MARKET INSIGHTS

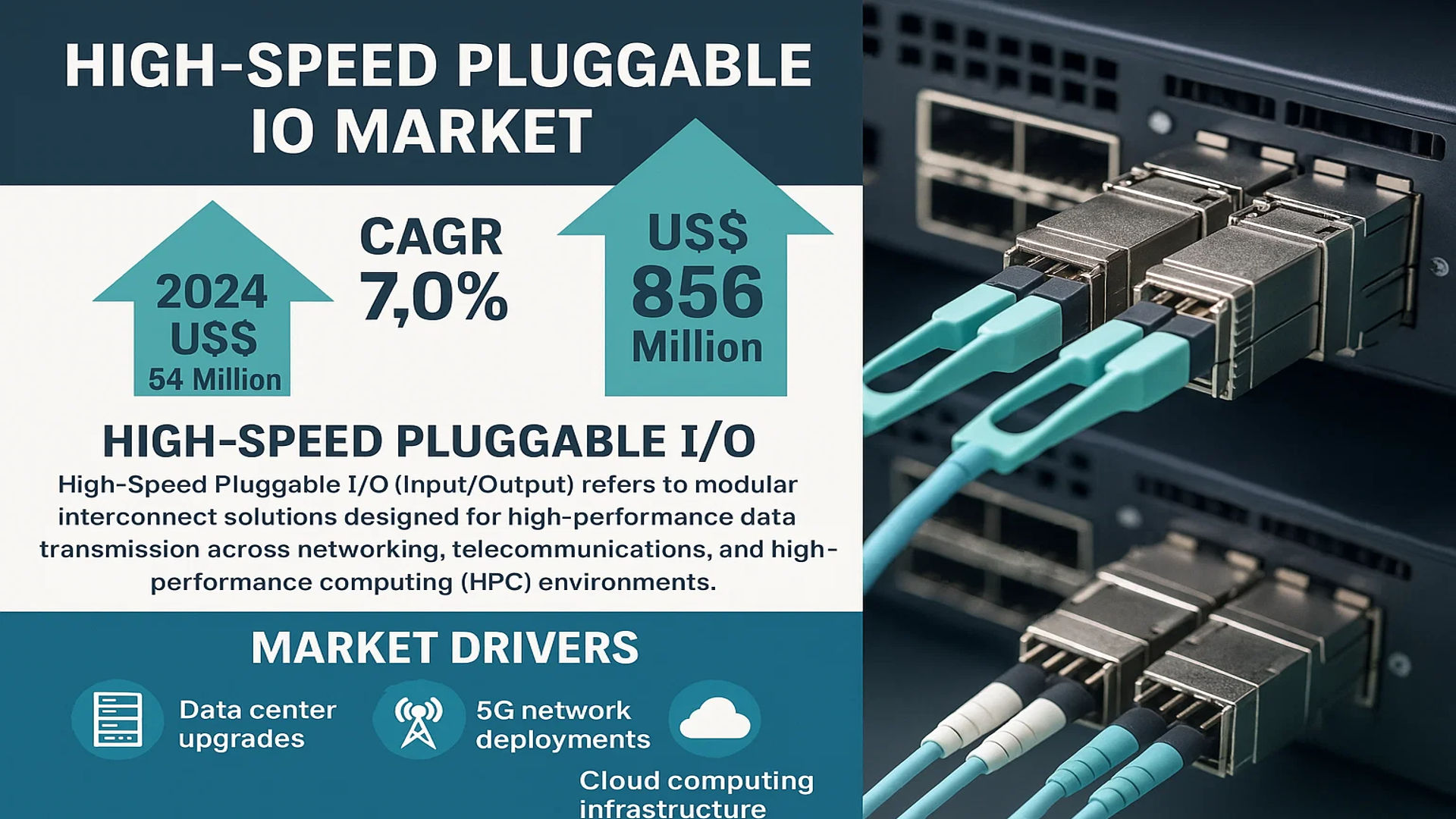

The global High-Speed Pluggable IO Market was valued at 514 million in 2024 and is projected to reach US$ 856 million by 2032, at a CAGR of 7.0% during the forecast period.

High-Speed Pluggable I/O (Input/Output) refers to modular interconnect solutions designed for high-performance data transmission across networking, telecommunications, and high-performance computing (HPC) environments. These hot-swappable interfaces facilitate rapid communication between critical infrastructure components including servers, switches, routers, and optical transceivers, supporting bandwidth-intensive applications.

The market expansion is driven by escalating demand for data center upgrades, 5G network deployments, and cloud computing infrastructure. While copper-based solutions dominate cost-sensitive applications, optical-based variants are gaining traction for long-distance, high-bandwidth requirements. Key players like Molex, TE Connectivity, and Amphenol collectively hold significant market share, leveraging their expertise in high-speed connectivity solutions. Recent technological advancements in 400G and 800G transceivers are further accelerating market adoption across communication and industrial sectors.

