MARKET INSIGHTS

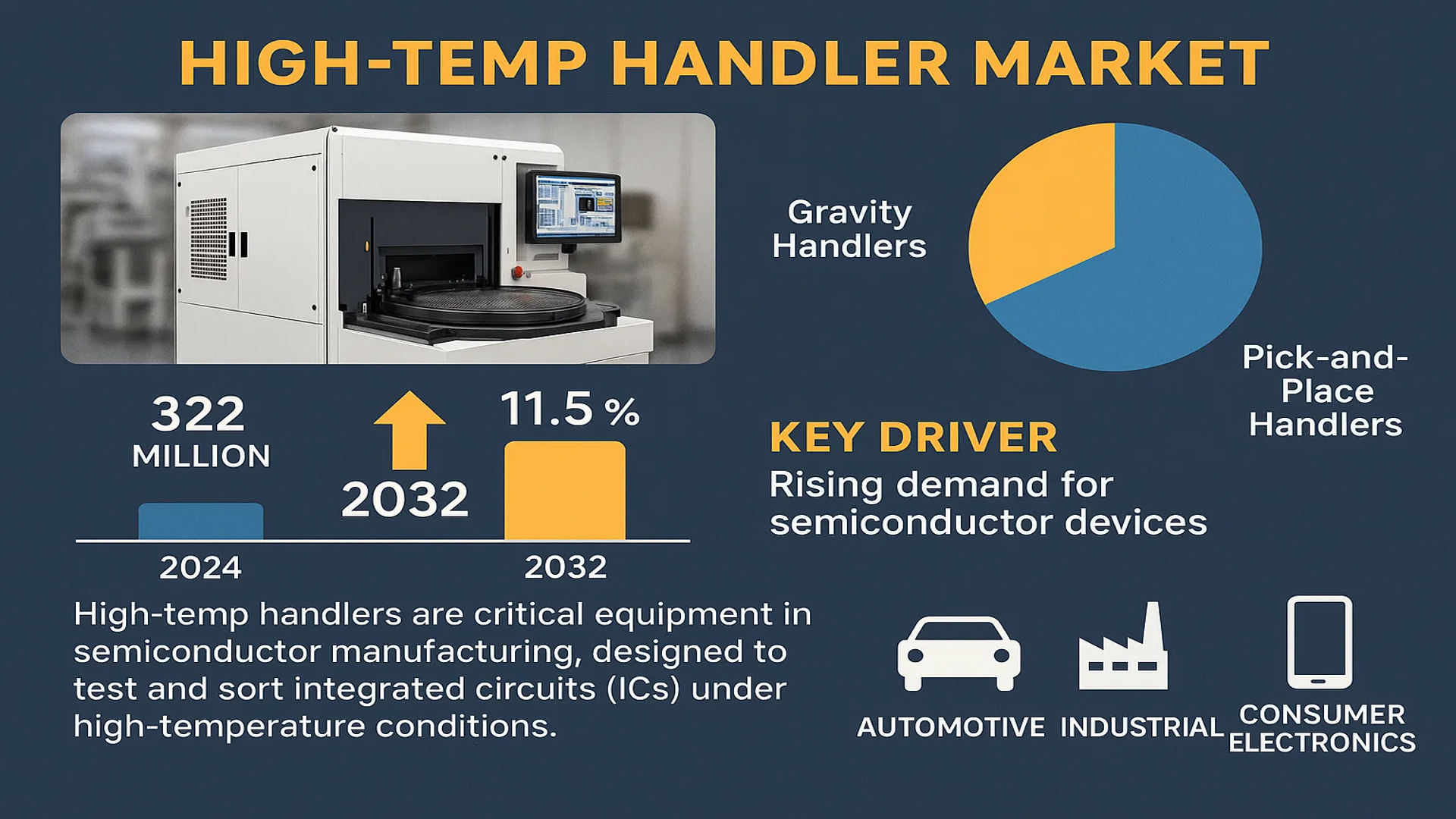

The global High-temp Handler market was valued at 322 million in 2024 and is projected to reach US$ 650 million by 2032, at a CAGR of 11.5% during the forecast period.

