IoT Components Market Insights

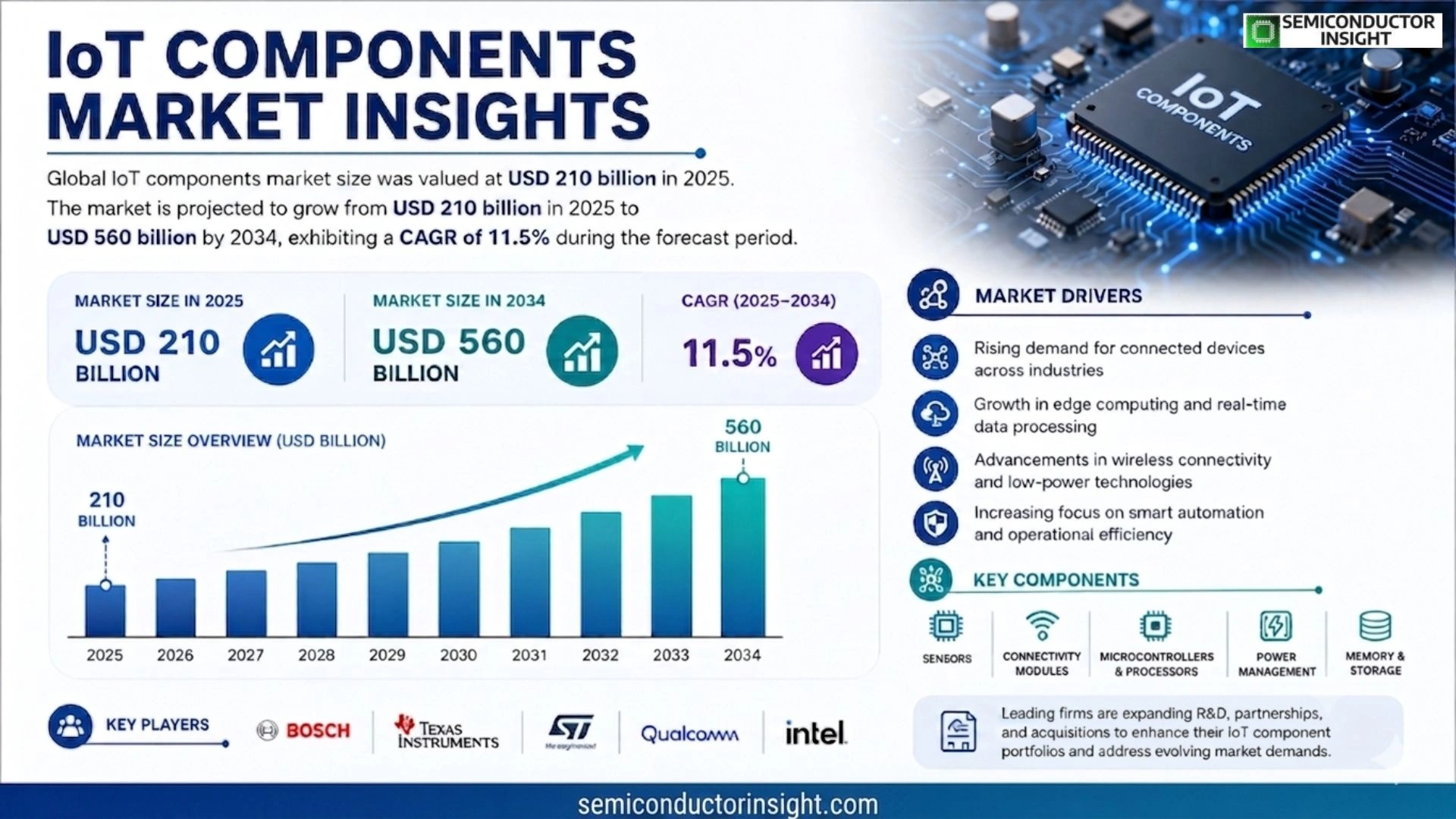

Global IoT Components Market size was valued at USD 210 billion in 2025. The market is projected to grow from USD 210 billion in 2025 to USD 560 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period.

IoT components comprise sensors, actuators, connectivity modules (Wi‑Fi, Bluetooth, LPWAN), edge processors and power‑management ICs that enable devices to collect data, communicate and execute actions autonomously across consumer, industrial and infrastructure domains.

The market is experiencing rapid growth due to rising investment in smart‑city projects, expanding industrial automation initiatives and increasing demand for connected healthcare solutions. Furthermore, advancements in low‑power wireless technologies and the rollout of private‑network LTE/5G are accelerating adoption. Initiatives by leading players are also fueling expansion; for example, in March 2024 Bosch partnered with Amazon Web Services to deliver edge‑AI capabilities for industrial IoT deployments. Texas Instruments, STMicroelectronics, Qualcomm and Intel continue to broaden their portfolios through strategic acquisitions and innovative product launches.

