MARKET INSIGHTS

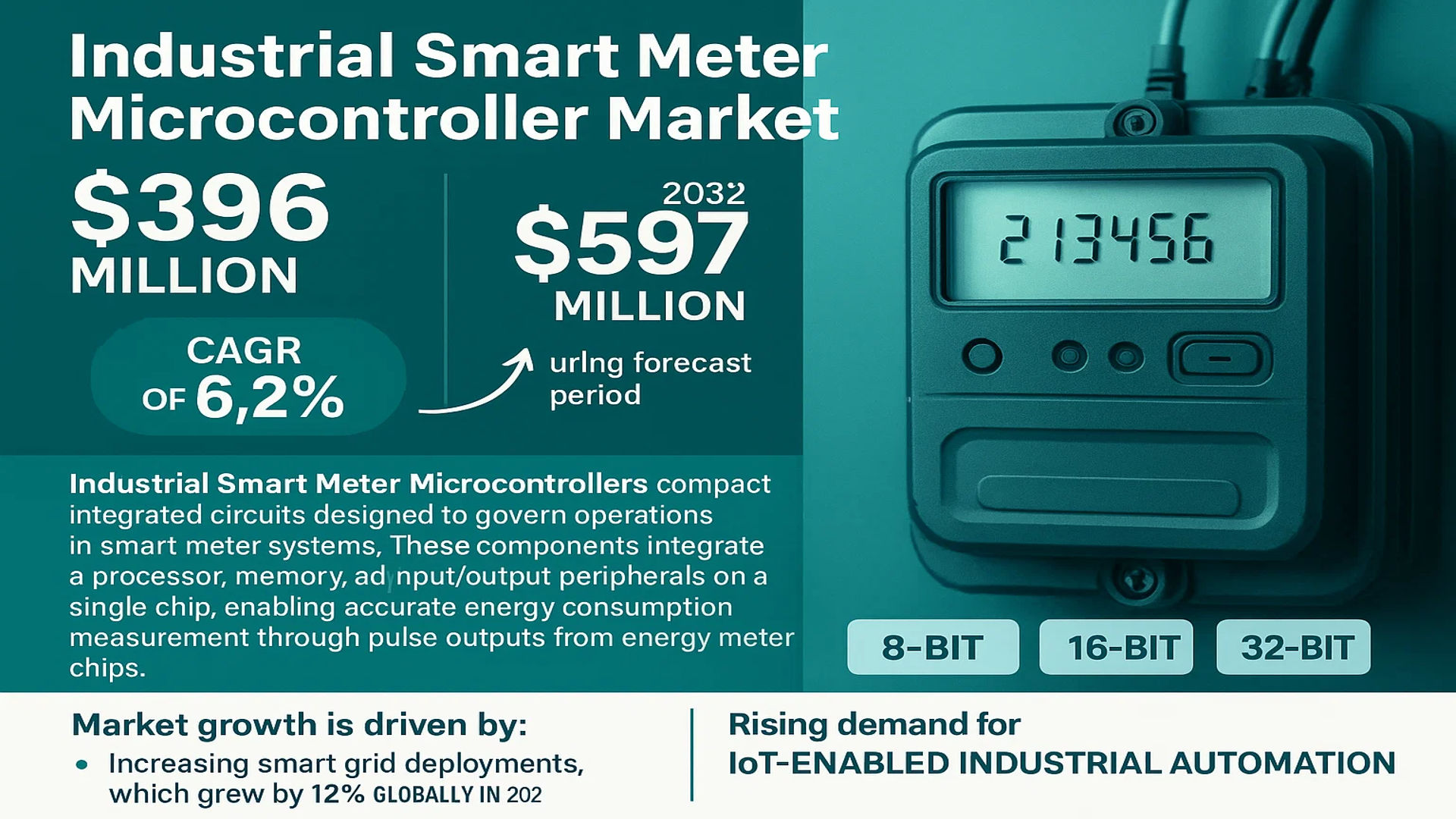

The global Industrial Smart Meter Microcontroller Market was valued at 396 million in 2024 and is projected to reach US$ 597 million by 2032, at a CAGR of 6.2% during the forecast period.

