MARKET INSIGHTS

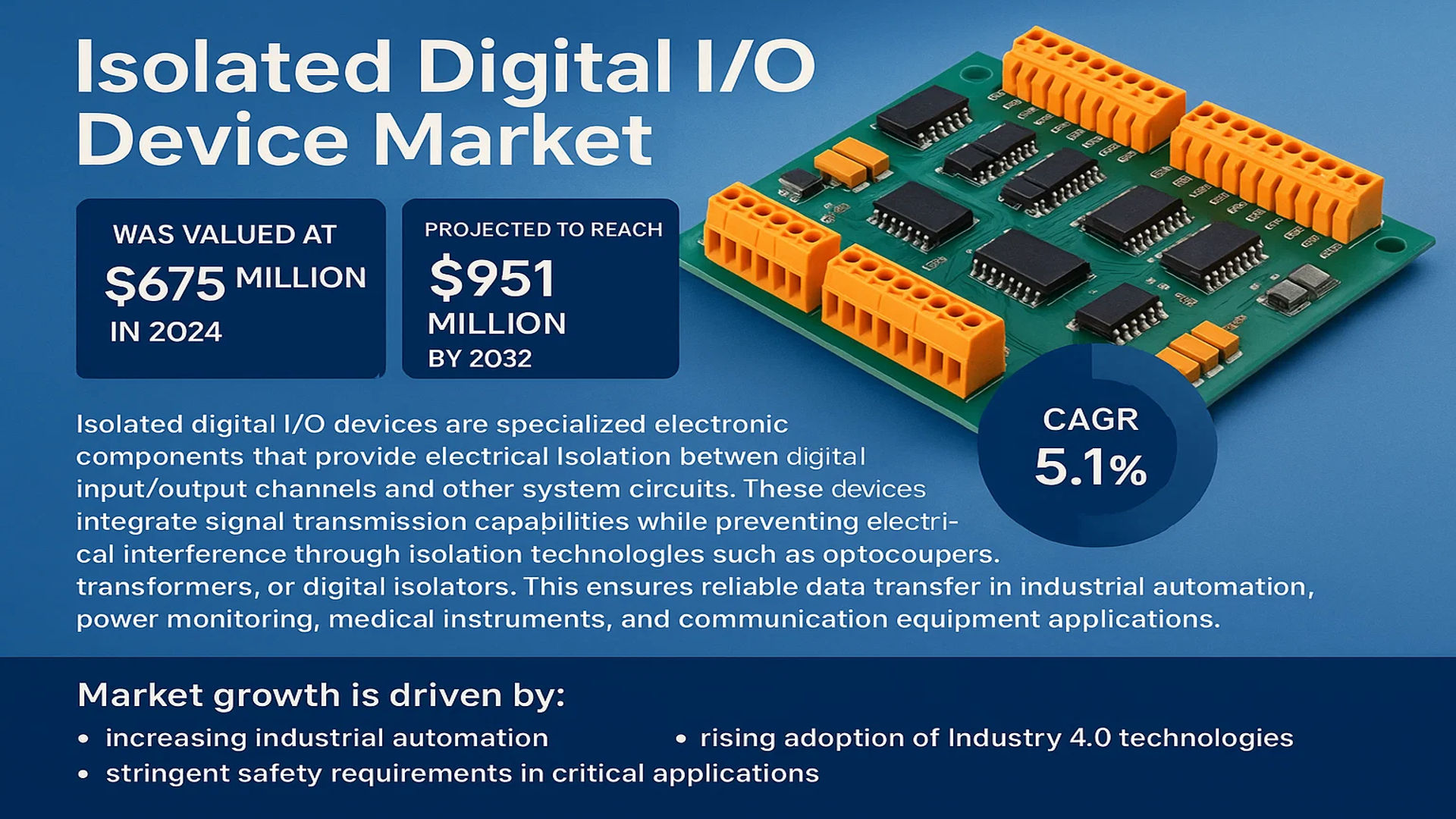

The global Isolated Digital I/O Device Market was valued at 675 million in 2024 and is projected to reach US$ 951 million by 2032, at a CAGR of 5.1% during the forecast period.

