MARKET INSIGHTS

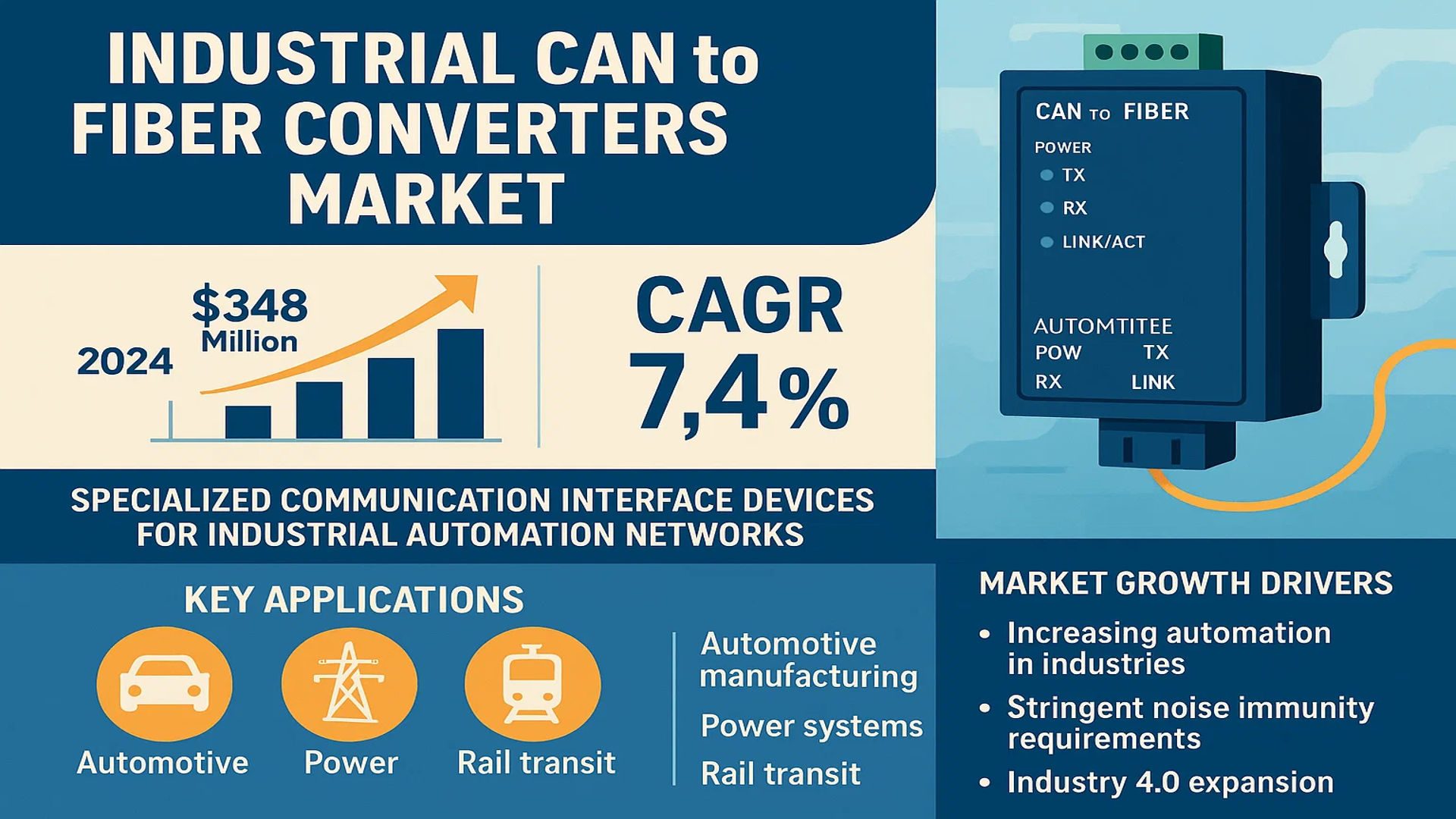

The global Industrial CAN to Fiber Converters Market was valued at 348 million in 2024 and is projected to reach US$ 588 million by 2032, at a CAGR of 7.4% during the forecast period.

Industrial CAN to Fiber Converters are specialized communication interface devices designed for industrial automation networks. These converters facilitate reliable data transmission by converting electrical signals from Controller Area Network (CAN bus) protocols into optical signals for fiber optic cables. Key applications include harsh environments such as automotive manufacturing, power systems, and rail transit, where they provide electrical isolation (2500V), wide temperature tolerance (-40°C to 85°C), and immunity to electromagnetic interference (EMI) across distances up to 20km.

