MARKET INSIGHTS

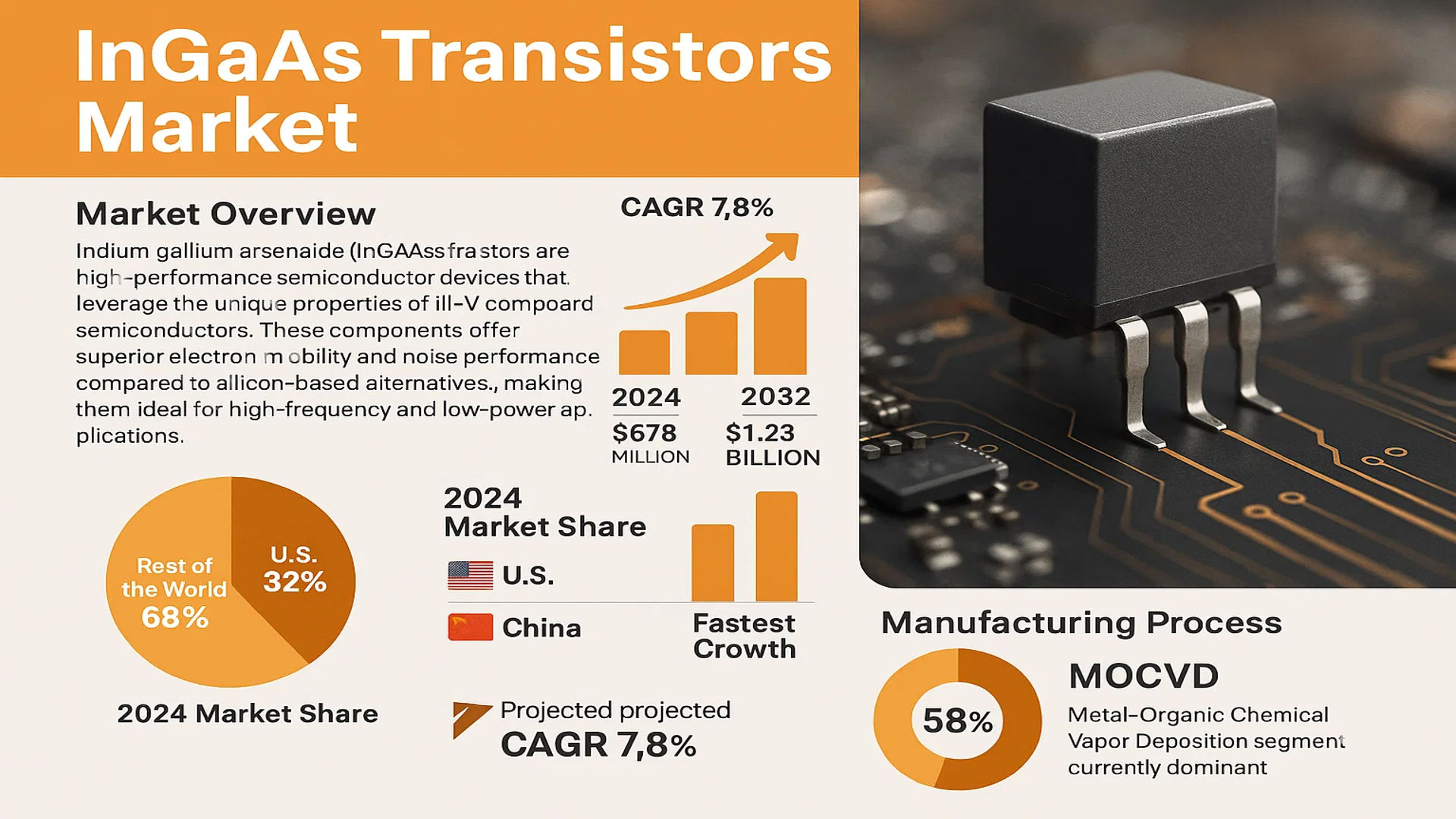

The global InGaAs Transistors Market size was valued at US$ 678 million in 2024 and is projected to reach US$ 1.23 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the fastest growth with a projected CAGR of 7.8% through 2032.

