Healthcare AI Chip Market Insights

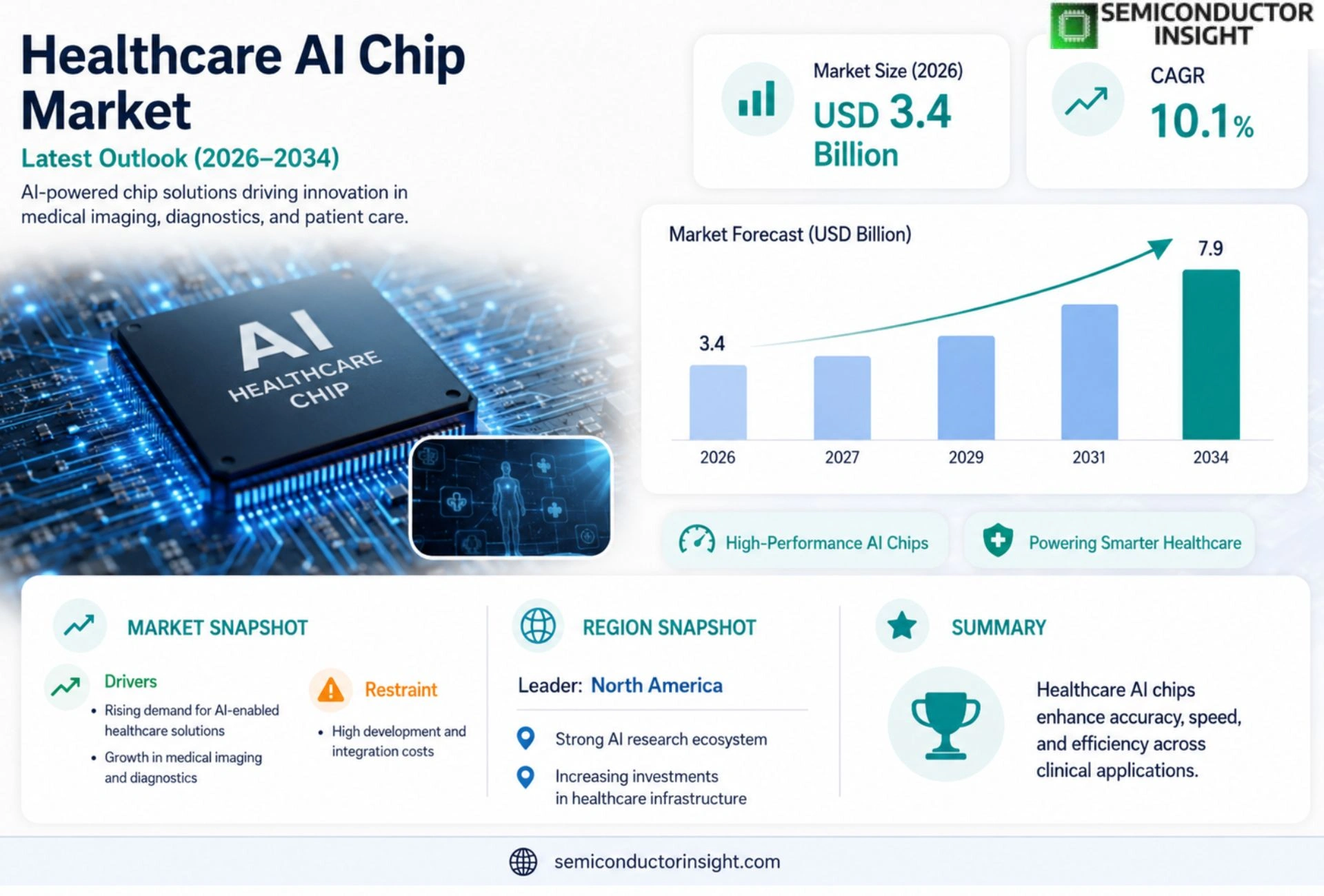

Global Healthcare AI Chip market size was valued at USD 3.2 billion in 2025. The market is projected to grow from USD 3.4 billion in 2026 to USD 7.9 billion by 2034, exhibiting a CAGR of 10.1% during the forecast period.

