Integrated passive device capacitor for RF matching network Market Insights

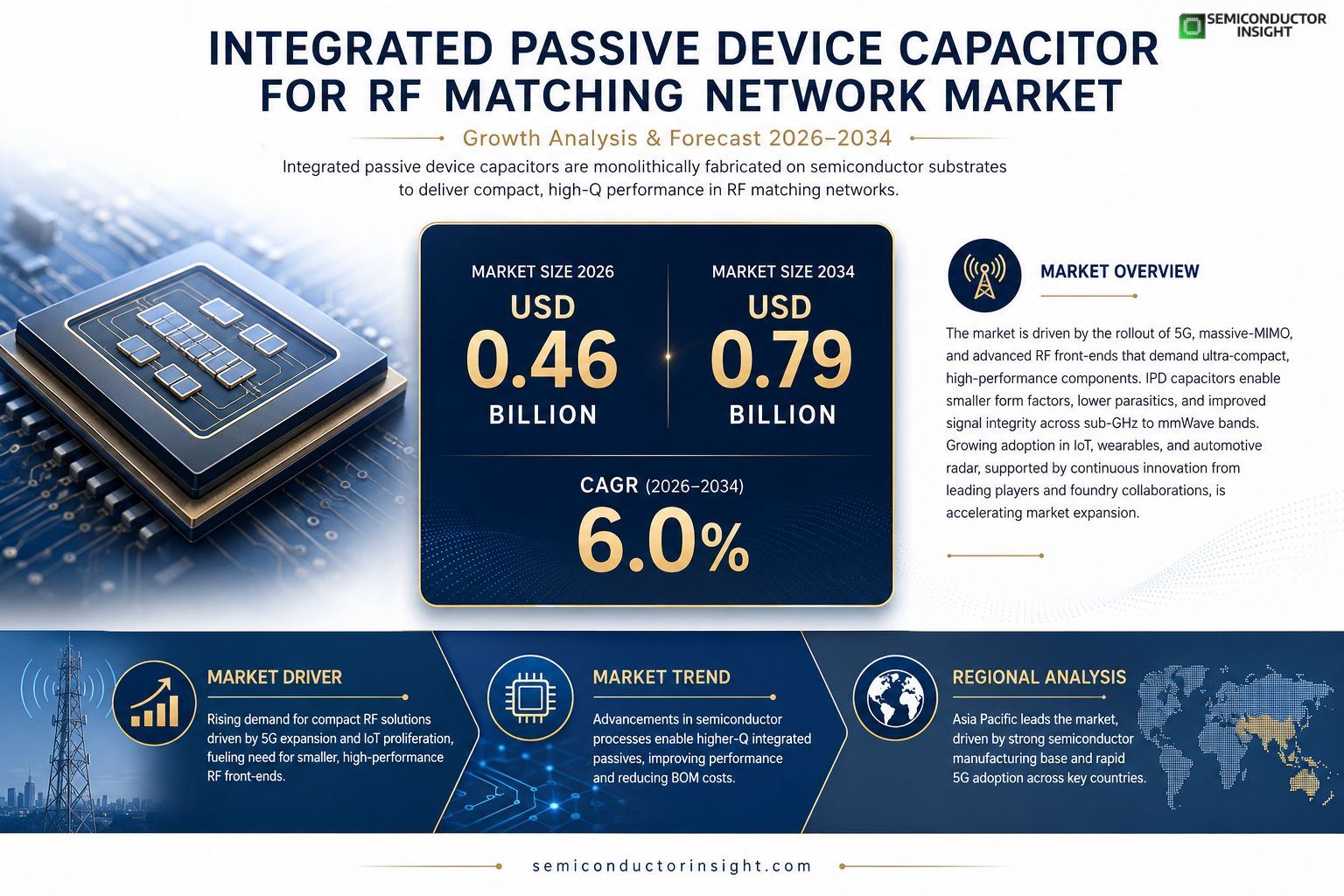

Integrated passive device capacitor for RF matching network market size was valued at USD 0.46 billion in 2025. The market is projected to grow from USD 0.46 billion in 2025 to USD 0.79 billion by 2034, exhibiting a CAGR of 6% during the forecast period.