Indium gallium arsenide (InGaAs) transistors are high-performance semiconductor devices that leverage the unique properties of III-V compound semiconductors. These components offer superior electron mobility and noise performance compared to silicon-based alternatives, making them ideal for high-frequency and low-power applications. The technology finds extensive use in military communications, aerospace systems, and industrial automation where precision and reliability are critical.

Market growth is driven by increasing demand for high-speed communication networks and advancements in 5G infrastructure. The MOCVD (Metal-Organic Chemical Vapor Deposition) segment currently dominates manufacturing processes, accounting for 58% of production in 2024. However, emerging applications in quantum computing and autonomous vehicles are creating new growth opportunities. Key players including Qorvo and Nordamps are investing in R&D to develop next-generation transistors, with recent advancements focusing on improving power efficiency and thermal stability for harsh environment applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Speed and High-Frequency Applications to Propel Market Growth

The InGaAs transistor market is experiencing robust growth due to increasing demand in high-frequency and high-speed applications such as 5G networks, satellite communications, and radar systems. InGaAs transistors, known for their superior electron mobility and low noise characteristics, are becoming essential components in next-generation telecommunications infrastructure. The global rollout of 5G technology, which requires efficient power amplifiers and low-noise amplifiers (LNAs), has significantly boosted adoption. Industry trends indicate that the 5G infrastructure market is projected to grow at a compound annual growth rate (CAGR) of over 30% in the next five years, creating a parallel demand for InGaAs transistors.

Increasing Investment in Defense and Aerospace to Expand Market Potential

The defense and aerospace sectors are increasingly adopting InGaAs transistors for applications in surveillance, electronic warfare, and satellite communications. With governments worldwide increasing defense budgets—global military spending reached $2.1 trillion in recent years—there is heightened demand for advanced semiconductor technologies capable of operating in harsh environments. The superior performance of InGaAs transistors in infrared imaging and high-frequency signal processing makes them indispensable for modern defense systems. Leading manufacturers are collaborating with defense contractors to develop customized solutions, further driving market expansion.

Advancements in Metrology and Sensing Applications to Augment Market Prospects

InGaAs transistors are gaining traction in scientific and industrial metrology due to their ability to detect near-infrared (NIR) wavelengths with high precision. Applications range from spectroscopy in pharmaceuticals to quality control in semiconductor manufacturing. The increasing integration of automation and Industry 4.0 technologies has heightened the need for reliable sensing solutions, where InGaAs-based components offer superior performance. Emerging applications in autonomous vehicles and medical diagnostics are expected to provide additional growth avenues. For instance, the adoption of InGaAs sensors in medical imaging is projected to rise due to their efficiency in detecting tissue abnormalities.

MARKET RESTRAINTS

High Fabrication Costs and Technical Complexities to Impede Adoption

Despite their advantages, InGaAs transistors face challenges related to high production costs and complex manufacturing processes. The epitaxial growth of InGaAs layers requires sophisticated techniques like Metal-Organic Chemical Vapor Deposition (MOCVD) or Molecular Beam Epitaxy (MBE), which are significantly more expensive than conventional silicon-based fabrication. The cost-sensitive nature of consumer electronics makes widespread adoption difficult, as manufacturers often prioritize cost-efficiency over performance for mass-market devices.

Material Supply Chain Uncertainties

The availability of rare-earth materials such as indium and gallium, critical for InGaAs transistor fabrication, remains a concern. Geopolitical tensions and supply chain disruptions have led to price volatility, impacting production stability. Additionally, stringent environmental regulations governing mining activities for these materials could further strain supply, limiting scalability.

