MARKET INSIGHTS

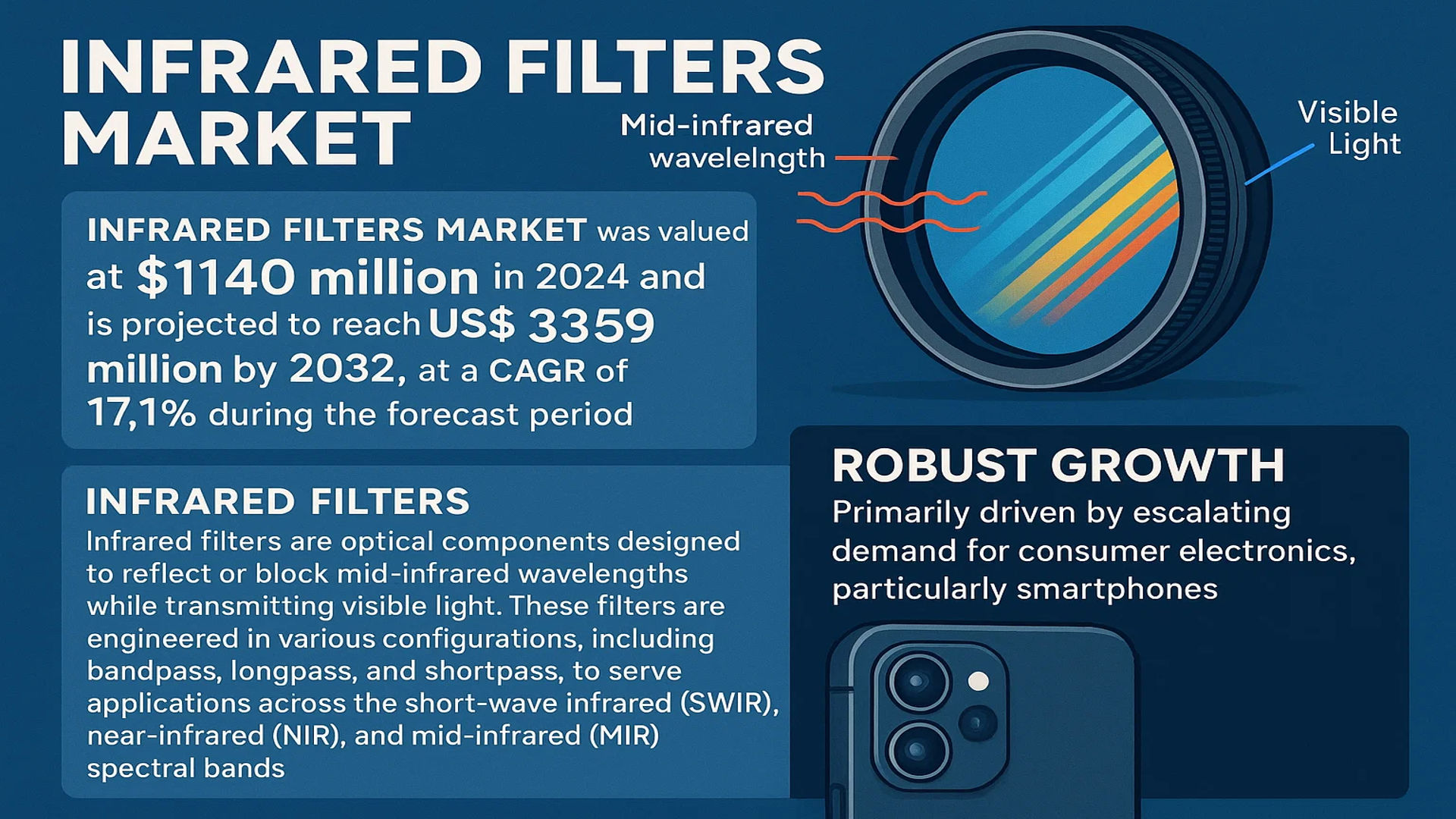

The global Infrared Filters Market was valued at 1140 million in 2024 and is projected to reach US$ 3359 million by 2032, at a CAGR of 17.1% during the forecast period.

Infrared filters are optical components designed to reflect or block mid-infrared wavelengths while transmitting visible light. These filters are engineered in various configurations, including bandpass, longpass, and shortpass, to serve applications across the short-wave infrared (SWIR), near-infrared (NIR), and mid-infrared (MIR) spectral bands. They are critical for enhancing image quality and enabling specific spectral functions in a wide range of electronic devices.

