MARKET INSIGHTS

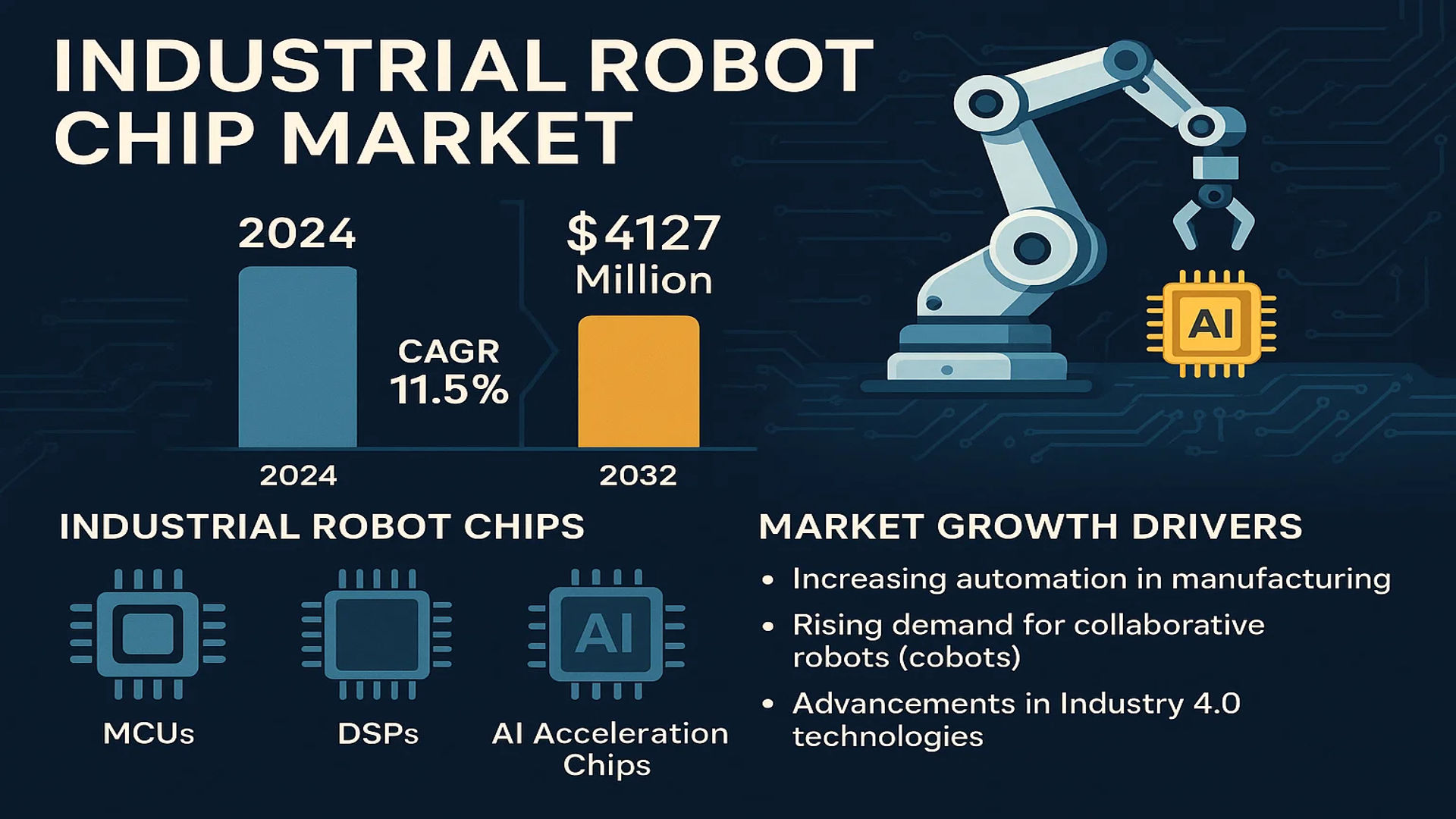

The global Industrial Robot Chip Market was valued at 2060 million in 2024 and is projected to reach US$ 4127 million by 2032, at a CAGR of 11.5% during the forecast period.

Industrial robot chips are specialized semiconductor components designed to enable advanced functionalities in robotic systems. These chips integrate processing power, real-time motion control, AI-based decision-making capabilities, and secure communication protocols essential for industrial automation. They are categorized into microcontroller units (MCUs), digital signal processors (DSPs), and specialized AI acceleration chips, each serving distinct functions in robotic applications.