Competition from Alternative Semiconductor Technologies

Silicon-based transistors continue to dominate the semiconductor industry due to their established infrastructure and lower costs. Emerging technologies like gallium nitride (GaN) and silicon carbide (SiC) are also gaining momentum in high-frequency applications, intensifying competition for InGaAs transistors. While each technology has distinct advantages, the semiconductor industry’s reluctance to shift from legacy systems poses a significant restraint.

MARKET OPPORTUNITIES

Expansion in Quantum Computing to Unlock New Growth Avenues

The rapid development of quantum computing presents a transformative opportunity for the InGaAs transistor market. Quantum processors require ultra-sensitive readout electronics, where InGaAs-based low-noise amplifiers (LNAs) can play a crucial role. Governments and private enterprises are heavily investing in quantum technologies, with funding for quantum research surpassing $30 billion globally. As quantum computing transitions from research labs to commercial applications, the demand for specialized semiconductors like InGaAs transistors is expected to surge.

Emerging Markets in Asia-Pacific to Drive Future Demand

The Asia-Pacific region, particularly China, Japan, and South Korea, is witnessing exponential growth in telecommunications, consumer electronics, and industrial automation. Government initiatives such as China’s “Made in China 2025” are accelerating semiconductor innovation, creating fertile ground for InGaAs transistor adoption. With over 60% of global semiconductor manufacturing concentrated in this region, proximity to supply chains and a skilled workforce position Asia-Pacific as a high-growth market.

Integration with Photonics for Next-Generation Optical Communication

The convergence of InGaAs transistors with silicon photonics is opening new possibilities in optical communication networks. High-speed data centers and fiber-optic networks require efficient optoelectronic components, where InGaAs transistors excel in converting electrical signals to optical signals with minimal loss. The increasing demand for hyperscale data centers—expected to grow at a CAGR of 20%—will further amplify opportunities for InGaAs-based integrated circuits.

MARKET CHALLENGES

Scalability and Yield Issues in Mass Production to Restrict Growth

While InGaAs transistors offer superior performance, their mass production faces significant challenges related to yield rates and scalability. The defect density in InGaAs epitaxial layers is higher compared to silicon, leading to lower yields in wafer production. Achieving uniformity across large-scale production runs remains a technical hurdle, with industry estimates suggesting yield rates below 70% for high-performance InGaAs devices. This limitation increases per-unit costs and discourages adoption in price-sensitive applications.

Thermal Management and Power Handling Constraints

InGaAs transistors exhibit higher thermal resistance compared to silicon or GaN alternatives, making heat dissipation a critical challenge in high-power applications. Without efficient thermal management solutions, device reliability can be compromised, limiting their use in mission-critical systems such as aerospace or defense electronics. Research into advanced packaging techniques is ongoing, but commercial solutions are yet to achieve widespread adoption.

Regulatory and Standardization Gaps

The lack of standardized testing protocols for InGaAs transistors creates uncertainty for manufacturers and end-users alike. Regulatory bodies have yet to establish uniform performance benchmarks, leading to discrepancies in quality and reliability assessments. This ambiguity complicates procurement decisions for industries requiring certified components, such as medical devices and automotive electronics.

Increased Adoption in High-Frequency Applications Drives InGaAs Transistors Market Growth

The global InGaAs transistors market is witnessing significant growth due to rising demand for high-speed and high-frequency applications in telecommunications and defense sectors. With a projected CAGR of nearly 7% from 2024 to 2032, these transistors are becoming increasingly essential in 5G networks, satellite communications, and radar systems due to their superior electron mobility and low noise characteristics. The market valuation is expected to surpass $450 million by 2032, driven by technological advancements in compound semiconductor materials.

