MARKET INSIGHTS

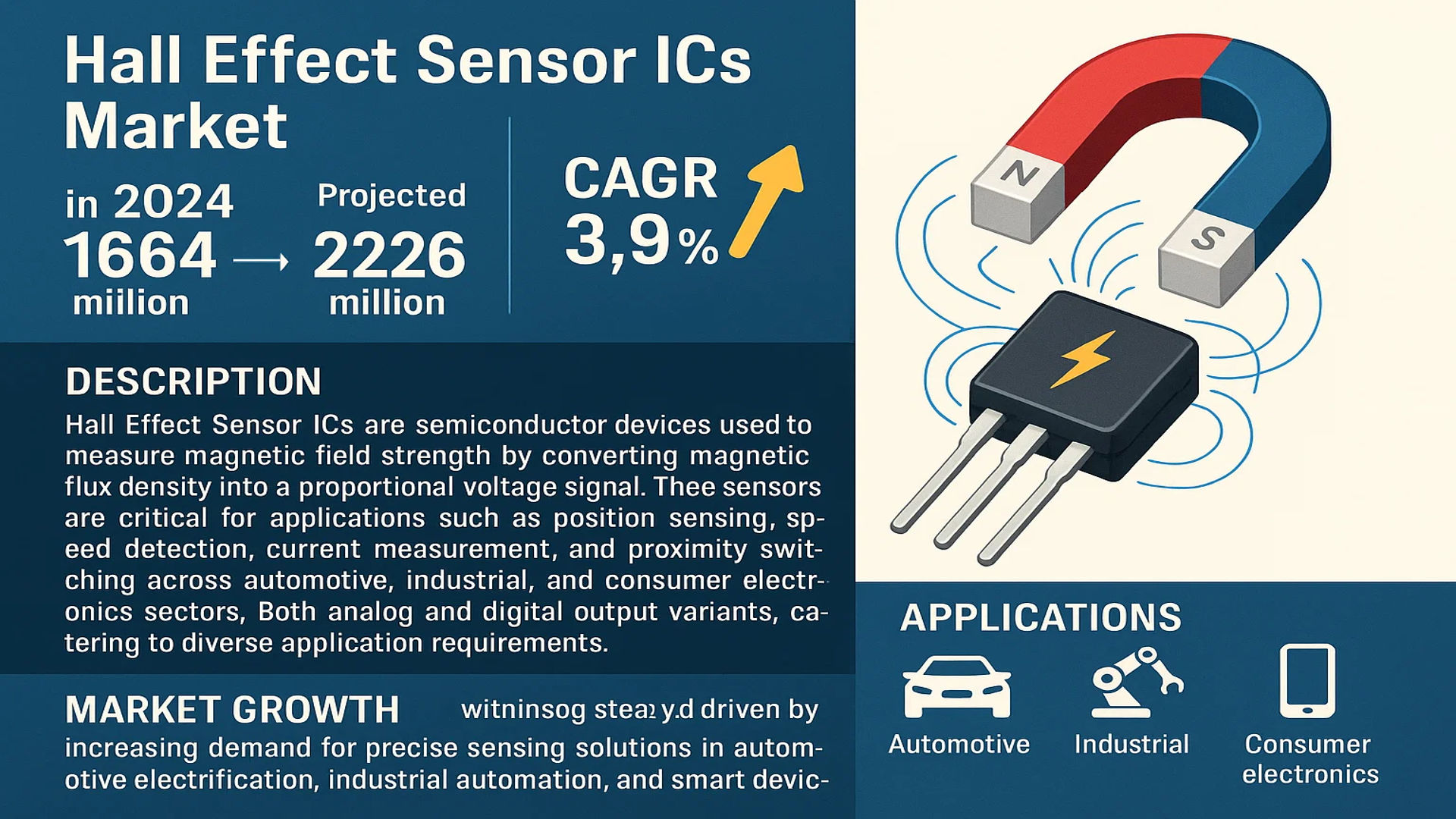

The global Hall Effect Sensor ICs market was valued at 1664 million in 2024 and is projected to reach US$ 2226 million by 2032, at a CAGR of 3.9% during the forecast period.

