Market Insights

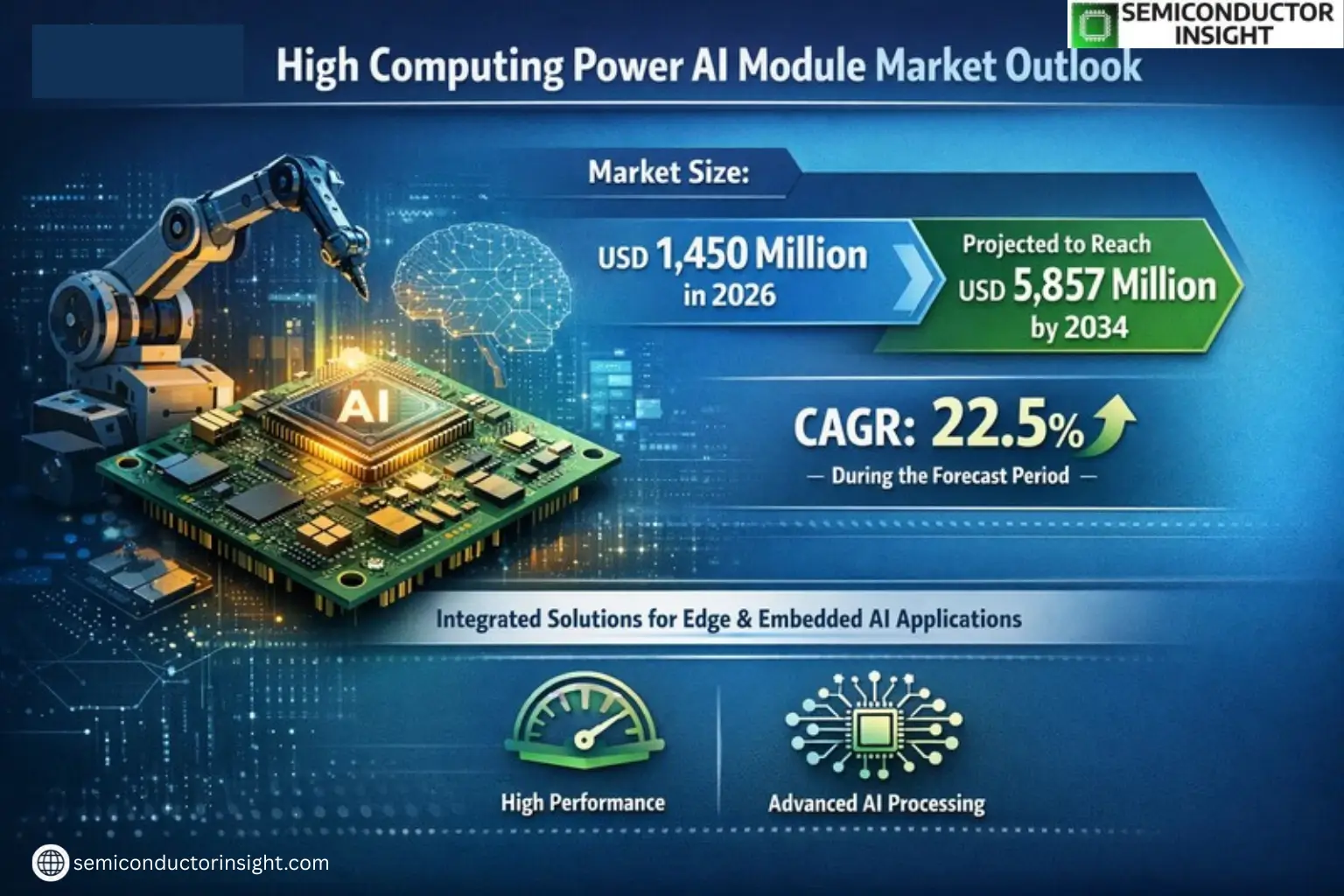

Global High Computing Power AI Module Market was valued at USD 1,450 million in 2026 and is projected to reach USD 5,857 million by 2034, exhibiting a CAGR of 22.5% during the forecast period.

High Computing Power AI Modules are integrated computing solutions designed for edge and embedded artificial intelligence applications requiring superior performance compared to traditional IoT or communication modules. These modules combine multi-core CPUs, GPUs, and/or NPUs with on-board memory, multimedia engines, and high-speed interfaces in compact form factors such as system-on-module (SoM) designs. They serve critical roles in industrial edge AI, robotics, intelligent transportation systems, smart cities, and advanced video analytics applications.