Other Trends

Emerging Photonics and Sensing Applications

InGaAs transistors are gaining traction in optoelectronics and sensing technologies due to their ability to operate efficiently in near-infrared wavelengths. This is particularly valuable for applications like LIDAR systems in autonomous vehicles and medical imaging devices. The development of highly sensitive InGaAs-based sensors has opened new opportunities in environmental monitoring and industrial quality control systems, contributing to market expansion across multiple verticals.

Advancements in Manufacturing Processes

Manufacturers are increasingly adopting Metal-Organic Chemical Vapor Deposition (MOCVD) techniques to produce high-performance InGaAs transistors, accounting for over 45% of production methods. This shift is driven by the technology’s capability to achieve precise layer thickness and superior material quality at commercial scales. While Molecular Beam Epitaxy (MBE) remains crucial for research-grade components, MOCVD dominates commercial production due to its cost-effectiveness and scalability advantages in volume manufacturing scenarios.

Military and Aerospace Applications Fueling Demand

The military sector represents one of the fastest-growing segments for InGaAs transistors, with defense applications accounting for nearly 30% of total market share. These components are critical in electronic warfare systems, missile guidance technologies, and secure communications equipment where reliability under extreme conditions is paramount. Furthermore, the aerospace industry’s transition to more compact and energy-efficient avionics systems has led to increased adoption of InGaAs-based solutions in next-generation aircraft designs.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Collaborations Drive Market Leadership in InGaAs Transistors

The global InGaAs transistors market features a mix of established semiconductor manufacturers and specialized players competing through technological differentiation. As of 2024, the market remains moderately concentrated, with the top five companies collectively holding significant revenue share. Qorvo emerges as a dominant force, leveraging its expertise in RF semiconductor solutions for aerospace and defense applications where InGaAs transistors are critical for high-frequency performance.

Meanwhile, Nordamps has carved a niche in industrial applications through its vertically integrated manufacturing process, which enables cost-efficient production of medium-power InGaAs components. Their 2023 acquisition of a German epitaxial wafer supplier strengthened their supply chain resilience against geopolitical disruptions.

The competitive intensity is escalating as companies address the growing demand from 5G infrastructure deployments. Analog Devices Inc., though not traditionally focused on III-V semiconductors, entered the space through strategic partnerships with foundries, signaling the market’s expanding attractiveness. Smaller players like Comptek Solutions compete through application-specific designs, particularly in quantum sensing and photonics where customized InGaAs solutions command premium pricing.

Recent developments highlight two strategic directions: established silicon players are expanding into compound semiconductors through M&A, while pure-play III-V companies are focusing on yield improvement and fab automation to reduce costs. This dual trajectory suggests the market will see both consolidation among smaller players and increased competition from large semiconductor conglomerates.

List of Key InGaAs Transistor Manufacturers

- Qorvo, Inc. (U.S.) – RF solutions leader

- Nordamps Semiconductors (Netherlands) – Industrial applications specialist

- Comptek Solutions (Finland) – Custom design provider

- Win Semiconductors Corp. (Taiwan) – Foundry services

- II-VI Incorporated (U.S.) – Photonics integration

- MACOM Technology Solutions (U.S.) – Defense/aerospace focus

- Sumitomo Electric Industries (Japan) – Substrate supplier

- Ommic SAS (France) – Millimeter wave applications

- Microchip Technology (U.S.) – Through acquisition of [Company]

Segment Analysis:

By Type

MOCVD Segment Dominates Due to High Demand in Optoelectronic Applications

The market is segmented based on type into:

- MOCVD (Metal-Organic Chemical Vapor Deposition)

- MBE (Molecular Beam Epitaxy)

- Others

By Application

Military Segment Leads Due to Critical Use in Defense Technologies

The market is segmented based on application into:

- Military

- Industry

- Manufacturing

- Aerospace

- Others

By End User

Telecommunication Sector Drives Adoption for High-Frequency Applications

The market is segmented based on end user into:

