MARKET INSIGHTS

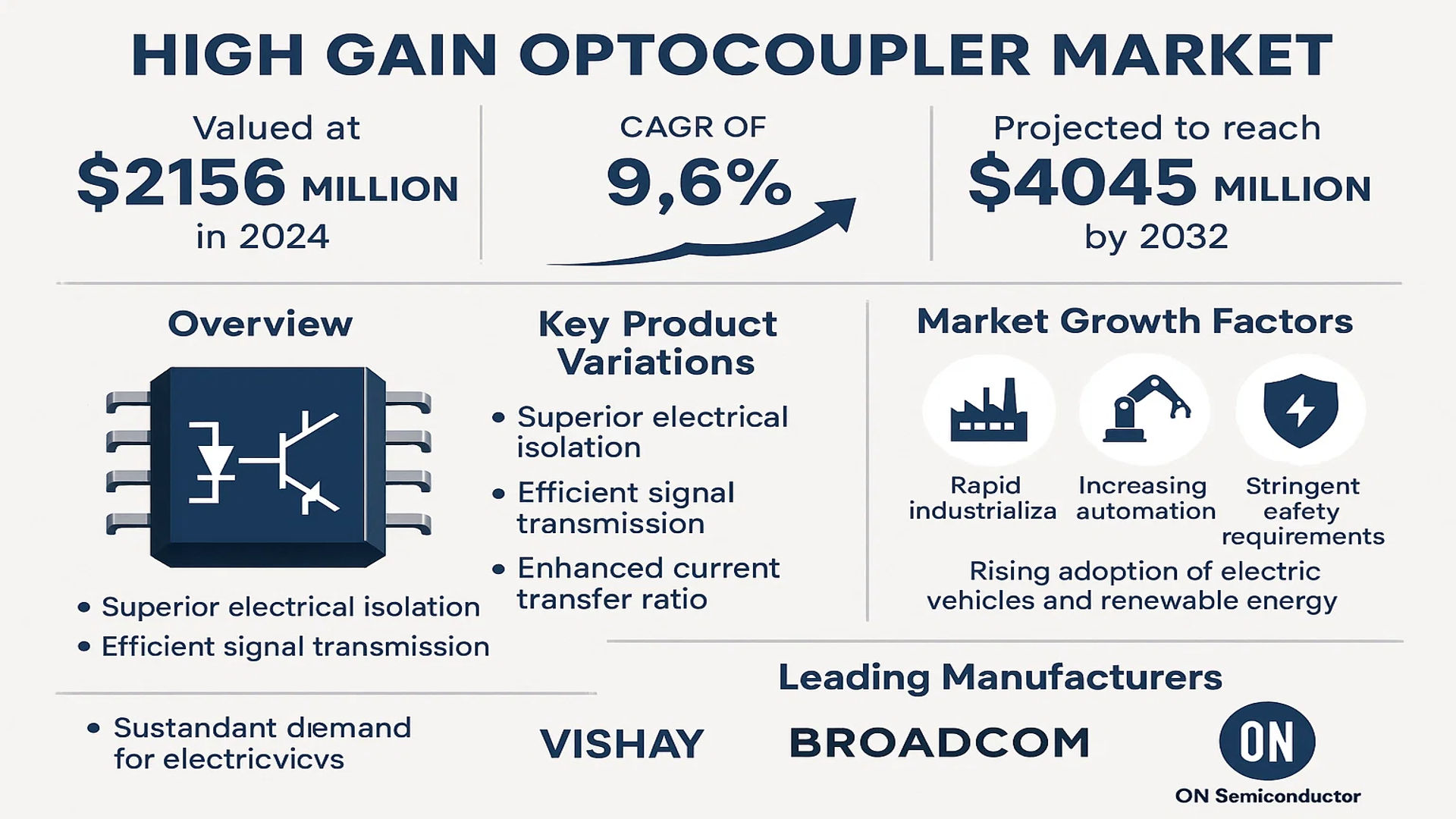

The global High Gain Optocoupler Market was valued at 2156 million in 2024 and is projected to reach US$ 4045 million by 2032, at a CAGR of 9.6% during the forecast period. The market demonstrates strong expansion potential, primarily driven by increasing demand for electrical isolation solutions across industries.

High gain optocouplers are specialized semiconductor devices designed to provide superior electrical isolation while enabling efficient signal transmission through light. These components feature enhanced current transfer ratio (CTR) characteristics, making them ideal for applications requiring high sensitivity and noise immunity. Key product variations include single-channel, dual-channel, and quad-channel configurations.

