MARKET INSIGHTS

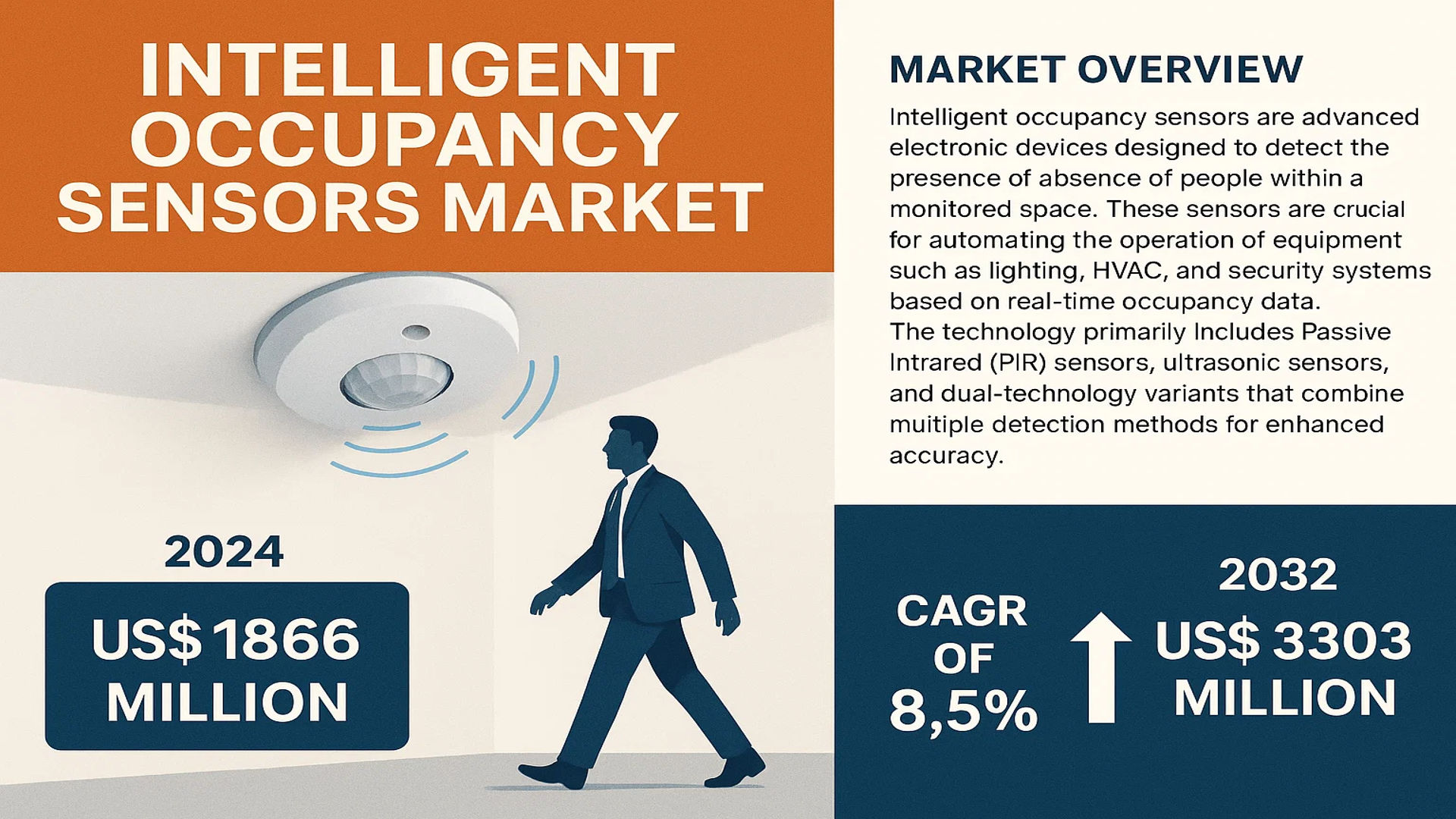

The global Intelligent Occupancy Sensors Market was valued at 1866 million in 2024 and is projected to reach US$ 3303 million by 2032, at a CAGR of 8.5% during the forecast period.