The market demonstrates strong growth momentum with global production reaching approximately 3.75 million units in 2024 at an average price point of USD 350 per unit. This expansion is primarily driven by accelerating adoption of edge AI across industrial and commercial sectors. Key product segments include Ultra-High Computing Power (100+ TOPS), High Computing Power (50-100 TOPS), and Mid-High Computing Power (20-50 TOPS) modules that cater to diverse performance requirements across different application verticals.

MARKET DRIVERS

Increasing Demand for Edge AI Processing

High Computing Power AI Module Market is experiencing rapid growth due to the rising adoption of edge AI processing. Industries such as autonomous vehicles, robotics, and smart manufacturing require real-time decision-making capabilities. These applications demand high-performance AI modules with low latency and energy efficiency.

Advancements in Semiconductor Technology

Breakthroughs in semiconductor design, including 5nm and 3nm chip fabrication, have enabled the development of more powerful and energy-efficient AI modules. Major players are investing heavily in R&D to create specialized AI accelerators. This technological progress is directly fueling market expansion.

Growing adoption across healthcare for medical imaging analysis and drug discovery is creating new use cases for high-performance AI modules with specialized processing capabilities.

MARKET CHALLENGES

Thermal Management and Power Consumption

High Computing Power AI Modules generate significant heat while operating at peak performance levels. Effective thermal dissipation solutions add to the overall system cost and complexity, creating engineering challenges for compact applications.

Other Challenges

Supply Chain Constraints

The semiconductor shortage has impacted production timelines for AI modules, with lead times for advanced GPUs and TPUs extending beyond 30 weeks in some cases.

MARKET RESTRAINTS

High Development Costs

The R&D investment required to design and manufacture High Computing Power AI Modules creates significant barriers to entry. Smaller players face challenges competing with established semiconductor firms that dominate the market with vertically integrated solutions.

MARKET OPPORTUNITIES

5G and IoT Integration

The rollout of 5G networks is creating new opportunities for high-performance AI modules in distributed computing architectures. These modules enable intelligent processing at network edges, reducing latency for mission-critical applications in industrial automation and smart cities.

High Computing Power AI Module Market Trends

Explosive Growth in Edge AI Deployment Driving Market Expansion

Global High Computing Power AI Module Market is experiencing rapid growth, projected to expand from USD 1.45 billion in 2026 to USD 5.86 billion by 2034, representing a 22.5% CAGR. This surge is primarily fueled by accelerating adoption across industrial automation, smart city infrastructure, and robotics applications that require localized processing power. The market recorded production of 3,750 thousand units in 2024 at an average price point of USD 350 per unit.

Other Trends

Increasing Demand for Ultra-High Performance Modules

The segment delivering over 100 TOPS (Tera Operations Per Second) is gaining prominence as applications like autonomous vehicles and advanced robotics require real-time decision-making capabilities. This represents a shift from traditional embedded systems toward AI-optimized modular solutions with substantial neural processing power.

Supply Chain Evolution for AI-Optimized Components

Module manufacturers are increasingly dependent on advanced semiconductor nodes (5nm and below) for AI-specific SOCs, creating supply chain challenges but enabling significant performance gains. The BOM structure shows 60-70% of costs attributed to processors and memory components, with vendors differentiating through thermal solutions and software stack optimizations.

Vertical Integration Across Industrial Applications

System integrators are standardizing on High Computing Power AI Modules for machine vision, predictive maintenance, and autonomous material handling. The industrial sector now accounts for 42% of module deployments, benefiting from the combination of rugged form factors and cloud-comparable AI performance at the edge.

Competitive Landscape and Technology Roadmap

Leading vendors are focusing on performance-per-watt metrics while maintaining support for mainstream AI frameworks. The market is transitioning toward unified development environments that simplify deployment across different module performance tiers, from entry-level (10-20 TOPS) to ultra-high performance systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Alliances Define the AI Module Market

NVIDIA Corporation dominates the high computing power AI module sector with its Jetson AGX Orin series, offering unparalleled performance up to 275 TOPS for edge AI applications. The market exhibits an oligopolistic structure where five companies collectively control over 60% of global shipments. Intel follows closely through its Habana Gaudi accelerators and Movidius VPUs, benefiting from vertical integration with its foundry operations. Semiconductor leaders are increasingly adopting chiplet designs and 5nm/7nm process nodes to enhance module performance while managing thermal constraints.

