MARKET INSIGHTS

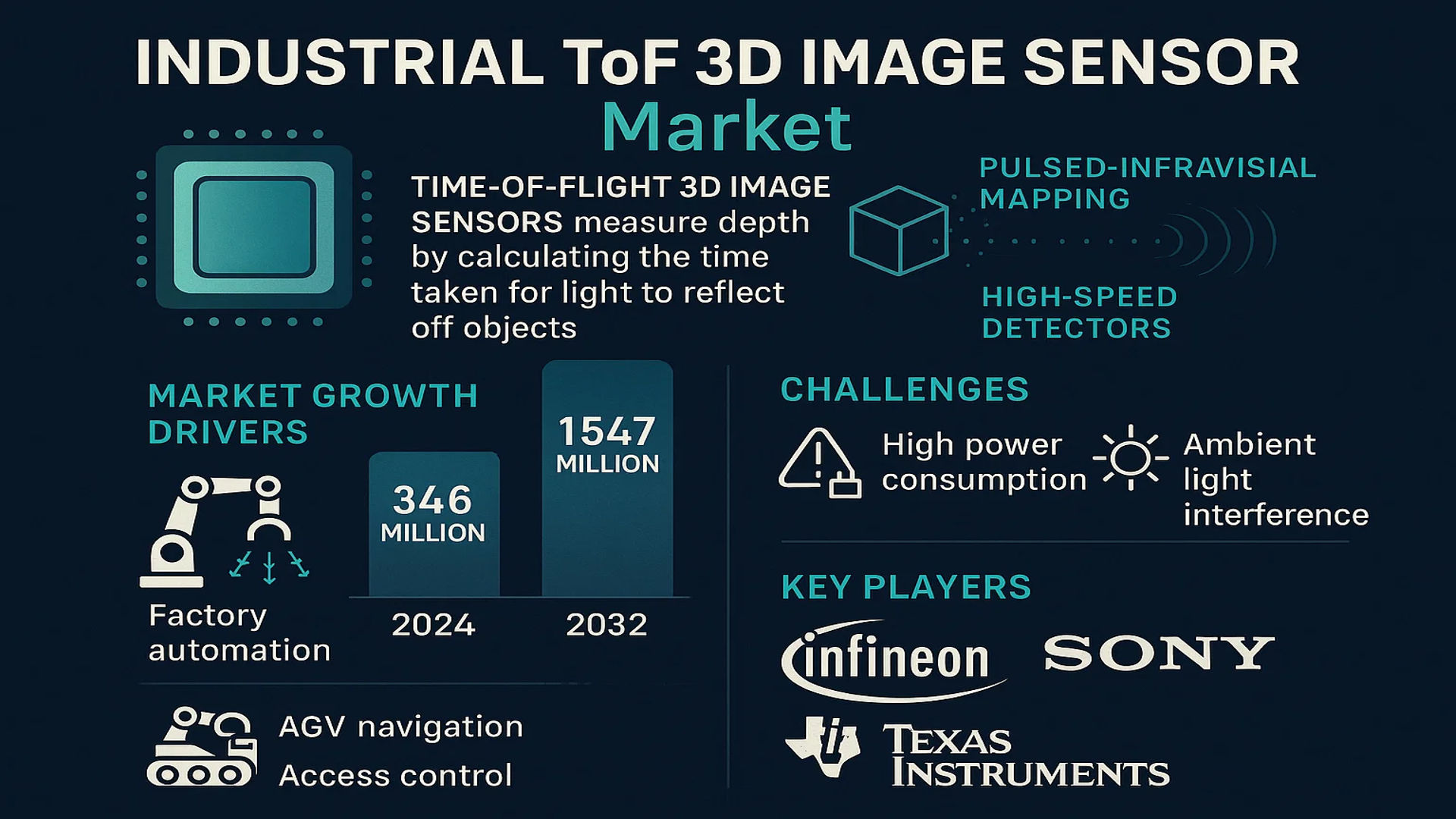

The global Industrial ToF 3D Image Sensor market was valued at 346 million in 2024 and is projected to reach US$ 1547 million by 2032, at a CAGR of 24.5% during the forecast period.