Intelligent occupancy sensors are advanced electronic devices designed to detect the presence or absence of people within a monitored space. These sensors are crucial for automating the operation of equipment such as lighting, HVAC, and security systems based on real-time occupancy data. The technology primarily includes Passive Infrared (PIR) sensors, ultrasonic sensors, and dual-technology variants that combine multiple detection methods for enhanced accuracy.

The market is experiencing robust growth driven by increasing global emphasis on energy efficiency and the rapid adoption of smart building solutions. Stringent government regulations promoting energy conservation, such as the Energy Policy Act in the U.S. and the Energy Performance of Buildings Directive in the EU, are significantly contributing to market expansion. Furthermore, technological advancements in IoT integration and the declining cost of sensor components are making these solutions more accessible. Key market players including Signify, Schneider Electric, and Honeywell collectively command approximately 40% of the global market share, continuously innovating to enhance product capabilities and expand their market presence.

MARKET DYNAMICS

MARKET DRIVERS

Global Energy Efficiency Mandates and Green Building Initiatives Accelerate Market Adoption

The implementation of stringent energy efficiency regulations worldwide serves as a primary catalyst for the intelligent occupancy sensors market. Governments and international bodies are increasingly mandating energy conservation measures in both commercial and residential buildings to reduce carbon footprints. Building codes such as ASHRAE 90.1 and various national standards now frequently require automatic lighting controls, including occupancy-based systems, in new constructions and major renovations. These sensors can reduce lighting energy consumption by an estimated 30% to 50% in commercial spaces by automatically turning off lights in unoccupied areas. The global push toward net-zero carbon buildings by 2050, supported by international agreements, further institutionalizes the adoption of these energy-saving technologies, creating a sustained demand driver across multiple regions.

Proliferation of Smart Building Infrastructure and IoT Integration Fuels Growth

The rapid expansion of smart building infrastructure represents a significant growth vector for intelligent occupancy sensors. These devices form a critical component of building automation systems, integrating seamlessly with IoT platforms to enable data-driven facility management. The global smart building market is projected to exceed $150 billion by 2026, with occupancy sensors serving as fundamental data collection points for space utilization analytics, predictive maintenance, and operational optimization. Modern sensors now incorporate multiple technologies—combining PIR, ultrasonic, and microwave detection—to achieve accuracy rates exceeding 95% in diverse environmental conditions. This technological evolution allows building managers to not only control lighting and HVAC systems but also to gather valuable occupancy pattern data that informs space planning, security protocols, and energy management strategies.

Rising Operational Cost Pressures and ROI Considerations Drive Commercial Adoption

Increasing operational expenses and the demonstrated return on investment are compelling commercial property owners to adopt intelligent occupancy sensors at an accelerated pace. Energy costs constitute approximately 25% of typical commercial building operating expenses, with lighting alone accounting for nearly 40% of total electricity consumption in office buildings. Occupancy sensors typically achieve payback periods of 2-3 years through energy savings, while also reducing maintenance costs by extending the lifespan of lighting systems. The post-pandemic focus on healthy buildings has further enhanced their value proposition, as these sensors can now integrate with ventilation systems to ensure adequate air changes based on actual occupancy levels, addressing both energy efficiency and indoor air quality concerns simultaneously.