The market growth is driven by increasing automation in manufacturing, rising demand for collaborative robots (cobots), and advancements in Industry 4.0 technologies. The U.S. currently represents a significant market share, while China is emerging as the fastest-growing region due to government initiatives like Made in China 2025. Leading semiconductor companies including Intel, Nvidia, and STMicroelectronics are investing heavily in robotics-specific chip development to capture this expanding market.

MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Automation Globally Fuels Market Expansion

The industrial robot chip market is experiencing robust growth driven by the accelerating adoption of automation across manufacturing sectors. Industrial robots equipped with advanced chips are enabling precise motion control, real-time data processing, and AI-powered decision making in production lines. The automotive industry remains the largest adopter, accounting for nearly 30% of industrial robot deployments, where chips support welding, painting and assembly applications with millimeter precision. Beyond traditional manufacturing, logistics operators are increasingly implementing robotic systems for sorting and material handling, further driving semiconductor demand.

Advancements in AI Chip Architecture Accelerate Market Growth

Innovations in microprocessor architecture are creating new opportunities for industrial robotics. Modern robot chips integrate neural processing units alongside traditional CPUs and GPUs to enable real-time machine learning at the edge. This evolution allows robots to adapt to dynamic environments without cloud connectivity. Leading semiconductor firms have developed specialized AI acceleration cores that deliver up to 10x performance improvements for robotic vision systems compared to conventional processors. Such technological breakthroughs are enabling a new generation of collaborative robots that can work safely alongside human operators while maintaining high precision.

Government Initiatives Supporting Smart Manufacturing Boost Adoption

National industrial policies worldwide are accelerating the transition to automated manufacturing, indirectly driving semiconductor demand. Many countries have introduced tax incentives and subsidy programs to encourage factory modernization, with particular emphasis on Industry 4.0 technologies. In certain markets, government-backed financing covers up to 40% of robotic system acquisition costs. These strategic initiatives combined with the growing need to reshore manufacturing operations are creating favorable conditions for industrial robot chip suppliers. As manufacturers strive to improve productivity amidst labor shortages, the demand for robot-enabled automation continues to rise substantially.

MARKET RESTRAINTS

Semiconductor Supply Chain Constraints Limit Market Potential

While industrial robot adoption grows, the market faces significant headwinds from ongoing semiconductor supply chain disruptions. Specialized chips for robotics often require advanced manufacturing nodes below 28nm, creating production bottlenecks. Average lead times for industrial-grade processors have extended to 45-55 weeks in recent years, forcing some robot OEMs to redesign systems around available components. This supply-demand imbalance has been particularly challenging for small and medium manufacturers who lack the purchasing power of large corporations.

Other Challenges

High Implementation Costs

The total cost of robotic automation remains prohibitive for many enterprises. Beyond the robot hardware itself, companies must invest in peripheral equipment, safety systems, and workforce training. For a single robotic cell integrating vision systems and force sensors powered by advanced chips, implementation costs frequently exceed $200,000. These substantial capital requirements create barriers to entry, particularly in cost-sensitive emerging markets.

Technical Complexity

Integrating robotic systems into existing production environments presents significant technical hurdles. Many industrial facilities lack the necessary digital infrastructure and skilled personnel to implement and maintain robotic solutions effectively. The interoperability challenges between different generations of automation equipment further complicate adoption timelines, sometimes delaying projects by six months or more.

MARKET OPPORTUNITIES

Emerging Applications in Non-Traditional Sectors Create New Growth Avenues

The industrial robot chip market is poised for expansion beyond manufacturing as new applications emerge across diverse sectors. Healthcare institutions are increasingly adopting robotic assistants for logistics and patient care, requiring specialized chips that meet medical safety standards. Agriculture represents another growth frontier, where autonomous robots with advanced sensor fusion capabilities are transforming harvest operations. The construction industry is similarly exploring robotic solutions for bricklaying and concrete work in hazardous environments.

Development of Edge Computing Solutions Enhances Market Potential

The shift toward decentralized computing architectures presents significant opportunities for industrial robot chip manufacturers. Modern robotic systems are incorporating more processing power directly into the robot controller to reduce latency and improve reliability. This trend is driving demand for system-on-chip solutions that integrate multiple processing units while meeting industrial temperature and vibration requirements. Semiconductor companies that can deliver these integrated solutions with long-term availability guarantees stand to gain substantial market share.

Advancements in Human-Robot Collaboration Open New Possibilities

The growing emphasis on collaborative robotics (cobots) creates opportunities for specialized chip designs. Unlike traditional industrial robots operating behind safety barriers, cobots require sophisticated sensors and processors that can ensure human safety in shared workspaces. Research into new tactile sensing technologies and predictive algorithms is enabling next-generation chips that can detect and react to human presence with millisecond response times. This emerging segment shows particular promise in SME applications where space constraints prohibit traditional automation approaches.