High-temp Handlers are critical equipment in semiconductor manufacturing, designed to test and sort integrated circuits (ICs) under high-temperature conditions. These machines ensure chip reliability and performance stability in extreme environments, playing a pivotal role in quality assurance for advanced electronics. The market primarily includes two types: Gravity Handlers and Pick-and-Place Handlers, which cater to different testing and sorting requirements.

Market growth is driven by rising demand for semiconductor devices, particularly in automotive, industrial, and consumer electronics sectors. The increasing complexity of ICs and stricter reliability standards further amplify the need for advanced High-temp Handlers. While North America remains a key market, Asia-Pacific, led by China and Japan, is witnessing accelerated adoption due to expanding semiconductor manufacturing capabilities. Key players like Advantest, Cohu, and Hangzhou Changchuan Technology dominate the competitive landscape, collectively holding a significant market share.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Semiconductor Industry to Boost Demand for High-Temp Handlers

The semiconductor industry is experiencing unprecedented growth due to increasing demand for consumer electronics, automotive electronics, and industrial automation. High-temp handlers are essential for testing semiconductor devices under extreme conditions, ensuring reliability in critical applications. The global semiconductor market is projected to grow at approximately 7% annually, creating substantial demand for testing equipment like high-temp handlers. Semiconductor manufacturers are increasingly adopting these systems to meet stringent quality requirements for advanced chips used in 5G, AI, and automotive applications. This trend is particularly evident in Asia, where semiconductor manufacturing is concentrated, with countries like China, Taiwan, and South Korea leading in production capacity expansion.

Growing Automotive Electronics Market to Drive Adoption

The automotive industry’s shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is creating significant demand for high-temperature semiconductor testing solutions. Automotive components must withstand temperature extremes from -40°C to 175°C, making high-temp handlers indispensable for quality assurance. The EV market is expected to grow at a CAGR of over 20% through 2030, with semiconductor content per vehicle increasing substantially. This growth is accelerating investments in test equipment capable of validating IC performance under harsh conditions. Manufacturers are particularly focused on power semiconductors and sensors that require rigorous high-temperature testing protocols.

➤ Major automotive semiconductor suppliers now mandate high-temp testing for all components, with some requiring extended thermal cycling tests of 1,000 hours or more at maximum operating temperatures.

Additionally, the proliferation of IoT devices and 5G infrastructure is creating new demand for reliable semiconductors tested under extreme conditions, further fueling market growth for high-temp handlers.

MARKET RESTRAINTS

High Capital Investment Requirements Limiting Market Penetration

The significant upfront cost of high-temp handler systems presents a major barrier to market adoption, particularly for small and medium-sized semiconductor test companies. Advanced high-temperature test solutions can cost between $500,000 to $2 million per unit, depending on configuration and testing capabilities. These systems require specialized thermal chambers, precision robotics, and sophisticated control systems that contribute to the high price point. While larger IDMs and OSATs can justify these investments, the cost structure makes it challenging for smaller players to adopt the technology, limiting overall market growth potential.

Additional Constraints

Technical Complexity in High-Temperature Testing

Maintaining testing accuracy at extreme temperatures presents significant engineering challenges. Thermal expansion of components can affect mechanical tolerances, while heat dissipation requirements complicate system design. These technical hurdles increase development costs and time-to-market for new high-temp handler models.

Limited Standards for High-Temp Testing

The lack of uniform industry standards for high-temperature semiconductor testing creates uncertainty for manufacturers. Without clear guidelines, companies must develop proprietary testing methodologies, increasing R&D expenditures and potentially delaying product certifications.

MARKET CHALLENGES

Skilled Workforce Shortage Impacting Market Development

The semiconductor test equipment industry faces a critical shortage of engineers and technicians qualified to operate and maintain high-temp handler systems. This skills gap has widened as semiconductor manufacturing has become more complex, with industry estimates suggesting a global deficit of over 100,000 skilled workers in semiconductor equipment fields. The specialized knowledge required for high-temperature testing, including thermal management and materials science expertise, makes personnel recruitment particularly challenging. Training programs often require 6-12 months to develop basic competencies, slowing the deployment of new systems and potentially affecting product quality.

