High-Reliability Components Market Insights

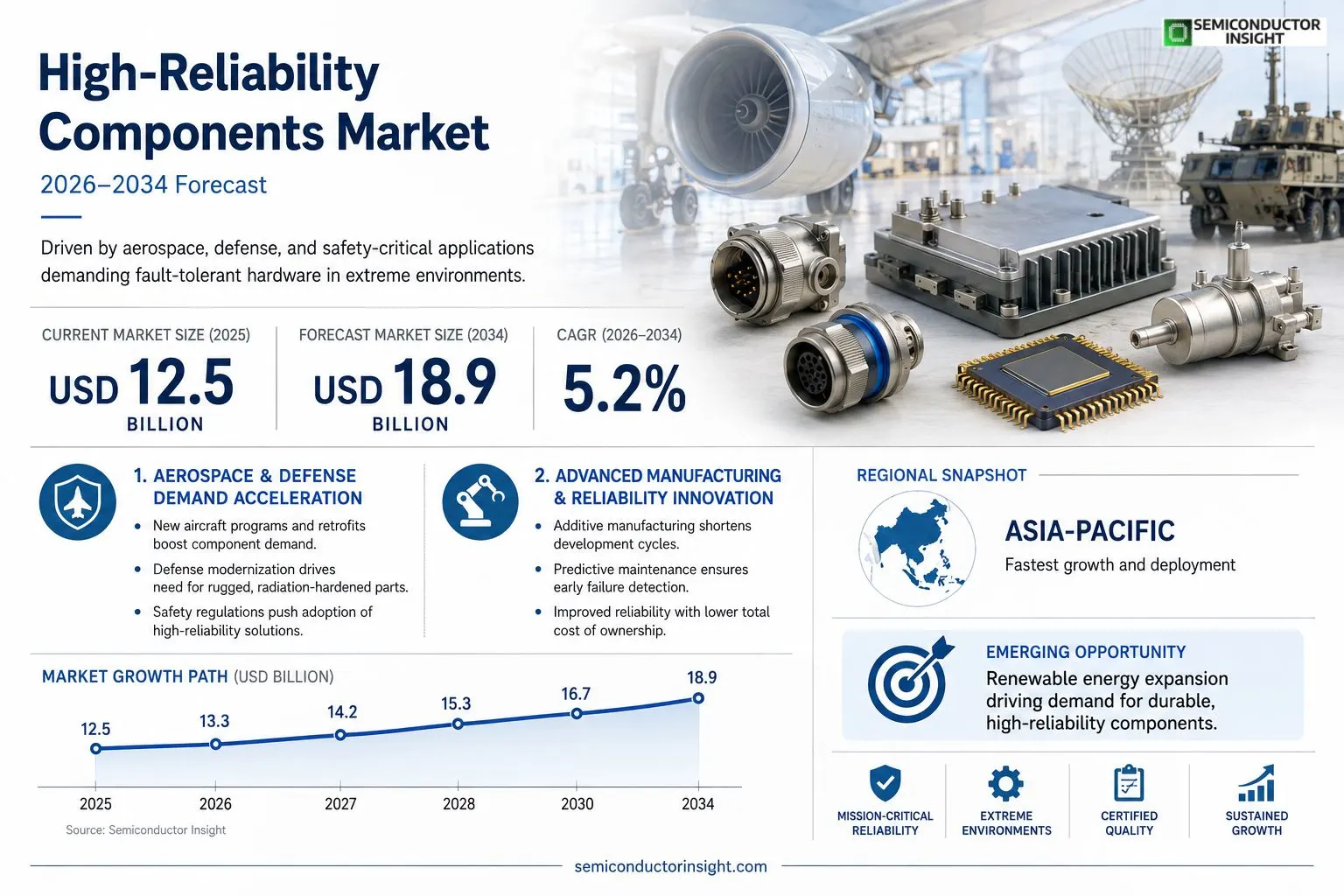

High‑Reliability Components Market size was valued at USD 12.5 billion in 2025. The market is projected to grow from USD 13.3 billion in 2026 to USD 18.9 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period.

High‑reliability components are engineered parts designed to operate under extreme conditions such as high temperature, vibration, radiation, or pressure while maintaining strict performance tolerances. Typical categories include aerospace‑grade connectors, defense‑qualified semiconductors, medical‑device micro‑actuators, and ruggedized power modules.The market is accelerating because aerospace expansion, defense modernization, and stringent safety regulations drive demand for fault‑tolerant hardware. However, supply‑chain constraints and high certification costs pose challenges. Furthermore, advances in additive manufacturing and predictive maintenance technologies enable manufacturers to deliver more reliable products faster, encouraging further investment from key players such as Honeywell International Inc., Raytheon Technologies Corp., and TE Connectivity Ltd.

