Industrial IoT Sensors Market Insights

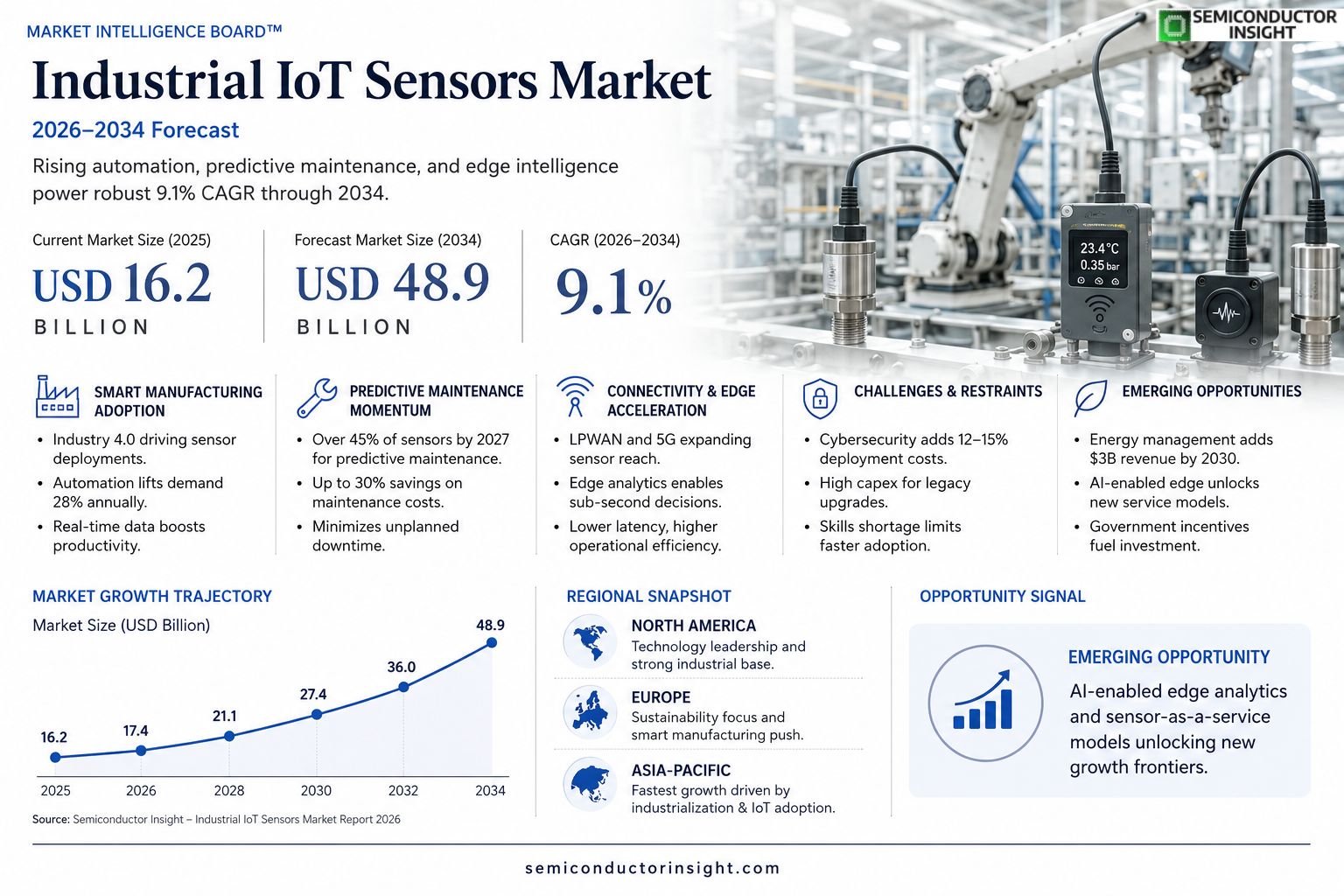

Global industrial IoT sensors market size was valued at USD 16.2 billion in 2025. The market is projected to grow from USD 17.4 billion in 2026 to USD 48.9 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period.

