High-frequency DC-link film capacitor for SiC inverter Market Insights

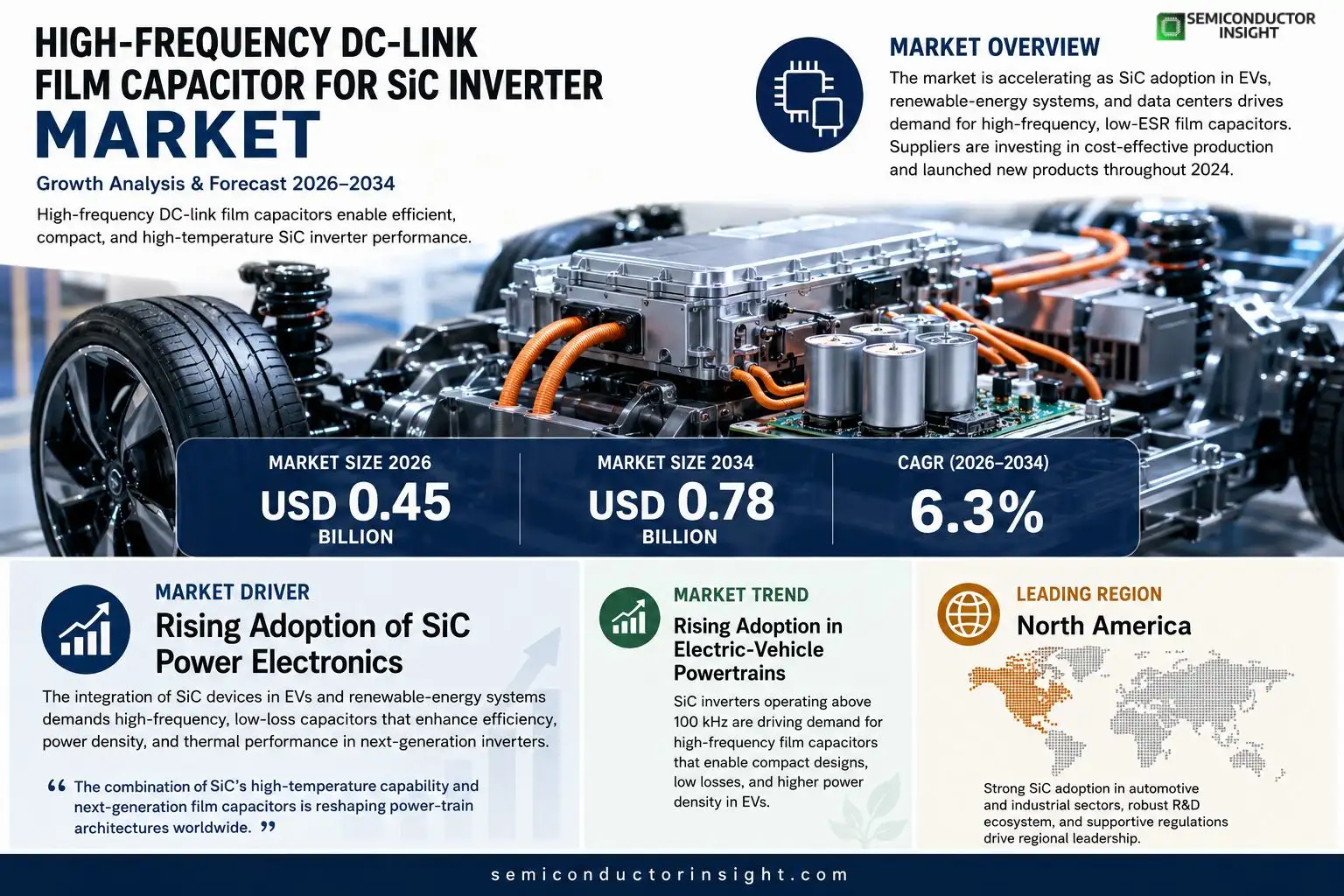

High-frequency DC-link film capacitor for SiC inverter market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.45 billion in 2025 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