MARKET DRIVERS

Increasing Demand in Aerospace & Defense

High-Reliability Components Market is being propelled by the aerospace sector’s requirement for components that can endure extreme temperature and vibration. In 2023, aerospace manufacturers accounted for roughly 38% of total component shipments, reflecting a steady upward trajectory driven by new fighter jet programmes and commercial aircraft retrofits.

Growth of Autonomous Systems

Autonomous vehicles and drones rely on fault‑tolerant electronics to meet safety standards. The market saw a 12% year‑over‑year increase as manufacturers integrated high‑reliability sensors and processors into next‑generation platforms, expanding the addressable market beyond traditional sectors.

➤ Analysts forecast that cumulative revenue could surpass $15 billion by 2028, driven largely by these two pillars.

Overall, the convergence of stringent performance criteria and expanding application domains creates a robust growth engine for High‑Reliability Components Market.

MARKET CHALLENGES

Stringent Certification Requirements

Regulatory bodies such as the FAA and MIL‑STD impose rigorous testing protocols that extend product development cycles. Companies often face delays of 9‑12 months, inflating costs and limiting the speed at which new components reach the market.

Other Challenges

Supply Chain Constraints

shortages of specialty alloys and semiconductor wafers have tightened inventory levels, causing average lead times to rise to 14 weeks, which hampers timely delivery to critical projects.

MARKET RESTRAINTS

High Manufacturing Costs

Fabricating components that meet reliability thresholds requires precision processes such as vacuum deposition and laser welding, which increase unit costs by 30‑45% compared with standard parts. This price premium restricts adoption in cost‑sensitive segments like consumer electronics.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy

Wind turbine generators and solar inverters are demanding components that can operate reliably under harsh environmental conditions for decades. Anticipated deployment of over 150 GW of new renewable capacity through 2027 presents a significant upside for providers of high‑reliability modules.

High-Reliability Components Market Trends

Growing Aerospace and Defense Demand

High‑Reliability Components Market is being reshaped by rapid expansion in aerospace and defense programs. Aircraft manufacturers are increasing orders for aerospace‑grade connectors and rugged power modules that can endure extreme temperature and vibration. Defense modernization initiatives require components qualified for harsh radiation and pressure environments, prompting procurement of fault‑tolerant semiconductors. This surge is amplified by tighter safety regulations that mandate higher performance tolerances, driving OEMs to source parts engineered for reliability rather than cost alone. As mission‑critical platforms become more complex, the need for hardware that can guarantee uninterrupted operation under stress is becoming a strategic priority across the sector.

Other Trends

Supply Chain Constraints and Certification Costs

Supply‑chain bottlenecks are limiting the speed at which manufacturers can deliver high‑reliability parts. Limited capacity at specialty foundries and the need for extensive qualification testing extend lead times. Certification processes, especially for defense‑qualified components, involve multiple rounds of testing and documentation, increasing overall project expenses. Companies are responding by investing in longer‑term supplier contracts and developing in‑house testing capabilities to reduce dependency on external labs. While these measures improve resilience, they also raise the upfront capital required for new product introductions, making strategic budgeting essential for sustained growth.

Emerging Manufacturing Technologies

Advances in additive manufacturing and predictive maintenance are opening new pathways for High‑Reliability Components Market. 3D‑printed metallic structures enable rapid prototyping of micro‑actuators and custom enclosures that meet stringent tolerance specifications while reducing material waste. Predictive analytics, integrated into production lines, allow early detection of potential failure modes, ensuring that components meet reliability standards before shipment. These technologies shorten development cycles and lower the total cost of ownership, encouraging key players to adopt more agile production models. The convergence of these innovations is expected to increase the availability of fault‑tolerant hardware, supporting broader adoption across aerospace, medical devices, and industrial automation.

COMPETITIVE LANDSCAPEKey Industry Players

High‑Reliability Components Market Competitive Overview

High‑Reliability Components Market is dominated by a few large, vertically integrated manufacturers that combine deep engineering expertise with extensive certification capabilities. Honeywell International Inc. leads the space with its aerospace‑grade connectors and defense‑qualified sensors, leveraging a supply chain that supports stringent aerospace and military programs. Raytheon Technologies Corp. follows closely, primarily through its subsidiary Collins Aerospace, which supplies ruggedized power modules and mission‑critical avionics hardware. TE Connectivity Ltd. rounds out the top tier, offering a broad portfolio of high‑temperature and vibration‑resistant connectors that serve both the aerospace and medical device segments. These three firms control a substantial share of the market, set pricing benchmarks, and drive technology standards through continuous investment in additive manufacturing and predictive‑maintenance enabled design.Beyond the leading trio, a diverse set of niche players contributes specialized expertise and regional strength. Safran (via its Aerosystems unit) provides high‑precision fasteners for aircraft propulsion systems, while Analog Devices and Texas Instruments deliver defense‑qualified semiconductors with radiation‑hardening. BAE Systems, L3Harris Technologies, and Cobham focus on ruggedized communication modules for defense applications. Microchip Technology and MTS Systems supply micro‑actuators for medical devices, and ABB offers rugged power converters for industrial aerospace ground support. Amphenol and Mersen round out the landscape with connector assemblies and high‑performance resistors that meet stringent reliability criteria, ensuring a competitive ecosystem that supports continuous market growth.