The market’s robust growth is primarily driven by the escalating demand for consumer electronics, particularly smartphones, where these filters are integral to camera systems. China dominates the global landscape, holding over 40% of the market share, followed by the USA and South Asia. The blue glass infrared filter segment is the largest product category, accounting for over 40% of the market. Furthermore, the mobile phone application is the leading end-use segment, propelled by the continuous innovation and high-volume production of smartphones globally.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Smartphones and Consumer Electronics to Accelerate Market Expansion

The global infrared filters market is experiencing robust growth driven by the widespread adoption of smartphones and consumer electronics. Infrared filters are critical components in mobile device cameras, enabling enhanced image quality by blocking unwanted infrared light while allowing visible light transmission. With over 1.4 billion smartphones shipped annually worldwide, the demand for high-quality imaging components continues to surge. The integration of multiple camera systems in modern smartphones, often featuring three or more lenses per device, further amplifies the need for infrared filters. This trend is particularly pronounced in emerging markets where smartphone penetration rates are growing rapidly, creating sustained demand for infrared filter components across both premium and mid-range device segments.

Advancements in Automotive Safety Systems to Fuel Market Growth

Infrared filter adoption is accelerating within the automotive sector, particularly through the integration of advanced driver-assistance systems (ADAS) and night vision technologies. Automotive manufacturers are increasingly incorporating infrared cameras and sensors that require specialized filters to function effectively in various lighting conditions. The global ADAS market is projected to grow significantly, with infrared-based systems playing a crucial role in pedestrian detection, lane departure warnings, and collision avoidance. These systems rely on precise infrared filtration to distinguish between thermal signatures and visible light patterns, enabling vehicles to make real-time safety decisions. The transition toward autonomous vehicles further amplifies this demand, as self-driving cars require sophisticated sensory systems that can operate reliably in all environmental conditions.

Expansion of Security and Surveillance Infrastructure to Drive Demand

The global security and surveillance market represents a substantial growth opportunity for infrared filters, particularly in both commercial and governmental applications. Infrared-enabled surveillance cameras provide critical capabilities for 24/7 monitoring, facial recognition, and perimeter security across various environments. The market has witnessed increased investment in smart city projects worldwide, with many governments implementing large-scale surveillance networks that incorporate infrared imaging technology. These systems require high-performance infrared filters to ensure clear imaging during nighttime operations and low-light conditions. The ongoing modernization of security infrastructure across airports, public spaces, and critical facilities continues to drive demand for advanced optical components, including specialized infrared filters designed for specific wavelength requirements.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes to Limit Market Penetration

The infrared filters market faces significant constraints due to the sophisticated manufacturing processes and substantial capital investment required for production. Creating high-quality infrared filters involves precise deposition techniques, specialized coating materials, and stringent quality control measures that contribute to elevated production costs. The manufacturing process often requires cleanroom environments, advanced vacuum deposition systems, and highly trained technical personnel, all of which add to the overall expense. These cost factors become particularly challenging when serving price-sensitive market segments, such as consumer electronics, where component pricing pressures are intense. Manufacturers must balance performance requirements with cost considerations, often limiting the adoption of premium infrared filter solutions in mass-market applications.

Technical Limitations in Filter Performance to Hinder Market Development

Infrared filter technology faces inherent technical challenges related to performance characteristics that can restrict application suitability. One significant limitation involves the trade-off between transmission efficiency and blocking capability—achieving high visible light transmission while effectively blocking infrared wavelengths remains technically demanding. Filters must maintain consistent performance across varying environmental conditions, including temperature fluctuations and humidity changes, which can affect optical properties. Additionally, different applications require specific wavelength cutoffs and transition slopes, creating engineering challenges in developing filters that meet diverse industry requirements. These technical constraints often necessitate custom solutions that increase development time and cost, potentially slowing adoption rates in applications requiring standardized, cost-effective components.

Supply Chain Vulnerabilities and Raw Material Dependencies to Constrain Market Stability

The infrared filters market is susceptible to supply chain disruptions and raw material availability issues that can impact production consistency and pricing stability. Specialized coating materials, particularly those containing rare earth elements and specific semiconductor compounds, face supply constraints and price volatility. Many infrared filter designs incorporate materials with limited global production capacity, creating dependency on specific suppliers and geographic regions. Recent global events have highlighted the vulnerability of optical component supply chains, with logistics challenges and material shortages affecting manufacturing output. These factors can lead to extended lead times, price fluctuations, and production delays, ultimately affecting the ability of infrared filter manufacturers to meet growing market demand consistently.

