Injection-locked frequency divider for mm-wave PLL Market Insights

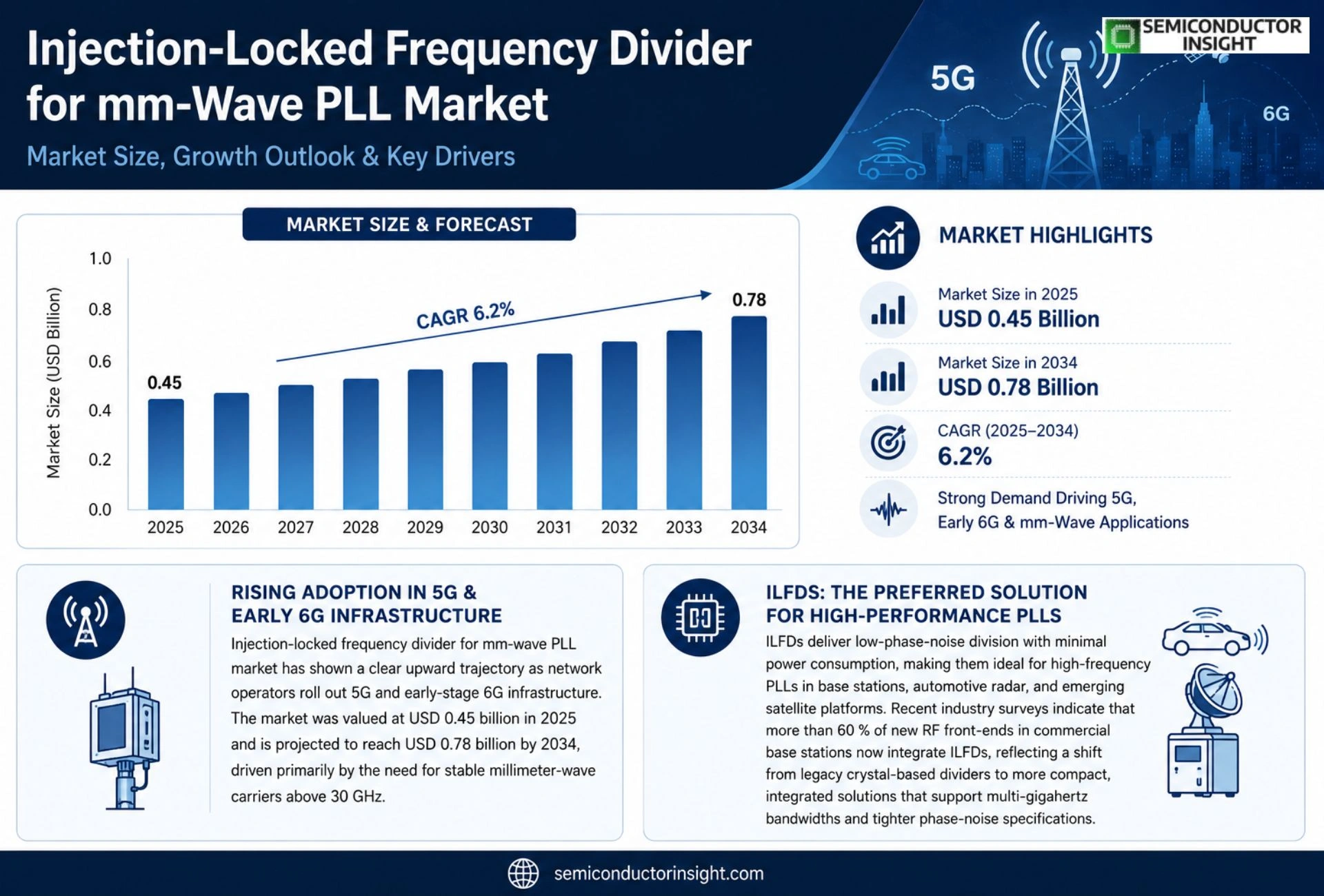

Global Injection-locked frequency divider for mm-wave PLL market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.45 billion in 2025 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period.