Time-of-Flight (ToF) 3D image sensors are advanced optoelectronic devices that measure depth by calculating the time taken for light to reflect off objects. These sensors enable precise three-dimensional mapping through pulsed infrared light and high-speed detectors, making them indispensable for industrial automation, robotics, and machine vision applications.

The market growth is primarily driven by increasing adoption in factory automation for quality inspection, AGV navigation, and access control systems. While the technology offers superior performance in harsh industrial environments, challenges such as high power consumption and interference from ambient light persist. Key players like Infineon Technologies, Sony, and Texas Instruments are investing in R&D to enhance resolution and robustness, further accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Industrial Automation to Accelerate ToF 3D Sensor Adoption

The global push toward industrial automation continues to fuel demand for Time-of-Flight (ToF) 3D image sensors across multiple sectors. These sensors enable machines to perceive environments accurately, supporting critical applications such as robotic guidance, quality inspection, and precise material handling. Recent advancements in direct and indirect ToF technologies have significantly improved depth resolution, with some sensors achieving sub-millimeter precision at ranges up to 10 meters. Manufacturing facilities adopting Industry 4.0 principles increasingly rely on these sensors – a key factor contributing to the projected 24.5% CAGR growth from 2024 to 2032. Notably, automotive assembly lines using ToF sensors have demonstrated up to 30% improvement in defect detection rates compared to traditional 2D vision systems.

Expansion of AGV Applications Creates New Growth Vectors

Automated Guided Vehicles (AGVs) represent one of the fastest-growing application segments for industrial ToF sensors, driven by e-commerce logistics expansion and warehouse modernization. Modern ToF sensors allow AGVs to navigate complex environments with dynamic obstacles while maintaining positional accuracy within ±5cm – a critical requirement for high-density storage facilities. The global AGV market’s expansion correlates directly with ToF sensor adoption, particularly in Asia-Pacific regions where logistics automation investments grew 18% year-over-year in 2023. Major manufacturers have responded by developing ruggedized ToF solutions capable of operating in challenging conditions, such as low-light environments and extreme temperatures from -40°C to +85°C.

Technological Advancements in Sensor Performance Drive Market Evolution

Recent breakthroughs in ToF sensor technology address longstanding industry challenges regarding accuracy and environmental interference. Next-generation chipsets now incorporate multi-zone depth mapping and ambient light cancellation technologies, achieving 95%+ reliability in high-glare manufacturing environments. In 2023, several leading manufacturers introduced sensors with integrated AI processors capable of real-time object classification – a feature that reduces latency in automated inspection systems by up to 40%. As these innovations reduce total system costs while improving performance, adoption barriers continue to decrease across small and medium enterprises.

MARKET RESTRAINTS

High Implementation Costs Limit SME Adoption Potential

While ToF 3D sensors offer clear operational benefits, their premium pricing structure remains a significant adoption barrier for cost-sensitive manufacturers. A complete industrial ToF vision system typically costs 3-5 times more than equivalent 2D solutions, with high-performance models exceeding $500 per unit. This pricing dynamic particularly impacts small-to-medium manufacturers operating on thin margins, where the return on investment period often exceeds 24 months. Additionally, integration expenses – including specialized mounting hardware, calibration tools, and software interfaces – can add 30-50% to total implementation costs, further slowing market penetration in certain industrial segments.

Technical Limitations in Challenging Environments Pose Adoption Barriers

Despite performance improvements, ToF sensors still face fundamental limitations in certain industrial scenarios. Highly reflective surfaces, fast-moving objects, and environments with particulate matter (such as welding shops or food processing plants) can degrade measurement accuracy by 15-25%. These challenges necessitate additional sensor fusion approaches or environmental modifications, increasing overall system complexity. In metal fabrication applications for example, many manufacturers continue to prefer laser triangulation systems which demonstrate better performance consistency on shiny surfaces compared to current ToF solutions, creating a persistent adoption hurdle in this $12 billion sector.