High‑frequency DC‑link film capacitors are thin‑film polymer devices designed to operate at switching frequencies above 100 kHz in silicon‑carbide (SiC) inverter topologies. Their low equivalent series resistance (ESR), superior temperature stability up to 200 °C, and compact form factor enable higher power density and improved efficiency in electric‑vehicle drivetrains and renewable‑energy converters.The market is accelerating because automotive manufacturers are rapidly integrating SiC modules into next‑generation EVs, while renewable‑energy installations demand lightweight converters with minimal losses.Furthermore, data‑center power supplies are shifting toward higher switching frequencies to reduce size and cooling requirements.However, the premium cost of advanced film materials remains a barrier; consequently, leading suppliers such as KEMET Corporation, AVX Corp., and Vishay Intertechnology are investing in cost‑effective production lines and have announced new product launches throughout 2024.

MARKET DRIVERS

Rising Adoption of SiC Power Electronics

High-frequency DC-link film capacitor for SiC inverter Market is being propelled by the accelerating integration of silicon‑carbide (SiC) devices in automotive and renewable‑energy applications. SiC inverters deliver higher efficiency and lower thermal losses, which create a clear demand for capacitors that can operate at elevated switching frequencies without performance degradation.

Innovation in Film‑Capacitor Materials

Advances in polymer‑film technology, such as nanocomposite dielectrics, enable capacitors to achieve higher voltage ratings while maintaining low ESR. These material breakthroughs allow designers to reduce inverter size and weight, directly supporting the market’s growth trajectory.

➤ “The combination of SiC’s high‑temperature capability and next‑generation film capacitors is reshaping power‑train architectures worldwide.”

Additionally, regulatory pressure to improve energy‑conversion efficiency in industrial drives is encouraging OEMs to select SiC‑based solutions paired with high‑frequency DC‑link capacitors, further reinforcing market momentum.

MARKET CHALLENGES

Cost Competitiveness with Traditional Capacitors

Although performance advantages are evident, the higher material and processing costs of advanced film capacitors pose a barrier to widespread adoption, especially in price‑sensitive segments such as consumer electronics.

Other Challenges

Supply Chain Constraints

Limited availability of high‑purity polymer films and specialized winding equipment can delay product launches, impacting market entry timelines.Manufacturers must also address long‑term reliability testing to satisfy the rigorous qualification standards demanded by automotive and aerospace customers.

MARKET RESTRAINTS

Technical Integration Barriers

Integrating high‑frequency film capacitors into existing SiC inverter designs often requires redesign of PCB layouts and thermal management schemes, which can increase development cycles and engineering costs.Furthermore, the limited familiarity of many design engineers with the nuanced trade‑offs of film‑capacitor technology may slow acceptance, as conventional electrolytic solutions remain the default choice.Regulatory compliance for high‑voltage applications adds another layer of complexity, requiring extensive testing that can deter smaller players from entering the market.

MARKET OPPORTUNITIES

Expansion in Electric‑Vehicle Powertrains

Electric‑vehicle manufacturers are targeting higher power densities and faster charging capabilities, creating a substantial opportunity for High-frequency DC-link film capacitor for SiC inverter Market to supply next‑generation inverters that meet these performance targets.Parallel growth in renewable‑energy converters, particularly in offshore wind farms where weight and reliability are critical, further expands the addressable market for high‑frequency film capacitors.Strategic partnerships between capacitor producers and SiC device vendors are emerging, enabling co‑development of optimized inverter modules that could unlock new revenue streams and accelerate market penetration.

High-frequency DC-link film capacitor for SiC inverter Market Trends

Rising Adoption in Electric‑Vehicle Powertrains

The transition to silicon‑carbide (SiC) inverter topologies in modern electric vehicles is driving a noticeable shift toward high‑frequency DC‑link film capacitors. Their low equivalent series resistance and ability to operate reliably above 100 kHz enable compact, lightweight designs that meet the efficiency targets of next‑generation drivetrains. Automotive manufacturers are integrating these capacitors to achieve higher power density while maintaining thermal stability up to 200 °C, which translates into longer service life under demanding operating conditions.

Other Trends

Renewable‑Energy Converter Optimization

Wind‑turbine converters and utility‑scale photovoltaic inverters are increasingly specifying high‑frequency film capacitors to reduce overall system mass and improve efficiency. The thin‑film polymer construction minimizes losses at switching frequencies that exceed traditional electrolytic solutions, supporting the push for greener, more compact power conversion equipment in remote installations.