Industrial IoT sensors are devices that capture real‑time measurements such as temperature, pressure, vibration, humidity and proximity within manufacturing plants, energy facilities, transportation systems and critical infrastructure. By transmitting this data over wired or wireless networks to analytics platforms, they enable predictive maintenance, process optimization and enhanced safety.The market is experiencing rapid growth because of expanding Industry 4.0 initiatives, rising automation demand across factories and a strong focus on energy efficiency and sustainability. Furthermore, advances in low‑power wide‑area network (LPWAN) technologies and edge computing are accelerating sensor deployments. Initiatives by key players such as Siemens AG, Honeywell International Inc., Bosch Sensortec GmbH and Texas Instruments are also expected to fuel market expansion.

MARKET DRIVERS

Rapid Adoption of Smart Manufacturing

Industrial IoT Sensors Market is being propelled by manufacturers’ shift toward smart factories, where real‑time data collection improves equipment uptime and reduces waste. Automation initiatives are projected to lift global sensor deployments by 28% annually, creating a robust demand pipeline.

Growth of Predictive Maintenance Strategies

Enterprises are increasingly leveraging predictive maintenance to avoid costly unplanned outages. By 2027, predictive‑maintenance‑enabled sensors are expected to account for over 45% of total sensor shipments, driven by measurable cost savings of up to 30% on maintenance budgets.

➤ Integration of 5G connectivity enhances sensor data latency, enabling sub‑second decision loops for critical process control.

In addition, the rollout of private 5G networks across industrial parks accelerates edge‑to‑cloud data flows, further cementing the role of Industrial IoT Sensors Market as a foundational technology for next‑generation production.

MARKET CHALLENGES

Cybersecurity Concerns in Connected Environments

As sensor networks expand, the attack surface for cyber threats widens. Companies must invest in robust encryption and authentication mechanisms, which can add 12‑15% to total deployment costs and slow adoption curves.

Other Challenges

Standardization Gaps

The lack of universally accepted communication standards leads to interoperability issues, forcing end‑users to rely on proprietary gateways that increase system complexity.Furthermore, regulatory compliance in regions such as the EU and North America imposes stringent data‑privacy requirements, compelling manufacturers to incorporate additional compliance layers into sensor solutions.

MARKET RESTRAINTS

High Capital Expenditure for Legacy Plant Upgrades

Many established factories operate on aging equipment that cannot accommodate modern sensor interfaces without significant retrofitting. The associated capital outlay, often exceeding $1.5 million per plant, deters smaller operators from immediate investment.Additionally, the cost of skilled personnel to install, calibrate, and maintain advanced sensor arrays remains a limiting factor, especially in regions with limited technical talent pools.Current economic uncertainty also pressures capital budgets, prompting firms to prioritize short‑term operational improvements over long‑term digital transformation projects.

MARKET OPPORTUNITIES

Emerging Applications in Energy Management

Energy‑intensive sectors such as steel, chemicals, and oil & gas are exploring sensor‑driven optimization to lower consumption. Deployments that enable real‑time monitoring of temperature, vibration, and flow are projected to add $3 billion in revenue to Industrial IoT Sensors Market by 2030.Another promising avenue lies in the integration of AI‑enabled edge analytics, which reduces dependence on centralized cloud infrastructure and offers faster anomaly detection. This convergence is expected to unlock new business models centered on sensor‑as‑a‑service.Finally, government incentives for Industry 4.0 initiatives across Asia‑Pacific and Europe are creating a favorable investment climate, encouraging both incumbents and startups to accelerate sensor‑centric solutions.

Industrial IoT Sensors Market Trends

Rise of Edge‑Enabled Predictive Maintenance

Manufacturers are increasingly embedding edge‑computing capabilities directly within sensor nodes to reduce latency and bandwidth consumption. This shift enables real‑time analysis of temperature, vibration, pressure and humidity data at the source, allowing maintenance teams to identify equipment anomalies before failure occurs. The result is a measurable decline in unplanned downtime and a smoother production flow. Companies are also integrating these edge‑enabled sensors with cloud‑based analytics platforms, creating a hybrid architecture that balances local decision‑making with centralized insight. The combined approach supports more accurate forecasting of component wear and aligns maintenance schedules with actual operating conditions, rather than fixed calendar intervals.