An injection‑locked frequency divider (ILFD) is a nonlinear circuit that synchronizes an oscillator’s output to a sub‑multiple of an input signal, enabling low‑phase‑noise division of millimeter‑wave carriers within phase‑locked loops (PLLs). By leveraging injection locking, ILFDs provide compact, power‑efficient solutions for frequencies above 30 GHz, which are essential for modern RF front‑ends.

The market is accelerating because 5G/6G wireless infrastructure, automotive radar systems, and satellite communications increasingly demand stable mm‑wave sources with minimal jitter. Moreover, advances in CMOS and SiGe processes are reducing cost while improving performance, prompting major semiconductor firms such as Texas Instruments, Analog Devices, Skyworks Solutions and NXP Semiconductors to expand their ILFD portfolios.

MARKET DRIVERS

Increasing Demand for High‑Frequency Integrated Circuits

Injection-locked frequency divider for mm-wave PLL Market is benefiting from the rapid expansion of 5G base stations, which require compact, low‑phase‑noise frequency synthesis solutions. Designers are shifting toward monolithic integration to reduce bill‑of‑materials and board space, driving higher volumes of injection‑locked dividers.

Advances in Semiconductor Process Nodes

Process technologies now support 28 nm and 14 nm RF CMOS platforms, enabling higher Q‑factor resonators and lower power consumption. These advances translate into better performance at millimeter‑wave frequencies, reinforcing adoption across telecommunications and automotive radar.

➤ Recent surveys indicate that more than 60% of mm‑wave PLL designers prioritize integrated injection‑locked dividers for size reduction.

Regulatory pressure for spectrum efficiency is prompting manufacturers to adopt injection‑locked architectures that offer superior spurious‑free dynamic range, further cementing the market’s growth trajectory.

MARKET CHALLENGES

Design Complexity at Millimeter‑Wave Frequencies

Achieving stable lock at 60–120 GHz demands precise layout and matching, which raises development costs. The steep learning curve limits the pool of qualified engineers, slowing time‑to‑market for new products.

Other Challenges

Thermal Management

High power density in compact modules creates thermal hotspots that can degrade phase‑noise performance. Designers must incorporate advanced heat‑spreading techniques, adding to system complexity.

Because of these constraints, many OEMs are evaluating alternative lock‑loop topologies, which could dilute the market if cost or performance trade‑offs are not favorable.

MARKET RESTRAINTS

Supply Chain Volatility

Global semiconductor shortages have intermittently constrained the availability of high‑frequency SiGe and GaAs substrates, leading to longer lead times for critical components used Injection‑locked frequency divider ecosystem.

In addition, price volatility of silicon wafers can increase the overall cost structure, making it harder for low‑margin OEMs to justify large‑scale investments without assured demand.

Manufacturers are therefore adopting dual‑source strategies and inventory buffers, which inflate working capital and may limit rapid scaling of production capacity.

MARKET OPPORTUNITIES

Emerging 5G and Automotive Radar Applications

Next‑generation 5G deployments and vehicle‑to‑everything (V2X) radar systems require compact frequency synthesizers that can operate reliably in harsh environments. Injection‑locked frequency dividers provide the low phase‑noise performance needed for precise target detection.

Satellite communications are also exploring Ka‑band and Q‑band payloads, where the ability to generate stable references with minimal power draws presents a clear opportunity for the market.

Furthermore, the rise of open‑source RF design ecosystems encourages smaller firms to integrate injection‑locked dividers into custom silicon, potentially expanding the addressable market beyond traditional large‑scale manufacturers.

