MARKET INSIGHTS

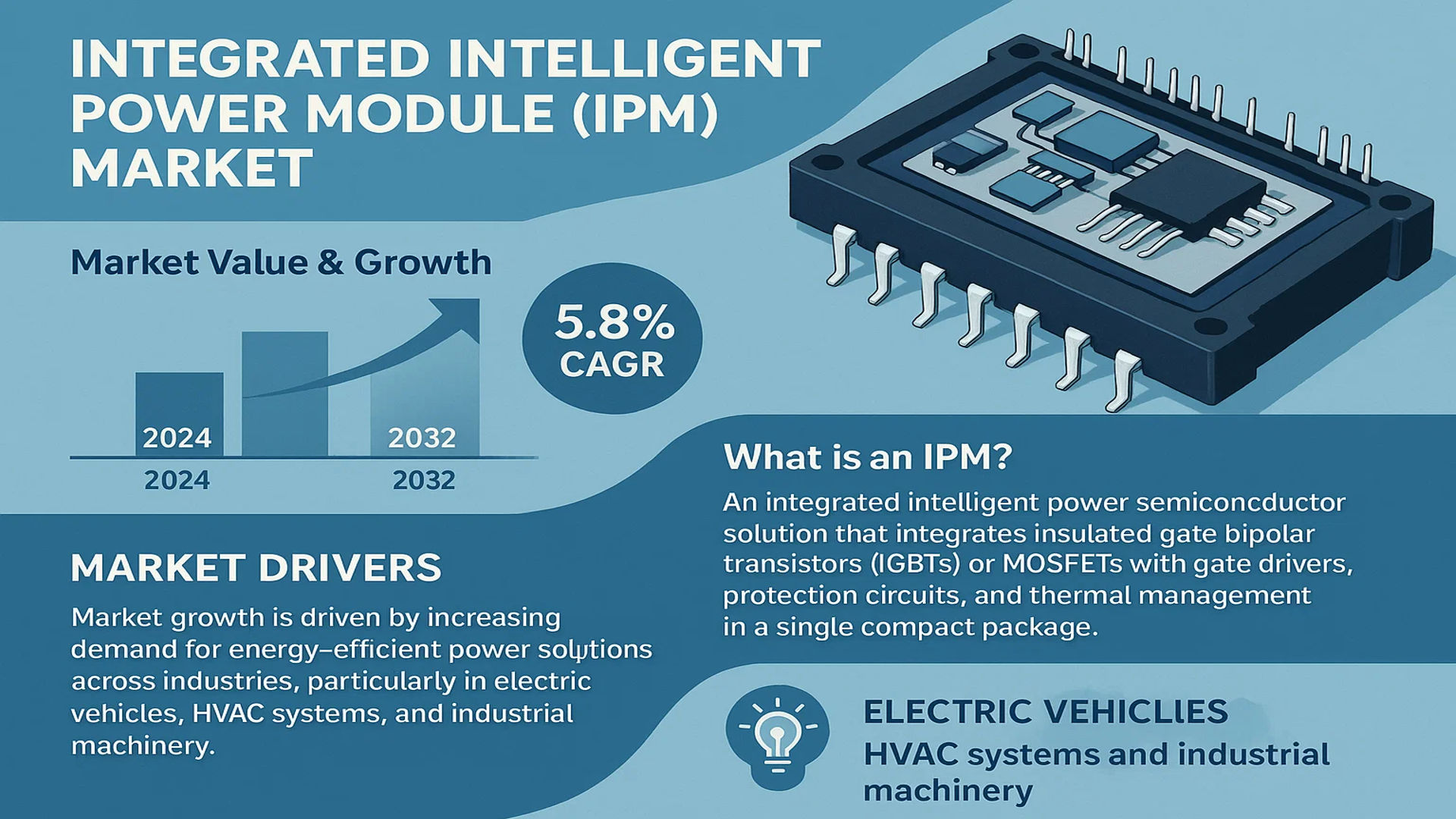

The global Integrated Intelligent Power Module (IPM) Market was valued at 5383 million in 2024 and is projected to reach US$ 7720 million by 2032, at a CAGR of 5.8% during the forecast period.