Isolated digital I/O devices are specialized electronic components that provide electrical isolation between digital input/output channels and other system circuits. These devices integrate signal transmission capabilities while preventing electrical interference through isolation technologies such as optocouplers, transformers, or digital isolators. This ensures reliable data transfer in industrial automation, power monitoring, medical instruments, and communication equipment applications.

The market growth is driven by increasing industrial automation, stringent safety requirements in critical applications, and the rising adoption of Industry 4.0 technologies. While North America currently holds significant market share, Asia-Pacific is expected to witness faster growth due to expanding manufacturing sectors. Key players like National Instruments, Advantech, and Siemens are enhancing their product portfolios with advanced isolation technologies to meet evolving industry demands.

MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Automation Adoption to Fuel Market Expansion

The global push towards Industry 4.0 and smart manufacturing is significantly driving demand for isolated digital I/O devices. These components play a critical role in ensuring reliable signal transmission in electrically noisy industrial environments, with the industrial automation sector accounting for over 45% of total market revenue. The growing need for plant efficiency and predictive maintenance capabilities, particularly in automotive and semiconductor manufacturing, has accelerated adoption. For instance, automotive manufacturers are increasingly integrating these devices in robotic assembly lines to maintain signal integrity while protecting sensitive control systems from high-voltage transients.

Stringent Safety Regulations Accelerate Product Demand

Enhanced safety standards across industries are compelling organizations to invest in isolated I/O solutions. The power monitoring sector has witnessed particularly strong growth, with isolated digital I/O devices becoming mandatory in many regions for grid-connected equipment. These regulations aim to prevent electrical hazards and ensure operational continuity, with the global market for power monitoring applications projected to grow at a 6.3% CAGR through 2032. Recent updates to international standards like IEC 61010 have further expanded application requirements, particularly in medical and laboratory equipment where patient and operator safety is paramount.

Technological Advancements in Isolation Techniques

Innovations in isolation technology are transforming market capabilities and applications. The introduction of capacitive and magnetic isolation techniques has enabled smaller form factors with higher channel densities, addressing space constraints in modern equipment designs. These advancements have been particularly impactful in communication equipment, where port density and signal integrity are critical. The transition from traditional optocouplers to digital isolators has improved reliability while reducing power consumption by up to 30%, making these solutions increasingly viable for battery-powered and portable medical devices.

MARKET RESTRAINTS

High Implementation Costs Constrain Market Penetration

Despite their advantages, isolated digital I/O devices face adoption barriers due to their premium pricing compared to non-isolated alternatives. The average selling price for industrial-grade isolated I/O modules remains 40-60% higher than basic digital I/O solutions, creating resistance in price-sensitive markets. Small and medium enterprises, particularly in developing regions, often perceive the added safety and reliability benefits as unjustified expenditures when working with low-voltage applications. This cost sensitivity has slowed market growth in sectors with tight budget constraints and limited technical requirements for isolation.

Other Restraints

Design Complexity Challenges

System integration hurdles frequently emerge when implementing isolated I/O solutions in legacy equipment not originally designed for galvanic isolation. Retrofitting existing automation systems often requires additional components and careful signal routing that add both cost and complexity to projects. These technical barriers are particularly pronounced when upgrading older manufacturing facilities where equipment may lack the necessary power supplies or mounting provisions for isolated I/O modules.

Technical Limitations in High-Speed Applications

While isolated digital I/O devices excel in robust industrial environments, they typically cannot match the speed capabilities of advanced non-isolated alternatives. Certain high-frequency communication protocols and precision timing applications require switching speeds beyond what most isolated solutions can practically deliver, limiting their adoption in specialized sectors such as automated test equipment and high-speed data acquisition systems.