MARKET CHALLENGES

Technical Limitations in Detection Accuracy and Environmental Adaptability Pose Implementation Challenges

Despite technological advancements, intelligent occupancy sensors continue to face technical challenges that affect their reliability and widespread adoption. False triggers and missed detections remain persistent issues, particularly in environments with complex layouts or varying occupancy patterns. PIR sensors struggle with detecting stationary occupants, while ultrasonic sensors can be affected by air currents and certain building materials. Dual-technology sensors improve reliability but increase system complexity and cost. Environmental factors such as temperature fluctuations, humidity, and acoustic interference can reduce detection accuracy by 15-20% in suboptimal conditions. These technical limitations require careful sensor selection, placement, and calibration, often necessitating professional installation and ongoing maintenance to maintain performance standards.

Other Challenges

Interoperability and Standardization Issues

The lack of universal communication protocols creates significant integration challenges across different building systems. While BACnet and LonWorks are established in building automation, the proliferation of IoT has introduced numerous wireless protocols including Zigbee, Z-Wave, and Bluetooth Low Energy, often creating compatibility issues. This fragmentation requires additional gateways and middleware, increasing implementation complexity and costs by approximately 20-30% for multi-system integrations.

Privacy Concerns and Data Security Risks

The data collection capabilities of advanced occupancy sensors raise privacy concerns regarding occupant monitoring. Organizations must navigate evolving data protection regulations such as GDPR and CCPA, which govern the collection and use of occupancy data. Cybersecurity vulnerabilities in connected sensor networks also present risks, with building management systems increasingly targeted for unauthorized access and data breaches.

MARKET RESTRAINTS

High Initial Investment and Perceived Complexity Deter Widespread Adoption

The substantial upfront costs associated with intelligent occupancy sensor implementation act as a significant market restraint, particularly for small and medium-sized enterprises and in price-sensitive regions. A comprehensive occupancy sensor system including hardware, installation, and integration with existing building management systems can require investments ranging from $2,000 to $15,000 per floor in commercial buildings, depending on system sophistication. Many decision-makers perceive the technology as complex to specify, install, and maintain, often requiring specialized expertise that may not be available in-house. This perception of complexity, combined with concerns about disruption during installation and ongoing maintenance requirements, causes hesitation among potential adopters despite the demonstrated long-term energy savings and operational benefits.

Economic Volatility and Construction Cycle Sensitivity Impact Market Growth

The intelligent occupancy sensors market demonstrates sensitivity to economic conditions and construction industry cycles, which can restrain growth during periods of economic uncertainty. Commercial real estate development and renovation activity, which drives a significant portion of sensor demand, typically declines during economic downturns as businesses delay capital investments. The market experienced a notable contraction of approximately 15-20% during recent global economic challenges as construction projects were postponed or canceled. Additionally, retrofit projects—which represent a substantial market segment—often face budget constraints during economic downturns, with building owners prioritizing essential maintenance over energy efficiency upgrades despite their long-term benefits.

MARKET OPPORTUNITIES

Integration with Advanced Analytics and AI-Powered Building Management Systems Creates New Value Propositions

The convergence of intelligent occupancy sensors with artificial intelligence and advanced analytics platforms presents substantial growth opportunities beyond basic energy savings. Modern sensor systems can now collect and process occupancy pattern data to optimize space utilization, predict maintenance needs, and enhance occupant comfort. AI algorithms can analyze historical occupancy data to predict building usage patterns with over 90% accuracy, enabling predictive HVAC operation and dynamic space allocation. This evolution transforms occupancy sensors from simple automation devices into valuable sources of business intelligence, allowing facility managers to reduce redundant space, optimize cleaning schedules, and improve workplace experience based on actual usage data rather than assumptions.

Expansion into Healthcare, Educational, and Industrial Applications Broadens Market Scope

Emerging applications in specialized vertical markets offer significant expansion opportunities for intelligent occupancy sensor manufacturers. The healthcare sector increasingly utilizes these sensors for patient flow monitoring, staff efficiency tracking, and infection control through optimized ventilation in response to occupancy levels. Educational institutions deploy sensors to enhance campus security and optimize energy use in variably occupied spaces like lecture halls and libraries. Industrial facilities implement occupancy-based lighting and climate control in warehouses and manufacturing areas where occupancy patterns are irregular. These specialized applications often command premium pricing due to their specific reliability requirements and integration needs, creating higher-margin opportunities for manufacturers who can develop sector-specific solutions.