Other Critical Challenges

Supply Chain Disruptions Affecting Component Availability

The global semiconductor supply chain crisis continues to impact test equipment manufacturers, with lead times for critical components like precision thermal sensors and specialty alloys extending to 12 months or more. This situation forces manufacturers to maintain higher inventory levels, increasing working capital requirements.

Maintaining Stability at Extreme Temperature Ranges

Achieving and maintaining precise temperature control (±0.5°C) above 200°C presents ongoing engineering challenges. Thermal drift, chamber uniformity, and material degradation at high temperatures require continuous R&D investments to maintain competitive performance.

MARKET OPPORTUNITIES

Emerging Compound Semiconductor Applications Creating New Demand

The development of wide-bandgap semiconductors using materials like silicon carbide (SiC) and gallium nitride (GaN) presents significant growth opportunities for high-temp handler manufacturers. These advanced semiconductors operate at much higher temperatures than traditional silicon, requiring specialized testing solutions. The SiC power device market alone is projected to grow at 30% CAGR through 2030, driven by EV and renewable energy applications. This growth is prompting test equipment vendors to develop innovative handling solutions capable of testing at temperatures exceeding 300°C while maintaining throughput and accuracy.

Additionally, the increasing complexity of 3D chip packaging and heterogeneous integration is creating demand for handlers that can test stacked dies under thermal stress conditions. Advanced packaging now accounts for nearly 50% of semiconductor test requirements, with this proportion expected to increase as chip architectures become more complex.

Automation and AI Integration Offering Competitive Advantages

The integration of artificial intelligence and advanced automation into high-temp handlers is creating new market opportunities. AI-powered thermal management systems can optimize test sequences, predict maintenance needs, and automatically compensate for thermal drift – improving throughput by up to 30%. Industry leaders are investing heavily in smart handler technologies that combine IoT connectivity with machine learning algorithms. These systems generate valuable data analytics that help semiconductor manufacturers improve yield rates and reduce test costs. As fabs embrace Industry 4.0 principles, demand for intelligent high-temp handling solutions is expected to accelerate significantly.

HIGH-TEMP HANDLER MARKET TRENDS

Semiconductor Industry Expansion Driving High-Temp Handler Demand

The global semiconductor industry’s rapid expansion, valued at over $600 billion, continues to fuel demand for high-temp handlers as these critical components ensure chip reliability in extreme conditions. With automotive electronics requiring stable performance at temperatures exceeding 125°C and 5G infrastructure components facing thermal challenges, test handlers capable of maintaining precision at elevated temperatures have become indispensable. The market has responded with advanced thermal control systems achieving ±0.5°C stability during testing cycles, substantially improving yield rates for power semiconductors and advanced processor packages.

Other Trends

Transition to Advanced Packaging Technologies

The shift towards 3D IC packaging and heterogeneous integration is reshaping handler requirements, with tier-one manufacturers now demanding systems capable of processing wafer-level packages at 200°C. This evolution stems from the growing adoption of chiplet designs in high-performance computing applications, where thermal cycling reliability directly impacts product lifetimes. Recent data indicates that nearly 40% of new handler installations now incorporate multi-zone temperature control specifically for advanced packaging applications, a significant increase from just 15% five years ago.

Automation and Smart Manufacturing Integration

The integration of Industry 4.0 technologies into high-temp handlers represents a paradigm shift in semiconductor testing workflows. Modern systems increasingly incorporate AI-driven predictive maintenance algorithms that reduce downtime by anticipating thermal component failures before they occur. Furthermore, the implementation of IoT-enabled monitoring has enabled real-time adjustment of handling parameters, achieving throughput improvements of 15-20% in high-volume manufacturing environments. This digital transformation aligns with the broader industry push towards autonomous fabs, where smart handlers serve as critical nodes in interconnected production ecosystems.

