MARKET INSIGHTS

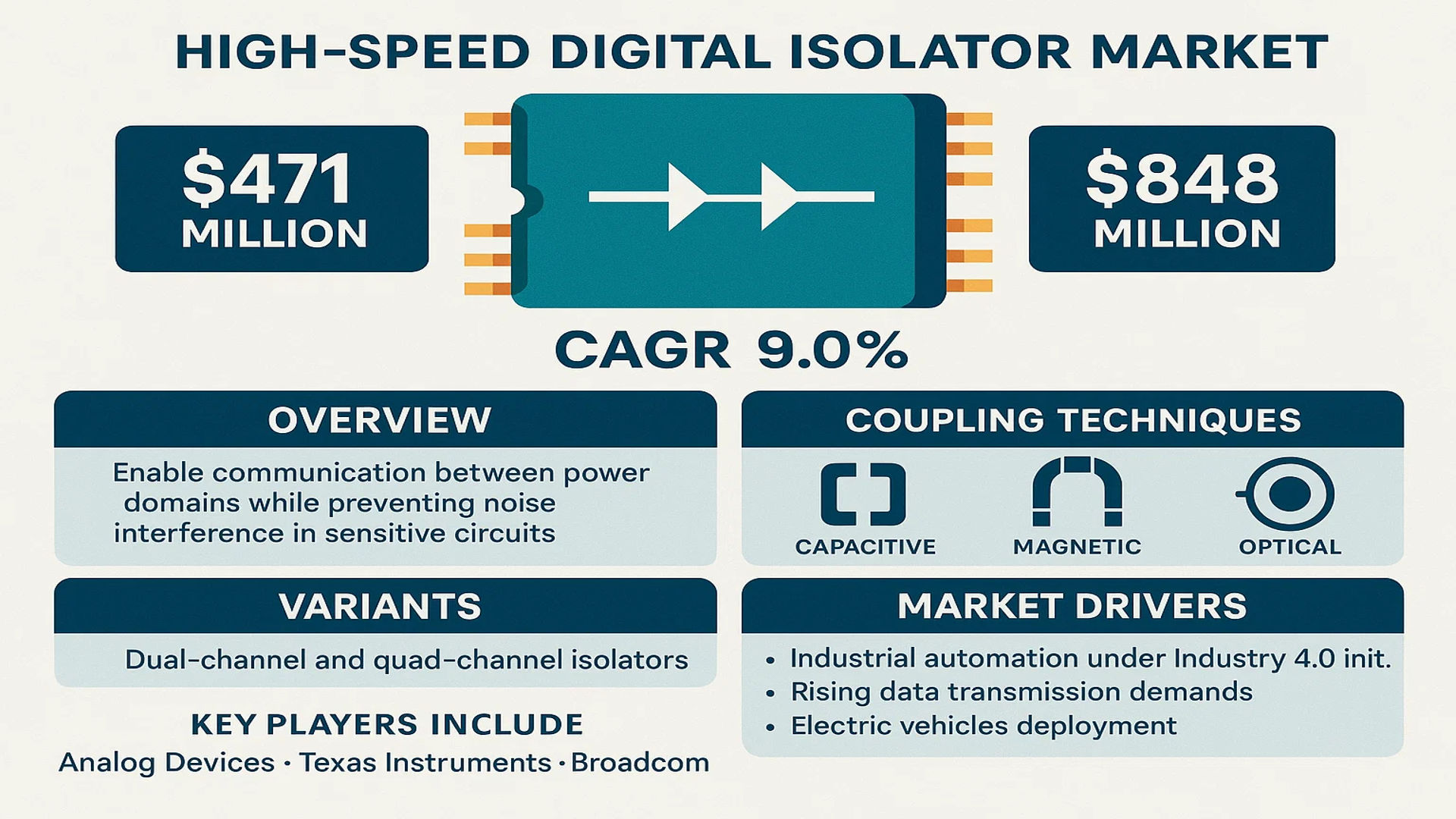

The global High-Speed Digital Isolator Market was valued at 471 million in 2024 and is projected to reach US$ 848 million by 2032, at a CAGR of 9.0% during the forecast period.