Industrial Smart Meter Microcontrollers are compact integrated circuits designed to govern operations in smart meter systems. These components integrate a processor, memory, and input/output peripherals on a single chip, enabling accurate energy consumption measurement through pulse outputs from energy meter chips. Key variants include 8-bit, 16-bit, and 32-bit microcontrollers, catering to diverse industrial requirements.

Market growth is driven by increasing smart grid deployments, which grew by 12% globally in 2023, and rising demand for IoT-enabled industrial automation. While the broader semiconductor market faces stagnation in MPU/MCU segments, Industrial Smart Meter Microcontrollers show resilience due to utility modernization initiatives. Recent developments include NXP Semiconductors’ 2023 launch of energy-efficient 32-bit MCUs specifically optimized for smart metering applications, addressing the sector’s demand for higher precision and lower power consumption.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Smart Meter Deployments Fueling Microcontroller Demand

The global push for energy efficiency and grid modernization is driving unprecedented smart meter installations, with annual deployments exceeding 120 million units worldwide. Industrial smart meters, requiring robust microcontroller units (MCUs) for advanced metering infrastructure (AMI), are witnessing particularly strong growth. These 32-bit MCUs process complex algorithms for real-time energy monitoring, two-way communication, and predictive maintenance capabilities. Regulatory mandates across regions like the European Union’s Clean Energy Package, which targets 80% smart meter penetration by 2025, are creating sustained demand for industrial-grade microcontrollers with enhanced computational power and connectivity features.

Industrial IoT Expansion Creating New Application Horizons

Industrial IoT adoption is transforming energy monitoring applications, with the industrial IoT market projected to grow at over 15% CAGR through 2030. Smart meter MCUs now integrate wireless protocols like LoRaWAN and NB-IoT directly on-chip, enabling seamless connectivity in harsh industrial environments. This technological evolution allows manufacturers to develop single-chip solutions that reduce board space by up to 30% while improving power efficiency. The convergence of edge computing capabilities with metering applications is further expanding microcontroller requirements, as industrial users demand local data processing to reduce cloud dependency and latency.

Energy Transition Policies Accelerating Market Growth

Global decarbonization initiatives are creating robust demand for precision energy measurement in industrial facilities. Governments worldwide are implementing policies requiring detailed energy consumption reporting from energy-intensive industries. This has led to a 40% increase in demand for industrial smart meters with high-accuracy measurement capabilities over the past three years. Modern microcontrollers now incorporate specialized analog front-ends that achieve measurement accuracy within 0.2% across wide current ranges, making them indispensable for compliance with emerging energy standards and carbon accounting requirements.

MARKET RESTRAINTS

Semiconductor Supply Chain Volatility Impacts Production

The industrial smart meter microcontroller market faces significant challenges from ongoing semiconductor supply chain disruptions. Specialized MCUs for metering applications often require 40-60 weeks lead time due to capacity constraints at mature process nodes. While the broader semiconductor market is projected to grow at 6% annually, microcontroller availability remains tight as industrial customers compete with automotive and consumer segments. This supply-demand imbalance has caused price increases of 15-20% for industrial-grade MCUs over the past two years, forcing some meter manufacturers to redesign products around available components.

Technical Complexity Increases Development Costs

Developing industrial smart meter solutions has become increasingly complex, requiring MCUs to support multiple wireless protocols, security standards, and regional certification requirements. The engineering effort to develop and certify a new industrial smart meter has increased by approximately 35% compared to five years ago. Modern MCUs must now integrate hardware-based security features like secure boot and cryptographic accelerators, while maintaining ultra-low power consumption for battery-powered field deployments. This technical arms race raises both development costs and time-to-market for new metering solutions.

