MARKET INSIGHTS

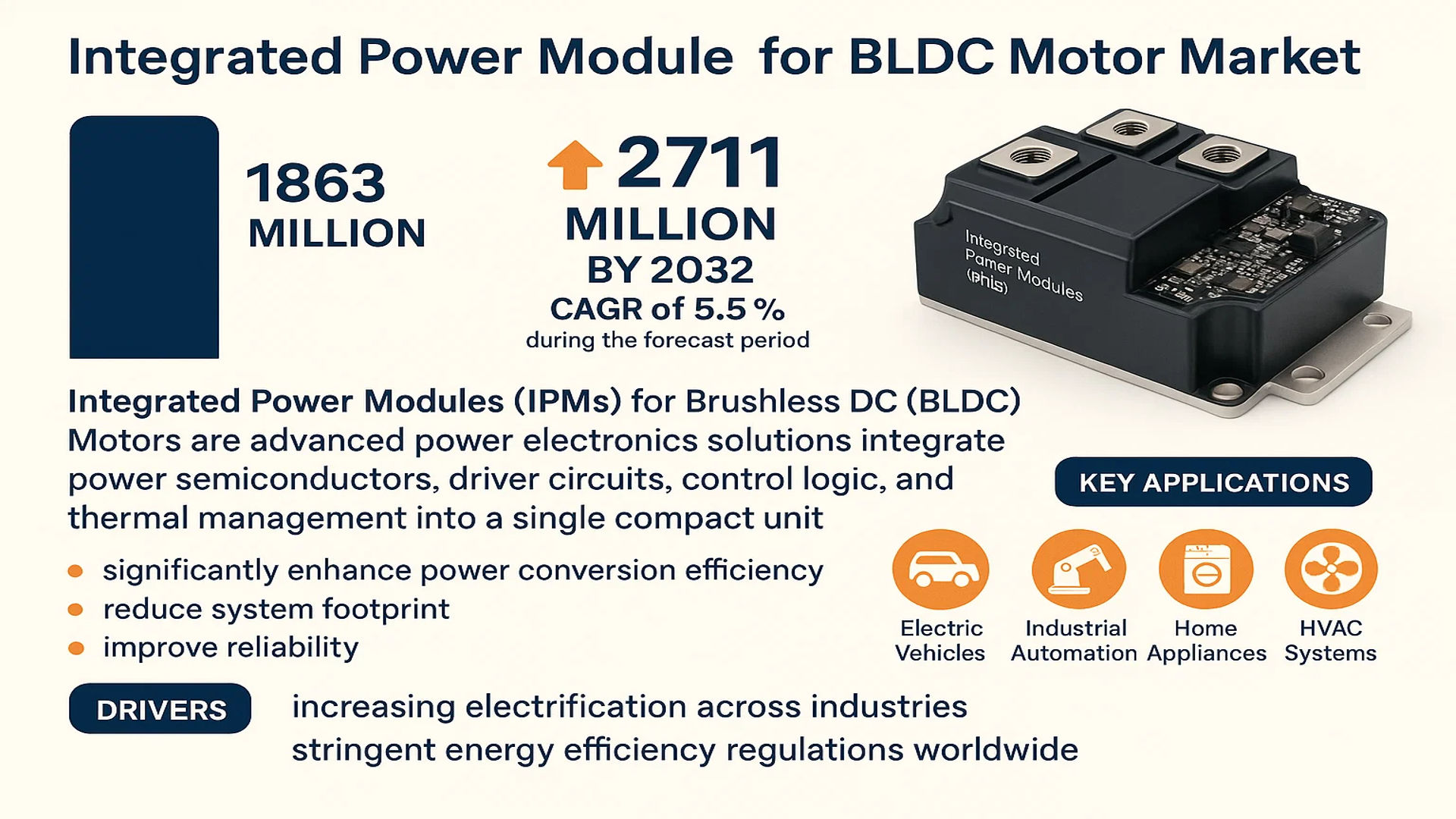

The global Integrated Power Module for BLDC Motor Market was valued at 1863 million in 2024 and is projected to reach US$ 2711 million by 2032, at a CAGR of 5.5% during the forecast period.

Integrated Power Modules (IPMs) for Brushless DC (BLDC) Motors are advanced power electronics solutions that integrate power semiconductors, driver circuits, control logic, and thermal management into a single compact unit. These modules significantly enhance power conversion efficiency while reducing system footprint and improving reliability compared to traditional discrete component designs. Key applications span electric vehicles, industrial automation, home appliances, and HVAC systems.