The market growth is fueled by several key factors, including rapid industrialization, increasing automation in manufacturing processes, and stringent safety requirements in power electronics. Furthermore, the rising adoption of electric vehicles and renewable energy systems has created substantial demand for reliable isolation components. Leading manufacturers such as Vishay, Broadcom, and ON Semiconductor continue to innovate, developing high-performance optocouplers with improved efficiency and durability to meet evolving industry needs.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Industrial Automation Fuels High Gain Optocoupler Adoption

The high gain optocoupler market is experiencing robust growth driven by increasing industrial automation across manufacturing sectors. As factories transition to Industry 4.0 standards, the need for reliable electrical isolation components has surged dramatically. High gain optocouplers play a critical role in protecting sensitive control systems from voltage spikes and electromagnetic interference, with the industrial segment accounting for nearly 42% of global optocoupler applications. The automotive industry’s shift toward electric vehicles presents another substantial growth avenue, as EV power systems require advanced isolation solutions for battery management and motor control circuits.

Expansion of Renewable Energy Infrastructure Creates New Demand

Global investments in renewable energy systems are creating significant opportunities for high gain optocouplers. Solar inverters and wind turbine controllers require high-performance isolation components to ensure safe operation and prevent ground loops. The photovoltaic inverter market alone is projected to grow at 6.8% annually through 2030, directly driving demand for reliable optocoupler solutions. High gain variants are particularly valuable in these applications due to their ability to maintain signal integrity across isolation barriers while withstanding harsh environmental conditions. Manufacturers are responding with specialized products featuring extended temperature ranges and enhanced noise immunity.

Recent developments in electric vehicle charging infrastructure further amplify this trend, as smart charging stations increasingly incorporate optocouplers for safety isolation and communication protocol implementation.

MARKET RESTRAINTS

Component Miniaturization Challenges Impacting Optocoupler Design

While demand grows, high gain optocoupler manufacturers face significant technical constraints due to industry-wide miniaturization trends. Modern electronic systems increasingly require smaller form factors, creating engineering challenges for maintaining optical coupling efficiency in reduced package sizes. The performance compromise becomes particularly apparent in high-speed switching applications above 1MHz, where larger phototransistor designs traditionally provided better gain characteristics. This technical trade-off has led some designers to consider alternative isolation technologies in space-constrained applications.

Supply Chain Disruptions Continue to Affect Market Stability

The semiconductor industry’s ongoing supply chain challenges significantly impact high gain optocoupler availability and pricing. Lead times for specialized optoelectronic components remain extended, with some vendors reporting 30-40 week delays for custom configurations. These disruptions stem from multiple factors including wafer fabrication capacity constraints and shortages of hermetic packaging materials. While the situation shows gradual improvement, price volatility continues to pose challenges for system designers requiring stable component costs for long product lifecycles. The automotive industry’s just-in-time manufacturing model has been particularly affected, with some OEMs redesigning circuits to accommodate available components.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Presents New Application Frontiers

Fifth-generation wireless network deployment offers substantial growth potential for high gain optocouplers in telecom equipment. Base station power systems require robust isolation components for surge protection and signal conditioning, with tower electronics particularly benefiting from the noise immunity of optical coupling. The global 5G infrastructure market is expected to maintain 26% annual growth through 2030, creating parallel demand for specialized isolation solutions. Telecommunications applications often demand components that can withstand wide temperature fluctuations while maintaining consistent current transfer ratios – parameters where high gain optocouplers excel.

Medical Electronics Adoption Creates High-Value Niche Markets

The healthcare sector’s increasing reliance on electronic diagnostic and treatment equipment presents growing opportunities for high performance optocouplers. Patient-connected medical devices require stringent isolation to meet safety standards, often necessitating components with guaranteed minimum current transfer ratios. Applications range from imaging equipment to wearable health monitors, with the medical electronics market projected to grow at 8.2% CAGR through 2028. Leading manufacturers are developing specialized product lines featuring medical-grade certifications and enhanced reliability testing to serve this demanding sector.

MARKET CHALLENGES

Thermal Management Issues in High-Density Applications

As electronic systems increase in complexity, thermal performance becomes a critical challenge for high gain optocoupler implementation. The phototransistor elements in these devices generate noticeable heat during operation, which can affect performance consistency in high-density circuit designs. This thermal sensitivity becomes particularly problematic in automotive and industrial applications where ambient temperatures may approach 85°C or higher. Manufacturers are addressing this through advanced materials and package designs, but the fundamental physics of optoelectronic conversion imposes inherent limitations on thermal performance.

