MARKET INSIGHTS

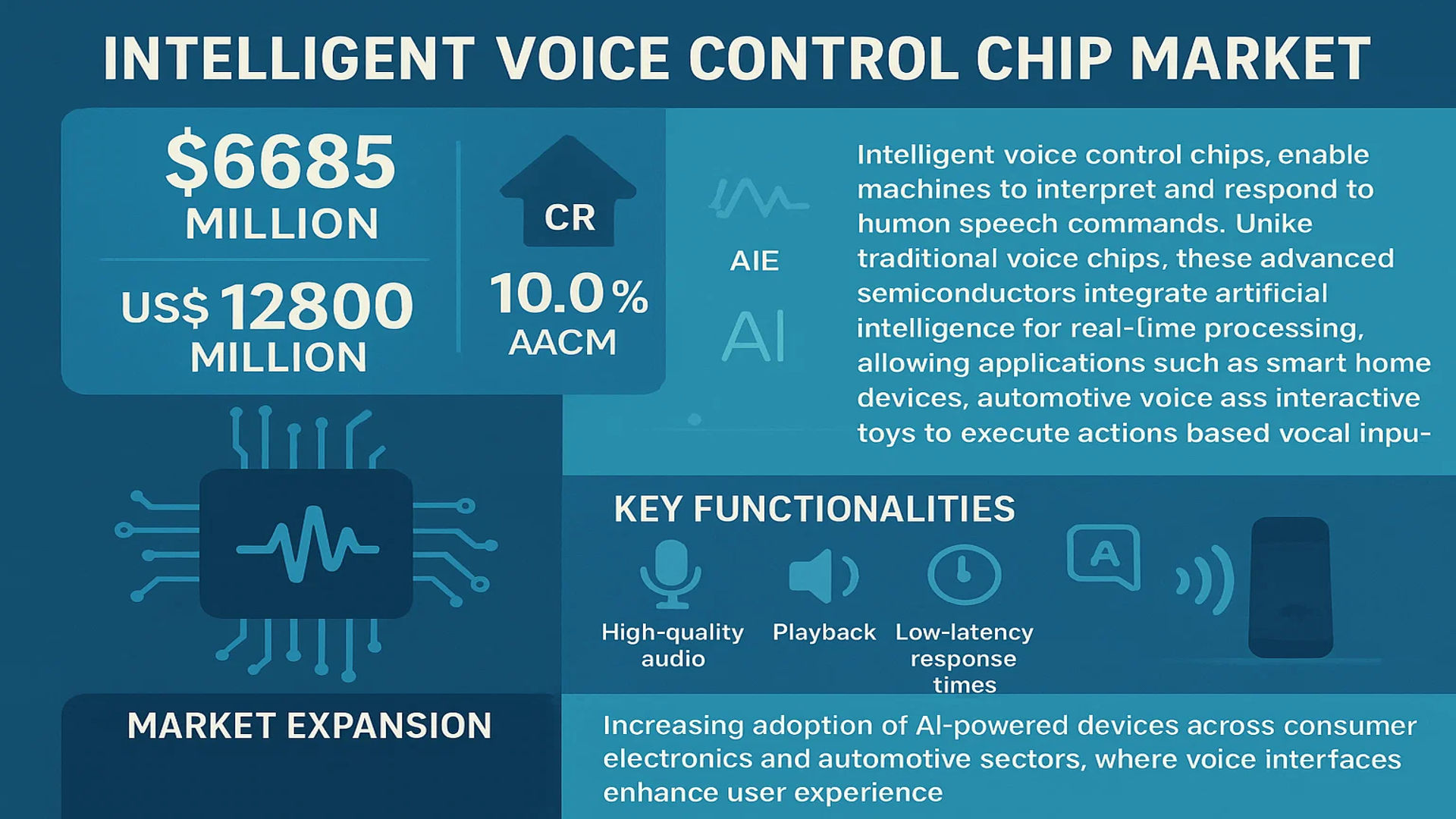

The global Intelligent Voice Control Chip Market was valued at 6685 million in 2024 and is projected to reach US$ 12800 million by 2032, at a CAGR of 10.0% during the forecast period.

Intelligent voice control chips, also known as voice recognition ICs, enable machines to interpret and respond to human speech commands. Unlike traditional voice chips, these advanced semiconductors integrate artificial intelligence (AI) algorithms for real-time processing, allowing applications such as smart home devices, automotive voice assistants, and interactive toys to execute actions based on vocal inputs. Key functionalities include high-quality audio recording, playback, and low-latency response times.