MARKET DRIVERS

Increasing Demand for Edge Connectivity

IoT Components Market is being propelled by the rapid adoption of edge computing architectures, which require compact, high‑performance modules to process data locally. Enterprises are investing in edge gateways and microcontrollers that reduce latency and bandwidth costs, creating a strong demand ripple across component suppliers.

Advancements in Low‑Power Sensors

Innovations in low‑power sensor technology enable longer battery life for remote installations, making IoT solutions more viable in agriculture, logistics, and health monitoring. These advancements are driving higher procurement volumes of MEMS, optical, and environmental sensors with IoT Components Market.

➤ “The convergence of 5G connectivity and ultra‑low‑power ASICs is expected to double component shipments by 2028.”

Overall, the synergy between connectivity upgrades and energy‑efficient designs is establishing a robust growth foundation for IoT Components Market over the next five years.

MARKET CHALLENGES

Regulatory Complexity

Global regulatory fragmentation, especially concerning wireless spectrum allocation and data privacy, poses compliance hurdles for manufacturers. Navigating divergent standards across regions can delay product launches and increase certification costs for IoT Components Market.

Other Challenges

Supply Chain Constraints

The reliance on rare earth materials and semiconductor fab capacity creates bottlenecks, leading to longer lead times and price volatility. Companies must diversify sourcing strategies to mitigate these risks.

MARKET RESTRAINTS

High Capital Expenditure

Establishing advanced manufacturing lines for high‑frequency components demands substantial capital outlays. Smaller players often lack the financial resources to scale, limiting competitive pressure and slowing overall market expansion withIoT Components Market.

MARKET OPPORTUNITIES

Growth in Smart Cities

Urban initiatives targeting intelligent traffic management, waste optimization, and energy efficiency are opening new demand channels for connected sensors, actuators, and communication modules. IoT Components Market stands to benefit from multi‑billion‑dollar public‑private projects that prioritize interoperable, scalable component ecosystems.

IoT Components Market Trends

Smart‑City Infrastructure Drives Adoption

IoT Components Market is experiencing a decisive shift as municipalities invest heavily in smart‑city projects. Deployments of wide‑area low‑power sensors for traffic, lighting, and environmental monitoring are creating a surge in demand for connectivity modules that support LPWAN and emerging private 5G networks. This momentum is reinforced by public‑private partnerships that integrate edge processors to enable real‑time analytics at the network edge, reducing latency for city‑scale operations. Recent collaborations, such as Bosch’s partnership with Amazon Web Services, are delivering edge‑AI capabilities that further accelerate sensor data processing on‑site. As city authorities prioritize energy efficiency, power‑management ICs are becoming essential for prolonged sensor lifetimes, driving a steady increase in component orders. Municipal data platforms are increasingly adopting open APIs, which further amplifies the need for interoperable communication modules that can bridge legacy systems with next‑generation sensors.

Other Trends

Industrial Automation Expansion

Industrial automation is another catalyst. Leading manufacturers are standardizing on modular actuator and sensor platforms that can be retrofitted to existing machinery, allowing factories to scale production lines without extensive re‑engineering. The integration of robust power‑management ICs ensures continuous operation in harsh environments, while Bluetooth and Wi‑Fi connectivity modules simplify machine‑to‑machine communication across the shop floor. Companies such as Texas Instruments and Qualcomm are introducing ultra‑low‑power transceivers that extend battery life for remote monitoring devices, and STMicroelectronics is broadening its portfolio of industrial‑grade sensors with built‑in diagnostics. These developments reduce total cost of ownership and encourage broader adoption of IoT components across sectors ranging from automotive assembly to food processing. The shift toward digital twins in manufacturing also pushes demand for high‑precision sensors that feed accurate real‑time data into simulation models.

Connected Healthcare Accelerates Demand

Connected healthcare solutions are further expanding IoT Components Market. Wearable sensors and implantable devices rely on ultra‑low‑power communication chips to transmit patient data securely to cloud platforms. Recent collaborations between device makers and cloud service providers have accelerated the rollout of edge‑AI capabilities, enabling on‑device inference that minimizes data transfer and preserves battery life. As hospitals adopt remote monitoring systems, demand for reliable power‑management and secure connectivity components continues to rise. Emerging standards for medical‑grade encryption are prompting manufacturers such as Intel and STMicroelectronics to embed hardware‑based security modules directly into connectivity ICs. The convergence of telehealth services with real‑time analytics is expected to sustain strong, long‑term growth for component suppliers. Regulatory guidance on data privacy is encouraging vendors to certify their components against international standards, enhancing trust among healthcare providers.

COMPETITIVE LANDSCAPE

Key Industry Players

IoT Components Market – Competitive Overview

IoT Components market, valued at USD 210 billion in 2025, is projected to reach USD 560 billion by 2034, driven by a robust 11.5% CAGR. Leading firms such as Bosch, Texas Instruments, STMicroelectronics, Qualcomm and Intel dominate the landscape by leveraging extensive R&D pipelines, strategic partnerships, and acquisitions to broaden sensor, connectivity‑module and edge‑processor portfolios. Bosch’s collaboration with Amazon Web Services for edge‑AI, TI’s emphasis on low‑power mixed‑signal ICs, and Intel’s push into AI‑optimized edge CPUs illustrate how top tier players shape market structure, capture large‑scale industrial and consumer contracts, and set pricing benchmarks across the ecosystem.