List of Key High‑Reliability Components Companies Profiled

- Honeywell International Inc.

- Raytheon Technologies Corp.

- TE Connectivity Ltd.

- Safran

- Analog Devices

- Texas Instruments

- BAE Systems

- L3Harris Technologies

- Cobham

- Microchip Technology

- MTS Systems

- ABB

- Amphenol

- Mersen

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Defense‑qualified semiconductors dominate this classification because they are engineered to survive extreme radiation and temperature gradients, making them indispensable for mission‑critical aerospace and defense platforms.

|

| By Application |

|

Spacecraft propulsion control emerges as the leading application segment due to the uncompromising demand for components that can endure vacuum, thermal cycling, and high‑g forces while delivering precise actuation.

|

| By End User |

|

Defense contractors command the highest preference for high‑reliability components because mission assurance and regulatory compliance are non‑negotiable.

|

| By Technology |

|

Advanced ceramic encapsulation is identified as the most influential technology trend, delivering superior thermal resistance and dielectric stability for extreme environments.

|

| By Certification |

|

Space qualified (NASA/ESA) leads this segment because the aerospace sector insists on components that have passed exhaustive environmental testing and certification processes, ensuring mission reliability.

|

Regional Analysis: North America

United States

This sector represents a significant portion of High-Reliability Components Market in the US, driven by stringent performance requirements and safety regulations. Advancements in aircraft technology and defense systems continually necessitate more durable and dependable components.

The healthcare industry’s reliance on intricate medical devices fuels demand for high-reliability components. These components directly impact patient safety and the efficacy of diagnostic and therapeutic procedures.

The expansion of 5G networks and the increasing reliance on data centers are driving demand for high-reliability components in telecommunications infrastructure. These components ensure network stability and data integrity.

The growth of automation in manufacturing and other industrial sectors necessitates high-reliability components to ensure continuous operation and minimize downtime.

Europe

Europe presents a substantial and steadily growing market for High-Reliability Components. The region’s strong engineering tradition and advanced manufacturing capabilities contribute to a consistent demand for dependable solutions. Stringent regulatory environments, particularly in sectors like automotive and aerospace, foster the adoption of high-reliability components. Emphasis on sustainability is also influencing the market, with growing demand for components that enhance energy efficiency and reduce environmental impact. Innovation in electric vehicles and smart grid technologies presents new opportunities for component manufacturers. The focus on circular economy principles is also impacting component design and lifecycle management.

Asia-Pacific

Asia-Pacific represents the fastest-growing region within High-Reliability Components Market. Fueled by rapid industrialization in countries like China and India, the region is experiencing exponential growth in demand. The expansion of manufacturing sectors, coupled with increasing investments in infrastructure development and technological advancements, are key drivers. The electronics industry in Asia-Pacific is a major consumer of high-reliability components, supporting the growth of consumer electronics, industrial automation systems, and telecommunications networks. Government initiatives promoting domestic manufacturing and technological self-reliance are further boosting the market. Competitive pricing and a large pool of skilled labor contribute to the region’s attractiveness for component manufacturers.

South America

South America’s High-Reliability Components Market is characterized by moderate growth potential. The expansion of the mining, energy, and telecommunications sectors are key demand drivers. Infrastructure development projects, particularly in Brazil and Argentina, are creating opportunities for component suppliers. The increasing adoption of automation in industries like agriculture and manufacturing is also contributing to market growth. Economic fluctuations and political instability can pose challenges to market development. Regional variations in industrialization levels create diverse market dynamics across the continent.

Middle East & Africa

The Middle East & Africa region exhibits promising growth prospects for High-Reliability Components Market. Significant investments in infrastructure projects, particularly in the oil & gas, transportation, and defense sectors, are fueling demand. The expanding telecommunications infrastructure and the increasing adoption of smart city technologies are also contributing to market growth. The region’s focus on energy diversification and renewable energy initiatives presents new opportunities for component suppliers specializing in these areas. Geopolitical factors and regional conflicts can influence market stability and investment patterns.

Report Scope

This market research report provides a comprehensive analysis of the High-Reliability Components Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-Reliability Components Market?

-> High-Reliability Components Market was valued at USD 12.5 billion in 2025 and is expected to reach USD 18.9 billion by 2034. The projected CAGR for the period 2026‑2034 is 5.2%.

Which key companies operate in High-Reliability Components Market?

-> Key players include Honeywell International Inc., Raytheon Technologies Corp., and TE Connectivity Ltd.

What are the key growth drivers?

-> Key growth drivers include aerospace expansion, defense modernization, and stringent safety regulations driving demand for fault‑tolerant hardware.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include advances in additive manufacturing, predictive maintenance technologies, and integration of AI/IoT for enhanced reliability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...