The market growth is driven by increasing automation in industries, stringent requirements for noise immunity in critical infrastructure, and the expansion of Industry 4.0 initiatives. While North America leads in adoption with the U.S. accounting for the largest regional share, Asia-Pacific shows the highest growth potential with China’s rapid industrial digitization. Leading manufacturers like Moxa, Peak-System Technik, and Advantech are focusing on ruggedized designs and protocol compatibility to meet diverse industrial needs.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Industrial Automation and IIoT to Accelerate Adoption of CAN to Fiber Converters

The rapid expansion of Industrial Internet of Things (IIoT) applications is a key driver for the CAN to fiber converter market. Global industrial automation investments are projected to grow significantly, with manufacturing plants increasingly adopting smart factory solutions that rely on robust communication networks. CAN to fiber converters enable reliable data transmission in electrically noisy environments while extending network ranges beyond the limitations of traditional copper-based CAN systems. These devices are becoming indispensable in automotive assembly lines, where electromagnetic interference can disrupt critical control signals. The ability to transmit data over 20 km with immunity to interference makes fiber optic conversion essential for large-scale industrial deployments.

Growing Need for Long-Distance and EMI-Immune Communication in Harsh Environments

Industries operating in extreme environments are driving demand for ruggedized CAN to fiber solutions. The power generation sector particularly benefits from fiber optic conversion in high-voltage substations where electrical isolation up to 2500V prevents ground loops and protects sensitive equipment. Similarly, maritime and offshore applications require the corrosion resistance and reliability that fiber optic connections provide. With industrial networks expanding across larger facilities and remote locations, the market for optical conversion technology continues to grow. Modern CAN to fiber converters operate reliably in temperature ranges from -40°C to 85°C, making them ideal for outdoor installations and challenging industrial settings where standard copper cabling would fail.

Recent product innovations have further stimulated market growth. Leading manufacturers now offer converters with enhanced features like diagnostic LEDs, redundant power inputs, and DIN-rail mounting options. These advancements address the evolving needs of industrial customers who require not just basic signal conversion, but comprehensive network management capabilities. The integration of advanced diagnostics helps maintenance teams quickly identify and resolve network issues, minimizing costly downtime in production environments.

MARKET RESTRAINTS

Higher Implementation Costs Compared to Conventional CAN Solutions Limit Wider Adoption

While offering significant technical advantages, CAN to fiber converters face adoption barriers due to their premium pricing. The total cost of ownership includes not just the converter units but also specialized fiber optic cabling and installation expertise, creating a substantial cost differential versus traditional copper-based CAN networks. Small and medium-sized enterprises often perceive the added expense as prohibitive, especially when their existing copper infrastructure appears functional for short-range applications. This cost sensitivity is particularly evident in developing markets where budget constraints take precedence over future-proofing industrial networks.

The complexity of migrating from legacy systems presents another restraint. Many industrial facilities have extensive investments in copper-based CAN infrastructure, and the transition to fiber optics requires careful planning to avoid disruptions. Retraining maintenance personnel to handle both the fiber optic components and the associated test equipment adds to the implementation costs. These factors collectively slow adoption rates, particularly in price-sensitive industries where the immediate benefits may not justify the capital expenditure.

MARKET OPPORTUNITIES

Expansion of Smart Grid Infrastructure Creates New Application Potential

The global push toward modernizing power distribution networks presents significant opportunities for CAN to fiber converter suppliers. Smart grid deployments require reliable communication across vast geographical areas while withstanding electromagnetic interference from high-voltage equipment. Fiber optic solutions are becoming the preferred choice for these applications, with utilities increasingly specifying optical isolation for substation automation systems. The ability to integrate with legacy industrial protocols while providing future-ready bandwidth makes CAN to fiber converters a strategic component in grid modernization projects.

Emerging industrial wireless applications also create complementary opportunities. While wireless technologies gain traction for mobile equipment and temporary installations, they often require fiber backbone connections for backhaul and system integration. CAN to fiber converters serve as vital bridges between wireless edge devices and wired control systems, enabling hybrid network architectures. Manufacturers who can deliver converters with advanced synchronization features and support for time-sensitive networking protocols are well-positioned to capitalize on these evolving market needs.

MARKET CHALLENGES

Compatibility Issues with Legacy Industrial Systems Pose Integration Hurdles

The industrial automation sector faces significant challenges in integrating modern fiber optic solutions with aging control systems. Many facilities operate equipment with proprietary CAN implementations that don’t fully comply with standard protocols. These variations create compatibility issues when introducing fiber optic converters, as timing requirements and message handling may differ from standardized CAN 2.0A/B specifications. Engineers often need to implement custom solutions or protocol converters, adding complexity and potential points of failure to the network architecture.