An Integrated Intelligent Power Module (IPM) is a high-performance power semiconductor solution that integrates insulated gate bipolar transistors (IGBTs) or MOSFETs with gate drivers, protection circuits, and thermal management in a single compact package. These modules are widely used in motor drives, industrial automation, consumer appliances, and renewable energy systems due to their efficiency, reliability, and space-saving design. IPMs reduce system complexity by incorporating built-in protections against short-circuit, overcurrent, and overtemperature conditions, making them ideal for demanding power electronics applications.

The market growth is driven by increasing demand for energy-efficient power solutions across industries, particularly in electric vehicles, HVAC systems, and industrial machinery. Asia-Pacific dominates the market due to strong manufacturing presence and rapid industrialization. Recent technological advancements, such as wide-bandgap semiconductors (SiC and GaN), are further enhancing IPM performance, enabling higher power density and thermal stability. Key players like Infineon Technologies, Mitsubishi Electric, and STMicroelectronics are investing heavily in R&D to develop next-generation IPMs, supporting the market’s expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Power Electronics Fuels IPM Market Growth

The global push toward energy efficiency across industries is accelerating adoption of Integrated Intelligent Power Modules (IPMs). These modules achieve up to 30% higher energy efficiency compared to discrete power components, making them indispensable for modern power management systems. The industrial sector alone accounts for nearly 40% of IPM applications, driven by automation trends and the need for compact, high-performance motor control solutions. With governments worldwide implementing stricter energy regulations, such as the EU’s Ecodesign Directive, IPMs are becoming the preferred solution for achieving compliance while maintaining operational performance.

Electric Vehicle Revolution Creates Significant Demand Surge

The rapid electrification of transportation presents a substantial growth opportunity for IPM manufacturers. Electric vehicle production is projected to increase at a compound annual growth rate of over 25% through 2030, with each EV requiring multiple IPMs for traction inverters, onboard chargers, and auxiliary systems. Major automotive manufacturers are forming strategic partnerships with semiconductor companies to secure IPM supply, with recent contracts valued at several billion dollars collectively. The shift toward 800V battery systems in next-generation EVs further intensifies demand for advanced IPMs capable of handling higher voltages while maintaining efficiency.

Renewable Energy Expansion Drives Adoption in Power Conversion Systems

Global renewable energy capacity additions reached record levels in recent years, with solar and wind installations requiring sophisticated power conversion technologies. IPMs have become critical components in solar inverters and wind turbine converters, offering superior reliability and power density. The wind power generation segment now represents approximately 18% of the total IPM market, with growth expectations exceeding the overall market average. Furthermore, the increasing installation of grid-scale battery storage systems creates additional demand for IPMs in bidirectional power conversion applications.

MARKET CHALLENGES

Thermal Management Concerns Pose Technical Hurdles

As IPMs handle higher power levels in increasingly compact form factors, thermal dissipation becomes a critical challenge. Power densities exceeding 100W/cm² require advanced cooling solutions that can add 15-20% to system costs. The industry faces particular difficulties in electric vehicle applications where ambient temperatures can reach 85°C, pushing device junction temperatures dangerously close to operational limits. While new packaging technologies like silver sintering offer improvements, their adoption remains limited by higher manufacturing costs and specialized equipment requirements.

Supply Chain Vulnerabilities Impact Production Reliability

The IPM market remains susceptible to semiconductor supply chain disruptions, with lead times for certain components still exceeding 52 weeks as of early 2024. A single IPM may incorporate over 20 different semiconductor dies, making procurement particularly challenging. The concentration of silicon carbide wafer production capacity in a limited number of facilities creates additional supply risks. These challenges have led some manufacturers to implement dual-sourcing strategies, though qualifying alternative suppliers can extend development cycles by 6-12 months.

Design Complexity Increases Development Costs

While IPMs simplify end-system design, their own development requires substantial R&D investment. Designing a new IPM platform can cost between $5-10 million, with electromagnetic compatibility testing and reliability validation accounting for nearly 30% of development expenses. The need to support multiple voltage ratings and package configurations within product families further escalates development costs. These challenges particularly affect smaller manufacturers attempting to compete with established players that benefit from economies of scale.

MARKET RESTRAINTS

High Initial Costs Limit Adoption in Price-Sensitive Markets

IPM solutions typically command a 40-60% price premium over discrete component implementations, creating adoption barriers in cost-sensitive applications. Consumer appliance manufacturers, for instance, often opt for discrete designs despite the increased board space requirements. In developing economies where price sensitivity is particularly acute, IPM penetration remains below 20% in many application segments. This pricing challenge persists even as production scales up, because material costs account for over 65% of IPM manufacturing expenses.