Hall Effect Sensor ICs are semiconductor devices used to measure magnetic field strength by converting magnetic flux density into a proportional voltage signal. These sensors are critical for applications such as position sensing, speed detection, current measurement, and proximity switching across automotive, industrial, and consumer electronics sectors. The market offers both analog and digital output variants, catering to diverse application requirements.

The market is witnessing steady growth driven by increasing demand for precise sensing solutions in automotive electrification, industrial automation, and smart devices. The proliferation of electric vehicles (EVs) and renewable energy systems is creating new opportunities, as Hall sensors are essential for motor control and power management. Major players like Allegro MicroSystems, Infineon, and TDK dominate the market, leveraging their technological expertise to develop high-performance, energy-efficient solutions. Recent innovations focus on integrated signal processing and miniaturization for IoT applications.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Automotive Electronics Sector to Accelerate Hall Effect Sensor IC Adoption

The automotive industry’s rapid technological transformation is generating substantial demand for Hall Effect Sensor ICs. Modern vehicles incorporate over 200 sensors in powertrain, chassis, and infotainment systems, with magnetic sensors representing approximately 15% of the total sensor count. Electric vehicle production, projected to grow at 22% CAGR through 2030, particularly drives this demand as Hall sensors provide critical current monitoring and position detection in battery management systems. Major automotive chip manufacturers have reported 28% year-over-year growth in magnetic sensor shipments as automakers prioritize safety and efficiency features.

Industrial Automation Boom Creating New Growth Frontiers

Industry 4.0 implementations are reshaping manufacturing floor requirements, with Hall Effect Sensor IC shipments for industrial applications growing at 9.3% annually. These components enable precise position detection in robotic arms, speed monitoring in conveyor systems, and current measurement in motor drives. The global industrial sensors market, valued at $21 billion in 2023, increasingly relies on magnetic sensing solutions that offer reliability in harsh environments. Brushless DC motor adoption in industrial equipment, forecast to grow by $4.2 billion through 2027, particularly benefits from the non-contact nature and durability of Hall-based position sensors.

Consumer Electronics Miniaturization Pushing Innovation

Smartphone manufacturers integrate Hall sensors for flip cover detection and compass functionality, with over 1.5 billion units shipped annually containing at least one magnetic sensor. The trend toward thinner wearables and foldable devices drives demand for compact, low-power sensor ICs that consume less than 2μA in standby mode. Recent advancements in 3D Hall technology enable precise angle measurement in joysticks and VR controllers, opening new application possibilities. The global MEMS sensor market expansion, expected to reach $30 billion by 2026, is closely tied to Hall effect component innovations that meet size and power constraints.

MARKET CHALLENGES

Precision and Stability Requirements Creating Technical Hurdles

While Hall Effect Sensor ICs offer numerous advantages, maintaining micron-level accuracy across temperature variations remains an engineering challenge. Temperature drift can cause up to 0.5% measurement error per degree Celsius in standard devices, requiring complex compensation circuits. Automotive qualification standards such as AEC-Q100 mandate operation across -40°C to +150°C ranges, pushing development costs 30-40% higher than commercial-grade components. The need for factory-programmed sensitivity trimming adds production complexity, with foundry lead times extending to 18 weeks for specialized magnetic sensor processes.

Other Challenges

Supply Chain Complexities

Geopolitical factors and semiconductor allocation priorities have created volatility in rare-earth material supplies essential for magnetic sensing elements. The 2022-2023 chip shortage particularly impacted sensor supply, with lead times peaking at 52 weeks for certain Hall effect variants. Automotive OEMs now require dual-source qualification for all sensing components, adding 6-9 months to product development cycles.

Legacy System Integration

Modern digital-output Hall sensors face compatibility issues with older analog control systems still prevalent in industrial environments. Retrofit solutions require additional signal conditioning circuits that increase total solution costs by 12-15%, slowing adoption in price-sensitive applications.

MARKET RESTRAINTS

Alternative Sensing Technologies Creating Competitive Pressure

Magnetoresistive (MR) sensors are gaining traction in precision applications, offering 10x better sensitivity than traditional Hall elements. The MR sensor market is projected to grow at 8.1% CAGR through 2028, particularly in automotive safety systems where detection ranges exceed 20mm. Optical encoders continue dominating high-accuracy position sensing, maintaining 65% market share in robotics despite higher costs. Emerging technologies like inductive and capacitive sensing provide contactless alternatives in some current measurement applications, though with tradeoffs in linearity and temperature performance.