Beyond the headline names, a cadre of niche but highly innovative companies enriches the market with specialized capabilities. Analog Devices and Silicon Labs excel in precision analog front‑ends and ultra‑low‑power wireless solutions, while Murata and MediaTek focus on compact modules and integrated connectivity for consumer wearables. Renesas, Broadcom, Infineon, Samsung Electronics and Huawei contribute deep expertise in power‑management ICs, high‑speed transceivers and 5G‑enabled modules, targeting verticals such as smart‑city infrastructure, industrial automation and connected healthcare. These firms, though smaller in revenue share, drive differentiation through application‑specific designs and rapid time‑to‑market, sustaining a dynamic competitive environment.

List of Key IoT Components Companies Profiled

- Bosch

- Texas Instruments

- STMicroelectronics

- Qualcomm

- Intel

- NXP Semiconductors

- Analog Devices

- Silicon Labs

- Murata Manufacturing

- MediaTek

- Renesas Electronics

- Broadcom

- Infineon Technologies

- Samsung Electronics

- Huawei Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sensors are the dominant driver in the IoT components ecosystem, underpinning data collection across diverse environments.

|

| By Application |

|

Industrial Automation represents the most compelling application segment, where robust, low‑latency components are essential.

|

| By End User |

|

Manufacturing end users drive demand for resilient, high‑performance components that can operate in noisy, high‑temperature settings.

|

| By Connectivity |

|

Private LTE/5G is emerging as the preferred connectivity backbone for mission‑critical deployments.

|

| By Power Management |

|

Ultra‑Low‑Power ASICs are critical for extending device lifecycles in remote and wearable applications.

|

Regional Analysis: North America

The industrial sector in the US is experiencing rapid IoT adoption for predictive maintenance, asset tracking, and process optimization. This creates a substantial demand for ruggedized sensors, wireless communication modules, and industrial-grade processors.

The healthcare industry’s increasing focus on remote patient monitoring, wearable health devices, and connected medical equipment is significantly boosting the demand for specialized IoT components that adhere to stringent regulatory standards.

Urban development initiatives across the US are driving the deployment of smart city solutions, necessitating a wide range of IoT components for applications like intelligent transportation, environmental monitoring, and public safety.

The continued growth of smart home devices, wearables, and connected appliances fuels the demand for low-power, high-performance IoT components in the consumer electronics market.

Europe

Europe is witnessing steady growth IoT Components Market, with key drivers including government initiatives promoting digital transformation and increasing industrial automation. The region’s strong emphasis on data privacy and security is shaping the development of IoT solutions, leading to a focus on secure components and data protection technologies. The automotive sector and manufacturing industries are significant contributors to the market’s expansion. Sustainability concerns are also influencing the adoption of energy-efficient IoT components across various applications. European regulations are fostering innovation in areas like smart grids and connected vehicles.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for IoT components globally. The region’s rapid industrialization, coupled with increasing disposable incomes and government support for technology adoption, is fueling significant demand. China, in particular, is a dominant force, driving demand through its vast manufacturing base and extensive deployment of smart infrastructure. The consumer electronics market in countries like India and Southeast Asia is also a key growth driver. The focus on affordable and low-power IoT components is particularly prominent in this region.

South America

IoT Components Market in South America is in an early stage of development, but it presents promising growth opportunities. Increasing investments in infrastructure, agriculture, and logistics are creating demand for IoT solutions. The adoption of connected agriculture technologies and smart city initiatives in select countries is driving market expansion. Challenges include limited technological infrastructure and varying levels of economic development across the region. However, the potential for growth remains significant as connectivity improves and awareness of IoT benefits increases.

Middle East & Africa

The Middle East and Africa represent a relatively nascent market for IoT components, with significant potential for future growth. Government initiatives focused on smart cities, infrastructure development, and industrial diversification are creating demand. The oil and gas sector in the Middle East is an early adopter of IoT solutions for predictive maintenance and operational efficiency. Increasing investments in telecommunications infrastructure and growing urbanization are also driving market expansion in Africa. The focus is on applications that address specific regional challenges, such as water management and energy efficiency.

Report Scope

This market research report provides a comprehensive analysis of the IoT Components Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of IoT Components Market?

-> IoT components market size was valued at USD 210 billion in 2025. The market is projected to grow from USD 210 billion in 2025 to USD 560 billion by 2034, exhibiting a CAGR of 11.5%.

Which key companies operate IoT Components Market?

-> Key players include Bosch, Amazon Web Services, Texas Instruments, STMicroelectronics, Qualcomm, Intel, among others.

What are the key growth drivers?

-> Key growth drivers include smart‑city investments, industrial automation expansion, connected healthcare demand, low‑power wireless technology advancements, and private LTE/5G network rollouts.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include edge‑AI integration, LPWAN connectivity, AI‑enabled sensors, and next‑generation power‑management ICs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...