Technical Expertise Shortage Slows Market Expansion

The specialized nature of IPM system integration requires engineers with expertise in power electronics, thermal management, and application-specific control algorithms. The global shortage of such professionals is estimated at over 50,000 positions, creating implementation bottlenecks. Small and medium enterprises often lack the resources to attract qualified personnel, forcing them to rely on external design houses that can double development costs. Educational institutions are struggling to keep pace with industry needs, with only about 30% of engineering programs offering dedicated power electronics coursework.

Legacy System Inertia Delays Technology Transition

Many industrial facilities continue operating equipment designed for discrete power components, with upgrade cycles typically spanning 10-15 years. This inertia slows IPM adoption despite their technical advantages. In some cases, the redesign required to implement IPMs can cost more than the components themselves, particularly when addressing electromagnetic interference issues or modifying cooling systems. The automotive sector shows slightly faster adoption rates, but even here, design cycles of 3-5 years limit how quickly new power architectures can be implemented.

MARKET OPPORTUNITIES

Wide Bandgap Semiconductor Integration Opens New Frontiers

The incorporation of silicon carbide and gallium nitride technologies into IPMs promises to revolutionize power electronics performance. SiC-based IPMs already demonstrate 50% lower switching losses compared to silicon equivalents at higher voltage ratings. The industrial motor drive segment stands to gain particular benefits, with potential system efficiency improvements up to 5 percentage points. As production costs for wide bandgap semiconductors decline—projected to reach cost parity with silicon by 2027—their integration into mainstream IPMs will accelerate.

Smart Manufacturing Creates Demand for Intelligent Power Solutions

Industry 4.0 initiatives are driving adoption of IPMs with built-in condition monitoring and predictive maintenance capabilities. Newer IPM generations incorporate temperature, current, and voltage sensors with digital interfaces, enabling real-time health monitoring. This functionality proves particularly valuable in critical applications such as data center power supplies and medical equipment, where unscheduled downtime costs can exceed $10,000 per minute. The convergence of power electronics with industrial IoT creates opportunities for value-added services and long-term customer relationships.

Emerging Applications in Aerospace and Defense Present Growth Potential

More electric aircraft architectures and naval electrification programs are creating specialized demand for ruggedized IPMs. These applications require components that can operate reliably in extreme environments while meeting stringent safety certifications. The aerospace sector presents particularly attractive margins, with IPMs for flight-critical systems commanding prices 3-5 times higher than commercial equivalents. Defense budgets allocating increasing shares to electrification—currently around 15% of total R&D spending in major markets—will further stimulate this niche segment.

INTEGRATED INTELLIGENT POWER MODULE (IPM) MARKET TRENDS

Growth of Electric Vehicles (EVs) and Renewable Energy Systems Drive IPM Adoption

The global Integrated Intelligent Power Module (IPM) market is experiencing significant growth, projected to reach $7.72 billion by 2032, with a CAGR of 5.8% from 2024. One of the key drivers is the rapid expansion of the electric vehicle (EV) industry, where IPMs play a crucial role in motor control and inverter systems. EV sales are expected to surpass 30 million units annually by 2030, further accelerating the demand for efficient power management solutions. Additionally, the rise of renewable energy systems, particularly solar and wind power, is increasing IPM adoption for power conversion and grid integration, enhancing overall energy efficiency.

Other Trends

Advancements in Wide-Bandgap Semiconductors (SiC & GaN)

The integration of Silicon Carbide (SiC) and Gallium Nitride (GaN) technologies within IPMs is revolutionizing power efficiency and thermal performance. These materials offer higher switching frequencies, lower power losses, and improved heat dissipation compared to traditional silicon-based modules. Major semiconductor manufacturers are investing heavily in these technologies, leading to IPMs that can operate at higher voltages while maintaining compact form factors, making them essential for applications such as industrial automation and high-power inverters.