High-speed digital isolators are critical components designed to enable communication between two different power domains while preventing noise interference in sensitive circuits. These devices use capacitive, magnetic, or optical coupling techniques to transmit digital signals across isolation barriers, ensuring signal integrity and protecting systems from voltage spikes or ground loops. Common variants include dual-channel and quad-channel isolators, which cater to diverse industrial and communication applications.

The market growth is driven by increasing adoption in industrial automation under Industry 4.0 initiatives, where robust signal isolation is essential for equipment safety and reliability. Furthermore, rising data transmission demands in 5G infrastructure, data centers, and electric vehicles are accelerating deployment. Key players like Analog Devices, Texas Instruments, and Broadcom continue to innovate with higher bandwidth solutions, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Industry 4.0 Adoption Fuelling Demand for High-Speed Digital Isolators

The rapid adoption of Industry 4.0 practices across manufacturing sectors is significantly boosting demand for high-speed digital isolators. As factories implement smart automation systems, these components become critical for maintaining signal integrity between high-voltage equipment and low-voltage control systems. The global industrial automation market is projected to grow at nearly 9% CAGR through 2030, with digital isolators playing a vital role in enabling safe, noise-free communication between disparate system components. Recent technological advancements have increased data transmission speeds up to 150 Mbps in modern digital isolators while maintaining robust isolation barriers exceeding 5 kV RMS.

5G Network Expansion Driving Telecom Infrastructure Requirements

The global rollout of 5G networks is creating substantial demand for high-speed digital isolators in telecommunications infrastructure. These components are essential for protecting sensitive circuitry in base stations, routers, and switches from electrical noise and surges while enabling high-frequency data transmission. With over 2 billion 5G subscriptions expected by 2025, network operators require robust isolation solutions that can withstand harsh environmental conditions while maintaining signal integrity at multi-gigabit speeds. Major telecom equipment manufacturers are incorporating next-generation digital isolators capable of operating at frequencies above 1 GHz to meet these demanding requirements.

Additionally, the transition to renewable energy sources is accelerating demand in power electronics applications:

➤ High-speed digital isolators with reinforced isolation ratings are becoming critical components in solar inverters and EV charging stations, where they enable safe monitoring and control of high-voltage systems while preventing ground loop interference.

This expanding application scope across multiple industries is driving product innovation and market growth, with leading manufacturers introducing new isolator families featuring reduced power consumption and enhanced electromagnetic compatibility.

MARKET RESTRAINTS

Technical Limitations in High-Frequency Applications Constrain Market Expansion

While high-speed digital isolators demonstrate excellent performance in most industrial applications, they face significant technical challenges in ultra-high frequency environments. The inherent limitations of isolation barrier technologies create signal integrity issues at frequencies above 2.5 GHz, restricting their use in cutting-edge communications equipment. These challenges become particularly apparent in emerging 6G research applications, where traditional digital isolator designs cannot maintain sufficient noise immunity at terahertz frequencies.

Supply Chain Disruptions Impacting Production Capacities

The semiconductor supply chain bottlenecks affecting the broader electronics industry have particularly impacted digital isolator manufacturers. Specialty materials used in isolation barriers, including polyimide and silicon dioxide, have experienced periodic shortages that constrain production volumes. These supply constraints come at a critical time when demand is surging across automotive, industrial, and telecommunications sectors. Many manufacturers face lead times exceeding 20 weeks for certain high-performance digital isolator variants, forcing system designers to explore alternative solutions or delay product launches.

Additional market constraints include:

Regulatory Compliance Costs

Meeting diverse international safety standards for reinforced isolation requires substantial R&D investment and testing expenditures. The certification process for medical-grade digital isolators can exceed 18 months, significantly delaying time-to-market for new products.

Thermal Management Challenges

High-speed operation in compact form factors generates substantial heat that must be effectively dissipated while maintaining isolation properties. This thermal-electrical trade-off presents ongoing design challenges for next-generation applications.