Market expansion is driven by increasing adoption of AI-powered devices across consumer electronics and automotive sectors, where voice interfaces enhance user experience. While growth in 2022 was tempered by semiconductor supply chain constraints – with the broader industry growing only 4.4% according to WSTS – segments like logic and sensors maintained double-digit gains. Asia-Pacific remains a critical region despite a 2.0% contraction in 2022, as local manufacturers scale production of cost-competitive chips for global OEMs.

MARKET DRIVERS

Rapid Expansion of Smart Home Devices to Fuel Market Growth

The proliferation of smart home devices has created substantial demand for intelligent voice control chips. With over 300 million smart home devices shipped globally in 2023, manufacturers are increasingly integrating voice recognition technology to enhance user experience. This chip technology enables seamless control of lighting, security systems, and smart appliances through natural language commands, driving adoption among tech-savvy consumers. The growing preference for hands-free operation in household environments continues to push innovation in voice chip accuracy and multilingual support.

Automotive Voice Assistant Integration Accelerates Market Penetration

Modern vehicles now incorporate an average of 3-4 voice-activated functions per unit, ranging from navigation to climate control. This automotive integration represents one of the fastest-growing segments for intelligent voice control chips, with vehicle manufacturers prioritizing driver safety through reduced manual controls. The technology’s ability to process commands in noisy environments while maintaining high accuracy rates has been particularly crucial for adoption. Recent advancements in noise cancellation algorithms and contextual understanding have further expanded application possibilities in the automotive sector.

➤ The Asian automotive market alone integrated approximately 45 million voice control units in 2023, demonstrating the technology’s rapid mainstream adoption.

MARKET RESTRAINTS

High Development Costs Create Barrier for Market Entry

The sophisticated nature of voice recognition technology requires substantial R&D investment, with average development cycles spanning 12-18 months per chip iteration. Small and medium-sized enterprises face particular challenges competing with established players who benefit from economies of scale. Cost factors include not only chip design but also the continuous machine learning improvements needed to maintain accuracy across dialects and languages. These financial demands have slowed innovation cycles in price-sensitive markets despite growing consumer demand.

Privacy Concerns Limit Consumer Adoption Rates

Data security issues surrounding voice-activated devices continue to impact market expansion. Approximately 38% of consumers express reluctance to adopt voice-controlled technology due to concerns about unauthorized audio collection and processing. Manufacturers must navigate complex regulatory landscapes regarding data storage and transmission while maintaining the responsiveness that users expect. European markets have proven particularly challenging with stringent GDPR compliance requirements adding approximately 15-20% to development costs for voice-enabled products.

MARKET OPPORTUNITIES

Healthcare Applications Present Untapped Potential

Voice-controlled medical devices represent a high-growth opportunity, particularly for elderly care and disability assistance applications. Current pilot programs demonstrate 92% accuracy in medication reminder systems and patient monitoring when using specialized voice chips. The healthcare sector’s need for hands-free operation in sterile environments and the growing telemedicine market create ideal conditions for voice technology integration. Regulatory approvals for medical-grade voice systems could unlock a market segment projected to reach $800 million by 2027.

Edge Computing Integration Enhances Market Potential

The shift toward edge processing in voice recognition reduces latency by 60-70% compared to cloud-based solutions, creating new possibilities for real-time applications. Manufacturers are developing chips with dedicated neural processing units that can handle complex voice commands locally without internet connectivity. This advancement addresses both privacy concerns and reliability issues while enabling usage in remote environments. The industrial sector shows particular interest for equipment operation in facilities where wireless connectivity remains limited or inconsistent.

MARKET CHALLENGES

Linguistic Complexity Creates Technical Hurdles

Developing chips that accurately process tonal languages and regional dialects remains a significant technical challenge. Mandarin Chinese speakers experience approximately 15% higher error rates compared to English in current voice recognition systems. The computational requirements for supporting multiple languages simultaneously also increase power consumption and chip size constraints. These linguistic barriers particularly affect markets in Southeast Asia and Africa where dialect variations are pronounced and literacy levels vary widely.

Supply Chain Disruptions Impact Production Timelines

The semiconductor shortage has delayed voice chip production by an average of 22 weeks across the industry, with lead times for certain components extending beyond nine months. This disruption comes at a critical growth period when consumer demand for voice-enabled devices continues to rise. Manufacturers face the dual challenge of securing wafer allocations while maintaining competitive pricing. The situation has prompted several companies to explore vertical integration strategies, though such moves require capital investments averaging $2-3 billion for new fabrication facilities.

