MARKET INSIGHTS

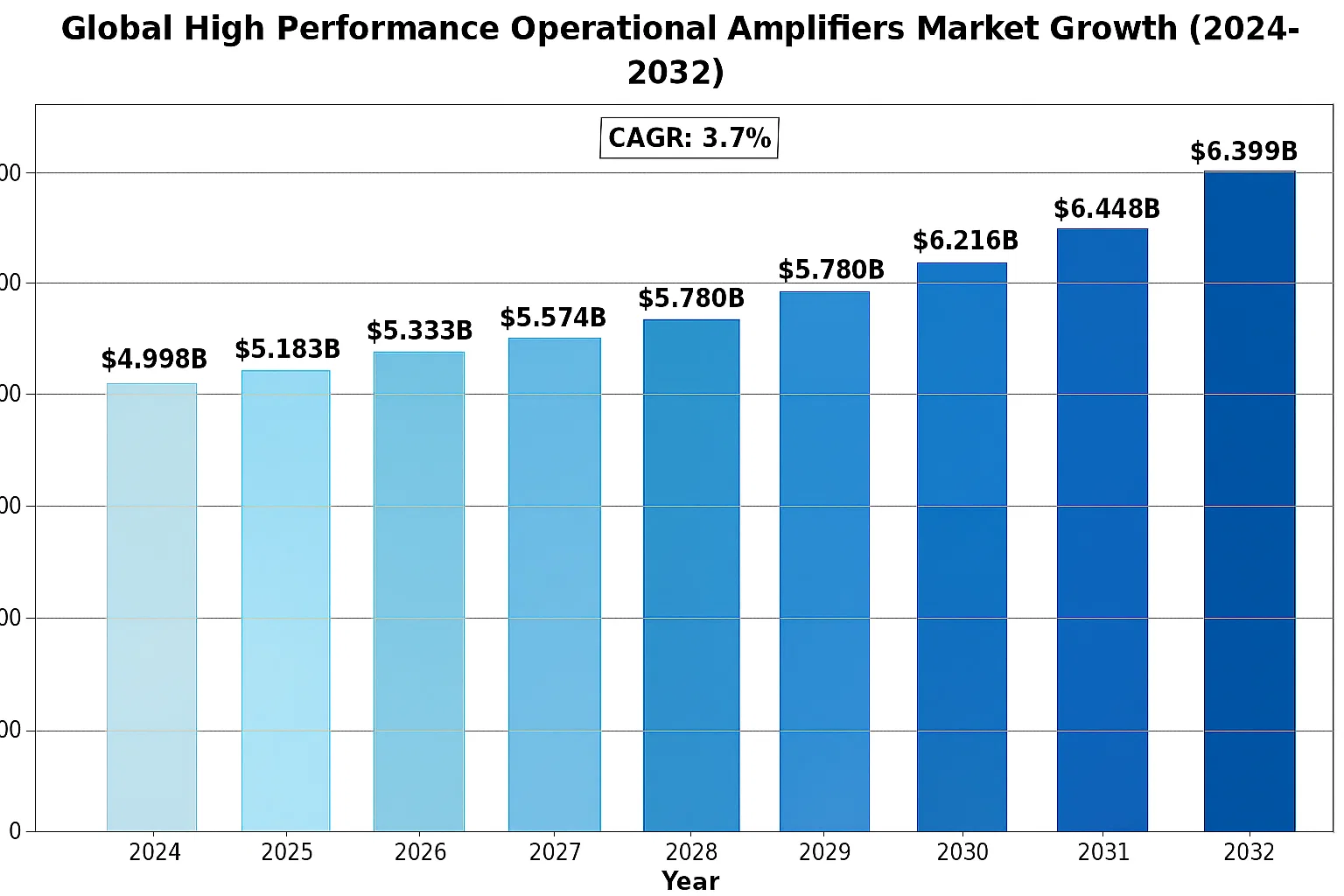

The global High Performance Operational Amplifiers market was valued at 4998 million in 2024 and is projected to reach US$ 6399 million by 2032, at a CAGR of 3.7% during the forecast period.