The market growth is driven by increasing electrification across industries and stringent energy efficiency regulations worldwide. Asia-Pacific currently dominates demand due to thriving EV production in China and growing industrial automation in Japan and South Korea. Major players like Infineon and STMicroelectronics are expanding production capacities to meet this demand, with Infineon reporting 22% year-over-year growth in its Power & Sensor Systems segment in Q1 2024. The automotive sector accounts for over 35% of IPM adoption as automakers transition to BLDC motors for improved vehicle efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of BLDC Motors in Electric Vehicles Accelerates Market Demand

The global shift toward electric mobility is creating unprecedented demand for BLDC motors and their integrated power modules. With electric vehicle production expected to surpass 40 million units annually by 2030, automakers are increasingly adopting BLDC technology for its superior efficiency, reliability, and power density compared to traditional brushed motors. Leading automotive manufacturers are integrating these modules into critical systems including powertrains, HVAC units, and power steering assemblies. The compact design and energy-efficient performance of integrated power modules make them ideal for EVs, where space optimization and battery range extension are paramount considerations.

Industry 4.0 Adoption Fuels Demand for Advanced Motor Control Solutions

As manufacturing facilities worldwide transition to smart factories, the demand for precision-controlled BLDC motors with intelligent power modules is surging. Modern industrial automation requires motors that can deliver precise speed control, energy efficiency, and real-time performance monitoring – all enabled by advanced integrated power modules. The industrial automation market growth, projected to maintain a CAGR of over 8% through 2030, is directly increasing adoption of these modules in robotics, conveyor systems, and CNC machinery. Integrated power modules significantly reduce system complexity while improving reliability in harsh industrial environments.

Energy Efficiency Regulations Drive Replacement of Traditional Motors

Stringent global energy efficiency standards are compelling manufacturers across industries to transition from conventional AC motors to BLDC alternatives. Regulations such as the EU’s Ecodesign Directive and similar initiatives in North America and Asia are eliminating less efficient motor technologies from the market. BLDC motors with integrated power modules typically achieve efficiency levels exceeding 90%, compared to 60-70% for traditional induction motors. This efficiency advantage, coupled with longer operational lifespans, is driving widespread replacement across appliance, HVAC, and industrial sectors, creating sustained demand for integrated power modules.

MARKET RESTRAINTS

Complex Thermal Management Requirements Limit Widespread Adoption

While integrated power modules offer numerous advantages, their high power density creates significant thermal challenges that restrain market growth. In demanding applications like electric vehicles and industrial machinery, these modules must dissipate substantial heat within constrained spaces. Maintaining optimal operating temperatures often requires expensive thermal interface materials and sophisticated cooling solutions, increasing total system costs. In automotive applications particularly, the need to maintain performance across temperature ranges from -40°C to 150°C presents ongoing engineering challenges that can delay product development cycles.

Material Shortages and Supply Chain Disruptions Impact Production

The semiconductor components critical to integrated power modules, including power MOSFETs and gate drivers, continue to face supply constraints across the electronics industry. The global chip shortage that began in 2020 still affects lead times for these specialized components, creating production bottlenecks for module manufacturers. Many power semiconductor fabs are operating at full capacity, yet demand continues to outstrip supply in key markets. These constraints are particularly acute for modules using wide bandgap semiconductors like SiC and GaN, where production capacity remains limited despite growing demand from high-performance applications.

MARKET CHALLENGES

Design Complexity and Certification Requirements Increase Development Costs

Developing integrated power modules for BLDC motors presents substantial engineering challenges that can deter market entry. These modules must meet diverse technical requirements including electrical isolation, electromagnetic compatibility, and mechanical robustness – all within increasingly compact form factors. Automotive-grade modules face particularly stringent certification processes, with qualification testing often taking 12-18 months and costing several million dollars. These barriers create significant challenges for smaller manufacturers and startups attempting to compete with established semiconductor companies in this market.

Other Challenges

Firmware Standardization Issues

The lack of standardized firmware interfaces across different module manufacturers complicates system integration and limits interoperability. Many modules require proprietary software tools and programming interfaces, forcing manufacturers to develop custom solutions for each module variant.

Legacy System Compatibility

Retrofitting existing motor systems with modern integrated power modules often requires complete system redesigns, creating resistance to adoption among operators of older industrial equipment and appliances.