Healthcare AI chips are specialized semiconductor devices optimized for executing deep‑learning models on medical data such as imaging scans, electronic health records, and genomic sequences. They combine high‑throughput tensor cores, low‑latency inference engines, and energy‑efficient architectures to accelerate diagnostic analytics, patient monitoring, and drug discovery.

The market is experiencing rapid growth due to rising investment in digital health, expanding use of AI‑driven radiology and pathology tools, and increasing demand for edge computing within hospitals. Furthermore, regulatory encouragement for AI‑based diagnostics and strategic collaborations,such as NVIDIA’s partnership with Siemens Healthineers announced in March 2023,are fueling expansion. Key players including NVIDIA Corporation, Intel Corporation (Habana Labs), Qualcomm Technologies Inc., AMD Inc., and Google Cloud (TPU) are actively developing next‑generation healthcare AI chips.

MARKET DRIVERS

Rising Demand for Real‑Time Diagnostics

Healthcare providers are increasingly adopting AI‑powered edge chips to accelerate imaging analysis, leading to faster diagnosis and reduced patient wait times. Healthcare AI Chip market, this trend translates into a projected compound annual growth rate of over 20% through 2030.

Regulatory Support for Advanced AI Devices

Recent policy revisions in major economies streamline the clearance process for AI‑driven medical hardware, encouraging manufacturers to invest in specialized chips. This regulatory momentum is a key catalyst for expanding Healthcare AI Chip market across hospitals and research centers.

➤ More than 65% of leading hospitals plan to integrate AI chips into their imaging suites by 2027.

Combined, these drivers create a robust ecosystem where technology vendors, healthcare institutions, and government bodies align toward faster, more accurate patient care powered by AI hardware.

MARKET CHALLENGES

Integration Complexity Across Legacy Systems

Many healthcare facilities operate on legacy IT infrastructures that are not optimized for high‑throughput AI processing. Deploying new AI chips often requires extensive system redesign, leading to longer implementation cycles and higher upfront costs Healthcare AI Chip market.

Other Challenges

Data Privacy Concerns

Stringent patient‑data protection regulations limit the flow of clinical data to AI algorithms, constraining the ability of chip manufacturers to train and validate models on real‑world datasets.

MARKET RESTRAINTS

High Development and Certification Costs

The design, testing, and regulatory certification of medical‑grade AI chips involve substantial financial outlays. These cost barriers restrict entry for smaller firms and slow the overall momentum of Healthcare AI Chip market.

MARKET OPPORTUNITIES

Emerging Edge AI Applications in Remote Care

Telemedicine and home‑based monitoring are rapidly expanding, creating demand for low‑power, on‑device AI chips that can analyze vital signs locally. This shift opens a high‑growth niche for Healthcare AI Chip market, especially in rural and underserved regions.

Healthcare AI Chip Market Trends

Accelerating Adoption of Edge AI in Clinical Settings

Healthcare providers are moving AI processing from centralized data centers to the point of care, embedding specialized chips directly into imaging consoles, bedside monitors, and portable diagnostic devices. These edge‑oriented solutions deliver sub‑second inference for tasks such as real‑time MRI anomaly detection, instantaneous triage alerts from vital‑sign streams, and on‑device segmentation of histopathology slides. By eliminating reliance on high‑bandwidth network connections, hospitals achieve lower latency, reduced operational costs, and compliance with patient‑data privacy regulations. Energy‑efficient architectures further extend battery life for mobile units, supporting continuous AI assistance in remote or emergency environments while maintaining clinical accuracy.

Other Trends

Strategic Partnerships Driving Innovation

Collaboration between semiconductor leaders and medical technology firms is reshaping the development pipeline for Healthcare AI Chip market. High‑profile alliances, such as the 2023 joint effort between a premier AI chip manufacturer and a global imaging equipment company, have produced integrated platforms that combine ultra‑fast tensor cores with proprietary diagnostic algorithms. Parallel initiatives see Intel’s Habana Labs aligning with hospital IT vendors, Qualcomm delivering low‑power vision processors for point‑of‑care ultrasound, and Google Cloud’s TPU solutions being piloted for large‑scale genomic analyses. These partnerships accelerate time‑to‑market, pool R&D resources, and generate a cohesive ecosystem that blends hardware excellence with clinical expertise.