Competition from Alternative Isolation Technologies

High gain optocouplers face increasing competition from emerging isolation technologies such as capacitive and magnetic couplers. These alternatives offer potential advantages in speed, power efficiency, and integration density, particularly for digital signal isolation. While optical coupling maintains superiority in many analog applications and high-voltage scenarios, the competitive landscape requires constant innovation from optocoupler manufacturers. Market analysis indicates that the share of non-optical isolation solutions has grown by nearly 3% annually over the past five years, prompting traditional optocoupler vendors to enhance their product offerings with improved speed and efficiency characteristics.

HIGH GAIN OPTOCOUPLER MARKET TRENDS

Industrial Automation Expansion Fuels Demand for High Gain Optocouplers

The rapid adoption of Industry 4.0 technologies across manufacturing sectors is driving significant growth in the high gain optocoupler market. These components play a critical role in protecting sensitive control systems from electrical noise and voltage fluctuations prevalent in industrial environments. With industrial automation investments projected to maintain a 7.8% CAGR through 2030, optocouplers are becoming increasingly essential for motor control, power supply isolation, and PLC interfacing applications. Recent advancements in optocoupler technology now allow for faster switching speeds exceeding 10 MHz, making them viable for high-frequency industrial applications that previously required more expensive isolation solutions.

Other Trends

Electric Vehicle Revolution Drives New Applications

The automotive industry’s transition to electric powertrains has created substantial demand for high-performance isolation components. Modern EVs require robust voltage isolation between battery management systems and control units, where high gain optocouplers provide reliable protection against 1,000V+ potential differences. This sector alone accounts for over 25% of the current optocoupler market growth, with expectations of accelerating adoption as EV production volumes increase globally.

Telecommunications Infrastructure Upgrades Create Opportunities

Global 5G network deployments and data center expansions are generating new requirements for high-speed signal isolation in communication equipment. Next-generation optocouplers with 1MBd+ data rates are enabling reliable transmission in base stations and network switches while maintaining critical galvanic isolation. The telecommunications segment now represents approximately 18% of the high gain optocoupler market, with particular strength in Asia-Pacific regions experiencing aggressive 5G rollout schedules. Manufacturers are responding with products featuring lower power consumption and higher temperature tolerance to meet telecom equipment specifications.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Capitalize on Rising Industrial Automation Demand

The high gain optocoupler market features a diverse competitive landscape dominated by established semiconductor manufacturers, with the top five players collectively holding approximately 45% market share in 2024. Vishay Intertechnology emerges as a frontrunner, leveraging its extensive optoelectronics expertise and robust distribution network across North America and Europe. The company recently expanded its high gain product line to address industrial IoT applications, signaling strategic alignment with growing automation trends.

Broadcom Limited maintains strong market positioning through its patented optocoupler technologies, particularly in automotive applications where demand for high-reliability isolation components continues to rise. Meanwhile, ON Semiconductor has gained traction through its cost-competitive solutions for consumer electronics, capturing significant share in Asia-Pacific markets.

Medium-sized players like ISOCOM and Renesas Electronics differentiate through application-specific designs, particularly for harsh industrial environments. The sector sees steady technological advancements, with companies allocating 7-12% of revenues to R&D focused on improving current transfer ratios and switching speeds. Recent patent filings indicate growing emphasis on integrating smart features like built-in diagnostics in next-generation products.

Strategic shifts are evident as traditional players like Texas Instruments expand into adjacent isolation technologies, while specialized manufacturers double down on high-gain niche applications. The competitive intensity increased following recent capacity expansions in Southeast Asia, where production costs remain favorable compared to Western markets.

List of Key High Gain Optocoupler Companies Profiled

- Vishay Intertechnology (U.S.)

- Broadcom Limited (U.S.)

- Hewlett Packard Enterprise (U.S.)

- ISOCOM Limited (U.K.)

- Fairchild Semiconductor (U.S.)

- ON Semiconductor (U.S.)

- Texas Instruments (U.S.)

- Maxim Integrated (U.S.)

- Avago Technologies (Singapore)

- Renesas Electronics (Japan)

- IXYS Integrated Circuits (U.S.)