MARKET OPPORTUNITIES

Emerging Smart Factory Initiatives Open New Application Frontiers

Global smart factory initiatives present a $500+ billion opportunity for advanced sensing technologies, with ToF sensors positioned to capture significant market share. Modern facilities increasingly deploy these sensors for volumetric monitoring, worker safety systems, and predictive maintenance applications – use cases expected to grow 35% annually through 2030. Particularly promising is the integration of ToF sensors with digital twin systems, where real-time spatial data improves simulation accuracy by 40-60% compared to conventional input methods. Early adopters in electronics manufacturing have already demonstrated 18-22% productivity gains through such implementations, creating strong incentives for broader industry adoption.

Advancements in Multi-Sensor Fusion Create High-Value Applications

The combination of ToF sensors with complementary technologies like LiDAR and thermal imaging unlocks new capabilities in industrial environments. Recent developments in sensor fusion algorithms now enable millimeter-level accuracy across varied conditions – a capability transforming quality inspection processes in automotive and aerospace sectors. For example, combined ToF-thermal systems can simultaneously detect surface defects and thermal anomalies, reducing inspection times by 50%+ in battery production lines. As fusion technologies mature and standardization improves (with initiatives like OPC UA for device interoperability), the addressable market for these advanced solutions is expected to expand significantly.

MARKET CHALLENGES

Integration Complexity Slows Deployment Timelines

Industrial ToF sensor implementation often requires substantial system integration expertise, creating delays in technology adoption. Many manufacturing facilities report 3-6 month deployment cycles for comprehensive ToF solutions due to calibration requirements, software customization, and operator training needs. This complexity is particularly pronounced in brownfield installations where legacy equipment integration adds further challenges. Surveys indicate that 65% of industrial users consider integration complexity a primary barrier to expanding their ToF sensor deployments, emphasizing the need for more plug-and-play solutions.

Competition from Alternative Technologies Intensifies

The industrial sensing landscape features competing 3D technologies that challenge ToF’s growth trajectory. Stereo vision systems have achieved sub-millimeter accuracy in controlled environments, while structured light solutions continue to dominate high-precision applications under 2 meter ranges. Perhaps most significantly, LiDAR prices have fallen 45% since 2020, making them increasingly competitive for long-range industrial applications. Technology selection remains highly application-specific, requiring thorough evaluation that slows purchase decisions and creates fragmented adoption patterns across different industrial verticals.

INDUSTRIAL TOF 3D IMAGE SENSOR MARKET TRENDS

Advancements in Industrial Automation to Accelerate Adoption of ToF 3D Sensors

The global Industrial Time-of-Flight (ToF) 3D image sensor market is experiencing robust growth, driven by increasing automation across manufacturing sectors. With the market valued at $346 million in 2024 and projected to reach $1.54 billion by 2032 (CAGR of 24.5%), industries are rapidly integrating these sensors for applications like robotic navigation, quality inspection, and volumetric measurement. Recent technological breakthroughs, such as high-resolution ToF sensors capable of functioning in harsh industrial environments, are enhancing their appeal. The development of direct ToF (dToF) sensors with improved depth accuracy and indirect ToF (iToF) variants offering higher frame rates is expanding the technology’s versatility in industrial settings.

Other Trends

Expansion of Smart Factory Initiatives

The proliferation of Industry 4.0 and smart factory concepts is significantly boosting demand for ToF 3D sensors in industrial environments. These sensors enable real-time 3D mapping for autonomous mobile robots (AMRs) and automated guided vehicles (AGVs), critical for modern warehouse logistics. In automotive manufacturing, ToF sensors provide millimeter-accurate measurements for assembly line quality control, reducing defect rates by up to 30% in some applications. The growing emphasis on predictive maintenance systems also relies on continuous 3D monitoring capabilities offered by these sensors.

Emergence of Compact and Robust Sensor Designs

Manufacturers are innovating compact, IP-rated ToF sensor modules that withstand industrial challenges like temperature variations, dust, and vibrations. Recent product launches feature sensors with VGA resolution (640×480 pixels) and measurement ranges exceeding 10 meters, allowing for large-area monitoring in factory settings. These advancements address the critical need for reliable 3D vision systems in heavy industries where traditional cameras struggle with low-light or reflective surface conditions. Moreover, integration with edge computing platforms enables real-time processing of depth data without external computing resources.

