiatives, digital transformation programs, and education technology rollouts across the region are elevating the need for reliable display-integrated electronics. As the regional electronics ecosystem matures and global manufacturers seek to diversify their operational geographies, the Middle East and Africa is expected to represent a longer-term growth opportunity within the broader LCD Driver IC Tester Market through 2034.

Report Scope

This market research report provides a comprehensive analysis of LCD Driver IC Tester Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of LCD Driver IC Tester Market?

-> Global LCD Driver IC Tester Market was valued at USD 295 Million in 2025 and is projected to reach USD 372 Million by 2032, growing at a CAGR of 3.5% during the forecast period.

Which key companies operate in LCD Driver IC Tester Market?

-> Key players include Teradyne, Cohu, Inc., Advantest, YTEC, King Long Technology, Wuhan Jingce Electronic Group, and HangZhou Speedcury Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for LCD driver ICs in smartphones, TVs, monitors, and automotive dashboards, growing need for quality assurance and functional testing of display components, and rapid expansion of consumer electronics and automotive display applications worldwide.

Which region dominates the market?

-> Asia is a dominant and fastest-growing region in LCD Driver IC Tester Market, led by key countries including China, Japan, South Korea, and Southeast Asia, driven by large-scale electronics manufacturing and display production hubs.

What are the emerging trends?

-> Emerging trends include increasing adoption of TFT LCD Driver testing, growth in LVDS LCD Driver applications, advancements in 512 IO Channel testers, and rising integration of automated and high-precision IC testing solutions to meet stringent display performance requirements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...