Laser Optoelectronics Market Insights

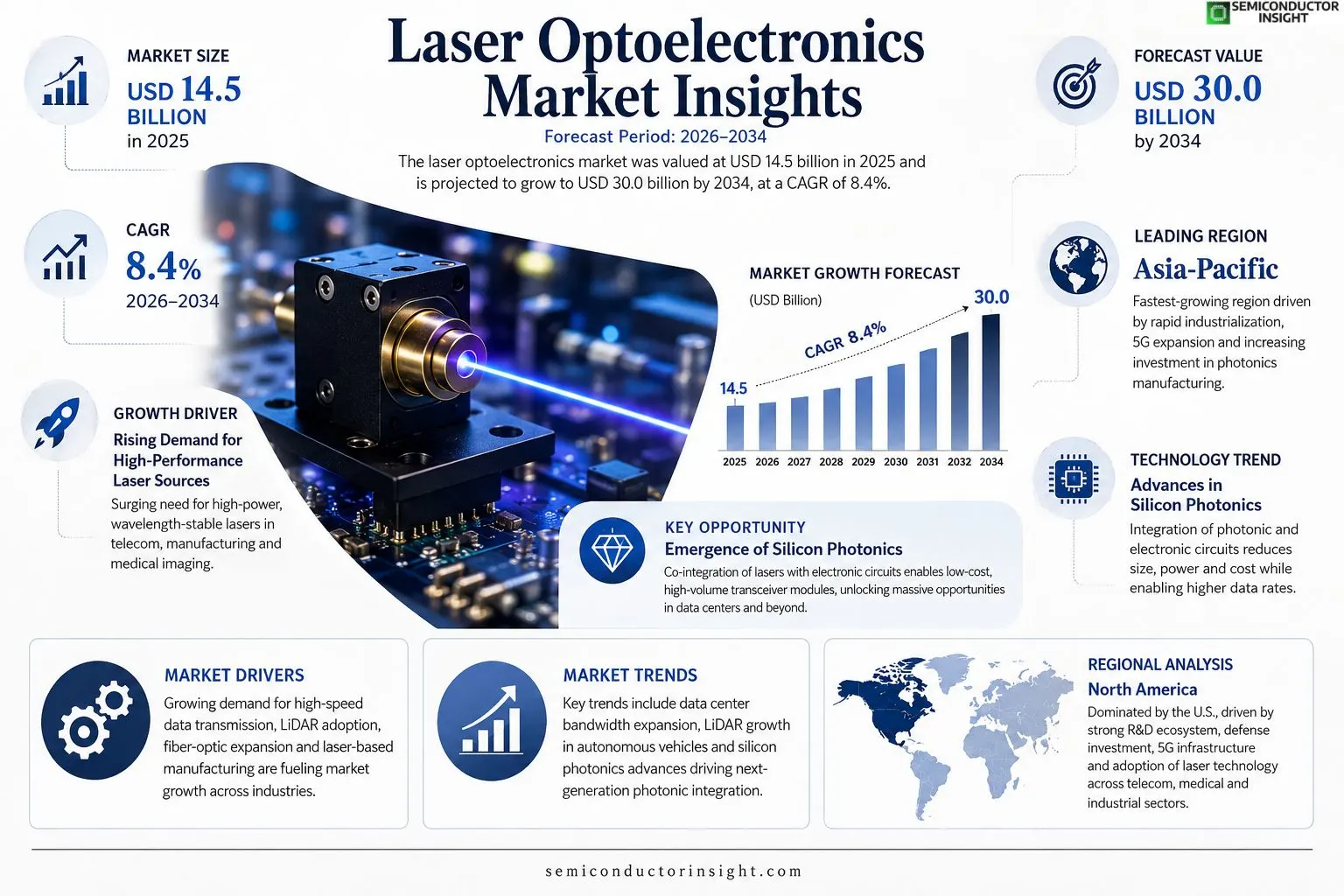

Laser optoelectronics market size was valued at USD 14.5 billion in 2025. The market is projected to grow from USD 14.5 billion in 2025 to USD 30.0 billion by 2034, exhibiting a CAGR of 8.4% during the forecast period.