INTELLIGENT VOICE CONTROL CHIP MARKET TRENDS

Expansion of AI and IoT Ecosystems Driving Adoption of Intelligent Voice Control Chips

The proliferation of Artificial Intelligence (AI) and Internet of Things (IoT) applications is significantly boosting the demand for intelligent voice control chips. These advanced semiconductor components enable seamless human-machine interaction, which is critical for smart home devices, automotive voice assistants, and industrial automation. The global market, valued at $6.68 billion in 2024, is projected to grow at a CAGR of 10.0%, reaching $12.8 billion by 2032. This growth is largely attributed to advancements in Natural Language Processing (NLP) algorithms and edge computing capabilities, allowing for faster and more accurate voice recognition even in noisy environments. Furthermore, the integration of machine learning in voice chips enhances contextual understanding, improving user experience across diverse applications.

Other Trends

Smart Home and Automotive Applications

Voice assistants in smart homes and automobiles have emerged as key growth drivers for intelligent voice control chips. With smart speakers and IoT-enabled appliances seeing a 35% annual increase in adoption, manufacturers are prioritizing energy-efficient and low-latency chip designs. Meanwhile, the automotive sector is incorporating voice-controlled infotainment and navigation systems, particularly in electric and autonomous vehicles. These chips not only improve driver safety but also offer predictive responses based on user behavior patterns. Additionally, advancements in far-field voice recognition have enabled hands-free operation even in high-background-noise environments, further accelerating market penetration.

Rising Demand for Edge-Based Processing in Consumer Electronics

The shift toward edge computing in consumer electronics is reshaping the intelligent voice control chip landscape. Unlike cloud-dependent solutions, edge-based voice processing enhances privacy and reduces latency, making it ideal for real-time applications. Companies are developing ultra-low-power System-on-Chip (SoC) designs with integrated neural processing units (NPUs) to handle complex voice commands locally. This trend is particularly prominent in wearable devices and smart locks, where battery efficiency and instant response times are critical. Furthermore, the growing sophistication of multilingual support in voice chips is opening new opportunities in emerging markets, where demand for localized voice interfaces is rising steadily.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define the Intelligent Voice Control Chip Market

The global intelligent voice control chip market is characterized by a dynamic mix of established semiconductor giants and emerging innovators, all competing to capitalize on the growing demand for voice-enabled devices. With the market projected to grow at a CAGR of 10.0% through 2032, reaching $12.8 billion, companies are aggressively investing in R&D to enhance speech recognition accuracy and power efficiency.

ARC and Global Unichip currently dominate the market with their vertically integrated solutions, combining hardware design with AI-powered voice processing algorithms. These leaders have secured 35% combined market share in 2024, particularly strong in consumer electronics and automotive applications where low-latency response is critical.

Meanwhile, Chinese manufacturers like Shenzhen Bnr Industry and Guangzhou Jiuxin Electronic Technology are rapidly gaining traction through cost-competitive offerings. These companies benefit from China’s robust semiconductor ecosystem and government support, capturing nearly 22% of the APAC market in price-sensitive segments.

The competitive intensity is further amplified by strategic moves from distributors such as Mouser Electronics and Kk International, who are expanding their voice chip portfolios through partnerships with multiple fabless semiconductor companies. This allows them to offer diverse solutions across OTP, FLASH, and MP3 decoding types.

List of Key Intelligent Voice Control Chip Companies

- ARC (U.S.)

- Mouser Electronics (U.S.)

- Global Unichip (Taiwan)

- Microdevice Technology (Japan)

- Shenzhen Bnr Industry Co., Limited (China)

- Guangzhou Jiuxin Electronic Technology Co., Ltd. (China)

- Dongguan City Zhigan Electronic Technology Co. (China)

- Kk International (India)

- WayTronic (China)

- WINKISON COMPANY LIMITED (Hong Kong)

- Mythic (U.S.)

- UC-Davis (U.S.)

Segment Analysis:

By Type

FLASH Type Segment Dominates the Market Due to High Flexibility and Reprogrammability

The intelligent voice control chip market is segmented based on type into:

- OTP Type

- Subtypes: Mask ROM-based, UV-EPROM-based, and others

- FLASH Type

- Subtypes: NOR Flash, NAND Flash, and others

- MP3 Decoding Type

- Others

By Application

Consumer Electronics Segment Leads Due to Growing Demand for Smart Home Devices

The intelligent voice control chip market is segmented based on application into:

- Consumer Electronics

- Subcategories: Smart speakers, Smart TVs, Smart home appliances

- Automobile

- Smart Lock

- Kids Toys

- Others

By Technology

AI-based Voice Recognition Shows Strong Growth Potential Due to Advancements in Machine Learning

The intelligent voice control chip market is segmented based on technology into:

- Speaker-dependent technology

- Speaker-independent technology

- AI-based voice recognition

- Hybrid systems

By End-user

Residential Sector Shows Increasing Adoption of Voice-controlled Smart Devices

The intelligent voice control chip market is segmented based on end-user into:

- Residential

- Commercial

- Industrial

- Automotive

- Healthcare

Regional Analysis: Intelligent Voice Control Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global intelligent voice control chip market, accounting for over 45% of revenue share in 2024. This leadership position is driven by China’s massive consumer electronics manufacturing ecosystem and Japan’s advanced semiconductor industry. Key factors include the presence of tech giants like Alibaba, Baidu, and Xiaomi integrating voice AI into smart devices, alongside government initiatives such as China’s “New Generation Artificial Intelligence Development Plan.” While cost-competitive OTP chips remain popular for budget devices, FLASH-type chips are gaining traction in premium products. Challenges include intellectual property disputes and supply chain vulnerabilities, but the region’s established semiconductor infrastructure and growing middle-class adoption of smart home products continue to fuel robust growth.

North America

North America represents the innovation hub for intelligent voice control technologies, driven by tech giants like Amazon, Google, and Apple. The region’s focus on R&D and early adoption of AI-powered devices has created premium demand for advanced FLASH and MP3 decoding chips. Strict data privacy regulations under CCPA and sector-specific standards push manufacturers toward secure, high-performance solutions. The automotive sector is emerging as a key growth driver, with voice-controlled infotainment systems becoming standard in 68% of new vehicles. However, higher production costs compared to Asian manufacturers and dependence on offshore fabrication pose challenges to domestic chip suppliers competing in this high-value market segment.

Europe

Europe’s intelligent voice control chip market is characterized by rigorous GDPR compliance requirements and strong demand for privacy-focused solutions. Germany leads in industrial applications, integrating voice control in smart manufacturing equipment, while the UK and France show strong adoption in consumer electronics. The region favors FLASH-type chips for their reprogrammability and security features, with particular growth in smart home and automotive applications. EU-funded projects like the Chips Act aim to reduce reliance on external suppliers, but current market dynamics still depend heavily on imports from Asian manufacturers. Environmental regulations also drive innovation in low-power consumption chip designs across the region.

South America

South America presents an emerging yet price-sensitive market for intelligent voice control chips, growing at approximately 8% CAGR. Brazil accounts for 60% of regional demand, primarily for low-cost OTP chips in consumer electronics and basic smart devices. Economic volatility and limited local semiconductor production constrain market expansion, but increasing smartphone penetration and developing smart city projects create opportunities. Manufacturers face challenges with currency fluctuations and complex import regulations, though partnerships with Chinese suppliers help maintain competitive pricing. The automotive aftermarket shows potential as voice control features gain popularity in mid-range vehicles across the region.

Middle East & Africa

The MEA region exhibits growing potential in selective high-growth markets, particularly the UAE, Saudi Arabia, and South Africa. Smart city initiatives in Dubai and Neom project investments are driving demand for voice-controlled IoT devices, favoring medium-tier FLASH chips. Religious and linguistic diversity creates unique localization challenges for voice recognition technologies. While the market remains small compared to other regions, increasing disposable incomes and government digital transformation programs support gradual adoption. Infrastructure limitations and low consumer awareness remain barriers, though telecom operators’ bundling strategies with smart devices are helping to overcome these challenges in urban centers.

Report Scope

This market research report provides a comprehensive analysis of the Global Intelligent Voice Control Chip Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 6,685 million in 2024 and is projected to reach USD 12,800 million by 2032, growing at a CAGR of 10.0%.

- Segmentation Analysis: Detailed breakdown by product type (OTP, FLASH, MP3 Decoding), application (Consumer Electronics, Automobile, Smart Lock, Kids Toys, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. Asia-Pacific leads in market share, driven by rapid adoption in consumer electronics and automotive sectors.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, and evolving industry standards such as low-power consumption and edge computing capabilities.

- Market Drivers & Restraints: Evaluation of factors driving market growth, including rising demand for smart home devices and voice assistants, along with challenges like supply chain constraints and regulatory hurdles.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global Intelligent Voice Control Chip Market?

-> Intelligent Voice Control Chip Market was valued at 6685 million in 2024 and is projected to reach US$ 12800 million by 2032, at a CAGR of 10.0% during the forecast period.

Which key companies operate in the Global Intelligent Voice Control Chip Market?

-> Key players include ARC, Global Unichip, Microdevice Technology, Mouser Electronics, WayTronic, and Shenzhen Bnr Industry Co., Limited, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for smart home devices, advancements in AI-based voice recognition, and increasing adoption in automotive infotainment systems.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by strong manufacturing capabilities and high consumer electronics demand, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration with edge AI, low-power chip designs, and multilingual voice recognition capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...