COMPETITIVE LANDSCAPE

Key Industry Players

Industrial ToF 3D Sensor Market Sees Intensified Competition as Players Expand Product Offerings

The global Industrial Time-of-Flight (ToF) 3D image sensor market exhibits a moderately consolidated competitive structure, dominated by semiconductor giants alongside specialized sensor manufacturers. With the market projected to grow at 24.5% CAGR through 2032, major players are aggressively expanding their portfolios to capitalize on rising demand for industrial automation solutions.

Infineon Technologies and Sony Semiconductor Solutions currently lead the market, together accounting for approximately 35% of 2024’s $346 million market revenue. Their dominance stems from vertically integrated manufacturing capabilities and established relationships with industrial automation OEMs. Infineon’s recent REAL3™ sensor series, optimized for harsh industrial environments, has been widely adopted in factory automation systems.

The competitive landscape features an interesting dynamic between established semiconductor players and emerging specialists. While giants like Texas Instruments leverage their analog expertise for high-performance indirect ToF solutions, niche players such as Terabee and PMD Technologies compete through innovative direct ToF architectures tailored for specific industrial applications including AGV navigation and volumetric measurement.

Strategic developments in 2023-2024 have further shaped the competitive environment:

- Sony’s partnership with key robotics manufacturers for customized ToF solutions

- AMS’s acquisition of a LiDAR specialist to enhance its 3D sensing capabilities

- Nuvoton’s expansion of industrial-grade ToF sensor production capacity

These moves reflect the broader industry trend of vertical specialization and technological convergence as companies position themselves for the projected $1.5 billion market opportunity by 2032.

Second-tier players including Hamamatsu Photonics and Elmos Semiconductor are responding by focusing on industrial niches – developing ruggedized sensors for extreme temperature operations and high-accuracy solutions for quality inspection applications respectively. This segmentation strategy allows them to maintain strong positions despite the dominance of larger competitors.

The market’s rapid growth continues to attract new entrants, particularly from China, with companies like Vzense and Opnous gaining traction in regional markets through cost-competitive offerings. However, established players maintain their edge through proven reliability, global support networks, and long-term industry partnerships – critical factors in industrial adoption cycles.

List of Key Industrial ToF 3D Image Sensor Companies Profiled

- Infineon Technologies (Germany)

- Sony Semiconductor Solutions (Japan)

- Nuvoton Technology (Taiwan)

- Texas Instruments (U.S.)

- Terabee (France)

- Brookman Technology (Japan)

- ams-OSRAM AG (Austria)

- Elmos Semiconductor (Germany)

- Hamamatsu Photonics (Japan)

- PMD Technologies (Germany)

- MESA Imaging (Switzerland)

- Espros Photonics (Switzerland)

- TriDiCam (Germany)

- Vzense (China)

- Opnous (China)

Segment Analysis

By Type

Direct ToF Sensors Hold Major Market Share Due to High Accuracy in Industrial Applications

The Industrial ToF 3D Image Sensor market is segmented based on sensing technology into:

- Direct Time-of-Flight (ToF)

- Subtypes: Single-point, array-based

- Indirect Time-of-Flight (ToF)

By Application

Factory Automation Emerges as Leading Application Sector Owing to Industrial 4.0 Adoption

The market is segmented based on industrial applications into:

- Factory Automation

- Autonomous Guided Vehicles (AGV)

- Access Control Systems

- Quality Inspection

- Others

By Resolution

High Resolution Sensors Experience Growing Demand for Precision Measurement

The market is segmented based on resolution capabilities into:

- Low Resolution (< QVGA)

- Medium Resolution (QVGA to VGA)

- High Resolution (> VGA)

By Range

Medium Range Sensors Dominate Industrial Applications for Optimal Performance

The market is segmented based on operational range into:

- Short Range (<1m)

- Medium Range (1-5m)

- Long Range (>5m)

Regional Analysis: Industrial ToF 3D Image Sensor Market

Asia-Pacific

Asia-Pacific currently leads the global Industrial ToF 3D Image Sensor market, accounting for over 40% of the total revenue share in 2024, driven primarily by China, Japan, and South Korea. The region dominates due to rapid industrialization, heavy investments in automation, and extensive manufacturing capabilities. China, as the world’s largest manufacturing hub, is accelerating adoption in factory automation, robotics, and quality control applications. Players like Hamamatsu Photonics and Sony are expanding production capacities to meet growing demand. Additionally, government initiatives like Japan’s Society 5.0 and South Korea’s Smart Manufacturing Innovation Strategy support technological adoption.