Emerging challengers like Hailo Technologies and Blaize are disrupting the market with specialized AI architectures optimized for edge deployment. Chinese players such as Horizon Robotics and Cambricon Technologies have gained significant traction in domestic markets through government-supported smart city initiatives. The mid-range segment (20-50 TOPS) has become fiercely competitive, with module vendors differentiating through software stacks, power efficiency, and customized support services for industrial customers.

List of Key High Computing Power AI Module Companies Profiled

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies

- AMD (Xilinx)

- Hailo Technologies

- Blaize

- Horizon Robotics

- Cambricon Technologies

- MediaTek

- Renesas Electronics

- Rockchip

- Huawei (Ascend)

- Samsung Semiconductor

- NXP Semiconductors

- Google (Coral)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High Computing Power (50-100 TOPS) modules are emerging as the industry sweet spot:

|

| By Application |

|

Industrial Automation represents the most mature application segment:

|

| By End User |

|

System Integrators are the primary adopters:

|

| By Form Factor |

|

System-on-Module (SoM) dominates in professional applications:

|

| By Cooling Method |

|

Hybrid Cooling solutions are gaining traction:

|

Regional Analysis: High Computing Power AI Module Market

The United States accounts for over 60% of North America’s High Computing Power AI Module demand, with California’s tech ecosystem driving cutting-edge developments in neural network processors and AI accelerators for cloud computing and autonomous systems.

Financial institutions and healthcare organizations in the region are aggressively implementing high-performance AI modules for fraud detection, risk analysis, and medical imaging, creating sustained demand for specialized computing solutions.

North America’s university research programs in AI hardware receive substantial funding, with institutions like MIT and Stanford pioneering novel architectures for high-performance AI computation, fueling continuous market innovation.

Defense and intelligence applications are spurring specialized AI module development, with DARPA and other agencies investing heavily in next-generation computing architectures for national security applications.

Asia-Pacific

The Asia-Pacific region exhibits the fastest growth in High Computing Power AI Module adoption, driven by expanding data center infrastructure and government-led digital transformation programs. China leads regional investments in domestic AI chip development, with technology parks in Shenzhen and Shanghai becoming hotspots for AI hardware innovation. South Korea and Japan maintain strong positions in semiconductor manufacturing for AI applications, while India’s growing IT sector creates new demand for AI acceleration solutions. The region benefits from increasing cloud service provider investments and local manufacturing capabilities for AI-specific processors.

Europe

Europe maintains a strong position in the High Computing Power AI Module Market with balanced growth across industrial and research applications. Germany’s automotive industry drives demand for AI modules in autonomous vehicle development, while France and the UK concentrate on healthcare and financial applications. The EU’s AI Act framework encourages ethical development of high-performance computing solutions. Leading semiconductor firms in the region focus on energy-efficient AI processors, aligning with sustainability goals, while academic collaborations support specialized AI hardware research.

Middle East & Africa

The Middle East is emerging as a strategic market for High Computing Power AI Modules, particularly in smart city and oil/gas applications. Gulf nations are investing heavily in AI infrastructure, with UAE’s AI strategy creating demand for advanced computing solutions. Africa shows growing potential as connectivity improves, with South Africa and Nigeria establishing initial footholds in AI adoption. The region benefits from increasing data center construction and government initiatives to develop local AI capabilities.

South America

South America demonstrates steady growth in High Computing Power AI Module adoption, led by Brazil and Argentina. Banking and agriculture sectors drive initial demand for AI solutions, while government digital transformation programs create infrastructure opportunities. The region faces challenges in local semiconductor production but benefits from cloud service expansion and increasing tech startup investments in AI-driven applications across various industries.

Report Scope

This market research report provides a comprehensive analysis of the High Computing Power AI Module Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High Computing Power AI Module Market?

-> High Computing Power AI Module Market was valued at USD 1,450 million in 2026 and is projected to reach USD 5,857 million by 2034, exhibiting a CAGR of 22.5% during the forecast period.

What are High Computing Power AI Modules?

-> High Computing Power AI Modules are integrated computing modules designed for edge and embedded AI applications, featuring multi-core CPUs, GPUs/NPUs, on-board memory, multimedia engines, and high-speed interfaces in compact form factors like system-on-module (SoM).

What was the production volume in 2024?

-> Global production reached approximately 3,750 thousand units in 2024, with an average market price of around USD 350 per unit.

What are the key applications of these modules?

-> They are widely deployed in industrial edge AI, robotics, intelligent transportation systems, smart cities, and advanced video analytics.

What drives the market growth?

-> Key growth drivers include rapid adoption of edge AI across industrial and commercial sectors, increasing demand for AI-capable hardware, and advancements in semiconductor technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...