Wireless and Self-Powered Sensor Technologies Enable Retrofit Market Expansion

Advancements in wireless communication and energy harvesting technologies are creating substantial opportunities in the building retrofit market, which represents approximately 60% of total construction activity in developed markets. Wireless occupancy sensors eliminate the need for extensive wiring, reducing installation costs by up to 40% compared to wired alternatives. Self-powered sensors utilizing kinetic, solar, or thermal energy harvesting further reduce installation barriers by eliminating battery replacement needs. These technological developments make occupancy sensor retrofits economically viable for a broader range of existing buildings, particularly in historical structures where wiring modifications are challenging or prohibited. The retrofit market expansion is further accelerated by increasingly attractive return on investment periods now frequently under two years due to these technological improvements.

INTELLIGENT OCCUPANCY SENSORS MARKET TRENDS

Integration with IoT and Smart Building Ecosystems Emerges as a Dominant Trend

The proliferation of the Internet of Things (IoT) is fundamentally reshaping the intelligent occupancy sensors landscape, driving a shift from standalone devices to interconnected components within larger smart building systems. This integration allows for the seamless collection and analysis of occupancy data, enabling predictive maintenance, dynamic space utilization optimization, and enhanced energy management. Modern sensors are increasingly equipped with wireless connectivity protocols like Zigbee, Bluetooth Mesh, and Wi-Fi, facilitating their incorporation into Building Management Systems (BMS) and Internet of Things platforms. This connectivity empowers facility managers to monitor building occupancy in real-time, adjust HVAC and lighting settings across entire floors based on actual usage patterns, and generate detailed reports on space efficiency. The value of this data extends beyond simple energy savings; it provides actionable insights for improving workplace productivity, streamlining cleaning schedules, and ensuring compliance with health and safety regulations, such as social distancing requirements that gained prominence in recent years. The trend is further accelerated by the global push towards smart city initiatives, where intelligent infrastructure is a cornerstone, creating a sustained demand for advanced, network-enabled occupancy sensing solutions.

Other Trends

Advancements in Sensor Fusion Technology

To overcome the limitations of single-technology sensors, such as the blind spots of Passive Infrared (PIR) sensors or the false triggers common in ultrasonic models, manufacturers are increasingly adopting dual-technology and multi-technology fusion approaches. Combining PIR with ultrasonic or microwave radar sensing significantly enhances detection accuracy and reliability, effectively eliminating false negatives and positives. This is particularly critical in complex environments like open-plan offices, restrooms, and conference rooms where precise occupancy detection is necessary for optimal system performance. The development of more sophisticated algorithms that can intelligently process data from multiple sensor inputs in real-time is a key innovation, allowing the system to distinguish between human movement and other environmental changes. This technological evolution is making intelligent occupancy sensors more robust and suitable for a wider range of applications, thereby expanding their market potential beyond traditional lighting control into advanced security, air quality monitoring, and space management systems.

Rising Demand for Energy Efficiency and Sustainability Mandates

Stringent global energy codes and a growing corporate emphasis on Environmental, Social, and Governance (ESG) criteria are powerful drivers for the adoption of intelligent occupancy sensors. Regulations such as the Title 24 in California and various LEED certification requirements mandate the use of automatic lighting controls in commercial buildings, directly fueling market growth. These sensors are one of the most effective and immediately deployable technologies for reducing a building’s energy footprint, with verified potential to cut lighting energy consumption by up to 30% and contribute significantly to HVAC savings by conditioning spaces only when occupied. Furthermore, businesses are leveraging their investments in these smart technologies to meet sustainability goals and enhance their green building credentials, which is increasingly important for corporate image and investor relations. The trend is not limited to new constructions; a substantial market is also developing in the retrofitting of existing buildings with modern occupancy sensing systems to improve efficiency and comply with modern standards, ensuring a continuous and diversified demand stream across both new and old infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Innovation and Strategic Expansion to Secure Market Position