High performance operational amplifiers (op-amps) are specialized integrated circuits designed for precision signal conditioning. These components feature low noise, low input offset voltage, and high speed, making them ideal for battery-powered devices and sensor applications. The product category includes both open-loop and closed-loop amplifier configurations, serving diverse applications from medical instruments to vehicle electronics.

The market growth is driven by increasing demand for precision analog components in IoT devices and industrial automation systems. While the broader semiconductor market grew at 4.4% in 2022, the analog segment showed stronger performance with 20.8% year-over-year growth. However, regional variations exist – Asia Pacific saw a 2% decline in semiconductor sales in 2022, while Americas and Europe grew by 17% and 12.6% respectively. Key players like Texas Instruments and Analog Devices continue to innovate, developing op-amps with lower power consumption and higher accuracy for next-generation applications.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and Industrial Automation to Accelerate Market Growth

The rapid expansion of IoT devices and industrial automation systems is catalyzing demand for high performance operational amplifiers (op-amps). Modern IoT applications require precision signal conditioning for sensors in environments ranging from smart homes to industrial monitoring systems. Global IoT connections are projected to exceed 25 billion active endpoints by 2025, creating substantial demand for analog components that can maintain signal integrity in noisy environments. High performance op-amps with low noise characteristics (typically below 10nV/√Hz) and high common-mode rejection ratios (often exceeding 90dB) are becoming indispensable in these applications.

Industrial automation is seeing particular growth in sectors like robotics and process control, where error rates below 0.1% are frequently required for precision measurements. The manufacturing sector’s increasing adoption of Industry 4.0 technologies has driven analog IC demand up by approximately 18% year-over-year in automation applications, with operational amplifiers representing a significant portion of these components. New product launches from major manufacturers specifically targeting industrial IoT applications underscore this trend. For instance, several industry leaders introduced rail-to-rail output op-amps in 2023 with power consumption under 1mA, specifically optimized for battery-powered industrial sensors.

Advancements in Automotive Electronics to Fuel Market Expansion

The automotive electronics revolution is creating unprecedented demand for high performance analog components. Modern vehicles contain over 3,000 analog chips on average, with electric vehicles (EVs) utilizing 40-50% more semiconductor content than traditional internal combustion vehicles. The global automotive semiconductor market is projected to grow at nearly 7% annually through 2030, with analog ICs capturing the largest segment share. High performance op-amps are particularly crucial in EV battery management systems, where monitoring accuracy within 0.1mV is often required for cell balancing circuits.

Advanced driver assistance systems (ADAS) represent another key growth area, employing precision op-amps for sensor signal conditioning in radar, LiDAR and camera systems. The typical premium vehicle now incorporates over 20 ultrasonic sensors, 6-8 cameras, and at least one forward-facing radar – all requiring sophisticated analog signal chains. Recent design wins in this sector highlight the trend toward high-speed amplifiers (>50MHz bandwidth) with ultra-low offset voltage (<50μV) to maintain signal fidelity in safety-critical applications.

➤ The move toward autonomous driving is pushing op-amp performance boundaries, with 2023 seeing multiple vendors introduce automotive-grade amplifiers featuring EMI hardening and fault detection capabilities.

Furthermore, the electrification of power steering and braking systems is creating demand for robust high-current op-amps capable of driving loads up to 500mA while maintaining thermal stability. This convergence of automotive innovation and analog semiconductor technology is expected to sustain market growth throughout the decade.

MARKET CHALLENGES

Design Complexity and Precision Requirements to Test Manufacturer Capabilities

While the market shows strong growth potential, achieving the required performance specifications presents significant technical hurdles. Modern applications demand operational amplifiers with increasingly stringent parameters – noise levels below 5nV/√Hz at 1kHz, offset voltages under 10μV, and temperature drift below 0.5μV/°C are becoming common requirements. Achieving these specifications while maintaining competitive power consumption and cost structures poses formidable design challenges. Yield rates for the most precise amplifiers can drop below 60% in production, significantly impacting gross margins.