Integrated passive device (IPD) capacitors are monolithically fabricated on semiconductor substrates and serve as compact, high‑Q components within radio‑frequency (RF) matching networks. By eliminating discrete passives, IPD capacitors enable tighter layout density, reduced parasitic inductance, and improved signal integrity across frequencies ranging from sub‑GHz IoT bands to millimeter‑wave 5G front‑ends.The market is experiencing accelerated growth because telecom operators are rolling out massive‑MIMO and beamforming arrays that demand ultra‑miniature RF front‑ends. Furthermore, the proliferation of wearable and automotive radar systems drives demand for low‑loss, temperature‑stable capacitors that can be co‑integrated with active silicon blocks. Key players such as Qorvo Inc., Skyworks Solutions, Murata Manufacturing, and TSMC’s advanced packaging division are expanding their IPD portfolios through strategic R&D investments and collaborations with foundries to address the stringent performance targets of next‑generation wireless standards.

MARKET DRIVERS

Rising Demand for Compact RF Solutions

The rapid expansion of 5G infrastructure and the proliferation of IoT devices have created a strong need for smaller, more efficient RF front‑ends. Integrated passive device capacitor for RF matching network Market suppliers are benefitting from design cycles that prioritize footprint reduction without compromising performance.

Advancements in Semiconductor Processes

Modern CMOS and SiGe processes now support higher‑Q passive elements, enabling designers to embed matching capacitors directly within the silicon die. This technological leap enhances signal integrity and reduces BOM costs, driving further adoption across automotive and consumer electronics.

➤ “Integrating passive capacitors can shrink overall module size by up to 30 % while delivering comparable loss performance.”

Overall, the convergence of miniaturization pressures and process innovations is accelerating growth, positioning Integrated passive device capacitor for RF matching network Market as a critical enabler for next‑generation wireless platforms.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Production

Although performance gains are evident, manufacturers face tight cost targets, especially in mass‑market smartphones. The added design complexity of integrated capacitors can increase wafer‑level expenses, challenging price‑competitive positioning.

Other Challenges

Manufacturing Complexity

Achieving consistent dielectric thickness and low‑loss characteristics across large wafers demands advanced metrology, which can affect yields and further elevate unit costs.

MARKET RESTRAINTS

Limited Frequency Band Coverage

Current integration techniques struggle to deliver high‑Q capacitors beyond 30 GHz, restricting use in emerging millimeter‑wave applications. This technical ceiling acts as a restraint for broader market penetration of Integrated passive device capacitor for RF matching network Market.

MARKET OPPORTUNITIES

Emerging Millimeter‑Wave Applications

Roll‑out of 5G‑advanced and automotive radar systems is creating a demand for RF components that operate efficiently at 60‑GHz and above. Innovations in material engineering and 3D integration are expected to unlock new opportunities, expanding the addressable market for integrated passive capacitors in matching networks.

Integrated passive device capacitor for RF matching network Market Trends

Rise of High‑Frequency Integrated Capacitors

Integrated passive device capacitor for RF matching network Market is benefitting from a rapid shift toward monolithic RF front‑ends. Growth drivers include the rollout of massive‑MIMO and beam‑forming antenna arrays, which require ultra‑miniature, low‑loss matching networks. By embedding capacitors directly on silicon, designers reduce parasitic inductance and achieve higher quality factors across sub‑GHz IoT bands and millimeter‑wave 5G spectra. The market valuation of USD 0.46 billion in 2025 and the projection of USD 0.79 billion by 2034 illustrate a steady compound increase of roughly 6 % per year. This trajectory reflects telecom operators’ demand for denser RF modules and the need for tighter layout density in base‑station chips. Additionally, the push toward integrated front‑ends in consumer smartphones is encouraging chipmakers to adopt IPD capacitors as part of System‑in‑Package solutions, which further compresses BOM cost and improves thermal management. Regulatory pressure for higher energy efficiency also favors monolithic passives, as they contribute to lower insertion loss across the entire RF chain.

Other Trends

Demand from Wearable and Automotive Radar

The expansion of wearable electronics and automotive radar systems is creating a parallel demand wave. Integrated passive device capacitors deliver temperature‑stable, low‑loss performance that meets the stringent power‑budget constraints of on‑body sensors while supporting the high‑frequency sweep required for collision‑avoidance radar. Co‑integration with active silicon blocks shortens signal paths, improving overall system reliability in harsh automotive environments. Market participants report a noticeable uptick in orders from OEMs seeking components that occupy less board area and can survive temperature cycles from –40 °C to 150 °C without detuning. This sub‑segment contributes to the broader market momentum by diversifying application portfolios beyond traditional telecom equipment. Furthermore, the rise of autonomous driving functions creates a need for radar modules that can operate continuously at millimeter‑wave frequencies, reinforcing the demand for stable IPD capacitors that maintain performance over long duty cycles.