Cost‑Reduction Initiatives by Key Suppliers

While performance advantages are clear, the premium cost of advanced film materials remains a barrier for broader market penetration. Leading manufacturers such as KEMET, AVX, and Vishay have announced investments in cost‑effective production lines and introduced new product families aimed at price‑sensitive segments. These initiatives focus on material engineering and scale‑up of manufacturing processes to bring unit costs closer to those of conventional capacitor types without sacrificing the high‑frequency capabilities essential for SiC applications.Data‑center power supplies represent another emerging segment where the demand for high‑frequency DC‑link film capacitors is growing. By operating at higher switching frequencies, system designers can achieve smaller magnetics and reduced cooling requirements, directly addressing the space and energy constraints typical of large‑scale server farms. The convergence of automotive, renewable‑energy, and data‑center drivers underscores a multi‑industry momentum that is reshaping the capacitor landscape.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑frequency DC‑link film capacitor market for SiC inverters – competitive overview

The market is dominated by a handful of established capacitor specialists that have leveraged thin‑film polymer technology to meet the rigorous ESR, temperature and size requirements of SiC‑based power converters. KEMET Corporation, AVX Corp., and Vishay Intertechnology lead the segment with broad product portfolios, extensive R&D pipelines, and recent 2024 launches targeting automotive EV drivetrains. Their manufacturing scale enables incremental cost reductions, positioning them as primary suppliers for Tier‑1 automotive OEMs and renewable‑energy integrators. These leaders also benefit from strategic partnerships with SiC‑device manufacturers, reinforcing a vertically integrated supply chain that supports high‑volume adoption.Beyond the top tier, a diverse set of niche players contributes specialized designs and regional market coverage. Companies such as TDK (EPCOS), Murata Manufacturing, Taiyo Yuden, Panasonic, Kyocera, Cornell Dubilier, Nissin Electric, Tai‑Rong, KEMET’s European subsidiary, and Infineon’s passive‑component unit are actively expanding their thin‑film capacities. Many focus on ultra‑high‑frequency (>200 kHz) variants or customized form factors for data‑center power supplies and aerospace applications. This fragmented layer drives competitive innovation, with several firms offering cost‑effective alternatives that challenge the incumbents on price‑performance trade‑offs.

List of Key High‑frequency DC‑link Film Capacitor for SiC Inverter Companies Profiled

- KEMET Corporation

- AVX Corp.

- Vishay Intertechnology

- TDK (EPCOS)

- Murata Manufacturing

- Taiyo Yuden

- Panasonic Corporation

- Kyocera International

- Cornell Dubilier Electronics

- Nissin Electric

- Infineon Technologies – Passive Components

- Tai‑Rong Electronics

- AVX Europe GmbH

- ROHM Semiconductor

- Würth Elektronik

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Film Capacitor – Polypropylene offers very low equivalent series resistance, enabling very high switching frequencies; provides outstanding thermal stability up to 200 °C, which is critical for SiC inverter environments; supports a compact form factor that reduces overall system volume and weight, thereby improving power‑density targets for automotive and renewable applications. |

| By Application |

|

Electric‑Vehicle Powertrain relies on the capacitor’s ability to sustain high‑frequency operation while maintaining low heat generation; the tight packaging enables lightweight inverter modules that meet vehicle range and efficiency goals; robust temperature tolerance aligns with the demanding thermal environment of automotive power electronics. |

| By End User |

|

Automotive OEMs value the capacitor’s contribution to higher inverter efficiency and reduced cooling infrastructure; the thin‑film architecture supports tighter packaging constraints inside vehicle power‑train bays; reliability at elevated temperatures aligns with long‑life durability expectations for next‑generation electric vehicles. |

| By Frequency Range |

|

Above 100 kHz is the foundational range where SiC inverter advantages become evident; capacitors operating in this band minimize reactive power loss, thereby enhancing system efficiency; the ability to function reliably at these frequencies allows designers to shrink magnetic components and achieve higher power density. |

| By Market Driver |

|

Efficiency Demands drive adoption because low ESR contributes directly to reduced losses in high‑frequency SiC converters; the resulting lower heat generation eases thermal‑design constraints, which is especially valuable for electric‑vehicle and data‑center applications where energy‑cost considerations dominate purchasing decisions. |

Regional Analysis: High-frequency DC-link film capacitor for SiC inverter Market

North America

Stringent efficiency standards and emissions regulations across the United States and Canada compel manufacturers to adopt SiC inverters, thereby creating a supportive environment for high‑frequency DC‑link film capacitors. Policy incentives and certification programs accelerate market uptake while ensuring component reliability and safety.