MARKET OPPORTUNITIES

Rising Demand for Modular and Wireless I/O Solutions

The shift toward decentralized control architectures presents significant growth potential for the isolated digital I/O market. Emerging modular systems allow plants to distribute I/O nodes closer to field devices while maintaining isolation through innovative bus communication techniques. The wireless I/O segment, though currently representing less than 10% of the market, is projected to grow at nearly 12% annually as industries adopt flexible, cable-free solutions that maintain galvanic isolation through advanced power harvesting techniques.

Expansion in Renewable Energy Infrastructure

Global investments in renewable energy are creating new opportunities for isolated I/O applications. Solar and wind installations require robust signal isolation to handle the electrical noise and voltage transients inherent in power conversion equipment. The renewable energy sector’s isolation requirements have spurred development of specialized products featuring enhanced surge immunity and extended temperature ranges, with the market segment expected to account for nearly 15% of total sales by 2030.

Growth in Condition Monitoring Applications

The predictive maintenance trend is driving adoption of isolated digital I/O in vibration monitoring and equipment health systems. These applications demand reliable signal acquisition in electrically harsh environments while providing electrical separation between sensors and control systems. Manufacturers have responded with specialized I/O modules featuring built-in signal conditioning and advanced diagnostics, with the condition monitoring segment currently growing at a 7.5% annual rate.

MARKET CHALLENGES

Component Shortages Disrupt Supply Chains

The industry faces ongoing challenges from semiconductor supply chain disruptions that specifically affect isolation components. Specialty materials used in optocouplers and isolation transformers have experienced extended lead times, with some manufacturers reporting allocation periods exceeding 40 weeks. These constraints have forced companies to redesign products with alternative isolation technologies or accept delayed deliveries, impacting project timelines across multiple industries.

Other Challenges

Standardization Issues

Lack of uniform standards for isolation performance metrics creates confusion in the market. While basic isolation voltage ratings are well-defined, other critical parameters like creepage distance, partial discharge characteristics, and long-term reliability metrics vary significantly between manufacturers. This inconsistency complicates product selection and comparison, particularly for applications with rigorous safety requirements.

Talent Shortage in Industrial Automation

The growing complexity of isolated I/O solutions has outpaced the availability of technically qualified personnel. System integrators and plant engineers often lack specialized knowledge in isolation techniques and safety certifications, leading to improper installations and suboptimal system performance. The skills gap is particularly acute in emerging markets where industrial automation adoption is rapidly growing but training infrastructure remains limited.

ISOLATED DIGITAL I/O DEVICE MARKET TRENDS

Growing Industrial Automation to Drive Demand for Isolated Digital I/O Devices

The surge in industrial automation across manufacturing, oil & gas, and automotive sectors is significantly boosting the adoption of isolated digital I/O devices. These components play a crucial role in ensuring reliable signal transmission in electrically noisy industrial environments, preventing ground loops and voltage spikes from disrupting critical operations. The global market for industrial automation is projected to grow at a compound annual growth rate (CAGR) of 8.9%, which directly correlates with increased demand for robust I/O solutions. The rise of Industry 4.0 and smart factories has further accelerated installations, with isolated digital I/O modules becoming indispensable in PLCs, robotics, and motion control systems.

Other Trends

Expansion of Power Monitoring Systems

With increasing emphasis on energy efficiency and grid modernization, isolated digital I/O devices are witnessing heightened adoption in power monitoring applications. Utilities and energy providers leverage these devices to isolate high-voltage circuits from control systems, ensuring accurate data acquisition while protecting sensitive equipment. Countries investing in renewable energy infrastructure, such as China and Germany, are driving demand, as isolated I/O modules enhance the reliability of solar and wind power monitoring systems. Innovations in digital isolator technology, offering higher voltage ratings and lower power consumption, are further strengthening this market segment.