MARKET OPPORTUNITIES

Emerging Automotive Electronics Applications Present Growth Potential

The automotive industry’s rapid electrification is creating significant opportunities for high-speed digital isolators. Modern electric vehicles contain over 100 isolation barriers in battery management systems, onboard chargers, and motor drives. With global EV production expected to surpass 30 million units annually by 2030, this represents one of the fastest-growing application segments. Digital isolators offer superior reliability compared to optocouplers in harsh automotive environments while providing the necessary data rates for real-time system monitoring.

Medical Equipment Modernization Driving Demand

The healthcare sector’s increasing adoption of digital imaging systems and robotic surgical equipment requires high-performance isolation solutions that meet stringent safety standards. Medical-grade digital isolators must provide reinforced isolation while handling high-speed data streams from sensors and imaging detectors. As hospitals worldwide upgrade their diagnostic and treatment equipment, the demand for these specialized components is expected to grow at nearly 12% annually through 2030. Recent product innovations include isolators with integrated power supplies specifically designed for portable medical devices.

The expanding renewable energy sector also presents substantial opportunities:

➤ Next-generation digital isolators with enhanced reliability ratings are becoming essential in utility-scale solar and wind installations, where they facilitate safe monitoring of high-voltage power conversion systems while withstanding extreme environmental conditions for decades.

This diversified growth across multiple industries is encouraging manufacturers to expand production capacities and develop application-specific digital isolator solutions.

MARKET CHALLENGES

Intense Price Competition Squeezing Manufacturer Margins

The digital isolator market faces growing pricing pressures as more semiconductor companies enter this segment. While premium-priced high-speed models maintain healthy margins, standard-speed variants have seen average selling prices decline nearly 8% annually. This price erosion is particularly challenging for smaller manufacturers who lack the economies of scale enjoyed by industry leaders. The situation is further complicated by the increasing availability of lower-cost alternatives from regional suppliers in Asia, forcing global players to optimize their manufacturing processes and product portfolios to remain competitive.

Other Challenges

Design Complexity

Developing digital isolators that meet evolving application requirements for speed, isolation voltage, and power efficiency requires increasingly sophisticated design expertise. Balancing these competing demands while maintaining high reliability standards presents ongoing engineering challenges, especially for emerging applications like aerospace and defense systems.

Technology Disruption Risks

Emerging isolation technologies based on novel materials and integration approaches could potentially disrupt traditional digital isolator markets. While most alternatives currently lag in performance and reliability, continued advances in areas like integrated passive devices and advanced packaging could reshape competitive dynamics over the long term.

HIGH-SPEED DIGITAL ISOLATOR MARKET TRENDS

Industrial Automation and Industry 4.0 Driving Market Expansion

The global high-speed digital isolator market is experiencing significant growth due to the rapid adoption of Industry 4.0 and industrial automation technologies. Digital isolators play a critical role in ensuring reliable signal transmission while protecting sensitive industrial control systems from electrical noise and voltage spikes. With an increasing number of manufacturing facilities implementing smart factory solutions, the demand for high-speed isolators capable of handling data rates exceeding 150 Mbps has grown substantially. The industrial control segment accounted for over 40% of total market revenue in recent years, reflecting this sector’s dominance.

Other Trends

5G Network Expansion

The global rollout of 5G infrastructure has created substantial demand for high-performance digital isolators in telecommunications equipment. These components are essential for maintaining signal integrity in base stations, routers, and backhaul equipment operating at millimeter-wave frequencies. As telecom providers continue expanding their 5G networks – with projected deployments increasing by approximately 25% annually through 2030 – the need for isolators capable of supporting multi-gigabit data rates continues to grow.

Advancements in Isolator Technology

Recent innovations in semiconductor materials and packaging technologies have led to significant improvements in digital isolator performance. Manufacturers are increasingly adopting silicon carbide (SiC) and gallium nitride (GaN) based designs that offer superior noise immunity and higher operating temperatures compared to traditional solutions. The development of multi-channel isolators with integrated power delivery has emerged as a key trend, particularly for space-constrained applications in motor drives and power conversion systems. These technological improvements have helped drive the market’s projected CAGR of 9.0% through 2032.