MARKET CHALLENGES

Cybersecurity Threats Require Continuous Innovation

Industrial smart meters face growing cybersecurity risks as connectivity expands, with reported attacks on meter infrastructure increasing by over 200% since 2020. Microcontroller manufacturers must constantly evolve security architectures to address vulnerabilities, adding development overhead. Modern industrial MCUs now incorporate hardware security modules (HSMs) and tamper detection circuitry, but maintaining certification compliance across global markets requires significant ongoing investment. The cybersecurity arms race shows no signs of abating, with regulators increasingly mandating post-quantum cryptography readiness in new meter deployments.

Other Challenges

Long Product Lifecycles Create Compatibility Issues

Industrial smart meters often remain in service for 15-20 years, creating challenges for microcontroller suppliers to maintain long-term component availability. This contrasts sharply with the typical 3-5 year lifecycle of commercial MCUs, requiring specialized product roadmaps and inventory management strategies.

Regional Certification Complexities

Diverging technical standards across markets force MCU vendors to maintain multiple product variants. A single microcontroller platform might need to support 10-15 different regional metering standards, each with unique accuracy, communication protocol, and security requirements.

MARKET OPPORTUNITIES

Next-Generation Energy Management Systems Creating New Demand

The emergence of industrial energy management systems (I-EMS) is driving demand for smart meters with advanced analytics capabilities. Modern microcontrollers now integrate machine learning accelerators that enable local processing of energy consumption patterns. This allows real-time identification of equipment faults and optimization opportunities without cloud connectivity. Leading manufacturers are developing MCU solutions that reduce energy analysis latency from minutes to milliseconds, enabling new preventive maintenance applications that could save industries billions annually in unplanned downtime costs.

Wireless Protocol Convergence Opens New Markets

The ongoing consolidation of industrial IoT wireless standards presents significant opportunities for microcontroller suppliers. Emerging unified protocols like Matter-over-Thread are reducing the need for multiple radio chips in smart meters. MCU vendors that can integrate these evolving standards while maintaining long-range performance will gain competitive advantage in price-sensitive industrial markets. This technology evolution is particularly relevant for industrial campuses implementing comprehensive smart metering networks across diverse equipment and facilities.

INDUSTRIAL SMART METER MICROCONTROLLER MARKET TRENDS

Rising Demand for Smart Grid Modernization Drives Market Growth

The global Industrial Smart Meter Microcontroller Market is experiencing significant momentum due to the accelerating adoption of smart grid technologies. With the market valued at $396 million in 2024 and projected to reach $597 million by 2032, growing at a CAGR of 6.2%, the surge is attributed to infrastructure upgrades in energy management systems. Smart meters equipped with advanced microcontrollers enable real-time electricity monitoring, predictive maintenance, and dynamic pricing models, aligning with global energy conservation mandates. The increasing deployment of 32-bit microcontrollers, which offer superior processing power and connectivity for IoT applications, further strengthens this trend. Utilities across North America, Europe, and Asia-Pacific are actively investing in these solutions to reduce operational inefficiencies.

Other Trends

Integration of AI and Edge Computing

The fusion of AI-driven analytics with smart meter microcontrollers is emerging as a transformative trend. AI enhances the accuracy of load forecasting and anomaly detection by processing real-time energy usage data at the edge—eliminating latency and bandwidth constraints. For instance, microcontrollers with embedded machine learning capabilities are being deployed in industrial smart meters to detect equipment failures before they disrupt operations. Additionally, edge computing minimizes reliance on cloud infrastructure, improving data security. This shift is particularly critical for sectors like manufacturing and healthcare, where uninterrupted power supply is non-negotiable.