Medical Instrumentation Adopting Advanced Isolation Technologies

The medical sector is increasingly incorporating isolated digital I/O devices in diagnostic and therapeutic equipment to meet stringent safety standards. These devices prevent leakage currents in patient-connected systems like ECGs and MRI machines, where electrical isolation is critical for compliance with IEC 60601 standards. The growing prevalence of portable medical devices and telemedicine solutions has amplified this trend, as compact, low-power isolated I/O interfaces enable safer patient monitoring. The global medical electronics market, valued at over $6.5 billion, reflects this upward trajectory, with isolation components becoming a key enabling technology.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation to Maintain Dominance in Industrial Automation

The global Isolated Digital I/O Device market features a dynamic mix of established electronics giants and specialized automation solution providers. National Instruments currently leads the market with its comprehensive PXI and CompactRIO modular platforms that dominate laboratory and industrial automation applications. The company’s success stems from its software-driven approach to measurement systems, with isolated I/O modules accounting for approximately 24% of their test & measurement hardware revenue in 2024.

German industrial powerhouses Siemens and Beckhoff Automation have made significant inroads in the market through their industrial PC-based control solutions. Both companies have aggressively expanded their digital I/O module offerings with galvanic isolation technologies, particularly for harsh manufacturing environments where signal integrity is critical. Their combined share in the European market now exceeds 35%.

Meanwhile, Asian players like Advantech and Omron are gaining traction through cost-optimized solutions for high-volume applications. Advantech’s WebAccess IoT platform has become particularly popular for distributed monitoring systems, while Omron’s G3PX isolators set new benchmarks for power efficiency in factory automation.

The competitive landscape is further shaped by semiconductor specialists like Texas Instruments and Analog Devices, who supply isolation ICs to module manufacturers. These companies are driving innovation in digital isolator technology, with recent product releases offering superior noise immunity and smaller form factors that enable more compact I/O designs.

List of Key Isolated Digital I/O Device Companies Profiled

- National Instruments (U.S.)

- Advantech (Taiwan)

- Keysight Technologies (U.S.)

- ADLINK Technology (Taiwan)

- Phoenix Contact (Germany)

- Omron (Japan)

- Weidmüller (Germany)

- Beckhoff Automation (Germany)

- Siemens (Germany)

- Contec (Japan)

- Analog Devices (U.S.)

- Texas Instruments (U.S.)

- Infineon Technologies (Germany)

- Rockwell Automation (U.S.)

- Hunan Aixep Measurement and Control Technology (China)

Segment Analysis:

By Type

Parallel Segment Dominates Market Share Due to High Data Transmission Efficiency

The isolated digital I/O device market is segmented based on type into:

- Parallel

- Subtypes: 8-bit, 16-bit, 32-bit, and others

- Serial

- Subtypes: RS-232, RS-485, USB, and others

- Hybrid

- Others

By Application

Industrial Automation Leads Market Adoption Due to Growing Smart Factory Trends

The market is segmented based on application into:

- Industrial Automation

- Power Monitoring

- Medical Instruments

- Communication Equipment

- Others

By Isolation Technology

Optocouplers Remain Preferred Choice for Reliable Signal Isolation

The market is segmented based on isolation technology into:

- Optocouplers

- Digital Isolators

- Magnetic Isolators

- Others

By Voltage Range

Medium Voltage Segment Sees Strong Growth for Industrial Applications

The market is segmented based on voltage range into:

- Low Voltage (Below 100V)

- Medium Voltage (100V-1kV)

- High Voltage (Above 1kV)

Regional Analysis: Isolated Digital I/O Device Market

Asia-Pacific

The Asia-Pacific region dominates the global Isolated Digital I/O Device market, driven by rapid industrialization and expansive automation projects in manufacturing hubs like China, Japan, and India. China leads regional demand due to its robust electronics manufacturing sector and government initiatives like Made in China 2025, which prioritizes industrial IoT adoption. The proliferation of smart factories and Industry 4.0 technologies is accelerating the deployment of isolated digital I/O solutions for safety-critical applications. While cost-competitive local manufacturers such as Jingchuang Yueshi Technology and ADLINK Technology cater to mid-range demand, multinational players like Omron and Siemens are expanding high-performance offerings for precision-driven industries. However, fragmented regulatory standards and intellectual property concerns pose challenges for market consistency.