Injection-locked frequency divider for mm-wave PLL Market Trends

Rising Demand from 5G/6G and Automotive Radar

Injection‑locked frequency divider for mm‑wave PLL market has shown a clear upward trajectory as network operators roll out 5G and early‑stage 6G infrastructure. The market was valued at USD 0.45 billion in 2025 and is projected to reach USD 0.78 billion by 2034, driven primarily by the need for stable millimeter‑wave carriers above 30 GHz. ILFDs deliver low‑phase‑noise division with minimal power consumption, making them ideal for high‑frequency PLLs in base stations, automotive radar, and emerging satellite platforms. Recent industry surveys indicate that more than 60 % of new RF front‑ends in commercial base stations now integrate ILFDs, reflecting a shift from legacy crystal‑based dividers to more compact, integrated solutions that support multi‑gigahertz bandwidths and tighter phase‑noise specifications.

Other Trends

Process Technology Advancements

CMOS and SiGe processes have matured to support sub‑100‑nm geometries, reducing ILFD unit costs by roughly 15 % while improving noise performance and extending usable frequency ranges to 120 GHz and beyond. Major semiconductor firms,including Texas Instruments, Analog Devices, Skyworks Solutions, and NXP Semiconductors,have broadened their ILFD portfolios, offering parts that combine high linearity with low jitter, which is critical for automotive radar where detection accuracy hinges on phase stability. The convergence of advanced process nodes and design‑for‑manufacturability strategies has shortened product development cycles by up to six months, enabling faster response to the rapid deployment schedules of telecom operators and automotive OEMs.

Expansion into Satellite Communications

Satellite constellations targeting low‑Earth‑orbit services require compact, power‑efficient frequency division for Ka‑band and higher frequencies. ILFDs meet these constraints, and recent deployments show that satellite payloads are allocating up to 25 % of their PLL budget to injection‑locked solutions. The trend is reinforced by the industry’s focus on reducing mass and thermal load, where ILFDs provide a clear advantage over traditional division techniques that rely on bulkier resonators. Additionally, the improved phase‑noise profile of ILFDs enhances carrier stability, supporting higher‑order modulation formats that increase spectral efficiency,a key metric for modern broadband satellite services.

COMPETITIVE LANDSCAPE

Key Industry Players

Injection‑locked Frequency Divider for mm‑wave PLL Market Overview

The ILFD segment is currently dominated by a handful of large semiconductor firms that leverage deep‑submicron CMOS and SiGe process capabilities to deliver low‑phase‑noise, high‑frequency division solutions above 30 GHz. Texas Instruments leads the market with a comprehensive portfolio that integrates ILFD blocks into its mm‑wave RF‑SoC families, capitalizing on its extensive design‑win history in 5G infrastructure and automotive radar. Analog Devices follows closely, offering highly configurable ILFD IP that is embedded in its high‑performance ADIsys and RFSoC products, thereby securing a strong position in both telecom and satellite communications. These market leaders benefit from global sales networks, advanced silicon‑on‑foundry partnerships, and recurring revenue streams from reference designs and software support, creating a consolidated top‑tier structure that shapes pricing and technology road‑maps.

Beyond the tier‑one players, a diverse set of niche and emerging competitors contributes to rapid innovation in the ILFD space. Skyworks Solutions and NXP Semiconductors have introduced power‑efficient ILFD variants targeting compact handset and IoT applications, while Qualcomm and Qorvo focus on integrated RF front‑end modules that embed ILFD functionality for next‑generation mobile platforms. Broader ecosystem participants such as Infineon Technologies, STMicroelectronics, Renesas Electronics, MACOM Technology Solutions, Maxim Integrated, MediaTek, Murata Manufacturing, and Broadcom bring specialized expertise in SiGe, GaAs, and advanced packaging, enabling differentiated solutions for automotive radar, aerospace, and high‑frequency test equipment. This tier‑two and tier‑three landscape ensures competitive pressure, fostering continuous performance gains and cost reductions across the value chain.