Automotive Electrification

The shift toward electric vehicles (EVs) and autonomous driving systems has created new opportunities for high-speed digital isolators in automotive applications. These components are critical for battery management systems, onboard chargers, and vehicle-to-grid communication interfaces. With global EV sales expected to surpass 30 million units annually by 2030, automotive applications are becoming an increasingly important growth segment for isolator manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation in High-Speed Digital Isolation Technologies

The global high-speed digital isolator market exhibits a competitive and dynamic landscape, dominated by established semiconductor manufacturers while witnessing increasing participation from regional players. Analog Devices and Texas Instruments collectively hold over 35% market share as of 2024, leveraging their extensive product portfolios and strong distribution networks in industrial and automotive sectors. These companies continue to invest heavily in R&D to develop isolation solutions supporting data rates beyond 150 Mbps while maintaining stringent safety standards.

Skyworks Solutions has emerged as a key disruptor with its proprietary capacitive isolation technology, particularly gaining traction in 5G infrastructure applications. Meanwhile, Broadcom maintains significant presence in data center applications through its optocoupler alternatives offering superior common-mode transient immunity. The market has seen growing competition from Asian manufacturers such as Renesas Electronics and ROHM Semiconductor, who are aggressively expanding their high-speed isolator lines to cater to regional demand in industrial automation and new energy applications.

Strategic acquisitions have shaped the competitive dynamics, exemplified by Infineon’s acquisition of Cypress Semiconductor, strengthening its position in automotive digital isolation. Chinese players like NOVOSENSE and Shanghai Chipanalog Microelectronics are capturing domestic market share through cost-competitive solutions, though they face challenges in meeting international certification standards for high-reliability applications.

The competitive intensity is expected to increase as companies develop isolated gate drivers for wide-bandgap semiconductors (SiC/GaN) and ultra-high-speed interfaces for industrial IoT. Product miniaturization, lower power consumption, and enhanced EMC performance remain key differentiation factors as the market progresses toward the projected $848 million valuation by 2032.

List of Key High-Speed Digital Isolator Companies Profiled

- Analog Devices, Inc. (U.S.)

- Skyworks Solutions, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Broadcom Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Vicor Corporation (U.S.)

- NVE Corporation (U.S.)

- ROHM Semiconductor (Japan)

- Mornsun Power (China)

- Renesas Electronics Corporation (Japan)

- Shanghai Chipanalog Microelectronics (China)

- Beijing Zhongke Gree Micro (China)

- 2Pai Semiconductor (China)

- NOVOSENSE (China)

- Hoperf (China)

Segment Analysis:

By Type

Dual-Channel Digital Isolators Lead the Market Due to Their Versatility in Industrial and Telecom Applications

The market is segmented based on type into:

- Dual-Channel Digital Isolator

- Quad-Channel Digital Isolator

By Application

Industrial Control Segment Dominates with Growing Automation and Industry 4.0 Adoption

The market is segmented based on application into:

- Industrial Control

- New Energy

- Digital Power

- Other

By Data Rate

High-Speed Isolators (>1Gbps) Gain Traction in 5G and Data Center Infrastructure

The market is segmented based on data rate into:

- <100Mbps

- 100Mbps-1Gbps

- >1Gbps

By Isolation Technology

Capacitive Coupling Technology Prevalent Due to Its High-Speed Performance

The market is segmented based on isolation technology into:

- Optocoupler

- Magnetic Coupling

- Capacitive Coupling

Regional Analysis: High-Speed Digital Isolator Market

Asia-Pacific

The Asia-Pacific region dominates the high-speed digital isolator market, accounting for over 40% of global demand in 2024. China and Japan are the primary growth engines, driven by rapid industrialization, 5G deployment, and increasing investments in semiconductor fabrication. The region benefits from strong manufacturing ecosystems and government initiatives like China’s “Made in China 2025” policy, which prioritizes advanced electronics. However, intense price competition among local manufacturers (e.g., Shanghai Chipanalog Microelectronics) and global players creates margin pressures. Taiwan and South Korea are also key contributors due to their thriving data center and telecom infrastructure markets.