MARKET OPPORTUNITIES

Emergence of Wide Bandgap Semiconductors Opens New Application Areas

The integration of silicon carbide (SiC) and gallium nitride (GaN) power devices into BLDC motor modules creates significant growth opportunities in high-performance applications. These advanced semiconductor materials enable modules to operate at higher voltages, frequencies, and temperatures while reducing energy losses by up to 50% compared to silicon-based solutions. Markets such as industrial motor drives, electric vehicle powertrains, and aerospace systems are rapidly adopting wide bandgap-enabled modules, driving premium pricing opportunities. Several leading manufacturers have recently introduced 800V capable modules specifically targeting next-generation EV platforms.

Expanding IoT and Predictive Maintenance Capabilities Create Value-Added Services

The integration of advanced diagnostics and connectivity features into power modules enables new service-based business models. Modern modules increasingly incorporate current sensing, temperature monitoring, and communication interfaces that support condition-based maintenance strategies. This capability is particularly valuable in industrial settings where unplanned motor downtime can cost thousands of dollars per hour. Manufacturers are developing cloud-connected modules that provide real-time performance analytics, predictive failure warnings, and remote configuration options, creating ongoing revenue streams beyond the initial hardware sale.

INTEGRATED POWER MODULE FOR BLDC MOTOR MARKET TRENDS

Increasing Demand for Energy-Efficient Motor Drives Fuels Market Growth

The global Integrated Power Module (IPM) for Brushless DC (BLDC) motor market is witnessing robust growth due to rising demand for energy-efficient motor drives across multiple industries. These modules integrate power semiconductors, gate drivers, and control circuitry into a single package, significantly improving power density and thermal management. The automotive sector, particularly electric vehicles (EVs) and hybrid electric vehicles (HEVs), accounts for over 35% of the market share as automakers increasingly adopt BLDC motors for their efficiency and compact design. Additionally, advancements in semiconductor materials like silicon carbide (SiC) and gallium nitride (GaN) are enhancing the performance and reliability of IPMs, further accelerating adoption.

Other Trends

Expansion of Industrial Automation

The rapid adoption of automation in manufacturing and robotics is driving demand for high-performance BLDC motor drives. Integrated power modules enable precise control, reduced energy consumption, and minimal heat generation, making them ideal for servo motors and conveyor systems. In 2024, the industrial sector contributed nearly 25% of the total market revenue, with Asia-Pacific leading due to increasing factory automation initiatives. The growing shift toward Industry 4.0 and smart factories further strengthens the role of IPMs in enhancing operational efficiency.

Technological Innovations in Power Electronics

The ability to integrate advanced features, such as overcurrent protection, temperature monitoring, and fault diagnostics, into compact power modules is revolutionizing motor drive applications. Leading semiconductor manufacturers are focusing on developing multi-chip modules (MCMs) that combine MOSFETs, IGBTs, and microcontroller units (MCUs) onto a single substrate, reducing system complexity. For instance, recent product launches have introduced modules with >95% efficiency, significantly cutting energy losses in HVAC systems and home appliances. These innovations are expected to push average selling prices (ASPs) down by 3-5% annually, increasing affordability for mid-tier applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Drive Innovation in BLDC Motor Power Modules

The global integrated power module for BLDC motor market features a mix of established semiconductor leaders and specialized electronics manufacturers. STMicroelectronics and Infineon Technologies currently dominate the landscape, collectively holding over 30% of market share through their comprehensive portfolios spanning automotive, industrial, and consumer applications. Their advantage lies in vertical integration capabilities and strong relationships with motor manufacturers across key regions.

Asian players like ROHM Semiconductor and Toshiba Electronic Devices have been gaining traction by offering cost-optimized solutions for high-volume applications such as home appliances and electric two-wheelers. These companies demonstrate particular strength in the APAC region, benefiting from localized supply chains and manufacturing bases in key markets including China and Japan.

Mid-tier competitors such as Diodes Incorporated and onsemi are carving out niches through specialized offerings. Diodes has seen success with its single-phase modules for HVAC systems, while onsemi’s focus on automotive-grade solutions positions it well for the growing EV market. Both companies have been actively expanding their production capacity to meet rising demand.

The competitive environment remains dynamic, with several notable recent developments:

- Infineon’s 2023 acquisition of a GaN power IC startup to enhance its high-efficiency module offerings

- ROHM’s strategic partnership with a leading Chinese EV manufacturer for customized power modules

- STMicroelectronics’ launch of its third-generation intelligent power modules featuring integrated current sensing

List of Key Integrated Power Module Manufacturers

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Diodes Incorporated (U.S.)

- ROHM Semiconductor (Japan)

- Renesas Electronics (Japan)

- Fuji Electric (Japan)

- Texas Instruments (U.S.)

- Microchip Technology (U.S.)