Expansion of AI‑Powered Drug Discovery Platforms

The pharmaceutical segment is increasingly leveraging the computational strengths of Healthcare AI Chip market to shorten drug‑development cycles. Chips optimized for deep‑learning inference enable rapid processing of massive genomic and proteomic datasets, allowing researchers to identify viable molecular targets in days rather than weeks. On‑premise high‑performance clusters equipped with these chips support confidential data handling while delivering accelerated model training for predictive toxicity and efficacy profiling. As a result, biotech firms are integrating AI‑enhanced pipelines into early‑stage discovery, fostering more precise candidate selection and reducing reliance on traditional high‑throughput screening methods.

COMPETITIVE LANDSCAPE

Key Industry Players

Healthcare AI Chip market Is Shaped by a Concentrated Group of Semiconductor Giants and Emerging Specialized Chipmakers Competing on Performance, Power Efficiency, and Clinical Integration Capabilities

Healthcare AI Chip market is dominated by a handful of large-scale semiconductor and technology corporations that have made substantial investments in AI-optimized hardware tailored for medical applications. NVIDIA Corporation leads the competitive landscape with its GPU-based platforms , particularly the A100 and H100 tensor core architectures , which have been widely adopted across medical imaging, genomics, and clinical decision support systems. The company’s strategic collaboration with Siemens Healthineers, announced in March 2023, further reinforced its foothold in the healthcare AI infrastructure space by integrating NVIDIA’s computing capabilities into advanced radiology and diagnostics workflows. Intel Corporation, through its Habana Labs subsidiary, competes directly with purpose-built AI inference and training processors, while Google Cloud continues to expand its Tensor Processing Unit (TPU) ecosystem into healthcare-specific AI workloads, particularly for large-scale diagnostic analytics and drug discovery pipelines. Qualcomm Technologies Inc. and AMD Inc. are also gaining notable traction, with Qualcomm leveraging its edge AI expertise for in-hospital and point-of-care monitoring devices, and AMD advancing its Instinct GPU series for high-performance medical data processing.

Beyond the dominant tier, a growing number of specialized and emerging players are carving out significant positions Healthcare AI Chip market by targeting niche clinical use cases, edge deployment scenarios, and energy-efficient inference at the device level. Companies such as Arm Holdings provide foundational chip architectures widely adopted by medical device manufacturers building custom AI silicon. Graphcore has gained recognition for its Intelligence Processing Unit (IPU) technology, which demonstrates strong performance in neural network training relevant to biomedical research. Cerebras Systems has positioned its wafer-scale engine as a breakthrough solution for large AI model training in genomics and drug discovery. Samsung Electronics and Micron Technology contribute through advanced memory and storage semiconductor solutions that are integral to healthcare AI chip performance. Additionally, startups and fabless design firms including Mythic AI and BrainChip Holdings are advancing analog compute and neuromorphic chip architectures respectively, offering low-power AI inference suited for wearable health monitors and implantable diagnostic devices. The competitive intensity across the market is expected to escalate as healthcare providers increasingly prioritize on-premises and edge AI deployments to address data privacy, latency, and regulatory compliance requirements.

List of Key Healthcare AI Chip Companies Profiled

- NVIDIA Corporation

- Intel Corporation (Habana Labs)

- Google Cloud (Tensor Processing Unit)

- Qualcomm Technologies Inc.

- AMD Inc.

- Arm Holdings

- Samsung Electronics Co., Ltd.

- Micron Technology Inc.

- Graphcore Ltd.

- Cerebras Systems Inc.

- Mythic AI

- BrainChip Holdings Ltd.

- Siemens Healthineers AG

- IBM Corporation

- Huawei Technologies Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASICs

|

| By Application |

|

Diagnostic Imaging

|

| By End User |

|

Hospitals & Clinics

|

| By Deployment Model |

|

Edge Devices

|

| By Integration Level |

|

Integrated SoCs

|

Regional Analysis: North America

North America

The primary drivers for Healthcare AI Chip market in North America include growing healthcare expenditure, increasing prevalence of chronic diseases, and the rising demand for precision medicine. Advancements in edge computing and 5G technology are also facilitating the deployment of AI solutions in healthcare settings.