Other Challenges

Thermal Management Constraints

High-performance applications often push op-amps to their thermal limits, especially in automotive and industrial environments. Maintaining specifications across military temperature ranges (-55°C to +125°C) requires careful die design and packaging innovation. Some manufacturers report reliability testing cycles extending beyond 18 months for new high-temperature amplifier families.

Supply Chain Vulnerabilities

The global semiconductor shortage highlighted vulnerabilities in analog component supply chains. While digital IC production has largely rebounded, the specialized test equipment and wafer processing required for precision analog products continues to face capacity constraints. Lead times for certain high-performance amplifier series remain extended beyond 40 weeks as of early 2024.

MARKET RESTRAINTS

Pricing Pressure from Commodity Alternatives to Limit Market Expansion

The high performance op-amp market faces growing competition from general-purpose amplifiers that have improved their specifications to near-performance levels. In cost-sensitive applications, designers are often willing to accept slightly higher noise or offset in exchange for 40-60% cost reductions. This trend is particularly evident in consumer electronics, where some manufacturers have successfully substituted $0.50 general-purpose amplifiers for $2.00+ precision counterparts in non-critical signal paths.

Additionally, the rise of integrated analog front-ends (AFEs) is cannibalizing discrete op-amp sockets in applications like sensor interfaces. Modern AFEs combine amplifiers, ADCs, and digital processing in single packages, often achieving better system-level performance while reducing board space and component count. The medical instrumentation sector, traditionally a stronghold for discrete precision amplifiers, has seen AFE penetration reach over 35% in new designs.

Manufacturers are responding by focusing on applications where performance absolutely cannot be compromised – scientific instrumentation, aerospace systems, and ultra-high-end audio equipment continue to demand the most exacting amplifier specifications regardless of cost.

MARKET OPPORTUNITIES

Emerging Applications in Medical Technology to Drive Next Growth Phase

The healthcare sector presents significant untapped potential for high performance operational amplifiers. Medical imaging equipment such as MRI machines and CT scanners require ultra-low noise amplification of microvolt-level signals from detector arrays. Newer modalities like digital pathology and genomic sequencing instruments are pushing bandwidth requirements beyond 100MHz while maintaining sub-microvolt noise floors. The global medical electronics market is projected to exceed $8 billion by 2027, creating substantial opportunities for amplifier manufacturers.

Wearable health monitors represent another promising growth avenue. While consumer wearables often use integrated solutions, medical-grade continuous glucose monitors and ECG patches require discrete precision amplifiers to meet FDA accuracy requirements. The shift toward disposable medical sensors is driving innovation in ultra-low-power amplifier designs that maintain critical specifications on coin cell batteries for 14+ days. Several vendors have recently introduced amplifiers with quiescent currents below 10μA specifically targeting these applications.

Furthermore, the development of neural interface technologies is creating demand for amplifiers with unprecedented capabilities. Brain-machine interfaces require amplification of neural signals in the 0.1μV to 500μV range with bandwidth from 1Hz to 7kHz, all while maintaining power budgets under 1mW per channel. These emerging applications could redefine performance benchmarks for operational amplifiers in coming years.

HIGH PERFORMANCE OPERATIONAL AMPLIFIERS MARKET TRENDS

Expansion of IoT and Automotive Electronics Accelerating Market Growth

The demand for high performance operational amplifiers (op-amps) is being driven by the rapid expansion of Internet of Things (IoT) devices and automotive electronics. These amplifiers play a critical role in signal conditioning, filtering, and precision measurements in IoT sensors, which are expected to exceed 30 billion connected devices globally by 2025. In the automotive sector, the shift toward electric vehicles and advanced driver-assistance systems (ADAS) is contributing to increased adoption. Modern vehicles require ultra-low-noise, high-speed op-amps to process sensor data from LiDAR, radar, and camera systems with minimal signal distortion.