INDUSTRIAL ROBOT CHIP MARKET TRENDS

AI and Edge Computing Integration Driving Industrial Robot Chip Expansion

The integration of Artificial Intelligence (AI) and edge computing into industrial robot chips is transforming automation capabilities across manufacturing and logistics sectors. Advanced chips with neural processing units (NPUs) enable real-time decision-making, predictive maintenance, and adaptive learning without relying on cloud-based systems. For instance, Nvidia’s Jetson AGX Orin chip delivers 275 trillion operations per second, empowering industrial robots with autonomous navigation and precision operations. As AI adoption in robotics grows at a CAGR of 29.2%, semiconductor manufacturers are prioritizing low-latency, high-performance designs to meet Industry 4.0 demands.

Other Trends

Surging Demand for Collaborative Robots (Cobots)

The rise of collaborative robots, or cobots, is accelerating demand for compact, energy-efficient robot chips. Unlike traditional industrial robots, cobots operate alongside humans, requiring chips with advanced safety protocols like torque-limiting sensors and AI-driven collision detection. The cobot market is projected to grow at 36% annually, driven by SMEs adopting automation. This trend favors microcontroller units (MCUs) with real-time operating systems, such as those from STMicroelectronics, which dominate 22% of the industrial MCU segment.

Semiconductor Shortages and Supply Chain Resilience

While the industrial robot chip market grows, it faces constraints from global semiconductor supply chain disruptions15-20% price increases for MCUs and DSPs since 2022. Companies like Qualcomm are mitigating risks through multi-sourcing strategies, while regionalization efforts in the U.S. (CHIPS Act) and EU (European Chips Act) aim to boost local production. The U.S. now accounts for 32% of industrial chip R&D, signaling a push for supply chain independence.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants and Emerging Innovators Compete for Robotics Market Share

The global industrial robot chip market features a highly competitive landscape dominated by semiconductor powerhouses alongside specialized AI and computing firms. STMicroelectronics has emerged as a frontrunner, leveraging its expertise in microcontroller units (MCUs) and power management ICs favored in precision robotics applications. The company’s strong European manufacturing base and recent partnerships with automation leaders have solidified its market position.

Nvidia and Intel have significantly increased their market penetration through AI-optimized processors, capturing nearly 28% combined share of high-performance robotics compute solutions in 2024 according to industry benchmarks. Their chips enable advanced capabilities like computer vision and machine learning, becoming essential for next-generation collaborative robots (cobots).

Meanwhile, Qualcomm has made substantial inroads in mobile robotics through its system-on-chip (SoC) designs optimized for 5G connectivity and edge computing. The company’s recent diversification into industrial applications has positioned it as a key supplier for autonomous guided vehicles (AGVs) and logistics robots.

Specialized players like NXP Semiconductors and Rockchip Electronics are gaining traction through customized solutions for specific robotic applications. Their focus on robust, real-time processing chips for harsh industrial environments has created strong niche positions in automotive manufacturing and heavy machinery sectors.

List of Key Industrial Robot Chip Manufacturers

- STMicroelectronics (Switzerland)

- Intel Corporation (U.S.)

- Nvidia Corporation (U.S.)

- Qualcomm Technologies (U.S.)

- HiSilicon (China)

- Amicro Semiconductor (China)

- Advanced Micro Devices (U.S.)

- NXP Semiconductors (Netherlands)

- Rockchip Electronics (China)

Competition in the industrial robot chip sector is intensifying as manufacturers expand beyond traditional computing capabilities to deliver integrated solutions combining processing, sensing, and connectivity. Many players are adopting vertical integration strategies, acquiring specialized AI startups or forming technology alliances to strengthen their offerings. The next phase of competition will likely focus on energy efficiency and miniaturization as robotic applications proliferate across industries.