Key trends shaping the market in North America involve the development of specialized AI chips for specific medical applications, the increasing adoption of federated learning for data privacy, and the integration of AI with wearable devices for remote patient monitoring. Focus on cybersecurity within healthcare AI systems is also gaining prominence.

The competitive landscape in North America is characterized by the presence of established semiconductor companies, AI chip startups, and collaborative partnerships between technology providers and healthcare organizations. Companies are focused on developing innovative AI chip architectures, optimizing power consumption, and ensuring compliance with stringent regulatory requirements.

Challenges include data security concerns, regulatory hurdles, and the need for skilled personnel. Opportunities lie in the development of AI solutions for drug discovery, personalized medicine, and robotic surgery.

Europe

Europe represents a significant and expanding market for Healthcare AI Chip market. Driven by government initiatives promoting digital health and healthcare innovation, the region is witnessing increasing investment in AI-powered medical technologies. The focus on data privacy regulations, such as GDPR, presents both a challenge and an opportunity for companies operating in this space. Key areas of application include medical imaging analysis, diagnostics, and drug development. Collaboration between academic institutions and industry players is fostering innovation in AI chip design and development. This region exhibits a strong emphasis on ethical considerations and responsible AI implementation within the healthcare sector. The demand for Healthcare AI Chip Market solutions is projected to grow steadily throughout the forecast period, supported by a growing elderly population and increasing healthcare costs.

Asia-Pacific

The Asia-Pacific region is poised for substantial growth Healthcare AI Chip market. Countries like China, Japan, and South Korea are investing heavily in AI and healthcare, creating a fertile ground for market expansion. The increasing prevalence of chronic diseases and a growing middle class are further driving demand. Government support for technological advancements and the availability of skilled labor are key factors contributing to this growth. The adoption of AI in medical imaging and diagnostics is particularly strong in this region. However, challenges remain in terms of data standardization and regulatory harmonization. The Asia-Pacific Healthcare AI Chip Market is expected to experience the highest growth rate during the forecast period, fueled by rapid economic development and increasing healthcare awareness.

South America

South America presents a developing market for Healthcare AI Chip market. While adoption is currently lower compared to North America and Europe, the region offers considerable potential for growth. Increasing healthcare investments and a growing awareness of AI’s capabilities in medical applications are key drivers. The focus is on leveraging AI for improving access to healthcare in underserved areas. Challenges include limited technological infrastructure and regulatory complexities. The market is expected to gradually expand as healthcare systems embrace digital transformation and AI-powered solutions.

Middle East & Africa

The Middle East and Africa represent emerging markets for Healthcare AI Chip market. With growing healthcare expenditure and increasing government initiatives to modernize healthcare infrastructure, the region is witnessing a gradual adoption of AI technologies. The focus is on leveraging AI for improving diagnostic accuracy and optimizing healthcare delivery in resource-constrained settings. Challenges include limited access to advanced technologies and a shortage of skilled personnel. However, the market is projected to experience significant growth in the coming years as healthcare investments continue to rise and AI adoption becomes more widespread.

Report Scope

This market research report provides a comprehensive analysis of the Healthcare AI Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Healthcare AI Chip Market?

-> Healthcare AI Chip market was valued at USD 3.2 billion in 2025 and is expected to reach USD 7.9 billion by 2034.

Which key companies operate Healthcare AI Chip market?

-> Key players include NVIDIA Corporation, Intel Corporation (Habana Labs), Qualcomm Technologies Inc., AMD Inc., and Google Cloud (TPU).

What are the key growth drivers?

-> Key growth drivers include rising investment in digital health, expanding use of AI‑driven radiology and pathology tools, increasing demand for edge computing in hospitals, regulatory encouragement for AI‑based diagnostics, and strategic collaborations such as NVIDIA’s partnership with Siemens Healthineers.

Which region dominates the market?

-> Global market activity is widespread, and the source does not indicate a single region dominating Healthcare AI Chip market.

What are the emerging trends?

-> Emerging trends include edge‑computing AI solutions for point‑of‑care devices, deeper integration of AI with electronic health records, collaborative R&D partnerships between chip makers and medical equipment manufacturers, and increased regulatory support for AI‑based diagnostic platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...