An integrated supply chain featuring established film‑capacitor manufacturers, specialized raw‑material suppliers, and logistics providers ensures consistent quality and timely delivery. Close proximity between component makers and OEMs reduces lead times and supports rapid prototyping cycles.

Automotive EV platforms, renewable energy converters, and high‑performance industrial drives are the primary adopters. Each vertical demands capacitors with low ESR, high ripple current capability, and thermal resilience, aligning with the strengths of high‑frequency film technology.

Ongoing research focuses on dielectric material enhancements, miniaturization, and improved voltage rating. Collaborative projects between universities, research institutes, and industry players accelerate the development of next‑generation capacitors tailored for SiC inverter applications.

Europe

Europe’s market for High-frequency DC-link film capacitor for SiC inverter is propelled by aggressive decarbonization targets and substantial investment in electric mobility. Countries such as Germany, France, and the United Kingdom host a dense network of automotive manufacturers and power‑electronics firms that are integrating SiC technology into their product lines. While the region lags slightly behind North America in overall volume, strong governmental subsidies for green transportation and a forward‑looking standards framework foster steady demand. Collaborative research initiatives across the EU support material innovations, positioning Europe as a critical hub for advanced capacitor development and niche market applications.

Asia‑Pacific

The Asia‑Pacific region exhibits rapid growth in High-frequency DC-link film capacitor for SiC inverter Market, driven primarily by China, Japan, and South Korea. Massive production capacity for electric vehicles, combined with aggressive national policies promoting energy‑efficient power electronics, fuels adoption. Local capacitor manufacturers are scaling up capabilities to meet the rising volume requirements while focusing on cost‑effective solutions. Although quality consistency remains a challenge, increasing participation in international standards and joint ventures with Western firms are enhancing technology transfer and market maturity across the region.

South America

South America’s involvement in the High-frequency DC-link film capacitor for SiC inverter sector is emerging, with Brazil and Argentina leading modest adoption in renewable‑energy projects and industrial automation. The region benefits from growing interest in solar and wind integration, where SiC inverters offer higher efficiency. However, limited local production and reliance on imports constrain market expansion. Strategic partnerships with capacitor suppliers and government incentives aimed at modernizing the power grid are expected to gradually improve market penetration over the forecast horizon.

Middle East & Africa

In the Middle East & Africa, demand for High-frequency DC-link film capacitor for SiC inverter is primarily linked to large‑scale solar farms and emerging smart‑grid initiatives. Nations such as the United Arab Emirates and South Africa are investing in SiC‑based power conversion to boost grid reliability and reduce losses. While the market remains relatively small, ongoing infrastructure projects and interest in energy‑storage solutions provide a foothold for future growth. Partnerships with established capacitor manufacturers help bridge the technology gap and introduce advanced film‑capacitor products to regional stakeholders.

Report Scope

This market research report provides a comprehensive analysis of the High-frequency DC-link film capacitor for SiC inverter Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-frequency DC-link film capacitor for SiC inverter Market?

-> High-frequency DC-link film capacitor for SiC inverter Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.78 billion by 2034.

Which key companies operate in High-frequency DC-link film capacitor for SiC inverter Market?

-> Key players include KEMET Corporation, AVX Corp., Vishay Intertechnology, among others.

What are the key growth drivers?

-> Key growth drivers include rapid integration of SiC modules in electric‑vehicle powertrains, rising demand for lightweight high‑frequency converters in renewable‑energy installations, and data‑center power supplies shifting toward higher switching frequencies to reduce size and cooling requirements.

Which region dominates the market?

-> Regional dominance information is not specified in the provided data.

What are the emerging trends?

-> Emerging trends include development of higher‑frequency thin‑film capacitors for improved power density, expansion of SiC‑based inverter applications in EVs and renewable energy, and cost‑reduction initiatives for advanced film materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...