Maintenance and troubleshooting in hybrid networks present another operational challenge. While fiber optics provide superior performance, they require specialized test equipment and skilled technicians for installation and maintenance. The scarcity of personnel trained in both industrial networking and fiber optic technologies creates bottlenecks in system deployment and support. This skills gap is particularly acute in regions experiencing rapid industrial growth but lacking the corresponding technical education infrastructure.

Standardization efforts across the industry aim to address these challenges, but progress remains gradual. Manufacturers who can deliver solutions with broader compatibility and simplified maintenance interfaces will gain competitive advantage in this evolving market landscape.

INDUSTRIAL CAN TO FIBER CONVERTERS MARKET TRENDS

Rising Demand for Industrial Automation Driving Market Growth

The global industrial automation sector is experiencing robust growth, fueling the adoption of Industrial CAN to Fiber Converters as critical components in network infrastructure. These devices enable reliable data transmission in harsh industrial environments, especially where electromagnetic interference (EMI) and long-distance communication are major challenges. The market is projected to grow at a compound annual growth rate (CAGR) of 7.4% through 2032, with an estimated valuation of $588 million by that year. The increasing deployment of smart factories and Industry 4.0 technologies is accelerating demand, as high-speed, interference-free communication becomes essential for automated production lines.

Other Trends

Expansion in Automotive and Aerospace Applications

The automotive and aerospace industries are significant contributors to the adoption of CAN to fiber converters, thanks to their high reliability and rugged design. In automotive manufacturing, these converters are used in electric vehicle (EV) production lines and testing environments, where they ensure stable communication between diagnostics systems and CAN-based control units. Similarly, aerospace applications leverage these devices to maintain signal integrity in avionics and ground support systems. With the global EV market projected to expand at a rapid pace, the demand for industrial CAN to fiber converters is expected to rise correspondingly in this segment.

Technological Advancements in Fiber Optic Communication

The integration of next-generation fiber optics is enhancing the capabilities of CAN to fiber converters, enabling faster data transmission and reduced latency. Innovations such as single-mode fiber converters are gaining traction due to their ability to transmit signals over distances exceeding 20 kilometers, making them ideal for large-scale industrial networks. Additionally, manufacturers are increasingly incorporating industrial-grade protection features, including 2500V electrical isolation and extended temperature ranges (-40°C to 85°C), ensuring reliability in extreme conditions. These advancements position CAN to fiber converters as a critical component in modern industrial networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance Strengthened Through Innovation and Strategic Expansion

The global Industrial CAN to Fiber Converters market showcases a competitive yet fragmented landscape, characterized by the presence of established industrial automation players and emerging innovators striving to capitalize on the growing demand for robust communication solutions. The market, valued at $348 million in 2024, is highly dynamic, with companies leveraging technological advancements to enhance product reliability and application-specific solutions.

Moxa leads the market, recognized for its extensive portfolio of industrial networking solutions, including high-performance CAN-to-fiber converters that cater to critical environments like automotive manufacturing and rail systems. The company’s dominance is reinforced by its strong regional presence, especially in North America and Asia-Pacific, where industrial automation investments are surging.

Peak-System Technik and Kvaser follow closely, specializing in CAN-based connectivity solutions with features such as extended temperature ranges (-40°C to 85°C) and high EMI immunity. These players are intensifying R&D efforts to develop compact, energy-efficient converters, targeting sectors like aerospace and renewable energy where space and power constraints are critical.

Meanwhile, Advantech and Renesas are adopting aggressive growth strategies, including partnerships with system integrators and acquisitions, to expand their foothold. For instance, Advantech’s recent collaboration with semiconductor manufacturers has enabled the integration of advanced signal-processing capabilities into their converter modules.

List of Key Industrial CAN to Fiber Converter Companies Profiled

- Moxa (Taiwan)

- Peak-System Technik (Germany)

- Kvaser (Sweden)

- RFC Union (China)

- Advantech (Taiwan)

- Renesas Electronics (Japan)

- RLH Industries, Inc. (U.S.)

- Softing (Germany)

- Brainboxes (U.K.)