Industrial Automation and Smart Manufacturing Adoption

The increasing automation in manufacturing industries is fueling the demand for high-performance IPMs capable of precise motor control and energy efficiency. Factories are implementing smart manufacturing practices, leveraging IPMs to optimize servo motors, robotic arms, and conveyor systems. With the global industrial automation market expected to grow at 9% annually, the need for reliable and integrated power solutions will continue to rise. Furthermore, advancements in IoT-enabled power modules are enhancing real-time monitoring and predictive maintenance, reducing downtime in critical industrial operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Expand Technological Capabilities to Maintain Market Position

The global Integrated Intelligent Power Module (IPM) market features a mix of established semiconductor giants and emerging specialists, creating a dynamic yet moderately consolidated competitive environment. Infineon Technologies currently leads the market with approximately 22% revenue share in 2024, driven by its comprehensive portfolio of IGBT and MOSFET-based IPM solutions across automotive, industrial, and consumer applications. The company’s recent $2 billion investment in SiC and GaN technologies positions it strongly for next-generation power module development.

Mitsubishi Electric and Fuji Electric maintain significant market presence through their vertically integrated manufacturing capabilities and strong foothold in Asian markets, accounting for nearly 18% and 12% of global IPM sales respectively. Both Japanese firms continue to capitalize on the rapid electrification trends in automotive and industrial sectors, with Mitsubishi recently launching its 7th-generation NX-Series IPMs featuring 10% higher power density than previous iterations.

The market also sees increasing competition from ROHM Semiconductor and STMicroelectronics, who are gaining traction through innovative packaging technologies and strategic partnerships with EV manufacturers. ROHM’s recent collaboration with a major Chinese automaker for bespoke IPM solutions highlights this trend, while ST’s ACEPACK power modules demonstrate the industry shift toward more compact form factors.

Chinese manufacturers like Hangzhou Silan Microelectronics and China Resources Microelectronics are emerging as formidable regional players, supported by government initiatives in semiconductor independence. These companies are rapidly closing the technology gap while competing aggressively on price, particularly in the home appliance and industrial motor control segments.

List of Key Integrated Intelligent Power Module Manufacturers

- Infineon Technologies (Germany)

- Mitsubishi Electric (Japan)

- STMicroelectronics (Switzerland)

- Fuji Electric (Japan)

- ON Semiconductor (U.S.)

- ROHM Semiconductor (Japan)

- Sanken Electric (Japan)

- Semikron Danfoss (Germany)

- Renesas Electronics (Japan)

- Texas Instruments (U.S.)

- Hangzhou Silan Microelectronics (China)

- China Resources Microelectronics (China)

- Zhuhai GREE Xinyuan Electronic (China)

Segment Analysis:

By Type

IGBT-Based IPM Segment Dominates Due to High Power Handling and Efficiency in Industrial Applications

The market is segmented based on type into:

- IGBT Based IPM

- Subtypes: Low-voltage, Medium-voltage, High-voltage variants

- MOSFET Based IPM

- Subtypes: Silicon, SiC (Silicon Carbide), GaN (Gallium Nitride) variants

- Others

By Application

Industrial Segment Leads Market Due to Widespread Automation and Motor Control Requirements

The market is segmented based on application into:

- Home Appliances

- Subtypes: Air conditioners, Refrigerators, Washing machines

- Industrial

- Subtypes: Robotics, CNC machines, Servo drives

- New Energy Vehicles

- Subtypes: Battery management systems, Traction inverters

- Wind Power Generation

- Others

By Protection Feature

Advanced Protection Segment Grows Rapidly with Increasing Demand for System Reliability

The market is segmented based on protection features into:

- Basic Protection IPM

- Advanced Protection IPM

- Subtypes: Overcurrent, Overtemperature, Short-circuit, Under-voltage protection

By Power Rating

Medium Power Segment Holds Significant Share for Balanced Performance in Multiple Applications

The market is segmented based on power rating into:

- Low Power (Up to 10kW)

- Medium Power (10kW-100kW)

- High Power (Above 100kW)

Regional Analysis: Integrated Intelligent Power Module (IPM) Market

Asia-Pacific

The Asia-Pacific region dominates the global IPM market, accounting for over 45% of total revenue in 2024. This leadership stems from China’s robust electronics manufacturing sector, Japan’s advanced semiconductor industry, and South Korea’s thriving consumer appliance market. Key factors driving growth include accelerating EV adoption (China accounted for 59% of global EV sales in 2023), government initiatives like India’s Production Linked Incentive scheme for semiconductor manufacturing, and increasing industrial automation across ASEAN nations. While IGBT-based IPMs remain prevalent, there’s growing demand for MOSFET variants in low-power applications. However, intense price competition among domestic manufacturers like Hangzhou Silan Microelectronics and international players creates margin pressures.