Industrial Robot Chip Market: Segment Analysis

By Type

MCU (Microcontroller Chip) Segment Leads Due to High Demand for Real-Time Control in Robotics

The market is segmented based on type into:

- MCU (Microcontroller Chip)

- Subtypes: 8-bit, 16-bit, 32-bit, and others

- DSP (Digital Signal Processing Chip)

- Subtypes: Fixed-point, Floating-point, and others

- FPGA (Field Programmable Gate Array)

- MPU (Microprocessor Unit)

- Others

- Including ASICs, AI accelerators, and hybrid chips

By Application

Multi-axis Robots Segment Dominates Owing to Increased Automation in Manufacturing

The market is segmented based on application into:

- Multi-axis Robots

- Subtypes: 6-axis, 7-axis, and collaborative robots (cobots)

- SCARA Robots

- Coordinate Robots

- Subtypes: Cartesian and parallel robots

- Mobile Robots

- Others

- Including service robots and specialty robots

By End-User Industry

Automotive Industry Holds Significant Share Due to High Robot Integration in Assembly Lines

The market is segmented based on end-user industry into:

- Automotive

- Electronics & Semiconductor

- Healthcare & Pharmaceuticals

- Food & Beverage

- Logistics & Warehousing

- Others

- Including aerospace, metal processing, and construction

Regional Analysis: Industrial Robot Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global industrial robot chip market, accounting for over 60% of worldwide demand, primarily driven by China’s aggressive manufacturing automation initiatives. With its “Made in China 2025” policy and rapid adoption of Industry 4.0 technologies, China alone represents nearly 45% of the regional market. Japan and South Korea follow closely, with established robotics industries supported by semiconductor leaders like HiSilicon and Rockchip Electronics. The region benefits from concentrated electronics manufacturing hubs, government subsidies for automation, and increasing labor costs pushing manufacturers toward robotic solutions. However, geopolitical tensions and semiconductor supply chain vulnerabilities present challenges to sustained growth.

North America

North America’s industrial robot chip market is propelled by advanced manufacturing sectors and significant R&D investments from firms like Intel and Nvidia. The U.S. accounts for approximately 85% of regional demand, with automotive and aerospace industries driving adoption of high-performance chips for collaborative robots (cobots) and AI-enabled systems. Recent CHIPS Act funding of $52 billion boosts domestic semiconductor production, reducing reliance on Asian suppliers. Strict export controls on advanced chips to China create both opportunities for local manufacturers and challenges for global supply chains. The region shows particular strength in DSP chips for precision robotics applications.

Europe

Europe maintains a strong position in the industrial robot chip market, with Germany leading through its Industrial IoT initiatives and robust automotive robotics sector. STMicroelectronics and NXP Semiconductors anchor the regional supply chain, focusing on energy-efficient chips compliant with EU sustainability directives. The market is transitioning toward AI-optimized chips for smart manufacturing, with collaborative robot applications growing at a 14% CAGR. Challenges include higher production costs compared to Asian manufacturers and fragmented adoption rates across Eastern and Western European nations. The EU’s Digital Compass initiative aims to double semiconductor production by 2030, potentially reshaping regional dynamics.

Middle East & Africa

This emerging market shows gradual growth, primarily concentrated in GCC nations’ oil/gas and logistics sectors. The UAE and Saudi Arabia lead in adopting robotic automation, with smart city projects driving demand for basic control chips. While the region currently represents less than 3% of global market share, increasing foreign investment in technology infrastructure and growing awareness of Industry 4.0 principles suggest long-term potential. Limited local semiconductor capabilities mean nearly all chips are imported, creating opportunities for international suppliers. Economic diversification strategies in the Gulf could accelerate robotics adoption in coming years.

South America

South America’s market remains nascent, constrained by economic volatility and limited industrial automation penetration. Brazil accounts for over 60% of regional demand, particularly in automotive and mining applications. The lack of local chip production facilities creates complete import dependence, with most suppliers serving the market through distributors. While countries like Argentina show growing interest in agricultural robotics, widespread adoption awaits more stable economic conditions and infrastructure development. The region presents opportunities for cost-effective MCU solutions targeting small-to-medium manufacturers beginning their automation journeys.

Report Scope

This market research report provides a comprehensive analysis of the Global Industrial Robot Chip Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 2060 million in 2024 and is projected to reach USD 4127 million by 2032, growing at a CAGR of 11.5%.

- Segmentation Analysis: Detailed breakdown by product type (MCU, DSP, Others), application (Multi-axis Robots, SCARA Robots, Coordinate Robots), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific showing rapid growth.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards in industrial robotics.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial Robot Chip Market?

-> Industrial Robot Chip Market was valued at 2060 million in 2024 and is projected to reach US$ 4127 million by 2032, at a CAGR of 11.5% during the forecast period.

Which key companies operate in Global Industrial Robot Chip Market?

-> Key players include STMicroelectronics, Intel, Nvidia, Qualcomm, HiSilicon, Amicro, Advanced Micro Devices, NXP, and Rockchip Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include automation in manufacturing, Industry 4.0 adoption, labor cost reduction, and demand for high-precision robotics.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by manufacturing expansion in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include AI-powered robotic chips, edge computing integration, and energy-efficient semiconductor designs for industrial automation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...