Material Science Breakthroughs

Recent advancements in thermal interface materials and ceramic-bearing systems are enabling handlers to achieve unprecedented temperature ranges while maintaining precision mechanical operation. Proprietary ceramic composites now allow continuous operation at 300°C with minimal thermal expansion variance, addressing one of the persistent challenges in high-temperature semiconductor testing. These material innovations, combined with electromagnetic shielding enhancements, are particularly crucial for the development of next-generation power devices operating in demanding automotive and industrial environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Accelerate R&D Investments to Capture High-Growth Semiconductor Testing Demand

The global high-temperature handler market features a mix of established semiconductor equipment providers and specialized testing solution developers. Advantest Corporation maintains a dominant position, accounting for over 20% of 2024 revenues, owing to its comprehensive portfolio of gravity and pick-and-place handlers capable of operating at extreme temperatures up to 200°C. The company’s strategic focus on AI-driven testing automation gives it a competitive edge in integrated device manufacturer (IDM) applications.

Meanwhile, Cohu, Inc. continues to strengthen its market position through targeted acquisitions, having recently integrated Delta Design’s thermal handling technologies. Their innovations in parallel testing solutions are particularly valued by outsourced semiconductor assembly and test (OSAT) providers in Asia-Pacific markets.

Emerging Chinese competitors like Hangzhou Changchuan Technology are rapidly gaining traction, supported by domestic semiconductor industry growth and government incentives. The company has achieved notable success with cost-effective alternatives to premium imported equipment, securing contracts with multiple domestic OSAT facilities.

Japanese precision engineering firms including Epson and Kanematsu differentiate through proprietary actuator technologies that enhance throughput in high-temperature environments. Their focus on reliability metrics appeals to automotive semiconductor manufacturers requiring extended operational lifetimes.

List of Key High-Temperature Handler Manufacturers

- Advantest Corporation (Japan)

- Cohu, Inc. (U.S.)

- HON PRECISION, INC (Korea)

- Hangzhou Changchuan Technology (China)

- JHT Design Co., Ltd (Taiwan)

- Epson Robots (Japan)

- SESSCO Technologies (Malaysia)

- Chroma ATE Inc (Taiwan)

- SYNAX Corporation (Japan)

- Microtec Handling Systems GmbH (Germany)

- Tesec Inc (Japan)

- Techwing Co., Ltd (Korea)

- Kanematsu (Japan)

- UENO SEIKI NAGANO (Japan)

- Shanghai Cascol (China)

The competitive dynamics are intensifying as established players strengthen their technological capabilities through partnerships. Microtec Handling Systems recently collaborated with a leading German automation firm to develop hybrid handling solutions, while Chroma ATE expanded its U.S. testing facilities to better serve North American clients. These strategic moves indicate the growing importance of geographical presence in securing long-term contracts as semiconductor testing requirements become more sophisticated.

Segment Analysis:

By Type

Gravity Handlers Segment Dominates Due to High Efficiency in Semiconductor Testing

The market is segmented based on type into:

- Gravity Handlers

- Subtypes: Vertical, Horizontal, and others

- Pick-and-Place Handlers

- Tower Handlers

- Turret Handlers

- Others

By Application

IDM Segment Leads Due to Increasing Demand for In-House Semiconductor Testing

The market is segmented based on application into:

- IDM (Integrated Device Manufacturers)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Foundries

- Research and Development Centers

By Temperature Range

High Temperature (Above 125°C) Segment Dominates for Automotive and Industrial Applications

The market is segmented based on temperature range into:

- Room Temperature (25°C to 85°C)

- High Temperature (Above 125°C)

- Extreme Temperature (Above 200°C)

By End User

Automotive Electronics Segment Leads Due to Stringent Quality Requirements

The market is segmented based on end user into:

- Automotive Electronics

- Consumer Electronics

- Industrial Electronics

- Aerospace & Defense

- Telecommunications

Regional Analysis: High-Temp Handler Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global High-temp Handler market, driven by China’s semiconductor manufacturing boom and Japan’s advanced semiconductor testing infrastructure. China alone accounts for over 40% of regional demand, fueled by massive investments in semiconductor self-sufficiency under initiatives like Made in China 2025. The country’s expanding OSAT (Outsourced Semiconductor Assembly and Test) industry creates strong demand for high-temperature testing equipment, with key players like Hangzhou Changchuan Technology and Shanghai Cascol increasing production capacity. Meanwhile, Japan maintains technological leadership through companies like Advantest, which holds significant market share in precision handlers. The region benefits from integrated supply chains and government-supported semiconductor cluster developments across Taiwan, South Korea, and Southeast Asia.