North America

North America’s IPM market is characterized by high-value, technologically advanced solutions, with the U.S. contributing over 80% of regional demand. The region benefits from strong R&D investments in wide-bandgap semiconductors (SiC/GaN IPMs grew 28% YoY in 2023), stringent energy efficiency standards (DOE regulations), and thriving renewable energy projects. Major applications include data center power systems and EV charging infrastructure, with companies like Onsemi and Texas Instruments introducing IPMs with higher thermal stability (up to 175°C operating temperature). The Canadian market shows promising growth in wind power applications, though dependence on imports creates supply chain vulnerabilities.

Europe

Europe’s IPM market is propelled by strict energy efficiency directives (EU Ecodesign 2021) and rapid electrification across automotive and industrial sectors. Germany leads with its strong automotive OEM base adopting IPMs for 48V mild hybrid systems, while Italy’s appliance manufacturers drive demand for compact IPM solutions. The region shows increasing preference for ROHM and Infineon’s automotive-grade IPMs, particularly in torque control applications. However, higher component costs and complex certification processes (particularly for industrial IPMs) somewhat limit market penetration in Eastern Europe.

Middle East & Africa

This emerging market is witnessing gradual IPM adoption, primarily in HVAC systems and oil/gas industrial applications. The UAE and Saudi Arabia account for 68% of regional demand, driven by smart city projects and diversification from oil-based economies. While most IPMs are imported, localized assembly is increasing through partnerships like STMicroelectronics’ collaboration with Egyptian electronics manufacturers. Market growth faces challenges including high temperature operating constraints (necessitating expensive cooling solutions) and limited technical expertise in power electronics maintenance.

South America

South America’s IPM market remains relatively small but shows steady growth in Brazil’s appliance sector and Argentina’s renewable energy projects. Cost sensitivity leads to preference for refurbished or lower-specification IPMs, though multinationals like WEG are driving adoption in industrial motor drives. The region struggles with currency volatility (impacting import costs) and insufficient local testing facilities, causing longer product qualification cycles. However, Chile’s push for solar energy and Brazil’s HVAC market expansion (projected 7.2% CAGR through 2028) present compelling opportunities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Integrated Intelligent Power Module (IPM) markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global IPM market was valued at USD 5,383 million in 2024 and is projected to reach USD 7,720 million by 2032, growing at a CAGR of 5.8%.

- Segmentation Analysis: Detailed breakdown by product type (IGBT-based and MOSFET-based IPMs), technology, application (home appliances, industrial, new energy vehicles, wind power generation), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with over 45% market share in 2024, driven by manufacturing hubs in China, Japan, and South Korea.

- Competitive Landscape: Profiles of 20+ leading market participants including Infineon Technologies, Mitsubishi Electric, STMicroelectronics, and ON Semiconductor, analyzing their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of wide-bandgap semiconductors (SiC/GaN), advanced packaging techniques, and integration of AI for predictive maintenance in power modules.

- Market Drivers & Restraints: Analysis of electrification trends, renewable energy adoption, and EV proliferation versus supply chain challenges and geopolitical factors affecting semiconductor supply.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, automotive OEMs, industrial automation providers, and investors on emerging opportunities in the IPM value chain.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory filings, trade associations, and proprietary databases to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Integrated Intelligent Power Module (IPM) Market?

-> Integrated Intelligent Power Module (IPM) Market was valued at 5383 million in 2024 and is projected to reach US$ 7720 million by 2032, at a CAGR of 5.8% during the forecast period.

Which key companies operate in Global IPM Market?

-> Key players include Infineon Technologies, Mitsubishi Electric, STMicroelectronics, ON Semiconductor, Fuji Electric, and ROHM, collectively holding over 60% market share.

What are the key growth drivers?

-> Growth is driven by electrification of vehicles (xEVs achieving 35% CAGR), industrial automation (7.2% annual growth), and renewable energy adoption (wind power installations growing at 9.4% CAGR).

Which region dominates the market?

-> Asia-Pacific leads with 46.3% market share in 2024, followed by Europe (28.1%) and North America (18.7%), with China accounting for 62% of regional demand.

What are the emerging trends?

-> Emerging trends include SiC/GaN-based IPMs (growing at 32% CAGR), integrated sensor technologies, and miniaturization for space-constrained applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...