- onsemi (U.S.)

- Toshiba Electronic Devices (Japan)

As the market evolves towards higher power densities and improved thermal performance, companies are increasingly differentiating through advanced packaging technologies and software integration capabilities. The ability to offer complete motor control solutions, including companion microcontrollers and development tools, has become a key competitive factor particularly in industrial and automotive segments.

Segment Analysis:

By Type

Single-phase Modules Dominate Due to Widespread Adoption in Low-Power Applications

The market is segmented based on type into:

- Single-phase

- Subtypes: Compact IPMs, Standard IPMs

- Dual-phase

- Subtypes: High-performance IPMs, Medium-power IPMs

- Others

By Application

Automotive Sector Leads As BLDC Motors Gain Traction in Electric Vehicles

The market is segmented based on application into:

- Heat Pumps

- Home Appliances

- Automotive

- Others

Regional Analysis: Integrated Power Module for BLDC Motor Market

Asia-Pacific

Asia-Pacific dominates the global BLDC motor power module market, driven by rapid industrialization, expanding electric vehicle (EV) adoption, and strong government initiatives promoting energy efficiency. China leads regional growth, accounting for over 40% of regional demand, supported by its robust manufacturing sector and increasing investments in automation. Japan and South Korea also contribute significantly, with key players like Toshiba, ROHM, and Fuji Electric accelerating R&D in high-efficiency power modules. Meanwhile, India is emerging as a high-growth market due to rising demand for consumer appliances and electric two-wheelers. However, cost sensitivity remains a challenge for premium module adoption in price-conscious segments.

North America

The North American market is propelled by stringent energy regulations and the shift toward EVs, with the U.S. accounting for over 60% of regional revenue. Innovations in thermal management and compact designs are prioritized, particularly for automotive and HVAC applications. Major suppliers, including Texas Instruments and onsemi, are focusing on silicon carbide (SiC)-based modules to enhance performance. Canada and Mexico are witnessing gradual adoption, supported by cross-border supply chain integrations with U.S. manufacturers. The Inflation Reduction Act’s incentives for domestic semiconductor production are expected to further bolster market growth.

Europe

Europe’s market is driven by strict EU efficiency standards and the automotive industry’s transition to electrification. Germany, home to Infineon and STMicroelectronics, leads in technological advancements, particularly for dual-phase modules used in industrial automation. France and the U.K. are emphasizing renewable energy integrations, spurring demand for BLDC modules in heat pumps and wind turbines. While Western Europe remains the core market, Eastern Europe shows potential with increasing FDI in manufacturing. Compliance with RoHS and REACH regulations continues to shape product development strategies.

South America

The region exhibits moderate growth, with Brazil and Argentina as focal points. Industrial modernization and the replacement of outdated motor systems are key drivers. However, economic instability and reliance on imports constrain market expansion. Local players are gradually adopting single-phase modules for cost-effective solutions in agriculture and appliances. Chile and Colombia are exploring utility-scale applications, though infrastructural gaps limit short-term potential.

Middle East & Africa

This region is in the nascent stage, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is primarily tied to HVAC systems in commercial buildings and oil & gas applications. Limited local manufacturing capabilities result in heavy dependency on imports from Asia and Europe. Governments are introducing incentives for sustainable technologies, but market penetration remains slow due to fragmented supply chains and low awareness of advanced motor solutions.

Report Scope

This market research report provides a comprehensive analysis of the global Integrated Power Module for BLDC Motor market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,863 million in 2024 and is projected to reach USD 2,711 million by 2032, growing at a CAGR of 5.5%.

- Segmentation Analysis: Detailed breakdown by product type (Single-phase, Dual-phase, Others), application (Heat Pumps, Home Appliances, Automotive, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in motor control, semiconductor design trends, and evolving industry standards for power efficiency and thermal management.

- Market Drivers & Restraints: Evaluation of factors driving market growth (electrification trends, energy efficiency mandates) along with challenges (supply chain constraints, regulatory complexities).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Integrated Power Module for BLDC Motor Market?

->Integrated Power Module for BLDC Motor Market was valued at 1863 million in 2024 and is projected to reach US$ 2711 million by 2032, at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Integrated Power Module for BLDC Motor Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient motors, growth in electric vehicles, and increasing adoption of industrial automation.

Which region dominates the market?

-> Asia-Pacific leads in market share due to manufacturing hubs in China and Japan, while North America shows strong growth in automotive applications.

What are the emerging trends?

-> Emerging trends include higher integration of power electronics, smart motor control solutions, and wide-bandgap semiconductor adoption.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...