Laser optoelectronics comprise semiconductor‑based components that emit, modulate, or detect light, such as Laser diodes, vertical‑cavity surface‑emitting Lasers (VCSELs), photodiodes, optical modulators and integrated photonic circuits. These devices enable high‑speed data transmission, precision sensing, medical imaging and advanced manufacturing because they convert electrical energy into coherent optical signals or vice versa.The market is experiencing rapid growth due to expanding data‑center bandwidth demands, rising adoption of LiDAR in autonomous vehicles, increased investment in fiber‑optic communication infrastructure and growing use of Laser‑based manufacturing processes. Furthermore, breakthroughs in silicon photonics and quantum dot Lasers are accelerating product launches while key players,including II‑VI Incorporated, Coherent Corp., Lumentum Holdings and NeoPhotonics,are pursuing strategic acquisitions and R&D partnerships that further fuel expansion.

MARKET DRIVERS

Rising Demand for High‑Performance Laser Sources

Laser Optoelectronics Market is being propelled by the surge in demand for high‑power, wavelength‑stable Laser sources across telecommunications, semiconductor manufacturing, and medical imaging. End‑users are seeking devices that deliver >90% efficiency, driving manufacturers to invest in advanced diode and fiber‑Laser technologies.

Growth of 5G and Data Center Infrastructure

Expansion of 5G networks and the need for ultra‑fast data center interconnects are creating a robust ecosystem for short‑reach and long‑reach optical transceivers. This trend is expected to lift overall market revenue by double‑digit percentages annually through 2030.

➤ “The convergence of photonic integration and AI‑driven design is set to double the output of Laser modules within five years.”

In addition, government incentives for photonics research in Europe and Asia are accelerating commercialization, further reinforcing the growth trajectory of Laser Optoelectronics Market.

MARKET CHALLENGES

Complexity of Manufacturing High‑Precision Devices

Producing Laser components with sub‑micron tolerances demands sophisticated cleanroom environments and skilled labor. The high capital expenditure required for epitaxial reactors and testing equipment raises entry barriers and compresses margins for smaller players.

Other Challenges

Supply Chain Vulnerabilities

Reliance on rare earth materials and specialized substrates exposes the market to geopolitical risks, leading to occasional shortages that can delay product launches and increase costs.

MARKET RESTRAINTS

Stringent Regulatory Standards

Regulatory compliance for Laser safety (IEC 60825) and environmental directives (RoHS) imposes additional testing and certification steps, extending time‑to‑market and raising operational expenses.

High Initial Capital Outlay

Investments in next‑generation photonic integration platforms exceed $200 million per facility, which can deter new entrants and limit the pace of innovation in Laser Optoelectronics Market.

MARKET OPPORTUNITIES

Emergence of Silicon Photonics

Silicon photonics enables the co‑integration of Lasers with electronic circuits, opening avenues for low‑cost, high‑volume production of transceiver modules. Companies that master this integration can capture a sizable share of the expanding data‑center market.

Laser‑Based Manufacturing Automation

Industries such as additive manufacturing and micro‑electronics are adopting ultrafast Laser systems for precision cutting and annealing, presenting a lucrative niche for specialized high‑peak‑power Lasers.

Growth in Biomedical Applications

Advances in minimally invasive surgery and diagnostic imaging are increasing demand for tunable, fiber‑delivered Laser sources, offering a long‑term growth trajectory for Laser Optoelectronics Market.

Laser Optoelectronics Market Trends

Data Center Bandwidth Expansion

The surge in cloud computing and high‑performance AI workloads is driving data‑center operators to seek ever‑greater optical throughput. Laser optoelectronic modules, especially high‑speed Laser diodes and VCSEL arrays, are being deployed to support transceiver links that exceed 400 Gb/s per channel. This infrastructure upgrade reduces latency and power consumption compared with traditional copper solutions, creating a steady pipeline of orders for component manufacturers. The trend is reinforced by industry standards bodies that are ratifying new optical interface specifications, ensuring a predictable demand curve for the next decade.