MARKET DYNAMICS

MARKET DRIVERS

Explosive Growth in Data Center Infrastructure Fuels Demand for High-Speed Pluggable I/O Solutions

The global data center infrastructure market is undergoing unprecedented expansion, with hyperscale facilities driving demand for high-bandwidth connectivity solutions. This growth is directly increasing adoption of high-speed pluggable I/O interfaces, as data centers require flexible, scalable interconnect solutions to handle exponential data traffic growth. The shift towards higher port densities and energy-efficient architectures favors modular pluggable designs over fixed configuration alternatives. Cloud service providers and colocation operators are rapidly upgrading facilities to support next-generation workloads, with deployment of 400G and emerging 800G Ethernet standards catalyzing demand for advanced pluggable I/O components.

5G Network Deployments Accelerate Need for High-Speed Interconnects

Global 5G network rollouts are creating substantial demand for high-performance pluggable I/O solutions across telecom infrastructure. The transition from 4G to 5G requires up to 100x greater network capacity in mobile fronthaul and backhaul segments, necessitating dense, high-speed fiber connectivity. Telecom equipment manufacturers are increasingly adopting pluggable optical modules and copper interconnects that offer both performance and serviceability advantages. The flexibility of pluggable architectures enables carriers to deploy and upgrade networks more efficiently while reducing operating expenses through hot-swappable maintenance capabilities.

➤ Network operators are projected to deploy over 7 million 5G base stations globally by 2025, each requiring multiple high-speed interconnects for signal transmission and switching.

Furthermore, emerging technologies like network function virtualization (NFV) and software-defined networking (SDN) are driving architectural shifts that benefit modular I/O solutions. These transformations enable dynamic resource allocation and require infrastructure that can adapt to changing traffic patterns and service requirements.

MARKET RESTRAINTS

Thermal Management Challenges Restrict Performance Scaling

As pluggable I/O interfaces push towards higher data rates exceeding 112Gbps per lane, thermal dissipation becomes a critical constraint. The compact form factors favored by data center operators create significant thermal challenges that limit performance scaling. Power consumption per port increases exponentially with data rates, creating hotspots in densely populated equipment racks. These thermal constraints force difficult tradeoffs between port density, performance, and reliability that inhibit market expansion in high-performance applications.

Standardization Fragmentation Creates Implementation Challenges

The high-speed pluggable I/O market faces significant challenges from competing standards and proprietary implementations. While multi-source agreements (MSAs) exist for common form factors, subtle implementation differences between vendors can create interoperability issues. This fragmentation increases development costs for OEMs who must validate compatibility across multiple supplier implementations. The lack of unified ecosystem support for emerging technologies like co-packaged optics creates uncertainty that may delay adoption timelines for next-generation solutions.

MARKET CHALLENGES

Power Efficiency Demands Increase Design Complexity

Energy consumption has become a critical design factor as data centers target ambitious sustainability goals. Pluggable I/O solutions must deliver better performance-per-watt metrics while maintaining signal integrity at higher data rates. This requires advanced materials, innovative circuit designs, and sophisticated power management techniques that increase development costs and time-to-market. The challenge is particularly acute for optical modules, where electro-optical conversion efficiency significantly impacts total cost of ownership.

Other Challenges

Supply Chain Vulnerabilities

The specialized components required for high-speed pluggable I/O, including high-performance ICs and optical components, remain subject to extended lead times and allocation pressures. These constraints limit production scalability and create inventory management challenges for manufacturers.

Signal Integrity at Higher Frequencies

Maintaining signal integrity becomes increasingly difficult as data rates exceed 100Gbps per lane. Skew management, crosstalk reduction, and impedance matching require precise engineering that drives up product costs and development cycles.

MARKET OPPORTUNITIES

Artificial Intelligence Workloads Drive Next-Generation Interconnect Requirements

The explosive growth of AI and machine learning applications is creating new opportunities for high-speed pluggable I/O solutions. AI clusters require ultra-low latency, high-bandwidth interconnects between accelerators, switches, and storage systems. This demand is driving innovation in standards like 800G and 1.6T Ethernet, with pluggable interfaces positioned to enable flexible, scalable AI infrastructure deployments. Hyperscale operators are actively collaborating with suppliers to develop optimized solutions that meet the unique requirements of distributed training workloads and inference processing.

