MARKET INSIGHTS

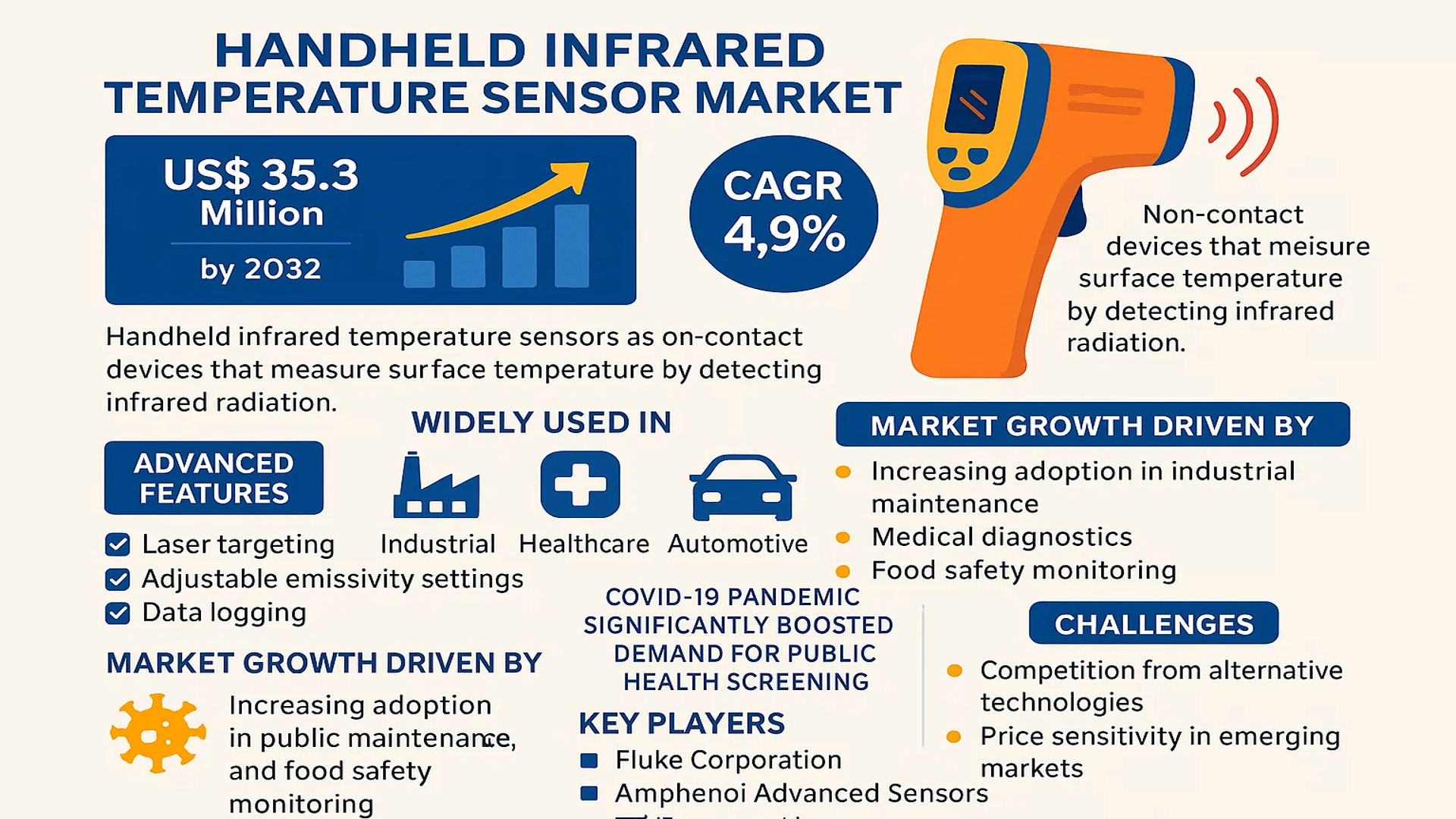

The global Handheld Infrared Temperature Sensor Market was valued at 35.3 million in 2024 and is projected to reach US$ 48.9 million by 2032, at a CAGR of 4.9% during the forecast period.