North America

North America represents the second-largest market, fueled by stringent safety standards and rapid adoption of Industry 4.0 technologies. The U.S. holds an 85% share of the regional market, with major demand from automotive electrification (EVs account for 30% of isolator applications) and data centers (supporting 40% of global cloud infrastructure). Silicon Valley-based innovators like Analog Devices and Texas Instruments lead in developing ultra-high-speed isolators (up to 150 Mbps) for aerospace and medical applications. Cross-border collaborations with Canadian and Mexican suppliers are strengthening the regional supply chain against semiconductor shortages.

Europe

Europe’s market growth is anchored by Germany’s industrial automation sector and Scandinavia’s renewable energy projects. The region shows 6.2% YoY growth in isolator demand, primarily for wind turbines and smart grid applications. EU safety directives (EN 61010-1) mandate isolator usage in critical equipment, creating steady demand. However, the market faces headwinds from strict RoHS compliance costs and reliance on Asian semiconductor imports. Automotive manufacturers like Volkswagen and BMW are driving innovation in galvanic isolation for next-gen electric vehicles, partnering with Infineon and STMicroelectronics for customized solutions.

South America

The South American market remains nascent but shows promise, with Brazil accounting for 60% of regional demand. Mining and oil/gas applications drive growth, though economic instability limits large-scale adoption. Local manufacturers focus on cost-effective, lower-speed isolators (under 25 Mbps) for consumer electronics. The lack of domestic semiconductor production creates dependency on U.S. and Chinese imports, resulting in supply chain vulnerabilities. Recent trade agreements with Asian suppliers aim to improve component availability for Argentina’s growing industrial automation sector.

Middle East & Africa

This region represents the smallest but fastest-growing market (CAGR 11.3%), led by UAE and Saudi Arabia’s smart city initiatives. Telecom infrastructure projects (including 5G rollouts) consume 70% of regional isolator supply. South Africa shows potential in automotive applications, though limited local expertise necessitates technology transfers from European partners. High import duties and lack of testing facilities slow market maturation, while growing data center investments in Morocco and Egypt present new opportunities for isolator suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High-Speed Digital Isolator markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global High-Speed Digital Isolator market was valued at USD 471 million in 2024 and is projected to reach USD 848 million by 2032, growing at a CAGR of 9.0%.

- Segmentation Analysis: Detailed breakdown by product type (Dual-Channel, Quad-Channel), application (Industrial Control, New Energy, Digital Power), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific holding the largest market share of 42% in 2024.

- Competitive Landscape: Profiles of 15 leading market participants including Analog Devices, Texas Instruments, Broadcom, and Infineon, who collectively hold 68% market share.

- Technology Trends & Innovation: Assessment of emerging technologies including advanced CMOS isolation techniques and integration with Industry 4.0/IoT systems.

- Market Drivers & Restraints: Evaluation of factors such as 5G expansion (global 5G infrastructure market projected at USD 47.78 billion by 2027) and Industry 4.0 adoption versus supply chain challenges.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, industrial automation providers, and investors in the high-speed isolation technology ecosystem.

The research employs both primary and secondary methodologies, including interviews with key industry players and analysis of verified market data from regulatory bodies and trade associations.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-Speed Digital Isolator Market?

-> High-Speed Digital Isolator Market was valued at 471 million in 2024 and is projected to reach US$ 848 million by 2032, at a CAGR of 9.0% during the forecast period.

Which key companies operate in Global High-Speed Digital Isolator Market?

-> Key players include Analog Devices, Texas Instruments, Broadcom, Infineon, Skyworks Solutions, and NVE Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, industrial automation growth, and increasing data rates in communication systems.

Which region dominates the market?

-> Asia-Pacific dominates with 42% market share, driven by semiconductor manufacturing in China and industrial automation in Japan.

What are the emerging trends?

-> Emerging trends include higher channel density isolators, integration with power management ICs, and automotive-grade isolation solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...