Growing Focus on Energy Efficiency Regulations

Governments worldwide are enforcing stringent energy efficiency standards, compelling industries to adopt smart metering solutions. The European Union’s Energy Efficiency Directive and the U.S. Department of Energy’s smart grid initiatives are key drivers, mandating the replacement of traditional meters with IoT-enabled alternatives. Emerging economies like India and China are also scaling up investments in smart grids to curb transmission losses, which currently account for nearly 20% of total electricity generation in some regions. Industrial smart meter microcontrollers, especially those with low-power designs and multi-protocol support (e.g., LoRaWAN, Zigbee), are critical to meeting these regulatory requirements while ensuring interoperability with existing infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Accelerate Innovation to Capture Market Share in Industrial Smart Meter Solutions

The global industrial smart meter microcontroller market exhibits a dynamic competitive environment, characterized by strategic collaborations and technology-driven product developments. With the market projected to grow at a 6.2% CAGR through 2032, key players are investing heavily in advanced microcontroller solutions that enhance energy measurement accuracy and IoT connectivity.

NXP Semiconductors currently leads the market with its robust portfolio of 32-bit ARM-based MCUs, capturing approximately 22% revenue share in 2024. The company’s dominance stems from its extensive smart grid solutions and strong partnerships with utility providers across Europe and North America. Meanwhile, Renesas Electronics follows closely with 18% market share, distinguishing itself through ultra-low-power RL78 MCU series specifically optimized for industrial metering applications.

Chinese manufacturers are making significant inroads, with Shanghai Fudan Microelectronics emerging as a key regional player. The company’s FM33系列 MCUs combine cost-effectiveness with reliable performance, making them particularly popular in Asia-Pacific smart meter deployments. This regional growth reflects the broader industry trend where local players are gaining traction by offering customized solutions for specific regulatory requirements and grid infrastructures.

The competitive landscape continues evolving as companies expand their technological capabilities. Microchip Technology recently introduced its PIC32CM microcontrollers with enhanced security features, addressing growing concerns about data protection in smart grid networks. Similarly, Silicon Labs has been focusing on wireless connectivity integration, enabling seamless communication between smart meters and utility management systems.

List of Key Industrial Smart Meter Microcontroller Companies

- NXP Semiconductors (Netherlands)

- Shanghai Fudan Microelectronics (China)

- HiTrend Technology (China)

- OKI Electric Industry Co., Ltd. (Japan)

- Renesas Electronics Corporation (Japan)

- Microchip Technology Inc. (U.S.)

- Silicon Laboratories Inc. (U.S.)

Segment Analysis:

By Type

32-bit Microcontrollers Lead the Market Due to Advanced Processing Capabilities for Smart Metering

The Industrial Smart Meter Microcontroller market is segmented based on product type into:

- 8-bit

- 16-bit

- 32-bit

By Application

Smart Grid Segment Dominates Owing to Global Infrastructure Modernization Initiatives

The Industrial Smart Meter Microcontroller market is segmented based on application into:

- Smart Grid

- Health Care

- Smart Appliances

- Others

By Technology

IoT-enabled Controllers Drive Growth Through Enhanced Connectivity Features

The Industrial Smart Meter Microcontroller market is segmented based on technology into:

- Wired Communication

- Subtypes: PLC, RS-485, Other Protocols

- Wireless Communication

- Subtypes: RF, Cellular, Other Wireless Technologies

By Power Consumption

Ultra-Low Power MCUs Gain Traction for Energy Efficient Metering Solutions

The Industrial Smart Meter Microcontroller market is segmented based on power consumption into:

- Low Power

- Ultra-Low Power

- Standard Power

Regional Analysis: Industrial Smart Meter Microcontroller Market

Asia-Pacific

The Asia-Pacific region dominates the Industrial Smart Meter Microcontroller market, accounting for over 42% of global demand in 2024, driven primarily by China’s aggressive smart grid initiatives and India’s rapid urbanization. China invested approximately $24 billion in smart meter installations last year as part of its 14th Five-Year Plan, creating sustained demand for 32-bit microcontrollers with advanced communication capabilities. India’s government-backed smart cities mission further propels adoption, though price sensitivity maintains demand for cost-effective 8-bit and 16-bit solutions in secondary markets. Japan and South Korea contribute significantly through their technologically advanced manufacturing ecosystems, focusing on high-precision metering solutions for industrial applications.