Strategic Portfolio Expansion by Leading Suppliers

Strategic portfolio expansion by leading suppliers is reinforcing the market’s growth path. Companies such as Qorvo, Skyworks, Murata and TSMC’s advanced packaging arm have announced multi‑year R&D programs focused on higher‑Q IPD capacitors and 3D‑stacked integration techniques. These initiatives aim to reduce unit cost per picofarad and to provide design‑win support for upcoming 5G‑Advanced and beyond‑5G standards. Collaborative efforts with foundries enable the use of mature CMOS processes, shortening time‑to‑market for new capacitor libraries. As a result, Integrated passive device capacitor for RF matching network Market is expected to maintain a steady climb, with emerging use‑cases in satellite communications and edge‑computing radios adding incremental volume.

COMPETITIVE LANDSCAPEKey Industry Players

Integrated Passive Device (IPD) Capacitors for RF Matching Networks – Competitive Overview

The Integrated passive device (IPD) capacitor market is anchored by a few large semiconductor firms that leverage advanced silicon‑on‑insulator (SOI) and advanced packaging capabilities to deliver high‑Q, low‑loss components for massive‑MIMO and beamforming arrays. Qorvo Inc. leads the segment with a broad IPD portfolio that combines its RF front‑end expertise and in‑house foundry access, enabling rapid scaling from sub‑GHz IoT bands to millimeter‑wave 5G front‑ends. Skyworks Solutions follows closely, emphasizing collaborative R&D with foundry partners to embed IPD capacitors within its power‑amplifier and antenna‑tuned modules, thereby simplifying bill‑of‑materials and reducing parasitic inductance. Murata Manufacturing supplements the landscape with a strong emphasis on compact, temperature‑stable ceramic‑based IPD solutions, targeting automotive radar and wearable devices where size and reliability are paramount.Beyond the dominant leaders, a cluster of niche players contributes specialized technologies that enrich the overall ecosystem. STMicroelectronics and Texas Instruments exploit their analog‑RF heritage to introduce IPD capacitors tightly coupled with mixed‑signal blocks, appealing to sensor‑fusion applications. NXP Semiconductors and Infineon Technologies focus on automotive‑grade IPDs with rigorous qualification processes for radar and ADAS systems. Rohm Semiconductor, Analog Devices, and Broadcom provide customized IPD offerings for high‑performance compute‑centric RF front‑ends. Finally, emerging foundry‑centric entities such as TSMC’s Advanced Packaging division and Foundries facilitate fab‑as‑a‑service models, allowing smaller fabless firms to access IPD fabrication without substantial capital outlay.

List of Key Integrated Passive Device Capacitor Companies Profiled

- Qorvo Inc.

- Skyworks Solutions

- Murata Manufacturing

- STMicroelectronics

- Texas Instruments

- NXP Semiconductors

- Infineon Technologies

- Rohm Semiconductor

- Analog Devices

- Broadcom Inc.

- TSMC – Advanced Packaging

- Foundries

- MediaTek Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MIM IPD Capacitors are widely recognized as the leading sub‑type because they deliver ultra‑high quality factor and tight dimensional control. They enable:

|

| By Application |

|

5G mmWave Base‑Station Front‑Ends dominate this dimension because the networks demand ultra‑compact, low‑loss matching networks. Key qualitative drivers include:

|

| By End User |

|

Telecom Equipment Manufacturers are the primary end‑users, steering the market toward large‑scale adoption. Their qualitative priorities comprise:

|

| By Integration Level |

|

Monolithic IPD Capacitors emerge as the leading integration approach, delivering the most compelling qualitative advantages:

|

| By Performance Parameter |

|

High‑Q Capacitors are identified as the dominant performance driver because they directly influence system efficiency. Qualitative benefits include:

|

Regional Analysis: Integrated passive device capacitor for RF matching network Market

North America

The region leads in adopting silicon‑based passive integration, allowing capacitors to be embedded directly within RF transceiver chips, which shortens signal paths and improves overall network stability.

A resilient supply chain, anchored by domestic wafer fabs and component distributors, ensures consistent availability of high‑quality passive devices even during disruptions.