The global intelligent occupancy sensors market exhibits a semi-consolidated structure, characterized by the presence of multinational corporations, specialized technology firms, and emerging regional players. This dynamic competition is driven by the escalating demand for energy-efficient building automation solutions across commercial, industrial, and residential sectors. Signify (formerly Philips Lighting) stands as a dominant force, largely due to its comprehensive portfolio of connected lighting systems and its extensive global distribution network. The company’s strong emphasis on IoT integration and sustainable solutions has solidified its leadership, particularly in the European and North American markets.

Schneider Electric and Honeywell also command significant market shares, a position bolstered by their deep expertise in building management systems and HVAC controls. Their growth is intrinsically linked to their ability to offer integrated solutions that combine occupancy sensing with broader building automation platforms. This approach is increasingly valued in large-scale commercial and infrastructure projects where system interoperability is critical.

Furthermore, these leading players are actively pursuing growth through strategic initiatives. Product innovation remains a primary focus, with companies investing heavily in R&D to enhance sensor accuracy, reduce false triggers, and develop multi-technology sensors that combine PIR, ultrasonic, and microwave detection. Geographical expansion into high-growth emerging markets, particularly in the Asia-Pacific region, is another key strategy being employed to capture new revenue streams.

Meanwhile, other significant participants like Johnson Controls and Siemens are strengthening their market presence through strategic acquisitions and partnerships. These moves are designed to expand their technological capabilities and product offerings, ensuring they remain competitive in an evolving landscape that increasingly values data-driven building insights and cloud connectivity.

List of Key Intelligent Occupancy Sensor Companies Profiled

- Signify (Netherlands)

- Schneider Electric (France)

- Honeywell International Inc. (U.S.)

- GE Current, a Daintree company (U.S.)

- Johnson Controls International plc (Ireland)

- Legrand (France)

- Crestron Electronics, Inc. (U.S.)

- Lutron Electronics Co., Inc. (U.S.)

- Acuity Brands, Inc. (U.S.)

- OPTEX CO., LTD. (Japan)

- Leviton Manufacturing Co., Inc. (U.S.)

- Enerlites Inc. (U.S.)

- Hubbell Incorporated (U.S.)

- ATSS (Advanced Technology Supplies & Services) (U.A.E.)

- Siemens AG (Germany)

Segment Analysis:

By Type

PIR (Passive Infrared) Sensors Segment Dominates the Market Due to Cost-Effectiveness and Widespread Adoption

The market is segmented based on type into:

- PIR (Passive Infrared) Sensors

- Ultrasonic Sensors

- Dual-technology Occupancy Sensors

- Others

By Application

Lighting Systems Segment Leads Due to Critical Role in Energy Efficiency and Building Automation

The market is segmented based on application into:

- Lighting Systems

- HVAC Systems

- Security and Surveillance Systems

- Others

By End User

Non-Residential Segment Leads Owing to High Adoption in Commercial and Industrial Infrastructure

The market is segmented based on end user into:

- Residential

- Commercial

- Industrial

By Technology

Wired Segment Holds Significant Share Due to Reliability in Critical Infrastructure Applications

The market is segmented based on technology into:

- Wired

- Wireless

Regional Analysis: Intelligent Occupancy Sensors Market

Asia-Pacific

The Asia-Pacific region dominates the global intelligent occupancy sensors market, accounting for approximately 40% of global market share. This leadership position is driven by massive infrastructure development, rapid urbanization, and strong government initiatives promoting smart city development and energy efficiency. China and India are the primary growth engines, with China’s ambitious 14th Five-Year Plan explicitly promoting building automation and energy conservation. The region’s manufacturing prowess also makes it a major production hub for sensor components, keeping costs competitive. While PIR sensors remain the most prevalent technology due to their cost-effectiveness, there is accelerating adoption of dual-technology and advanced IoT-integrated sensors in commercial buildings and new smart infrastructure projects across major metropolitan areas like Shanghai, Tokyo, and Singapore.