MARKET OPPORTUNITIES

Emergence of Medical Imaging and Diagnostic Applications to Create New Growth Avenues

The healthcare sector presents significant growth opportunities for infrared filters through expanding applications in medical imaging and diagnostic equipment. Infrared technology is increasingly employed in various medical devices, including endoscopes, dermatology instruments, and diagnostic imaging systems that utilize specific wavelength ranges for enhanced visualization. The global medical imaging market continues to grow, driven by technological advancements and increasing healthcare expenditure worldwide. Infrared filters enable improved contrast in medical imaging by isolating particular wavelength bands that enhance tissue differentiation and pathological identification. The development of minimally invasive surgical techniques and diagnostic procedures further amplifies the demand for precision optical components, creating substantial opportunities for infrared filter manufacturers to develop specialized products for medical applications.

Growth in Industrial Automation and Machine Vision Systems to Expand Market Potential

Industrial automation represents a promising growth area for infrared filters, particularly within machine vision systems and quality control applications. Manufacturing facilities increasingly employ automated inspection systems that utilize infrared imaging for defect detection, material classification, and process monitoring. These systems require specialized filters to enhance image contrast and isolate specific spectral features relevant to industrial processes. The transition toward Industry 4.0 and smart manufacturing initiatives drives adoption of advanced optical inspection technologies across various sectors, including electronics manufacturing, automotive production, and food processing. Infrared filters enable machines to “see” beyond human visual capabilities, detecting temperature variations, material composition differences, and structural anomalies that are invisible under normal lighting conditions.

Development of Augmented Reality and Virtual Reality Technologies to Open New Applications

The rapidly evolving augmented reality (AR) and virtual reality (VR) markets present innovative opportunities for infrared filter integration. AR/VR systems increasingly incorporate infrared sensors for motion tracking, gesture recognition, and environmental mapping, requiring precise optical filtration to function accurately. These applications demand filters that can separate visible light from infrared signals, enabling simultaneous display projection and environmental sensing. The growing adoption of AR/VR technologies across gaming, industrial training, educational, and healthcare applications creates substantial potential for specialized infrared filter solutions. As these technologies mature and find broader commercial application, the requirement for high-performance optical components will continue to expand, driving innovation in infrared filter design and manufacturing techniques.

MARKET CHALLENGES

Intense Price Competition and Margin Pressures to Challenge Market Sustainability

The infrared filters market faces significant challenges from intense price competition, particularly within the consumer electronics segment where cost sensitivity is extreme. Manufacturers encounter continuous pressure to reduce prices while maintaining or improving product performance, creating sustainability challenges for market participants. The industry has witnessed consolidation as smaller players struggle to compete with larger manufacturers that benefit from economies of scale and vertical integration. Price erosion affects profitability across the value chain, from raw material suppliers to filter manufacturers and integrators. This competitive environment necessitates continuous operational efficiency improvements and cost reduction initiatives, while simultaneously investing in research and development to maintain technological leadership.

Rapid Technological Obsolescence and Short Product Life Cycles to Complicate Planning

Infrared filter manufacturers operate in an environment characterized by rapid technological evolution and shortening product life cycles, particularly in consumer electronics applications. The pace of innovation in end-use products requires continuous adaptation of filter specifications and performance characteristics. This dynamic environment creates challenges in inventory management, production planning, and research investment decisions. Manufacturers must anticipate future requirements while managing current product portfolios, often facing the risk of technological obsolescence as new applications emerge and existing ones evolve. The need to continuously develop new products and improve existing ones requires substantial investment in research and development, creating financial challenges particularly for smaller market participants with limited resources.

Quality Consistency and Performance Standardization Issues to Affect Market Confidence

Maintaining consistent quality and performance standards represents an ongoing challenge for infrared filter manufacturers, particularly as applications become more demanding and specifications more stringent. Variations in filter performance can significantly impact the functionality of end products, leading to quality issues and customer dissatisfaction. The industry faces challenges in establishing universal performance standards across different applications and regions, creating confusion and compatibility issues. Manufacturing defects, including coating inconsistencies, surface imperfections, and spectral performance variations, can result in product failures and reliability concerns. These quality challenges become particularly critical in applications where infrared filters serve essential functions in safety systems, medical devices, and critical infrastructure, requiring exceptionally high reliability standards and rigorous quality assurance processes.

INFRARED FILTERS MARKET TRENDS

Proliferation of Consumer Electronics to Drive Market Expansion

The relentless growth of the consumer electronics sector, particularly smartphones and tablets, remains the primary catalyst for the infrared filters market. These devices increasingly incorporate multiple cameras for advanced photography features like night mode, portrait effects, and augmented reality, all of which rely heavily on high-performance infrared filters to ensure accurate color reproduction and block unwanted IR radiation. With global smartphone shipments consistently exceeding 1.4 billion units annually, the demand for these critical optical components is substantial and growing. Furthermore, the integration of 3D sensing and facial recognition technology in flagship devices has created a new, high-value application segment for specialized IR filters, particularly those operating in the near-infrared (NIR) spectrum. This trend is expected to intensify as these features trickle down to mid-range devices, significantly expanding the total addressable market.