Other Trends

Adoption of Low‑Power Wide‑Area Networks

Low‑Power Wide‑Area Network (LPWAN) technologies such as LoRaWAN and NB‑IoT are accelerating sensor deployments across geographically dispersed facilities. Their ability to transmit small data packets over several kilometers while consuming minimal energy makes them ideal for remote monitoring of pipelines, wind farms and large‑scale manufacturing plants. As LPWAN standards mature, integration with existing industrial protocols becomes seamless, reducing the need for extensive gateway infrastructure. Additionally, the extended battery life,often measured in years,lowers total cost of ownership and simplifies maintenance logistics. These network advantages are prompting a broader range of operators, including utilities and transportation agencies, to adopt industrial IoT sensors for continuous condition monitoring and regulatory compliance.

Sustainability and Energy‑Efficiency Focus

Regulatory pressure and corporate sustainability goals are driving investment in sensor solutions that improve energy efficiency. By delivering granular data on power consumption, temperature gradients and equipment load, sensors help facilities pinpoint wasteful processes and implement corrective actions. The resulting energy savings not only reduce operational expenditure but also support carbon‑reduction commitments. Vendors are responding with sensor packages that incorporate energy‑harvesting techniques, further minimizing the environmental footprint of monitoring systems. This convergence of sustainability imperatives and technology innovation is shaping the strategic roadmap for Industrial IoT Sensors Market.

COMPETITIVE LANDSCAPEKey Industry Players

Industrial IoT Sensors Market – Competitive Landscape Overview

Industrial IoT Sensors Market is dominated by a handful of large multinational technology firms that leverage extensive R&D budgets, global distribution networks, and deep integration capabilities. Siemens AG leads with its comprehensive portfolio that spans predictive‑maintenance sensors, edge‑ready connectivity modules, and fully managed analytics services for heavy‑industry customers. Honeywell International Inc. follows closely, offering robust sensor solutions for aerospace, oil & gas, and process automation, while Bosch Sensortec GmbH differentiates itself through miniaturized MEMS devices optimized for low‑power applications in smart factories. Texas Instruments contributes a strong analog and mixed‑signal sensor line that underpins many LPWAN deployments, reinforcing a market structure where a few tier‑1 players command the majority of high‑value contracts and set industry standards.Beyond the tier‑1 giants, a vibrant ecosystem of specialized manufacturers provides niche capabilities that address vertical‑specific requirements. Schneider Electric and ABB focus on integrated smart‑grid and factory‑automation sensor suites, whereas Rockwell Automation supplies rugged instrumentation for legacy PLC environments. TE Connectivity, Analog Devices, and STMicroelectronics deliver high‑precision sensing elements for vibration and temperature monitoring. Infineon Technologies, Yokogawa Electric, and Murata Manufacturing add expertise in wireless power and high‑frequency sensor designs, while GE Digital and Emerson Electric round out the landscape with software‑centric sensor analytics platforms that enable end‑to‑end digital transformation across diverse industrial segments.

List of Key Industrial IoT Sensors Companies Profiled

- Siemens AG

- Honeywell International Inc.

- Bosch Sensortec GmbH

- Texas Instruments

- Schneider Electric

- ABB Ltd.

- Rockwell Automation

- TE Connectivity

- Analog Devices

- STMicroelectronics

- Infineon Technologies

- Yokogawa Electric Corporation

- Murata Manufacturing Co., Ltd.