Segment Analysis:

By Type

Single-mode Segment Leads Owing to Long-Distance Transmission Capabilities

The market is segmented based on fiber type into:

- Single-mode

- Features: Supports distances up to 20km, low signal attenuation for critical infrastructure

- Multi-mode

- Features: Cost-effective solution for shorter-range industrial applications

By Application

Industrial Automation Segment Dominates Due to Growing Smart Factory Adoption

The market is segmented based on application into:

- Automotive manufacturing

- Use cases: Assembly line control, robotic systems integration

- Power systems

- Use cases: Substation automation, grid monitoring

- Rail transportation

- Use cases: Signaling systems, train communication networks

- Marine systems

- Use cases: Shipboard automation, navigation systems

- Other industrial applications

By Connectivity

Standalone Converters Remain Preferred for Dedicated Industrial Networks

The market is segmented based on connectivity type into:

- Standalone converters

- Rack-mounted solutions

- Modular systems

By Protocol Support

CAN 2.0B Segment Dominates Industrial Communication Standards

The market is segmented based on protocol support into:

- CAN 2.0A

- CAN 2.0B

- CAN FD

Regional Analysis: Industrial CAN to Fiber Converters Market

North America

The North American market for Industrial CAN to Fiber Converters is driven by robust industrial automation adoption, particularly in the U.S. and Canada. With industries like automotive and aerospace leading the demand, manufacturers prioritize high-performance converters to ensure reliable long-distance communication in EMI-heavy environments. The region’s strict industrial safety standards and investments in smart manufacturing under initiatives like Industry 4.0 further bolster growth. Key players like Moxa and RLH Industries dominate the market, offering solutions tailored for harsh operational conditions. However, high adoption costs may slightly hinder small and medium enterprises.

Europe

Europe showcases steady demand, propelled by stringent industrial communication reliability norms under EU directives and the push for energy-efficient automation. Germany, France, and the U.K. lead deployments in sectors like rail transit and industrial machinery. The presence of industry leaders such as Peak-System Technik and Softing ensures technological advancements in fiber-optic CAN solutions. The focus on reducing electromagnetic interference in manufacturing hubs aligns with the region’s sustainability goals. Though growth is consistent, market saturation in mature economies could limit rapid expansion.

Asia-Pacific

As the fastest-growing region, Asia-Pacific thrives due to rapid industrialization in China, India, and Japan. Expanding automotive production and infrastructure projects necessitate reliable data transmission, driving converter adoption. Local manufacturers like CTC Union and Kyland offer cost-competitive solutions, though international brands compete on advanced features. China’s “Made in China 2025” initiative further accelerates demand. However, price sensitivity in emerging markets occasionally leads to preference for non-fiber alternatives, posing a minor challenge to premium segments.

South America

South America presents niche opportunities, primarily in Brazil and Argentina, where mining and manufacturing sectors utilize CAN-to-fiber converters for rugged applications. Economic instability and limited industrial automation penetration hinder widespread adoption, but gradual modernization efforts signal long-term potential. Suppliers face challenges in convincing cost-conscious buyers to invest in fiber solutions over traditional copper-based systems, despite their clear advantages in harsh environments.

Middle East & Africa

The MEA region shows emerging demand, particularly in oil & gas and power utilities across the UAE and Saudi Arabia. Harsh desert conditions make fiber converters ideal for critical data transmission, yet low market awareness and budget constraints slow adoption. Infrastructure development projects, coupled with increasing foreign investments, could catalyze future growth, but the market currently remains in early stages.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Industrial CAN to Fiber Converters markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Industrial CAN to Fiber Converters market was valued at USD 348 million in 2024 and is projected to reach USD 588 million by 2032, growing at a CAGR of 7.4%.

- Segmentation Analysis: Detailed breakdown by product type (single-mode vs. multi-mode), application (automotive, aerospace, industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Moxa, IPC2U, CTC Union, Peak-System Technik, and RLH Industries, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends: Analysis of industrial communication protocols, fiber optic advancements, and integration with Industry 4.0 systems.

- Market Drivers & Restraints: Evaluation of factors including industrial automation growth, demand for EMI-resistant communication, and challenges in legacy system integration.

- Stakeholder Analysis: Strategic insights for industrial automation providers, system integrators, and component manufacturers.

The research employs both primary and secondary methodologies, including manufacturer surveys, expert interviews, and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial CAN to Fiber Converters Market?

-> Industrial CAN to Fiber Converters Market was valued at 348 million in 2024 and is projected to reach US$ 588 million by 2032, at a CAGR of 7.4% during the forecast period.

Which key companies operate in this market?

-> Major players include Moxa, IPC2U, CTC Union, Peak-System Technik, RLH Industries, Kvaser, Softing, and Renesas.

What are the key growth drivers?

-> Growth is driven by industrial automation expansion, need for EMI-resistant communication in harsh environments, and increasing adoption in automotive and aerospace applications.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe maintain significant market shares due to advanced industrial infrastructure.

What are the emerging trends?

-> Emerging trends include integration with IIoT systems, development of ruggedized converters for extreme environments, and adoption in smart manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...