Other Trends

LiDAR Adoption in Autonomous Vehicles

Automakers and technology firms are integrating solid‑state LiDAR sensors that rely on compact Laser diodes and photodiodes to generate precise range maps. Recent breakthroughs in beam‑forming techniques have lowered the cost per sensor, enabling mass‑production road‑mapping systems across multiple vehicle platforms. As safety regulations tighten and consumer expectations for autonomous features rise, the volume of Laser‑based ranging units is projected to increase dramatically, prompting suppliers to expand dedicated production lines and invest in reliability testing programs.

Advances in Silicon Photonics

Silicon photonics is reshaping the way optical circuits are fabricated, allowing photonic components to be integrated directly onto silicon wafers alongside electronic drivers. This convergence reduces package size and improves thermal management, making it attractive for both telecom back‑haul and emerging quantum communication applications. Major players are filing patents on quantum‑dot Laser sources that can be monolithically integrated, accelerating time‑to‑market for next‑generation transceivers. The cumulative effect is a broader adoption of Laser optoelectronic technology across sectors that previously relied on discrete components, reinforcing the overall growth trajectory of the market.

COMPETITIVE LANDSCAPEKey Industry Players

Laser Optoelectronics Market Competitive Overview

Laser Optoelectronics Market is presently anchored by a handful of large, vertically integrated manufacturers that dominate revenue streams and drive technology road‑maps. Lumentum Holdings and Coherent Corp. together account for roughly 35 % of shipments, leveraging extensive portfolios that span high‑power Laser diodes, VCSEL arrays, and advanced photonic integrated circuits. Their scale enables aggressive R&D investment in silicon photonics and quantum‑dot Lasers, while strategic acquisitions,such as Coherent’s purchase of Finisar’s optical‑module business,strengthen end‑to‑end supply chains. This concentration of capability creates high barriers to entry, shaping a market structure where tier‑1 suppliers secure the majority of data‑center and autonomous‑vehicle contracts.Beyond the tier‑1 tier, a diverse set of niche players contributes specialized expertise that sustains market growth. II‑VI Incorporated supplies compound‑semiconductor Laser diodes for aerospace and defense, while NeoPhotonics focuses on high‑speed telecom transceivers. Hamamatsu Photonics excels in precision photodiodes for medical imaging, and OSRAM (now ams OSRAM) leads in visible‑light Laser sources for automotive LiDAR. Additional innovators such as Sony, Panasonic, Mitsubishi Electric, Sharp, and Gooch & Housego provide complementary component families, enabling OEMs to source tailored solutions without relying on the dominant giants.

List of Key Laser Optoelectronics Companies Profiled

- Lumentum Holdings

- Coherent Corp.

- II‑VI Incorporated

- NeoPhotonics

- Finisar (now part of II‑VI)

- Hamamatsu Photonics

- ams OSRAM

- Sony Corporation

- Panasonic Corp.

- Mitsubishi Electric

- Sharp Corporation

- Gooch & Housego

- Broadcom Inc.

- Marvell Technology Group (via Inphi)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Laser Diodes remain the foundational component driving market momentum – they are valued for their maturity, reliability, and cost‑effectiveness in high‑volume data‑center links. – Continuous improvements in wavelength stability and packaging enable seamless integration with emerging silicon‑photonic platforms. – Their broad adoption fuels downstream innovations in VCSELs and photonic‑integrated circuits, creating a virtuous cycle of technology refinement across the ecosystem. |

| By Application |

|

Data‑Center Communications is the pre‑eminent application driving adoption – demand for higher bandwidth and lower latency pushes designers toward Laser‑based optical interconnects. – The shift to coherent detection and advanced modulation formats amplifies the relevance of integrated photonic modules. – Synergies with emerging silicon photonics reduce form‑factor and power consumption, reinforcing the strategic importance of this segment. |

| By End User |

|

Telecom Operators anchor the end‑user landscape – they prioritize ultra‑reliable, high‑capacity links for backbone and metro networks. – Investments in 5G and beyond create a sustained appetite for wavelength‑division multiplexed Laser sources. – Collaborative R&D with equipment vendors accelerates the rollout of low‑power, high‑density transceivers, cementing the central role of telecom operators in shaping product roadmaps. |

| By [Segment Category 3]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

| By [Segment Category 4]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

Regional Analysis: North America

United States

The telecommunications sector is a major driver for Laser optoelectronics, with increasing demand for Laser diodes and Laser modulators for high-speed data transmission. The rollout of 5G networks and the expansion of optical fiber infrastructure are key factors fueling this growth.