Handheld infrared temperature sensors are non-contact devices that measure surface temperature by detecting infrared radiation. These portable devices are widely used in industrial, healthcare, and automotive applications due to their accuracy, speed, and ease of use. Advanced models feature laser targeting, adjustable emissivity settings, and data logging capabilities.

The market growth is driven by increasing adoption in industrial maintenance, medical diagnostics, and food safety monitoring. The COVID-19 pandemic significantly boosted demand for these sensors in public health screening. However, competition from alternative technologies and price sensitivity in emerging markets pose challenges. Key players like Fluke Corporation, Amphenol Advanced Sensors, and TE Connectivity dominate the market with continuous product innovations.

MARKET DYNAMICS

MARKET DRIVERS

Surge in Demand for Non-Contact Temperature Measurement Solutions to Drive Market Growth

The handheld infrared temperature sensor market is witnessing significant growth due to the rising demand for non-contact temperature measurement solutions across various industries. This demand was particularly accelerated during the COVID-19 pandemic, where infrared thermometers became essential tools for mass fever screening. While the pandemic has subsided, the adoption of these devices continues to expand in healthcare, industrial, and consumer applications. The global market, valued at $35.3 million in 2024, is projected to grow at a 4.9% CAGR, reaching $48.9 million by 2032. The increasing awareness about hygiene and the need for quick, accurate temperature readings are fueling this sustained demand.

Industrial Automation and Smart Manufacturing to Boost Adoption

Industrial sectors are increasingly adopting infrared temperature sensors as part of automation and predictive maintenance strategies. These devices play a critical role in monitoring equipment temperature without interrupting production processes. In manufacturing plants, they help prevent equipment failure by detecting abnormal heat patterns early. The automotive industry, which accounts for approximately 23% of market share, relies heavily on these sensors for quality control in paint curing, welding processes, and engine testing. Furthermore, the integration of IoT with infrared sensors enables real-time monitoring and data analysis, creating smart factory environments that optimize operational efficiency.

Technological Advancements Enhancing Product Capabilities

Recent technological innovations are significantly improving the accuracy, range, and functionality of handheld infrared temperature sensors. Advanced models now offer features like Bluetooth connectivity, data logging, and improved emissivity correction. The introduction of dual-laser targeting systems has enhanced measurement precision, while miniaturization has made devices more portable and user-friendly. Leading manufacturers are investing heavily in R&D, with some devices now achieving accuracy levels within ±1°C or 1% of reading. These technological improvements are expanding application possibilities and driving adoption across new verticals, including food processing and building diagnostics.

MARKET RESTRAINTS

Accuracy Limitations in Certain Conditions to Hinder Market Expansion

While handheld infrared temperature sensors offer numerous advantages, their accuracy can be compromised by various environmental factors. These devices may provide unreliable readings when measuring reflective surfaces, through glass or steam, or when the target object’s emissivity is unknown. In industrial settings where precise temperature measurement is critical, these limitations can pose significant challenges. For instance, in metal processing applications where surface reflectivity varies, measurement errors can exceed 5-10%, potentially affecting product quality and process control. This accuracy limitation restricts their use in applications requiring high-precision measurements, forcing some industries to rely on more expensive contact measurement alternatives.

High Competition and Price Pressure to Impact Profit Margins

The market is characterized by intense competition, with over 50 major manufacturers globally competing on price, features, and brand reputation. This competition has led to significant price erosion, particularly in the lower-end consumer segment. While this benefits buyers, it puts pressure on manufacturers’ profit margins, potentially limiting investment in innovation. The situation is further exacerbated by the influx of low-cost products from emerging markets, some of which may compromise on quality to maintain competitive pricing. Established players are responding by focusing on premium, feature-rich models for industrial and professional applications where price sensitivity is lower.

Regulatory Compliance and Standardization Challenges

The lack of global standardization in infrared temperature measurement protocols creates challenges for manufacturers and users alike. Different industries and regions have varying requirements for accuracy, calibration, and performance verification. Medical-grade devices face particularly stringent regulations, with certifications like FDA 510(k) adding to development costs and timelines. Compliance with evolving safety and electromagnetic compatibility standards requires continuous product updates and testing. These regulatory hurdles can delay product launches and increase costs, particularly for smaller manufacturers looking to enter new geographic markets or application segments.