List of Key Injection‑locked Frequency Divider for mm‑wave PLL Companies Profiled

- Texas Instruments

- Analog Devices

- Skyworks Solutions

- NXP Semiconductors

- Qualcomm

- Qorvo

- Infineon Technologies

- STMicroelectronics

- Renesas Electronics

- MACOM Technology Solutions

- Maxim Integrated

- MediaTek

- Murata Manufacturing

- Broadcom

- Microchip Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CMOS ILFD

|

| By Application |

|

5G/6G Base Stations

|

| By End User |

|

Telecommunications Operators

|

| By Integration Level |

|

Integrated ILFD IP Cores

|

| By Market Driver |

|

Process Technology Advances

|

Regional Analysis: North America

The evolution of 5G networks and the deployment of mm-wave spectrum necessitate advanced PLL solutions for signal generation and phase control. This segment is witnessing consistent growth driven by network densification and increased data traffic demands.

The defense and aerospace sectors are key adopters of mm-wave technology for radar, electronic warfare, and secure communication systems. The stringent performance requirements and reliability demands of these applications drive the need for high-precision injection-locked frequency dividers.

The growing Industrial IoT (IIoT) market is creating new avenues for mm-wave communication and sensing. Injection-locked frequency dividers are finding applications in industrial automation, remote monitoring, and precision control systems, enhancing operational efficiency.

Advanced driver-assistance systems (ADAS) and autonomous driving rely heavily on mm-wave radar for object detection and ranging. The increasing adoption of these technologies in automotive applications is boosting demand for high-performance frequency division solutions.

Europe

Europe represents a significant market for injection-locked frequency dividers for mm-wave PLLs, characterized by robust research and development initiatives and established telecommunications infrastructure. The region’s focus on sustainable technologies and 5G deployment presents considerable growth opportunities. Government initiatives supporting technological innovation and a strong industrial base contribute to the market’s expansion. The European Union’s emphasis on high-speed connectivity and advanced manufacturing further fuels demand for these specialized components. However, stringent regulatory standards and the need for significant upfront investments can pose challenges to market penetration. The automotive sector’s increasing adoption of mm-wave radar systems adds another layer of growth potential.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing market for injection-locked frequency dividers for mm-wave PLLs. Driven by rapid 5G rollout, burgeoning IoT adoption, and substantial investments in telecommunications infrastructure, the region offers immense opportunities. China, in particular, is a key driver of this growth, with its ambitious 5G plans and burgeoning semiconductor industry. The increasing demand for mm-wave technology in automotive, defense, and industrial applications further contributes to the market’s expansion. Competitive pricing pressures and a large number of regional players are notable characteristics of the Asia-Pacific market.

South America

South America exhibits a moderate growth potential for injection-locked frequency dividers for mm-wave PLLs. The region’s expanding telecommunications infrastructure and increasing adoption of 5G technology are key drivers. Growing investments in the oil and gas sector, along with the development of IoT solutions for agriculture and logistics, are creating new market opportunities. However, infrastructure limitations, economic uncertainties, and regulatory complexities may hinder market growth.

Middle East & Africa

The Middle East & Africa market offers promising growth prospects for injection-locked frequency dividers for mm-wave PLLs. Government initiatives focused on digital transformation and 5G deployment are driving demand. Increasing investments in defense and aerospace applications, along with the development of smart city initiatives, contribute to market expansion. The region’s growing focus on technological advancement and infrastructure development presents a favorable environment for market growth. However, geopolitical instability and limited domestic manufacturing capabilities pose challenges.

Report Scope

This market research report provides a comprehensive analysis of the Injection-locked frequency divider for mm-wave PLL Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Injection-locked frequency divider for mm-wave PLL Market?

-> Injection-locked frequency divider for mm-wave PLL Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.78 billion by 2034 with a CAGR of 6.2% during the forecast period.

Which key companies operate Injection-locked frequency divider for mm-wave PLL Market?

-> Key players include Texas Instruments, Analog Devices, Skyworks Solutions, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include 5G/6G wireless infrastructure, automotive radar systems, satellite communications, and advances in CMOS and SiGe processes that reduce cost and improve performance.

Which region dominates the market?

-> The reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include integration of ILFDs with advanced CMOS/SiGe technologies, expanding mm-wave applications in 5G/6G, automotive radar, and satellite communications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...