The demand for Laser technology in defense applications, including Laser rangefinders, Laser designation systems, and Laser countermeasures, continues to rise. Government investments in advanced defense technologies are a significant catalyst for this market segment.

Laser technology plays a crucial role in medical procedures, including Laser surgery, diagnostics, and therapeutic applications. The increasing adoption of minimally invasive surgical techniques is driving demand for advanced Laser systems.

Laser applications in industrial settings include Laser cutting, Laser welding, and Laser marking, leading to increased precision and efficiency in manufacturing processes. The growth of automation in various industries is boosting the demand for these Laser systems.

North America

The North American Laser optoelectronics market is characterized by its technological sophistication and a strong emphasis on innovation. The region benefits from a well-established ecosystem of research institutions, manufacturers, and end-users. Key growth drivers include the expanding telecommunications infrastructure, increasing investments in defense technologies, and advancements in medical applications. The strong presence of major players and a competitive landscape contribute to continuous product development and market expansion within Laser optoelectronics market. Furthermore, government initiatives promoting domestic manufacturing and technological advancements are expected to further fuel growth in the coming years. The adoption of advanced Laser solutions is projected to be consistent across various sectors, solidifying North America’s position as a leading region.

Europe

Europe’s Laser optoelectronics market is experiencing steady growth, driven by increasing adoption in automotive, industrial, and medical sectors. Strong R&D activities, particularly in Germany and the UK, are fostering innovation in Laser technologies. Key applications include Laser diodes for automotive lighting and Laser systems for industrial processing. Government support for research and development, coupled with a focus on sustainable manufacturing, is expected to further promote market growth. The European Union’s initiatives promoting technological advancement and industrial competitiveness are also contributing to the expansion of Laser optoelectronics market in the region. The region is also witnessing a growing emphasis on energy-efficient Laser solutions.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for Laser optoelectronics, propelled by rapid industrialization and increasing investments in telecommunications and manufacturing. China, Japan, and South Korea are key contributors to this growth, with significant demand from sectors like consumer electronics, automotive, and industrial automation. The expanding 5G infrastructure and the growing adoption of Laser technology in manufacturing are major drivers. Government initiatives promoting technological innovation and industrial upgrading are further fueling market expansion. The Asia-Pacific Laser optoelectronics market is anticipated to remain dynamic with continued growth in emerging economies within the region.

South America

Laser optoelectronics market in South America is gradually growing, primarily driven by the expanding telecommunications infrastructure and increasing industrialization in countries like Brazil and Argentina. The demand for Laser diodes in telecommunication systems and Laser systems for industrial applications is on the rise. Government investments in infrastructure projects and a growing focus on technological advancement are supporting market expansion. While smaller compared to other regions, South America presents significant growth potential for Laser optoelectronics companies.

Middle East & Africa

Laser optoelectronics market in the Middle East & Africa is witnessing moderate growth, fueled by investments in infrastructure development, particularly in telecommunications and defense. Countries like Saudi Arabia and the UAE are increasingly adopting Laser technology in various applications. The growing focus on renewable energy and industrial expansion is expected to further drive market growth. The region presents opportunities for companies offering Laser solutions for infrastructure projects and industrial applications.

Report Scope

This market research report provides a comprehensive analysis of the Laser Optoelectronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Laser Optoelectronics Market?

-> Laser Optoelectronics Market was valued at USD 14.5 billion in 2025 and is expected to reach USD 30.0 billion by 2034.

Which key companies operate in Laser Optoelectronics Market?

-> Key players include II‑VI Incorporated, Coherent Corp., Lumentum Holdings and NeoPhotonics, among others.

What are the key growth drivers?

-> Key growth drivers include rising data‑center bandwidth demand, expanding LiDAR adoption in autonomous vehicles, increased investment in fiber‑optic communication infrastructure, and growth of Laser‑based manufacturing processes.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include advancements in silicon photonics, quantum‑dot Laser technologies, and integrated photonic circuits enabling next‑generation high‑speed data transmission.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...