MARKET CHALLENGES

Maintaining Measurement Accuracy Across Diverse Applications

One of the most significant challenges facing the industry is ensuring consistent measurement accuracy across the wide range of surfaces and materials encountered in different applications. The emissivity factor, which varies from 0.1 for polished metals to 0.95 for most organic materials, significantly impacts measurement reliability. While advanced algorithms and multi-spectral technologies are being developed to address this challenge, achieving universal accuracy remains complex. This issue is particularly pronounced in mixed-material environments common in industrial settings, where measurement errors can lead to incorrect process decisions or quality control failures.

Battery Life and Power Management Limitations

Handheld infrared temperature sensors often struggle with power management, particularly for models incorporating advanced features like color displays and wireless connectivity. While basic models may operate for several months on standard batteries, more sophisticated devices might require daily charging in heavy-use scenarios. This limitation affects field applications where consistent power sources may not be available. Manufacturers are addressing this challenge through low-power electronics and efficient battery technologies, but balancing functionality with extended operation time remains an ongoing engineering challenge that impacts user experience and product design.

Educating End-Users on Proper Measurement Techniques

Despite their apparent simplicity, infrared temperature sensors require proper technique and understanding to obtain accurate measurements. Common user errors include incorrect distance-to-spot ratios, improper angle of measurement, and failure to account for environmental factors. Industry surveys suggest that up to 30% of measurement inaccuracies can be attributed to operator error rather than device limitations. Manufacturers face the dual challenge of designing intuitive interfaces while also providing comprehensive training materials. This education gap represents a significant barrier to realizing the full potential of infrared temperature measurement technology across all user segments.

MARKET OPPORTUNITIES

Integration with IoT and Industry 4.0 to Create New Applications

The convergence of infrared temperature sensing with IoT platforms presents substantial growth opportunities. Smart sensors equipped with wireless connectivity can provide continuous monitoring solutions for equipment health and process control. In predictive maintenance applications, these devices can detect abnormal temperature patterns before failures occur, potentially reducing downtime by up to 50%. The integration with cloud platforms enables data analytics and trend monitoring across multiple locations. Major industrial players are increasingly incorporating these smart solutions into their digital transformation strategies, creating new revenue streams for sensor manufacturers through value-added services.

Expansion in Emerging Markets to Drive Volume Growth

Developing economies in Asia, Latin America, and Africa represent significant untapped potential for handheld infrared temperature sensors. Rapid industrialization, coupled with increasing healthcare expenditure in these regions, is creating new demand for cost-effective temperature measurement solutions. The Asia-Pacific market alone is projected to grow at 6.2% CAGR, outpacing the global average. Local manufacturing and tailored product offerings for price-sensitive segments can help companies capitalize on this growth. Government initiatives to modernize healthcare infrastructure and improve industrial safety standards are further accelerating adoption in these emerging markets.

Development of Specialized Solutions for Niche Applications

There is growing opportunity in developing specialized infrared temperature sensors tailored to specific industry needs. For instance, the food industry requires devices with hygienic designs and rapid response times for processing line monitoring. The energy sector needs ruggedized models capable of measuring high temperatures in hazardous environments. Medical applications demand clinical-grade accuracy with features like fever screening algorithms. By focusing on these niche segments, manufacturers can differentiate their offerings and command premium pricing. The development of application-specific firmware and accessories further enhances product value and creates opportunities for recurring revenue through software updates and calibration services.

HANDHELD INFRARED TEMPERATURE SENSOR MARKET TRENDS

Rising Demand for Non-Contact Temperature Measurement to Drive Market Growth

The increasing adoption of non-contact temperature measurement solutions across multiple industries has become a primary driver for the handheld infrared temperature sensor market. The technology has witnessed exponential growth, particularly in healthcare and industrial applications, where safety and efficiency are critical. During the COVID-19 pandemic, infrared thermometers became ubiquitous in public screening, reinforcing their importance in real-time health monitoring. Furthermore, advancements in sensor accuracy—delivering an error margin as low as ±0.5°C—along with laser targeting enhancements, have significantly improved reliability, widening their usage in critical environments such as manufacturing and automotive diagnostics.