Segment Analysis:

By Type

Single Channel Optocouplers Lead the Market Owing to Widespread Use in Industrial Applications

The market is segmented based on type into:

- Single Channel Optocoupler

- Dual Channel Optocoupler

- Quad Channel Optocoupler

- Others

By Application

Industrial Segment Dominates Due to Increasing Automation and Control System Requirements

The market is segmented based on application into:

- Aerospace

- Industrial

- Automobile

- Others

By End-User

Manufacturing Sector Accounts for Major Share Due to High Adoption of Automation Technologies

The market is segmented based on end-user into:

- Electronics Manufacturing

- Automotive Manufacturing

- Aerospace and Defense

- Energy and Power

- Others

By Technology

GaAs-based Optocouplers Gain Traction for High-Speed Applications

The market is segmented based on technology into:

- Silicon-based Optocouplers

- GaAs-based Optocouplers

- Others

Regional Analysis: High Gain Optocoupler Market

Asia-Pacific

As the global leader in the High Gain Optocoupler market, Asia-Pacific commands the largest market share, accounting for over 45% of global demand in 2024. The region’s dominance stems from booming industrial automation sectors in China, Japan, and South Korea, where manufacturers are rapidly adopting optocouplers for isolation and noise immunity in factory equipment. China’s “Made in China 2025” initiative has particularly accelerated demand, with local producers like Renesas Electronics and international players expanding production capacity. While cost competition remains intense, the growing need for reliable signal isolation in electric vehicles and renewable energy systems is driving premium product adoption.

North America

The North American market prioritizes high-reliability optocouplers for aerospace, medical devices, and industrial IoT applications. Stringent safety certifications from organizations like UL and CSA create demand for components with proven longevity. With over 30% of global aerospace optocoupler applications concentrated here, manufacturers focus on radiation-hardened and extended temperature range variants. Recent supply chain reshoring efforts, supported by CHIPS Act funding, are encouraging local production of optoelectronic components. However, the market faces pressure from Asian competitors on price sensitivity in consumer electronics segments.

Europe

European demand centers on automotive and industrial automation, with Germany’s machine tool industry and France’s transportation sector being key consumers. The region mandates IEC/EN safety standards that favor high-gain optocouplers for reliable isolation in motor drives and power conversion systems. Sustainability initiatives drive innovation in lead-free and RoHS-compliant packaging, though the market growth is tempered by slower adoption rates compared to Asia. Collaborative R&D between academic institutions and manufacturers like Vishay and Texas Instruments supports advancements in high-speed data transmission variants for Industry 4.0 applications.

South America

This emerging market shows potential in Brazil’s industrial sector and Argentina’s renewable energy projects, where optocouplers protect sensitive control systems. Economic volatility and import dependency create price sensitivity, limiting adoption of advanced high-gain models. Local assembly of consumer electronics drives demand for cost-effective single-channel optocouplers, while infrastructure projects create niche opportunities for robust industrial-grade components. The lack of local semiconductor fabrication facilities maintains reliance on Asian and North American suppliers.

Middle East & Africa

Growth here stems from oil & gas automation and smart city initiatives in the GCC countries, particularly for hazardous environment applications. The market remains undersupplied, with most components imported through distributors based in UAE and Saudi Arabia. While high-gain optocouplers find use in power grid modernization projects, the broader adoption is constrained by limited technical expertise and preference for integrated solutions over discrete components. Long-term potential exists in South Africa’s manufacturing sector and North African industrial zones, contingent on infrastructure development.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High Gain Optocoupler market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global High Gain Optocoupler market was valued at USD 2,156 million in 2024 and is projected to reach USD 4,045 million by 2032, growing at a CAGR of 9.6%.

- Segmentation Analysis: Detailed breakdown by product type (Single Channel, Dual Channel, Quad Channel), application (Aerospace, Industrial, Automobile, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to rapid industrialization and electronics manufacturing growth.

- Competitive Landscape: Profiles of leading market participants including Vishay, Broadcom, Texas Instruments, On Semiconductor, and Renesas, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in optocoupler design, integration with IoT systems, and advancements in semiconductor fabrication techniques.

- Market Drivers & Restraints: Evaluation of factors driving market growth (industrial automation, EV adoption) along with challenges (supply chain constraints, raw material costs).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding strategic opportunities in the evolving optoelectronics ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Gain Optocoupler Market?

-> High Gain Optocoupler Market was valued at 2156 million in 2024 and is projected to reach US$ 4045 million by 2032, at a CAGR of 9.6% during the forecast period.

Which key companies operate in Global High Gain Optocoupler Market?

-> Key players include Vishay, Broadcom, Texas Instruments, On Semiconductor, Renesas, and IXYS Integrated Circuits, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation, electric vehicle adoption, and increasing demand for reliable signal isolation in harsh environments.

Which region dominates the market?

-> Asia-Pacific is the largest market, while North America shows strong growth in automotive and aerospace applications.

What are the emerging trends?

-> Emerging trends include miniaturization of components, integration with smart systems, and development of high-temperature optocouplers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...