Edge Computing Expansion Creates New Deployment Scenarios

The proliferation of edge computing infrastructure presents significant growth potential for ruggedized pluggable I/O solutions. Unlike controlled data center environments, edge locations often require hardened components that can withstand wider temperature ranges and physical stresses. Manufacturers developing environmentally hardened pluggable interfaces can capture share in emerging 5G edge, industrial IoT, and smart city applications. The ability to support field upgrades and maintenance without specialized tools provides compelling advantages in distributed edge deployments.

HIGH-SPEED PLUGGABLE IO MARKET TRENDS

Rising Demand for High-Bandwidth Data Transmission to Drive Market Growth

The exponential growth in data traffic, driven by cloud computing, 5G networks, and hyperscale data centers, has significantly increased the demand for high-speed pluggable I/O solutions. With global internet traffic projected to reach over 4.8 zettabytes annually by 2030, the need for reliable and scalable interconnect solutions has never been greater. Market leaders are innovating in optical-based pluggable I/O to support ultra-high-speed connections exceeding 800G and 1.6T, catering to next-generation networking infrastructures. Meanwhile, advancements in copper-based solutions continue to offer cost-effective alternatives for short-reach applications.

Other Trends

Adoption of Optical-Based Pluggable I/O for AI and HPC

The proliferation of artificial intelligence (AI) workloads and high-performance computing (HPC) has accelerated the shift toward optical-based pluggable I/O solutions, which provide lower latency and higher bandwidth. AI server clusters increasingly rely on 400G and 800G transceivers for seamless data transfer between GPUs and accelerators, minimizing bottlenecks. Furthermore, the growing deployment of AI in edge computing and data centers is expected to sustain long-term demand for high-speed pluggable interconnects, reinforcing double-digit annual growth in this segment.

Competitive Landscape and Technological Advancements

The high-speed pluggable I/O market remains highly competitive, with key players such as Molex, TE Connectivity, and Amphenol dominating nearly 60% of global revenues. Strategic collaborations between manufacturers and network equipment providers have led to innovative form factors such as QSFP-DD and OSFP, optimizing power efficiency and port density. Additionally, ongoing R&D efforts focus on thermal management and signal integrity to support next-generation speeds while maintaining backward compatibility. Recent product launches demonstrate a clear trend toward modular designs that simplify upgrades without requiring infrastructure overhauls.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation in High-Speed Pluggable IO Solutions

The global High-Speed Pluggable IO market exhibits a diverse competitive landscape, characterized by established manufacturers and emerging technology providers racing to meet the exponential demand for faster data transmission solutions. Molex, TE Connectivity, and Amphenol currently dominate the market, collectively holding a substantial share of the revenue in 2024. Their dominance stems from decades of expertise in connectivity solutions and strong relationships with data center operators, telecom providers, and HPC manufacturers.

While these giants maintain their lead through continuous R&D investments, companies like Samtec and Luxshare Precision are gaining traction by offering specialized high-bandwidth solutions at competitive price points. This dual dynamic of technological leadership and cost optimization creates an intense race for market share, with each player investing heavily in both copper-based and optical-based pluggable I/O innovations.

Meanwhile, Foxconn Interconnect Technology (FIT) has emerged as a particularly agile competitor, leveraging its massive manufacturing scale and vertical integration advantages to capture growing demand in Asia-Pacific markets. Their ability to quickly scale production while maintaining quality standards presents a significant challenge to traditional Western manufacturers.

List of Key High-Speed Pluggable IO Companies Profiled

- Molex (U.S.)

- TE Connectivity (Switzerland)

- Amphenol (U.S.)

- Volex (U.K.)

- Samtec (U.S.)

- IPtronics (Denmark)

- Weidmüller (Germany)

- Luxshare Precision (China)

- Foxconn Interconnect Technology (FIT) (Taiwan)

- JAE (Japan)

Segment Analysis:

By Type

Optical-Based Pluggable I/O Segment Leads Due to Higher Data Transmission Efficiency

The market is segmented based on type into:

- Copper-Based Pluggable I/O

- Subtypes: QSFP, SFP, and others

- Optical-Based Pluggable I/O

- Subtypes: CFP, CFP2, CFP4, and others

By Application

Communications Sector Dominates Market Share Owing to Rising Bandwidth Demands

The market is segmented based on application into:

- Communications

- Financial Services

- Industrial Automation

- Healthcare IT

- Others

By Speed

100G+ Segment Experiences Rapid Growth for AI/ML Workloads

The market is segmented based on speed capabilities into:

- Below 10G

- 10G-40G

- 40G-100G

- Above 100G

By Form Factor

QSFP Modules Maintain Dominance for Datacenter Applications

The market is segmented based on form factors into:

- SFP/SFP+

- QSFP/QSFP+

- CFP/CFP2/CFP4

- Others

Regional Analysis: High-Speed Pluggable IO Market

Asia-Pacific

The Asia-Pacific region dominates the global High-Speed Pluggable IO market, accounting for over 40% of the total revenue share in 2024. This leadership position stems from massive investments in 5G infrastructure, hyperscale data centers, and government-supported digital transformation initiatives across China, Japan, and South Korea. China alone is projected to deploy over 2.3 million 5G base stations by 2025, creating substantial demand for high-bandwidth optical-based pluggable I/O solutions. While cost-competitive copper-based solutions remain popular for short-range applications, telecom operators and cloud service providers are increasingly adopting energy-efficient optical modules to handle exponential data traffic growth. The presence of manufacturing hubs and local players like Luxshare Precision further strengthens regional supply chains.