Other Trends

Advancements in Automotive Safety and Autonomous Driving Systems

The automotive industry is emerging as a significant growth vector for infrared filters, driven by the rapid adoption of advanced driver-assistance systems (ADAS) and the development of autonomous vehicles. LiDAR (Light Detection and Ranging) systems, a cornerstone of autonomous navigation, operate primarily in the infrared spectrum and require highly precise filters to function accurately in various environmental conditions. The market for automotive LiDAR is projected to experience a compound annual growth rate of over 30% in the coming years, directly fueling demand for specialized infrared filters. Night vision systems, which use thermal imaging cameras to detect pedestrians and animals beyond the reach of headlights, also depend on advanced IR filtering technology. This expansion is not just quantitative but also qualitative, pushing manufacturers to develop filters with higher durability, broader temperature stability, and superior optical performance to meet stringent automotive industry standards.

Technological Innovation in Filter Design and Manufacturing

Continuous innovation in thin-film deposition techniques and material science is fundamentally enhancing the performance and application range of infrared filters. The development of ultra-steep edge bandpass filters and filters with extremely high out-of-band rejection ratios is enabling more precise spectral control, which is critical for applications in scientific instrumentation, medical diagnostics, and military sensing. There is a pronounced shift towards the use of hard-coated, durable filters that can withstand harsh environments, replacing older, more delicate soft-coated alternatives. Manufacturers are also investing heavily in scaling production to meet high-volume demands from consumer electronics while maintaining micron-level precision, a challenge that has led to increased automation and process control in fabrication facilities. This focus on R&D is crucial for maintaining technological leadership and catering to the increasingly sophisticated requirements of end-users across diverse industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global infrared filters market exhibits a semi-consolidated competitive structure, characterized by a mix of large multinational corporations and specialized regional manufacturers. The market’s top five players collectively command a significant share, estimated at over 40% of the global market value in 2024. This dominance is primarily driven by their extensive R&D capabilities, established supply chains, and strong relationships with key end-users in the consumer electronics and industrial sectors.

Zhejiang Quartz Crystal Optoelectronic and Shenzhen O-film Tech Co. are recognized as leading players, largely due to their strategic positioning within China, which itself accounts for over 40% of the global market. Their growth is heavily attributed to the massive domestic demand for infrared filters from mobile phone manufacturers, the largest application segment. These companies benefit from economies of scale and cost-effective production, allowing them to serve both local and international markets competitively.

Meanwhile, companies like Viavi Solutions and Tanaka Engineering Inc. have carved out significant niches through technological innovation and high-precision product offerings. Viavi Solutions, for instance, leverages its expertise in optical coatings to produce advanced filters for demanding applications beyond consumer electronics, including aerospace and defense. Their strategy focuses on high-value segments where performance outweighs cost considerations.

Additionally, these key players are actively engaged in growth initiatives such as geographical expansion and new product launches to capture a larger market share. For example, investments in expanding production capacity across Southeast Asia are a common tactic to reduce costs and be closer to emerging consumer electronics manufacturing hubs. The pursuit of partnerships with device OEMs is also a critical strategy to secure long-term supply contracts and ensure stable revenue streams in this rapidly growing market.

List of Key Infrared Filters Companies Profiled

- Zhejiang Quartz Crystal Optoelectronic (China)

- Optrontec (South Korea)

- W-olf Photoelectric (China)

- Shenzhen O-film Tech Co. (China)

- Tanaka Engineering Inc. (Japan)

- Unionlight (China)

- Viavi Solutions Inc. (U.S.)

- Jingbang Optoelectronics Technology (China)

Segment Analysis:

By Type

Glass Type Segment Dominates the Market Due to Superior Durability and Optical Clarity

The market is segmented based on type into:

- Glass Type

- Subtypes: Blue Glass Infrared Filter, Clear Glass Infrared Filter, and others

- Film Type

By Application

Mobile Phone Segment Leads Due to Pervasive Integration in Smartphone Cameras for Enhanced Imaging

The market is segmented based on application into:

- Mobile Phone

- Tablet

- Notebook

- PC

- Game Console

- Others

By Configuration

Bandpass Filters Hold Significant Market Share Owing to Precise Wavelength Selection Capabilities

The market is segmented based on configuration into:

- Bandpass Filters

- Longpass Filters

- Shortpass Filters

By Wavelength Band

SWIR Band Gains Traction for its Applications in Industrial Inspection and Defense

The market is segmented based on wavelength band into:

- Short-Wave Infrared (SWIR)

- Near-Infrared (NIR)

- Mid-Infrared (MIR)

Regional Analysis: Infrared Filters Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the Infrared Filters market, accounting for over 60% of worldwide consumption by volume. This dominance is overwhelmingly driven by China, which alone holds a market share exceeding 40%. The region’s supremacy is built on its colossal consumer electronics manufacturing ecosystem, producing the majority of the world’s mobile phones, tablets, and notebooks—the primary applications for IR filters. While cost-competitive manufacturing remains a core strength, there is a significant and accelerating shift towards producing higher-performance filters for advanced smartphone camera systems and emerging applications in automotive sensing and machine vision. Government initiatives, such as China’s “Made in China 2025” policy, further bolster local technological advancement and supply chain dominance, making APAC both the largest consumer and producer of these critical optical components.

North America

North America represents a highly advanced and technologically sophisticated market for Infrared Filters, characterized by strong demand for high-performance, precision components. The region, particularly the United States, is a hub for innovation in defense, aerospace, medical imaging, and autonomous vehicle technologies, all of which utilize specialized IR filters in SWIR and MIR wavelength bands. While the volume consumption is lower than in Asia-Pacific, the value per unit is significantly higher due to the complex specifications required. The market is driven by stringent quality standards, substantial R&D investments from tech giants and defense contractors, and a robust ecosystem of specialized manufacturers like Viavi Solutions. Demand is further fueled by the integration of advanced sensing systems in next-generation consumer electronics and the rapid development of the region’s autonomous vehicle industry.

Europe

The European market for Infrared Filters is defined by its strong emphasis on research, high-quality manufacturing, and compliance with rigorous technical standards. The region is a key center for the automotive industry, where IR filters are increasingly used in driver-assistance systems (ADAS) and interior monitoring sensors. Furthermore, Europe has a well-established industrial and scientific sector that demands precision optical filters for spectroscopy, environmental monitoring, and machine vision applications. Innovation is a primary driver, with companies and research institutions focusing on developing filters with enhanced durability, precise cut-on/cut-off wavelengths, and compatibility with new sensor technologies. While the market faces cost pressures from Asian manufacturers, it maintains a competitive edge through specialization in high-value, custom-designed solutions for niche applications.

South America

The South American market for Infrared Filters is nascent but shows potential for gradual growth. Current demand is primarily linked to the consumer electronics aftermarket and the slow adoption of newer smartphone models equipped with better camera systems. The region’s industrial base for manufacturing these components is limited, leading to a heavy reliance on imports, chiefly from Asia. Economic volatility and currency fluctuations often hinder large-scale investments in local production or the widespread adoption of the latest technologies that incorporate advanced IR filters. However, as urbanization continues and disposable incomes rise, the replacement market for mobile devices presents a steady, though modest, opportunity for filter suppliers targeting this region.

Middle East & Africa

The Middle East and Africa region represents an emerging market with growth potential tied to economic diversification and technological adoption. In the Middle East, particularly in Gulf Cooperation Council (GCC) nations like the UAE and Saudi Arabia, investments in smart city infrastructure, security, and surveillance systems are creating new demand for IR filters used in thermal imaging and night vision equipment. Africa’s market is more fragmented, with growth primarily driven by the expanding penetration of mid-range smartphones. The lack of local manufacturing means the entire region is import-dependent. While the current market size is small relative to other regions, long-term prospects are tied to broader economic development and the increasing integration of optical sensors into various aspects of infrastructure and consumer goods.

Report Scope

This market research report provides a comprehensive analysis of the global Infrared Filters market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Infrared Filters Market?

-> Infrared Filters Market was valued at 1140 million in 2024 and is projected to reach US$ 3359 million by 2032, at a CAGR of 17.1% during the forecast period.

Which key companies operate in Global Infrared Filters Market?

-> Key players include Zhejiang Quartz Crystal Optoelectronic, Optrontec, W-olf Photoelectric, Shenzhen O-film Tech Co, Tanaka Engineering Inc, Unionlight, Viavi Solutions, and Jingbang Optoelectronics Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, advancements in smartphone camera technology, increased adoption of infrared filters in security & surveillance systems, and growing automotive applications.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China holding over 40% market share, followed by North America and Europe.

What are the emerging trends?

-> Emerging trends include development of multi-spectral filters, integration of AI for enhanced imaging, miniaturization of filter components, and increasing use in autonomous vehicles and medical imaging devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...