North America

North America’s High-temp Handler market is characterized by advanced semiconductor R&D and quality-focused production environments. The U.S. remains the largest market in the region, with strong demand from both IDMs (Integrated Device Manufacturers) and military/aerospace applications requiring rigorous high-temperature testing. Major players like Cohu and Chroma ATE Inc provide sophisticated handling solutions for next-generation chip testing, particularly for AI and automotive semiconductors. The CHIPS Act’s $52 billion funding commitment is expected to boost domestic semiconductor manufacturing, subsequently driving demand for testing equipment. However, higher equipment costs and preference for outsourcing testing to Asia pose challenges for market expansion in this region.

Europe

Europe’s High-temp Handler market benefits from the region’s strong automotive semiconductor sector and growing focus on power electronics for renewable energy applications. Germany leads regional demand, with companies like Microtec Handling Systems GmbH supplying precision handlers to major automotive chip manufacturers. The EU’s proposed Chips Act aims to double Europe’s share of global semiconductor production to 20% by 2030, creating opportunities for testing equipment providers. However, the market faces challenges from the region’s relatively small OSAT ecosystem and the high cost of locally manufactured equipment compared to Asian alternatives. Sustainability-focused innovations in handler design and energy efficiency are becoming key differentiators in this market.

Middle East & Africa

This emerging market shows gradual growth potential, primarily driven by increasing electronics manufacturing in countries like Israel and Turkey. While the current market size remains small compared to other regions, strategic investments in technology parks and semiconductor packaging facilities are creating niche opportunities. The lack of local semiconductor fabrication limits immediate demand for high-end testing equipment, but the growing electronics assembly sector generates need for basic IC testing capabilities. Long-term growth will depend on successful implementation of technology transfer programs and foreign investment in local semiconductor ecosystems.

South America

South America represents the smallest High-temp Handler market currently, with limited semiconductor manufacturing infrastructure. Brazil shows some demand from its automotive electronics sector, while Argentina has emerging microelectronics research capabilities. Economic volatility and reliance on imported semiconductor components continue to restrain market growth. However, the increasing trend toward regional electronics production for appliances and industrial equipment may stimulate gradual demand for basic IC testing solutions in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Global High-temp Handler Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the semiconductor testing equipment industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global High-temp Handler market was valued at USD 322 million in 2024 and is projected to reach USD 650 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Gravity Handlers, Pick-and-Place Handlers), application (IDM, OSAT), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with major contributions from China, Japan, and South Korea.

- Competitive Landscape: Profiles of leading market participants including Advantest, Cohu, Epson, Chroma ATE Inc, and Hangzhou Changchuan Technology, covering their product offerings, market share (top five players held approximately 45% revenue share in 2024), and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in semiconductor testing, automation integration, and precision handling solutions for high-temperature environments.

- Market Drivers & Restraints: Evaluation of factors including semiconductor industry growth, demand for reliable IC testing, and challenges like high equipment costs and technical complexity.

- Stakeholder Analysis: Insights for semiconductor manufacturers, testing service providers, equipment suppliers, and investors regarding market opportunities and strategic positioning.

Primary and secondary research methods were employed, including interviews with industry experts, analysis of financial reports from key players, and validation through multiple data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-temp Handler Market?

-> High-temp Handler market was valued at 322 million in 2024 and is projected to reach US$ 650 million by 2032, at a CAGR of 11.5% during the forecast period.

Which key companies operate in Global High-temp Handler Market?

-> Key players include Advantest, Cohu, HON PRECISION, Hangzhou Changchuan Technology, Epson, Chroma ATE Inc, and Microtec Handling Systems GmbH, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor demand, increasing complexity of IC testing requirements, and growth in automotive and industrial electronics sectors.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by semiconductor manufacturing hubs in China, Taiwan, and South Korea, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive maintenance, development of ultra-high temperature handlers, and increasing automation in testing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...