- GE Digital

- Emerson Electric Co.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Temperature sensors drive adoption because they provide continuous thermal monitoring that supports early fault detection, enable energy‑efficient process control, and integrate seamlessly with edge analytics platforms.

|

| By Application |

|

Predictive maintenance stands out as the primary driver, leveraging real‑time sensor data to anticipate equipment failures and schedule interventions without disrupting production.

|

| By End User |

|

Manufacturing plants exhibit the strongest appetite for IoT sensors, seeking tighter process control, higher throughput, and safer work environments.

|

| By Connectivity |

|

LPWAN emerges as the preferred connectivity for remote or distributed sensor deployments, offering extensive coverage with minimal power consumption.

|

| By Deployment Scale |

|

Plant‑wide networks dominate strategic initiatives, as they allow seamless data flow across production lines and facilitate enterprise‑level optimization.

|

Regional Analysis: North America

North America

The manufacturing sector in North America is a primary consumer of Industrial IoT Sensors. Companies are leveraging these sensors to monitor production processes, track asset utilization, and ensure quality control. The increasing adoption of smart factories is directly contributing to the demand for a wide range of sensors, from temperature and pressure sensors to vibration and proximity sensors.

The oil and gas industry in North America is actively implementing Industrial IoT Sensors for pipeline monitoring, equipment health assessment, and safety applications. Remote monitoring capabilities offered by these sensors are particularly valuable in geographically challenging environments, enhancing operational safety and reducing risks associated with leaks and spills.

The logistics and transportation sector is utilizing Industrial IoT Sensors to track shipments, monitor vehicle performance, and optimize delivery routes. Real-time visibility into asset locations and conditions is improving supply chain efficiency and reducing potential disruptions. This segment is also witnessing increased adoption of sensors for cold chain monitoring and inventory management.

North American infrastructure projects are incorporating Industrial IoT Sensors for monitoring structural health, predicting maintenance needs, and improving overall asset management. Sensors deployed on bridges, buildings, and utilities provide valuable data for proactive maintenance, enhancing safety and extending operational lifespans.

Europe

Europe presents a significant and steadily growing market for Industrial IoT Sensors. The region’s strong industrial heritage, combined with a focus on sustainability and energy efficiency, is driving adoption across various sectors. Government regulations promoting smart manufacturing and environmental monitoring are further boosting market growth. Key applications include predictive maintenance in automotive and aerospace, energy management in industrial facilities, and asset tracking in logistics. The emphasis on data security and privacy is a crucial consideration in the European market.

Asia-Pacific

Asia-Pacific is the fastest-growing region for Industrial IoT Sensors Market, driven by rapid industrialization in countries like China and India. The increasing adoption of Industry 4.0 initiatives, coupled with government support for technological advancements, is fueling demand. Key sectors driving growth include manufacturing, automotive, and infrastructure. The region offers significant opportunities for sensor manufacturers and service providers, but also presents challenges related to fragmented markets and varying regulatory landscapes.

South America

South America’s Industrial IoT Sensors Market is emerging, with growth potential driven by the expansion of manufacturing and mining industries. The increasing need for operational efficiency and cost optimization is a key driver. Key applications include predictive maintenance in mining operations, asset tracking in logistics, and monitoring of critical infrastructure. While the market is still relatively nascent, it presents long-term growth opportunities for players providing tailored solutions.

Middle East & Africa

The Middle East & Africa region is witnessing increasing adoption of Industrial IoT Sensors, particularly in the oil and gas, construction, and infrastructure sectors. Government investments in smart city initiatives and industrial development are contributing to market growth. The region’s focus on energy efficiency and resource management is also driving demand for sensors used in monitoring and optimizing industrial processes.

Report Scope

This market research report provides a comprehensive analysis of the Industrial IoT Sensors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Industrial IoT Sensors Market?

-> Industrial IoT Sensors Market was valued at USD 16.2 billion in 2025 and is expected to reach USD 48.9 billion by 2034.

Which key companies operate in Industrial IoT Sensors Market?

-> Key players include Siemens AG, Honeywell International Inc., Bosch Sensortec GmbH, and Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include Industry 4.0 initiatives, rising automation demand across factories, focus on energy efficiency and sustainability, low‑power wide‑area network (LPWAN) technologies, and edge computing.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include adoption of low‑power wide‑area network (LPWAN) technologies, edge computing integration, and expanded sensor deployments driven by Industry 4.0 initiatives.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...