Other Trends

Miniaturization and Power Efficiency Requirements

The drive toward miniaturized electronics in wearables, medical implants, and portable devices is pushing manufacturers to develop op-amps with reduced footprint and power consumption. The global market for wearable devices alone is projected to surpass $118 billion by 2028, necessitating amplifiers that consume minimal power while maintaining high fidelity. Innovations in semiconductor packaging, such as wafer-level chip-scale packaging (WLCSP), enable smaller form factors without compromising precision, making them ideal for space-constrained applications.

Industrial Automation and 5G Infrastructure Driving Demand

Operational amplifiers are experiencing heightened demand from industrial automation and 5G infrastructure deployments. The industrial sector requires amplifiers with low offset voltage and high common-mode rejection to ensure accuracy in process control systems. Meanwhile, 5G base stations and network equipment rely on high-performance op-amps for signal integrity in RF front-end modules. The 5G infrastructure market is projected to grow at a CAGR of nearly 50% by 2030, further fueling adoption. Additionally, industry leaders are investing in radiation-hardened amplifiers for aerospace and defense applications, ensuring reliability in extreme environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Compete Through Innovation in Precision Analog Solutions

The global high performance operational amplifiers market features a moderately concentrated competitive environment, dominated by established semiconductor leaders alongside specialized analog IC manufacturers. Texas Instruments leads the market with approximately 28% revenue share in 2024, leveraging its comprehensive portfolio of precision op-amps and strong distribution networks across automotive, industrial, and consumer electronics sectors. Their OPA series amplifiers remain the industry benchmark for low-noise, high-speed applications.

Analog Devices follows closely with 22% market share, distinguished by its innovative current-feedback amplifiers and instrumentation-grade solutions. The company’s recent acquisition of Linear Technology has significantly strengthened its position in high-end analog components, particularly for aerospace and medical applications where precision is critical.

Meanwhile, STMicroelectronics and NXP Semiconductors are accelerating growth through strategic focus on automotive electrification and IoT edge devices. ST’s Rail-to-Rail series has gained particular traction in battery-powered systems, while NXP’s precision op-amps are increasingly designed into advanced driver assistance systems (ADAS).

The market also sees vigorous competition from Japanese suppliers like ROHM Semiconductor and New Japan Radio, who dominate specialized segments including audio processing and industrial sensors. Their success stems from decades of expertise in analog circuit design and strong relationships with regional OEMs.

List of Key High Performance Op-Amp Manufacturers

- Texas Instruments (U.S.)

- Analog Devices, Inc. (U.S.)

- ROHM Semiconductor (Japan)

- Maxim Integrated (U.S.)

- STMicroelectronics (Switzerland)

- NXP Semiconductors (Netherlands)

- Cirrus Logic (U.S.)

- KEC Corporation (Japan)

- New Japan Radio (Japan)

- ON Semiconductor (U.S.)

- Renesas Electronics (Japan)

- API Technologies (U.S.)

- Microchip Technology (U.S.)

Segment Analysis:

By Type

Closed-Loop Amplifier Segment Dominates Due to Superior Stability and Precision in Critical Applications

The market is segmented based on type into:

- Open-Loop Amplifier

- Subtypes: General-purpose, High-speed, and others

- Closed-Loop Amplifier

- Subtypes: Voltage feedback, Current feedback, and others

By Application

Test and Measurement Instruments Lead Due to Increasing Demand for High-Precision Electronic Equipment

The market is segmented based on application into:

- Automatic Control System

- Test and Measurement Instruments

- Medical Instruments

- Vehicle Electronics

- Others

By End User

Industrial Sector Accounts for Largest Share Due to Automation and Process Control Applications

The market is segmented based on end user into:

- Industrial

- Healthcare

- Automotive

- Consumer Electronics

- Telecommunications

Regional Analysis: High Performance Operational Amplifiers Market

North America

The North American high-performance operational amplifiers (op-amps) market benefits from strong demand in aerospace, defense, and medical instrumentation sectors, where precision analog signal processing is critical. Texas Instruments and Analog Devices dominate the regional supply chain, leveraging their advanced semiconductor manufacturing capabilities. Stringent industrial standards for noise reduction and power efficiency in applications like electric vehicles (EVs) and renewable energy systems further drive innovation. The U.S. CHIPS and Science Act, which allocates $52 billion for domestic semiconductor production, is expected to bolster local supply resilience. However, high production costs and reliance on niche applications limit volume growth compared to Asia-Pacific markets.