North America

North America remains a high-growth market for Isolated Digital I/O devices, with the U.S. accounting for over 60% of regional revenue. Stricter safety regulations in sectors like oil & gas and pharmaceuticals mandate the use of isolated I/O modules to prevent electrical hazards. The presence of technology leaders such as National Instruments and Texas Instruments fuels innovation in galvanic isolation techniques, particularly for medical instrumentation and aerospace applications. Investments in grid modernization and renewable energy projects further propel demand for isolated digital I/O in power monitoring systems. Nevertheless, supply chain disruptions and tariff fluctuations periodically impact component availability.

Europe

Europe’s market thrives on stringent EMC and functional safety directives (e.g., IEC 61010-1) that necessitate isolated I/O solutions across industrial automation. Germany’s manufacturing excellence, supported by companies like Beckhoff Automation and Phoenix Contact, drives adoption in automotive and machinery sectors. The EU’s emphasis on sustainable production practices encourages energy-efficient isolated I/O designs with reduced footprint. Challenges include pricing pressures from Asian manufacturers and slower replacement cycles in mature industries. Recent partnerships between research institutes and semiconductor firms aim to advance optocoupler-free isolation technologies.

South America

The region shows nascent but steady growth, with Brazil and Argentina emerging as key markets for industrial automation upgrades. Mining and agricultural equipment industries increasingly integrate isolated I/O modules to enhance operational safety in harsh environments. Economic instability and reliance on imports constrain market expansion, though local assembly initiatives by players like Rockwell Automation aim to improve cost competitiveness. Regulatory harmonization with international standards remains a work in progress.

Middle East & Africa

This region presents long-term potential, particularly in GCC countries investing in smart infrastructure and oilfield digitization. The lack of local manufacturing bases results in dependence on European and Asian suppliers. While project-based demand spikes occur in energy and transportation sectors, market cultivation is hindered by limited technical expertise and budget allocations favoring turnkey solutions over component-level upgrades.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Isolated Digital I/O Device markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Isolated Digital I/O Device market was valued at USD 675 million in 2024 and is projected to reach USD 951 million by 2032, growing at a CAGR of 5.1%.

- Segmentation Analysis: Detailed breakdown by product type (Parallel, Serial), application (Industrial Automation, Power Monitoring, Medical Instruments, Communication Equipment), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K.), Asia-Pacific (China, Japan, South Korea), Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including National Instruments, Advantech, Keysight Technologies, Siemens, and Rockwell Automation, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging isolation technologies (opto-couplers, digital isolators), integration with Industry 4.0 systems, and advancements in signal processing.

- Market Drivers & Restraints: Evaluation of factors such as industrial automation growth, safety regulations, and the impact of semiconductor shortages on supply chains.

- Stakeholder Analysis: Strategic insights for equipment manufacturers, system integrators, and investors regarding market opportunities and competitive positioning.

Primary research includes interviews with industry experts from leading manufacturers, while secondary research incorporates data from trade associations, company reports, and verified market intelligence sources.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Isolated Digital I/O Device Market?

-> Isolated Digital I/O Device Market was valued at 675 million in 2024 and is projected to reach US$ 951 million by 2032, at a CAGR of 5.1% during the forecast period.

Which key companies operate in Global Isolated Digital I/O Device Market?

-> Key players include National Instruments, Advantech, Keysight Technologies, Siemens, Rockwell Automation, Phoenix Contact, and Omron, with the top five companies holding significant market share in 2024.

What are the key growth drivers?

-> Major growth drivers include increasing industrial automation, stringent safety regulations, and adoption of Industry 4.0 technologies across manufacturing sectors.

Which region dominates the market?

-> Asia-Pacific shows the highest growth potential due to manufacturing expansion, while North America leads in technological adoption and market value.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive maintenance, adoption of digital isolator technology, and development of compact, high-speed I/O modules for industrial IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...