Europe

Europe represents a highly mature and technologically advanced market for intelligent occupancy sensors, holding a significant portion of global revenue. Stringent EU energy efficiency directives, including the Energy Performance of Buildings Directive (EPBD), mandate the use of automated control systems in new and renovated buildings, creating a robust regulatory-driven demand. Countries like Germany, France, and the U.K. are at the forefront, with a strong emphasis on integrating sensors into Building Automation Systems (BAS) and HVAC systems to achieve high energy savings. The market is characterized by a high adoption rate of sophisticated, networked sensors that comply with strict data privacy regulations like GDPR. Innovation focuses on enhancing accuracy and reducing false triggers, with leading European manufacturers investing heavily in R&D.

North America

The North American market is characterized by high adoption in the non-residential sector, driven by well-established energy codes like ASHRAE 90.1 and Title 24 in California, which incentivize or require occupancy-based controls. The United States is the largest national market within the region. High consumer awareness about energy savings, coupled with a strong trend towards smart homes and intelligent buildings, fuels steady growth. The market demands high-reliability products, leading to significant penetration of dual-technology sensors in office spaces, retail stores, and healthcare facilities to overcome the limitations of single-technology sensors. Recent infrastructure bills have also allocated funds for modernizing public buildings, which is expected to further stimulate demand for advanced sensor solutions.

South America

The South American market for intelligent occupancy sensors is in a developing phase, presenting a landscape of untapped potential alongside significant challenges. Economic volatility in key countries like Brazil and Argentina often constrains large-scale investments in building automation. While major commercial projects in urban centers are beginning to incorporate basic occupancy sensing for lighting control to reduce operational costs, adoption is largely limited to the premium segment. The lack of stringent and uniformly enforced energy efficiency regulations is a major barrier to widespread adoption. However, growing urbanization and increasing awareness of energy management among large corporations are slowly creating a foundation for future market growth, albeit from a relatively small base.

Middle East & Africa

The MEA region is an emerging market where growth is primarily concentrated in the Gulf Cooperation Council (GCC) countries, notably the UAE, Saudi Arabia, and Qatar. Ambitious smart city projects, such as Saudi Arabia’s NEOM and UAE’s Smart Dubai initiative, are driving the demand for advanced building management systems that incorporate intelligent occupancy sensors. These projects prioritize high-tech, sustainable solutions, creating a demand for premium, connected sensor products. However, the broader regional market growth is uneven. In many African nations, market development is hindered by infrastructural limitations, lower prioritization of energy efficiency, and budget constraints. The focus remains on high-value commercial and hospitality projects rather than widespread residential or general commercial use.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Intelligent Occupancy Sensors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, sensor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Intelligent Occupancy Sensors Market?

-> Intelligent Occupancy Sensors Market was valued at 1866 million in 2024 and is projected to reach US$ 3303 million by 2032, at a CAGR of 8.5% during the forecast period.

Which key companies operate in Global Intelligent Occupancy Sensors Market?

-> Key players include Signify, Schneider Electric, Honeywell, GE Current, Johnson Controls, Legrand, and Siemens, among others.

What are the key growth drivers?

-> Key growth drivers include energy conservation mandates, smart building adoption, and integration with IoT ecosystems.

Which region dominates the market?

-> Asia-Pacific and Europe collectively hold approximately 60% of the global market share.

What are the emerging trends?

-> Emerging trends include multi-technology sensor fusion, AI-powered predictive analytics, and applications in healthcare occupancy monitoring.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...