- Telecommunication

- Defense and Aerospace

- Industrial Automation

- Research and Development

Regional Analysis: InGaAs Transistors Market

Asia-Pacific

The Asia-Pacific region dominates the InGaAs Transistors market, driven by semiconductor manufacturing expansion in countries like China, Japan, and South Korea. China’s semiconductor self-sufficiency initiatives, including the $150 billion Made in China 2025 program, are accelerating domestic production of advanced components like InGaAs transistors. Japan retains competitive advantages in material science and precision manufacturing, while South Korea’s robust electronics ecosystem creates steady demand. India is emerging as a growth hotspot, with government incentives for electronics manufacturing attracting foreign investment. The region benefits from strong supply chain integration, though geopolitical tensions and export controls present risks for technology transfer.

North America

North America maintains technological leadership in InGaAs transistor development, particularly for defense and telecommunications applications. The U.S. accounts for over 60% of regional demand, with significant R&D investments from both private sector players like Qorvo and government agencies including DARPA. Canada is growing its photonics industry, creating niche opportunities. While the market faces cost pressures from Asian competitors, North American manufacturers differentiate through high-reliability products for aerospace and military systems. Recent CHIPS Act funding allocations are strengthening domestic semiconductor infrastructure, which may bolster future InGaAs production capacity.

Europe

Europe’s InGaAs transistor market is characterized by specialized applications in industrial sensing and scientific instrumentation. Germany and the UK lead in photonic integration technologies, while France has notable capabilities in aerospace-grade components. The EU’s Horizon Europe program supports research into next-generation semiconductor materials, though commercialization lags behind Asia and North America. Strict environmental regulations influence material sourcing and manufacturing processes across the region. Collaborative R&D initiatives between academia and industry are helping maintain Europe’s position in high-value, low-volume InGaAs applications.

Middle East & Africa

This region represents an emerging market with growing investments in telecommunications infrastructure driving demand for optoelectronic components. Israel has developed specialized capabilities in defense-related semiconductor applications, while UAE and Saudi Arabia are investing in smart city technologies that may utilize InGaAs sensors. The lack of local manufacturing means most supply is imported, creating opportunities for distributors and system integrators. While current market size remains small relative to other regions, long-term growth potential exists as digital transformation initiatives accelerate across key economies.

South America

South America’s InGaAs transistor market is in early development stages, with Brazil accounting for the majority of regional demand through its aerospace and industrial sectors. Limited local expertise and infrastructure constrain market growth, though increasing foreign direct investment in electronics manufacturing may gradually improve access to advanced components. Argentina shows potential in scientific research applications but faces economic challenges that limit commercial scalability. The region currently relies heavily on imports, creating price sensitivity that favors more mature semiconductor technologies over cutting-edge InGaAs solutions except for specialized applications.

Report Scope

This market research report provides a comprehensive analysis of the Global InGaAs Transistors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (MOCVD, MBE, Others), application (Military, Industry, Manufacturing, Aerospace, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Nordamps, Comptek Solutions, and Qorvo, covering product portfolios, R&D investments, and strategic initiatives.

- Technology Trends: Assessment of emerging semiconductor fabrication techniques, integration with advanced electronics, and material innovations.

- Market Dynamics: Evaluation of growth drivers such as demand for high-frequency applications, alongside challenges like material sourcing constraints.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, component suppliers, and technology integrators.

The analysis combines primary research with industry data from verified sources to deliver accurate market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global InGaAs Transistors Market?

-> InGaAs Transistors market size was valued at US$ 678 million in 2024 and is projected to reach US$ 1.23 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032.

Which key companies operate in Global InGaAs Transistors Market?

-> Key players include Nordamps, Comptek Solutions, and Qorvo, with the top five companies holding approximately XX% market share in 2024.

What are the key growth drivers?

-> Market growth is driven by increasing demand for high-speed electronics, military applications, and aerospace technologies requiring advanced semiconductor solutions.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the highest CAGR during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of components, integration with IoT devices, and development of next-generation fabrication techniques.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...