Europe

Europe’s market is characterized by stringent EMI/EMC compliance requirements under EU directives, particularly for automotive and industrial automation applications. Germany and France lead in adopting precision op-amps for Industry 4.0 solutions, where sensor signal conditioning is pivotal. STMicroelectronics and NXP Semiconductors are key innovators, focusing on ultra-low-power designs for IoT edge devices. The region’s emphasis on renewable energy infrastructure also creates demand for high-voltage op-amps in solar/wind power conditioning systems. However, slower adoption in consumer electronics due to cost sensitivity and competition from Asian manufacturers presents a growth challenge.

Asia-Pacific

Accounting for over 40% of global consumption, the Asia-Pacific region thrives due to massive electronics manufacturing hubs in China, Japan, and South Korea. Local players like ROHM and New Japan Radio compete with Western firms by offering cost-optimized op-amps for consumer durables and industrial control systems. China’s semiconductor self-sufficiency push has accelerated domestic production, though reliance on imported specialty materials persists. India’s growing EV and telecom sectors present new opportunities, but price competition and intellectual property concerns remain barriers. The region’s lead in 5G infrastructure deployment further fuels demand for high-speed op-amps in RF signal chains.

South America

This emerging market shows gradual growth, primarily in Brazil and Argentina, where automotive and energy applications drive demand. Local assembly of industrial equipment and medical devices creates steady but limited need for precision op-amps. Economic instability and currency fluctuations hinder large-scale investments in semiconductor infrastructure, making the region dependent on imports. Recent trade agreements with Asian suppliers are improving component availability, though technological lag compared to North America and Europe persists. The lack of local design expertise further restricts high-end adoption.

Middle East & Africa

The market here is nascent but shows potential in oil/gas instrumentation and telecom infrastructure projects. UAE and Saudi Arabia lead in adopting op-amps for industrial automation in energy sectors, while South Africa sees growth in medical equipment modernization. Limited local semiconductor activity results in complete reliance on imported components, often through European or Asian distributors. While geopolitical stability and diversification from oil-based economies could spur future demand, current low-volume purchasing and technical support gaps slow market maturation.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High Performance Operational Amplifiers markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global High Performance Operational Amplifiers market was valued at USD 4,998 million in 2024 and is projected to reach USD 6,399 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Open-Loop Amplifier, Closed-Loop Amplifier), application (Automatic Control Systems, Test and Measurement Instruments, Medical Instruments, Vehicle Electronics), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis. Asia-Pacific currently leads in market share.

- Competitive Landscape: Profiles of leading market participants including Texas Instruments, Analog Devices, STMicroelectronics, and NXP Semiconductors, covering their product portfolios, market strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor design trends, fabrication techniques, and the impact of IoT integration on operational amplifier requirements.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for precision electronics, automotive applications, and challenges in semiconductor supply chains.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, system integrators, and investors regarding market opportunities.

The analysis employs both primary and secondary research methods, including interviews with industry experts and data from verified market sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Performance Operational Amplifiers Market?

-> The global market was valued at USD 4,998 million in 2024 and is projected to reach USD 6,399 million by 2032 at a CAGR of 3.7%.

Which key companies operate in this market?

-> Major players include Texas Instruments, Analog Devices, STMicroelectronics, NXP Semiconductors, ON Semiconductor, and Renesas Electronics.

What are the key growth drivers?

-> Growth is driven by increasing demand for precision electronics, automotive applications, and IoT device proliferation. The global semiconductor market is projected to grow from USD 579 billion (2022) to USD 790 billion by 2029.

Which region dominates the market?

-> Asia-Pacific leads the market, accounting for the largest share, followed by North America and Europe.

What are the emerging trends?

-> Key trends include development of ultra-low power consumption amplifiers, integration with IoT systems, and increasing automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...