Harmonized standards across FCC and Industry Canada streamline certification, allowing faster market entry for novel capacitor architectures tailored to emerging RF bands.

Companies such as Skyworks, Qorvo, and Analog Devices drive innovation, focusing on high‑Q, low‑loss capacitors optimized for dense antenna array deployments.

European firms emphasize heterogeneous integration, merging passive capacitors with RF‑CMOS processes to meet stringent automotive safety standards.

Asia‑Pacific benefits from a dense network of component manufacturers, but logistics complexity can affect lead times for specialized passive devices.

South America faces fragmented standards, prompting local OEMs to adopt flexible design approaches that accommodate varied certification requirements.

The Middle East & Africa see growing participation from regional distributors and niche design houses catering to defense and satellite communications.

Europe

Europe’s Integrated passive device capacitor for RF matching network Market is shaped by stringent electromagnetic compatibility directives and a strong focus on automotive electrification. Manufacturers prioritize robust, temperature‑stable capacitors to meet the rigorous reliability expectations of the automotive sector, while telecom providers seek components that support the rollout of private 5G networks across major cities. Collaborative initiatives under the European Semiconductor Alliance foster shared research, driving incremental improvements in dielectric materials and miniaturization techniques. The region’s mature design ecosystem, supported by a dense cluster of simulation software providers, helps engineers optimize passive networks for high‑frequency applications without excessive component count, sustaining Europe’s position as a significant, though secondary, market contributor.

Asia‑Pacific

The Asia‑Pacific region exhibits rapid growth in Integrated passive device capacitor for RF matching network Market, propelled by expansive mobile infrastructure upgrades and burgeoning IoT deployments. Countries such as China, South Korea, and Japan invest heavily in advanced packaging and wafer‑level integration, enabling higher component density within limited board real‑estate. While cost sensitivity remains high, manufacturers balance price with performance by adopting new dielectric compounds that deliver low loss at millimeter‑wave frequencies. Regional trade shows emphasize knowledge exchange, accelerating the diffusion of best practices across the supply chain. Despite occasional supply bottlenecks, the region’s scale and manufacturing agility foster an environment conducive to continuous innovation.

South America

In South America, market dynamics for Integrated passive device capacitors are influenced by a mix of telecommunications expansion and emerging defense projects. The focus is on adaptable passive solutions that can be quickly re‑engineered to support diverse frequency bands used in rural connectivity initiatives. Local OEMs often collaborate with North American partners to access cutting‑edge design libraries, ensuring that products meet performance benchmarks while remaining cost‑effective. Regulatory frameworks are evolving, encouraging broader adoption of standardized RF components that simplify certification across multiple national markets.

Middle East & Africa

The Middle East & Africa region is gradually embracing Integrated passive device capacitor for RF matching network Market, driven primarily by satellite communications, defense modernization, and the rollout of 5G pilot projects in urban hubs. Stakeholders prioritize passive components with high reliability under extreme temperature conditions common in desert environments. Partnerships with European and North American technology firms enable regional players to integrate advanced capacitor designs into localized RF subsystems. While overall market size remains modest, strategic investments in research collaborations signal a growing commitment to developing indigenous capabilities for high‑frequency passive networks.

Report Scope

This market research report provides a comprehensive analysis of the Integrated passive device capacitor for RF matching network Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Integrated passive device capacitor for RF matching network Market?

-> Integrated passive device capacitor for RF matching network Market was valued at USD 0.46 billion in 2025 and is expected to reach USD 0.79 billion by 2034, reflecting a CAGR of 6% during the forecast period.

Which key companies operate in Integrated passive device capacitor for RF matching network Market?

-> Key players include Qorvo Inc., Skyworks Solutions, Murata Manufacturing, and TSMC, among others.

What are the key growth drivers?

-> Key growth drivers include deployment of massive‑MIMO and beamforming arrays by telecom operators, and rising demand for wearable and automotive radar systems that require low‑loss, temperature‑stable IPD capacitors.

Which region dominates the market?

-> The market is ly balanced, with strong activity across North America, Europe, and Asia‑Pacific, the latter showing the fastest growth due to extensive 5G infrastructure roll‑out.

What are the emerging trends?

-> Emerging trends include greater integration of IPD capacitors within system‑on‑chip (SoC) designs, increased focus on ultra‑low‑loss materials, and co‑development of IPD technologies with advanced packaging solutions for next‑generation 5G and beyond.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...