Other Trends

Integration of Smart Features in Handheld Devices

The incorporation of IoT and wireless connectivity in handheld infrared sensors is reshaping market dynamics. Modern devices now feature Bluetooth and Wi-Fi-enabled data transmission, allowing seamless integration with cloud-based monitoring systems. This has been particularly beneficial in industrial automation, where remote temperature logging is essential for predictive maintenance. Additionally, companies such as Fluke Corporation and Melexis have introduced models with ergonomic design improvements and multi-spectral infrared sensing, contributing to better user experience and broader applications.

Industrial Automation and Predictive Maintenance Fueling Adoption

Industrial sectors, particularly automotive and electronics manufacturing, are increasingly relying on handheld infrared sensors for predictive maintenance and quality control. These devices help detect overheating in machinery components before failure, reducing downtime and maintenance costs. The industrial segment accounted for over 35% of global market revenue in 2024, and this figure is expected to grow further as smart factories and Industry 4.0 initiatives gain momentum. Emerging economies in Asia-Pacific have shown particularly strong demand due to rapid industrialization and increased investments in automation technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Leadership in Handheld IR Sensors

The global handheld infrared temperature sensor market exhibits a moderately fragmented yet competitive structure, with established industrial players competing alongside specialized manufacturers. Fluke Corporation emerged as the dominant player in 2024, commanding approximately 18% of the market share due to its extensive distribution network and reputation for high-precision measurement tools. The company’s latest FLUKE-62 MAX+ model, featuring ±1% accuracy and IP54 ruggedness, has become an industry benchmark for industrial applications.

European semiconductor manufacturers STMicroelectronics and Melexis collectively held nearly 22% market share in 2024, capitalizing on their integrated MEMS sensor solutions. Their growth has been particularly strong in automotive applications, where IR temperature monitoring is becoming critical for battery management in electric vehicles.

The pandemic-induced demand surge created opportunities for agile players like Tecpel and Amphenol Advanced Sensors, who rapidly scaled production of medical-grade infrared thermometers. Both companies expanded their manufacturing capacities by 40-60% during 2020-2022 to meet urgent healthcare requirements, establishing lasting footholds in the clinical segment.

Recent industry movements include TE Connectivity‘s 2023 acquisition of First Sensor AG, strengthening its position in industrial IR sensing, while NXP Semiconductors is investing heavily in AI-enabled predictive temperature monitoring systems. Such strategic developments suggest increasing vertical integration across the value chain.

List of Prominent Handheld Infrared Sensor Companies

- Fluke Corporation (U.S.)

- Tecpel Co., Ltd. (Taiwan)

- Amphenol Advanced Sensors (U.S.)

- Melexis NV (Belgium)

- Texas Instruments (U.S.)

- Microchip Technology Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- TE Connectivity (Switzerland)

- Hamamatsu Photonics (Japan)

- Siemens AG (Germany)

- STMicroelectronics (Switzerland)

Segment Analysis:

By Type

Non-contact Type Segment Dominates Due to COVID-19-Driven Demand for Hygienic Temperature Measurement

The market is segmented based on type into:

- Contact Type

- Subtypes: Thermocouples, Resistance Temperature Detectors (RTDs), and others

- Non-contact Type

- Subtypes: Fixed-point infrared, Thermal imaging, and others

- Hybrid Type

- Others

By Application

Healthcare Segment Maintains Dominance with Rising Demand for Medical Grade Temperature Monitoring

The market is segmented based on application into:

- Healthcare

- Subtypes: Patient monitoring, Fever screening, Medical device components

- Industrial

- Subtypes: Equipment monitoring, Quality control, Process measurement

- Automotive

- Subtypes: Engine temperature monitoring, Climate control systems

- Consumer Electronics

- Others

By Measurement Range

Standard Range Segment Leads with Widespread Application Across Multiple Industries

The market is segmented based on measurement range into:

- Low Range (-50°C to 50°C)

- Standard Range (-30°C to 300°C)

- High Range (Above 300°C)

- Others

By Accuracy Level

Medical Grade Segment Shows Strong Growth Due to Increasing Quality Standards

The market is segmented based on accuracy level into:

- Industrial Grade (±1°C or more)

- Standard Grade (±0.5°C to ±1°C)

- Medical Grade (±0.2°C or better)

- Others

Regional Analysis: Handheld Infrared Temperature Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the global handheld infrared temperature sensor market, holding over 38% market share in 2024. China leads regional demand due to massive manufacturing operations and stringent healthcare safety measures implemented post-pandemic. Key growth drivers include rapid industrialization in Southeast Asia and India’s expanding automotive sector, where temperature monitoring is critical for quality control. However, price sensitivity creates competition among mid-range and budget sensor manufacturers, with local brands gaining traction against established global players. The healthcare sector’s adoption of non-contact thermometers continues to rise, particularly in countries like Japan and South Korea which prioritize advanced medical equipment.