North America

North America represents the second-largest market, driven by cutting-edge innovations from Silicon Valley tech giants and substantial R&D investments in next-gen networking technologies. The U.S. accounts for approximately 75% of the regional demand, with hyperscalers like AWS, Microsoft, and Google driving adoption of 400G and 800G pluggable transceivers for data center interconnects. While the market remains concentrated on high-performance optical solutions, copper-based variants continue to serve enterprise networking needs. Recent developments include the adoption of pluggable coherent optics for metro and long-haul applications by major telecom operators. Regulatory emphasis on energy efficiency in data centers also accelerates innovation in low-power designs.

Europe

European markets demonstrate steady growth, particularly in Germany, the UK, and France, where telecom infrastructure modernization aligns with EU digital sovereignty objectives. The region shows strong preference for standardized, interoperable solutions that comply with stringent environmental regulations. Industrial applications of High-Speed Pluggable IO are growing fastest, with Industry 4.0 implementations demanding reliable real-time communication between manufacturing equipment. However, market expansion faces headwinds from prolonged equipment certification processes and cautious spending by traditional telecom operators. European players like Weidmüller focus on ruggedized industrial connectivity solutions that withstand harsh factory environments while meeting sustainability targets.

South America

The South American market remains in early growth stages, with Brazil representing nearly 60% of regional demand. Limited cloud infrastructure and reliance on legacy networks constrain market potential, though expanding submarine cable connections to North America and Europe are creating opportunities for high-speed interconnect solutions. Economic volatility continues to impact capital expenditure decisions, leading operators to prioritize cost-effective copper solutions over cutting-edge optical technologies. Nonetheless, strategic partnerships between global vendors and local distributors are gradually increasing market penetration, particularly for financial sector applications requiring low-latency trading connections.

Middle East & Africa

The MEA region shows divergent growth patterns – while Gulf Cooperation Council (GCC) countries invest heavily in smart city projects and data center infrastructure, sub-Saharan Africa relies primarily on mobile network expansions. UAE and Saudi Arabia lead adoption of high-speed pluggable solutions, driven by artificial intelligence deployments and sovereign cloud initiatives. However, the broader regional market faces constraints from limited technical expertise and infrastructure gaps, with many nations still dependent on imported equipment. Long-term growth potential exists as undersea cable projects improve connectivity and governments prioritize digital economy roadmaps, but progress will likely remain uneven across the region.

Report Scope

This market research report provides a comprehensive analysis of the global High-Speed Pluggable IO market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 514 million in 2024 and is projected to reach USD 856 million by 2032 at a CAGR of 7.0%.

- Segmentation Analysis: Detailed breakdown by product type (Copper-Based Pluggable I/O, Optical-Based Pluggable I/O) and application (Communications, Financial, Industrial, Healthcare, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including Molex, TE Connectivity, Amphenol, Volex, Samtec and others, covering their product portfolios, market shares, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies in high-speed data transmission, evolving interface standards, and integration with next-generation networking solutions.

- Market Drivers & Restraints: Evaluation of factors including growing data center demands, 5G deployment, and HPC requirements versus supply chain challenges and technical constraints.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, network equipment providers, and investors in the high-speed connectivity ecosystem.

The report employs both primary and secondary research methodologies, incorporating expert interviews, manufacturer surveys, and verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-Speed Pluggable IO Market?

-> High-Speed Pluggable IO Market was valued at 514 million in 2024 and is projected to reach US$ 856 million by 2032, at a CAGR of 7.0% during the forecast period.

Which key companies operate in Global High-Speed Pluggable IO Market?

-> Key players include Molex, TE Connectivity, Amphenol, Volex, Samtec, IPtronics, Weidmüller, Luxshare Precision, Foxconn Interconnect Technology (FIT), and JAE.

What are the key growth drivers?

-> Primary growth drivers include rising data center demands, 5G network expansion, increasing adoption of cloud computing, and growing requirements for high-performance computing applications.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include development of higher-speed interfaces (400G+), integration of optical connectivity solutions, and increasing adoption in AI/ML infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...