North America

Stringent energy efficiency mandates like California’s Title 20 and the U.S. Department of Energy’s grid modernization programs underpin a mature yet growing market. The region shows strong preference for secure, IoT-enabled 32-bit MCUs, with cybersecurity features becoming non-negotiable for smart grid operators. Canada’s focus on remote metering solutions for its expansive geography creates specialized demand for low-power, weather-resistant microcontroller designs. North American manufacturers increasingly integrate AI capabilities into metering systems, pushing MCU performance requirements beyond traditional measurement functions into predictive maintenance applications.

Europe

EU directives on energy efficiency (EU 2019/944) and the Green Deal initiative drive market growth, with Germany and France leading in advanced metering infrastructure (AMI) deployments. The region exhibits highest adoption of multi-core MCUs capable of handling complex billing algorithms and secure data transmission. Nordic countries pioneer innovative submetering solutions for district heating systems, requiring specialized microcontroller configurations. However, prolonged certification processes for utility-grade components under RED Directive occasionally delay product launches, creating supply chain bottlenecks for European smart meter manufacturers.

South America

Brazil’s large-scale AMI projects, particularly in São Paulo and Rio de Janeiro, generate steady demand, though economic volatility affects procurement cycles. Argentina shows potential with its RenovAr renewable energy program creating secondary demand for smart metering solutions. The region predominantly utilizes mid-range 16-bit MCUs, balancing functionality with cost considerations. Local content requirements in some countries encourage regional microcontroller assembly but limit access to cutting-edge global technologies due to intellectual property transfer constraints.

Middle East & Africa

GCC nations, particularly Saudi Arabia and UAE, drive regional growth through massive investments in smart city projects and utility digitization programs. Saudi Arabia’s Smart Meter Initiative aims to deploy 10 million units by 2025, favoring ruggedized MCUs capable of withstanding extreme temperatures. Africa’s market remains nascent but shows promise through donor-funded electrification projects incorporating prepaid metering. The region faces challenges in last-mile connectivity infrastructure, prompting demand for hybrid MCUs supporting both RF and PLC communication protocols.

Report Scope

This market research report provides a comprehensive analysis of the Global Industrial Smart Meter Microcontroller Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 396 million in 2024 and is projected to reach USD 597 million by 2032, growing at a CAGR of 6.2%.

- Segmentation Analysis: Detailed breakdown by product type (8-bit, 16-bit, 32-bit), application (Smart Grid, Health Care, Smart Appliances, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for major economies.

- Competitive Landscape: Profiles of leading market participants including NXP Semiconductors, Renesas Electronics, Microchip Technology, and Silicon Labs, covering their product portfolios, market strategies, and recent developments.

- Technology Trends: Assessment of IoT integration, advanced metering infrastructure (AMI) developments, and power management innovations in microcontroller design.

- Market Drivers & Restraints: Analysis of smart grid modernization initiatives, regulatory mandates for energy efficiency, and challenges in legacy system integration.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, smart meter OEMs, utility companies, and investors regarding market opportunities.

The research employs primary and secondary methodologies, including interviews with industry leaders and analysis of verified market data from authoritative sources.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial Smart Meter Microcontroller Market?

-> Industrial Smart Meter Microcontroller Market was valued at 396 million in 2024 and is projected to reach US$ 597 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in this market?

-> Major players include NXP Semiconductors, Renesas Electronics, Microchip Technology, Silicon Labs, Shanghai Fudan Microelectronics, and HiTrend Technology.

What are the key growth drivers?

-> Growth is driven by smart grid deployments, government energy efficiency mandates, and increasing IoT adoption in industrial applications.

Which region dominates the market?

-> Asia-Pacific leads in market share due to rapid smart meter adoption, while North America shows strong growth in advanced metering infrastructure.

What are the emerging trends?

-> Emerging trends include AI-enabled smart meters, ultra-low-power microcontroller designs, and integration with 5G networks for real-time data analytics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...