North America

North America is a key innovator in ToF sensing technology, with industrial applications growing at a CAGR of 21.3%. The U.S. holds the majority share due to strong demand for autonomous guided vehicles (AGVs) and smart factory solutions. Companies like Texas Instruments and Terabee are developing high-resolution sensors for harsh industrial environments. Stricter workplace safety regulations and labor shortages are pushing manufacturers toward automation, further driving adoption. The region also benefits from significant R&D investments in AI-driven machine vision, validating ToF sensors as a cornerstone of Industry 4.0.

Europe

Europe’s market is characterized by stringent industrial safety standards (e.g., ISO 13849), propelling demand for precision ToF sensors in hazardous environments. Countries like Germany and France lead adoption in automotive assembly lines and logistics automation, leveraging players like Infineon and AMS. The EU’s focus on digital transition under the Horizon Europe program supports sensor innovation. However, higher costs and slower ROI calculations compared to traditional sensors remain adoption barriers for SMEs. Despite this, partnerships between research institutions and manufacturers continue to drive cutting-edge developments.

South America

This region shows nascent but steady growth, with Brazil and Argentina as primary markets. The mining and agriculture sectors are early adopters, using ToF sensors for equipment automation and volumetric measurement. Economic constraints and limited local manufacturing limit widespread deployment, but multinational corporations are gradually introducing solutions through partnerships. Chile’s copper mining industry, for instance, has begun integrating ToF-based safety systems, signaling long-term potential.

Middle East & Africa

The market here remains in early stages, with growth concentrated in oil & gas operations and smart city projects across the UAE and Saudi Arabia. High infrastructure development costs slow adoption, but initiatives like NEOM highlight future integration opportunities. Unlike other regions, MEA’s growth is primarily import-driven, with European and Asian suppliers dominating distribution channels. As automation gains traction in logistics and energy sectors, demand for rugged ToF solutions is expected to rise.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Industrial Time-of-Flight (ToF) 3D Image Sensor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Industrial ToF 3D Image Sensor market was valued at USD 346 million in 2024 and is projected to reach USD 1,547 million by 2032, growing at a CAGR of 24.5%.

- Segmentation Analysis: Detailed breakdown by product type (Direct ToF, Indirect ToF), application (Factory Automation, AGV, Access Control, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific leads in adoption due to manufacturing expansion.

- Competitive Landscape: Profiles of 15+ leading market participants including Infineon Technologies, Sony, Texas Instruments, and Hamamatsu Photonics, covering their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends & Innovation: Assessment of AI/ML integration, miniaturization trends, hybrid ToF solutions, and advancements in resolution (up to VGA/1MP) for industrial environments.

- Market Drivers & Restraints: Evaluation of Industry 4.0 adoption, automation demand, and smart factory initiatives versus challenges like high implementation costs and technical limitations in harsh environments.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, industrial automation providers, robotics companies, and investors on emerging opportunities in logistics, quality control, and predictive maintenance applications.

Research methodology combines primary interviews with industry leaders (70% of data sources) and validated secondary data from trade associations, patent filings, and financial reports to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial ToF 3D Image Sensor Market?

-> Industrial ToF 3D Image Sensor market was valued at 346 million in 2024 and is projected to reach US$ 1547 million by 2032, at a CAGR of 24.5% .

Which key companies operate in this market?

-> Major players include Infineon Technologies, Sony, Texas Instruments, Hamamatsu Photonics, and AMS AG, holding 68% combined market share.

What are the key growth drivers?

-> Primary drivers are Industry 4.0 adoption (42% of new installations), demand for precision automation, and AGV deployment growing at 31% CAGR.

Which region dominates the market?

-> Asia-Pacific accounts for 53% market share in 2024, led by China’s manufacturing automation boom, while Europe shows strongest R&D activity.

What are the emerging trends?

-> Key trends include multi-sensor fusion systems, edge computing integration, and ToF solutions for hazardous area monitoring with ATEX certification.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...