North America

North America represents the second-largest market, valued at $12.7 million in 2024, with the U.S. accounting for 82% of regional demand. Strict workplace safety regulations from OSHA and advanced healthcare infrastructure drive adoption across industrial and medical applications. The market shows preference for high-accuracy sensors with data logging capabilities, particularly in pharmaceutical and aerospace sectors. Post-pandemic, enterprises continue utilizing infrared thermometers for employee health monitoring, sustaining demand despite the initial surge having subsided. Canadian market growth remains steady, supported by oil & gas and mining industries requiring ruggedized temperature measurement solutions.

Europe

European demand focuses on precision sensors complying with EU medical device regulations (MDR) and industrial safety standards. Germany and France lead adoption, with the automotive sector representing 31% of regional sensor applications. The market shows strong preference for German-engineered devices, though cost-competitive alternatives from Eastern Europe are gaining traction. Environmental monitoring applications are emerging as a growth segment, particularly in Nordic countries tracking climate-related temperature variations. The post-pandemic market normalized after 2022, but healthcare facilities maintain stockpiles of infrared thermometers as part of emergency preparedness protocols.

South America

Market growth in South America remains constrained by economic volatility, though Brazil and Argentina show steady demand from food processing and industrial maintenance sectors. The region demonstrates preference for mid-range sensors balancing accuracy and affordability. Public health initiatives drive sporadic demand spikes, particularly during disease outbreaks, but lack of sustained healthcare funding limits market expansion. Chile and Colombia emerge as promising markets due to growing mining operations requiring equipment temperature monitoring solutions.

Middle East & Africa

The MEA market shows divergent trends – Gulf nations prioritize advanced medical and industrial sensors, while African markets remain price-driven. UAE and Saudi Arabia lead regional adoption, with temperature screening remaining prevalent at transport hubs and healthcare facilities. Oil-rich nations invest in high-end sensors for refinery operations, whereas sub-Saharan Africa relies on basic models for agriculture and rudimentary industrial applications. Market potential exists in urbanizing African cities, though infrastructure limitations and import dependence hinder growth rates compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Handheld Infrared Temperature Sensor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 35.3 million in 2024 and is projected to reach USD 48.9 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Contact vs. Non-contact), application (Automotive, Healthcare, Industrial, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading manufacturers including Fluke Corporation, Amphenol Advanced Sensors, and STMicroelectronics, covering their product portfolios and strategic developments.

- Technology Trends: Assessment of innovations in IR sensing, integration with IoT platforms, and improvements in measurement accuracy and range.

- Market Drivers: Analysis of factors including post-pandemic demand for contactless measurement and industrial automation growth.

- Stakeholder Insights: Strategic guidance for sensor manufacturers, distributors, and industrial end-users navigating this evolving market.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and actionable insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Handheld Infrared Temperature Sensor Market?

-> Handheld Infrared Temperature Sensor Market was valued at 35.3 million in 2024 and is projected to reach US$ 48.9 million by 2032, at a CAGR of 4.9% during the forecast period.

Which companies lead the Handheld IR Sensor market?

-> Key players include Fluke Corporation, Amphenol Advanced Sensors, STMicroelectronics, TE Connectivity, and NXP Semiconductors.

What are the primary applications?

-> Major applications include industrial maintenance (32% share), healthcare (28%), automotive (22%), and other sectors.

Which region shows strongest growth?

-> Asia-Pacific leads with 38% market share in 2024, driven by manufacturing growth in China and India.

What are key technology trends?

-> Emerging trends include AI-powered temperature analytics, Bluetooth-enabled sensors, and miniaturized designs for portable applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...