Cost Sensitivity in Mature Applications Limiting Upside

Standard Hall switches for low-cost consumer applications face intense pricing pressure, with ASPs declining 3-5% annually. Mature markets like white goods and power tools demonstrate strong resistance to price increases, forcing manufacturers to achieve 5-8% annual cost reductions through wafer size migrations and package optimizations. The industrial sector shows similar cost sensitivity in basic position detection applications, where Hall sensors compete directly with mechanical switches that offer 70-80% cost savings.

MARKET OPPORTUNITIES

Next-Generation Electric Vehicle Platforms Opening New Design-Ins

Automotive OEMs developing 800V architectures require current sensors with enhanced isolation capabilities, creating opportunities for advanced Hall and fluxgate hybrid solutions. The transition to zone-based E/E architectures in vehicles will drive 25% more sensor content per car by 2027, with redundant sensing becoming standard for safety-critical functions. Battery management systems in next-gen EVs demand current measurement accuracy below 0.1%, pushing adoption of precision Hall sensors with integrated signal conditioning.

Industrial IoT Deployment Expanding Sensing Requirements

Predictive maintenance systems require condition monitoring sensors that can operate for years on battery power, creating demand for ultra-low-power Hall ICs with wake-on-event functionality. The industrial wireless sensor network market is forecast to exceed $1.5 billion by 2026, with magnetic sensors playing a key role in vibration and position monitoring applications. Smart building implementations increasingly utilize Hall-effect-based airflow and valve position sensors that offer longer lifespans than mechanical alternatives.

Medical Device Innovation Leveraging Contactless Sensing

Implantable medical devices increasingly incorporate Hall sensors for position detection in drug delivery systems and prosthetic controls, benefiting from the technology’s immunity to fluid exposure. The medical sensor market is projected to grow at 8.9% CAGR through 2028, with magnetic sensing playing a critical role in miniaturized diagnostic equipment. Recent FDA clearances for Hall-based surgical navigation systems demonstrate the technology’s potential in advanced medical applications requiring sub-millimeter accuracy.

HALL EFFECT SENSOR ICS MARKET TRENDS

Rising Demand in Automotive and Industrial Applications

The global Hall Effect Sensor ICs market is experiencing robust growth driven by increasing adoption in automotive and industrial applications. The automotive sector, in particular, accounts for over 35% of total Hall Effect Sensor ICs demand, primarily due to their crucial role in electric vehicles (EVs) and advanced driver-assistance systems (ADAS). These sensors enable precise position sensing in brushless DC (BLDC) motors, throttle control, and transmission systems, with the EV market alone expected to drive 25% year-on-year growth in sensor demand through 2032. Similarly, industrial automation applications, including robotics and motor control systems, are leveraging Hall Effect Sensor ICs for their non-contact sensing capabilities and durability in harsh environments.

Other Trends

Expansion of Smart Consumer Electronics

The proliferation of smart devices is creating new opportunities for Hall Effect Sensor ICs manufacturers. Smartphones, wearables, and IoT devices increasingly incorporate these sensors for functions like flip detection, screen rotation, and power management. The consumer electronics segment currently represents nearly 28% of market revenue, with projections indicating this share could grow as 5G-enabled devices and foldable smartphones gain wider adoption. Emerging applications in smart home appliances, particularly in position sensing for motorized components, are further broadening the addressable market for these components.

Technological Advancements Driving Market Evolution

Significant technological innovations are reshaping the Hall Effect Sensor ICs landscape. Leading manufacturers are focusing on developing integrated solutions that combine sensing elements with signal processing circuitry, reducing system complexity and board space requirements. The market is witnessing rapid adoption of digital output sensors, which now account for approximately 45% of new designs, offering advantages in noise immunity and direct microcontroller interfacing. Furthermore, advancements in low-power designs are enabling energy-efficient operation for battery-powered IoT devices, with some modern sensors consuming less than 10μA in active mode. These innovations are critical as end-users demand higher precision, lower power consumption, and smaller form factors across all application segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership

The global Hall Effect Sensor ICs market features a highly concentrated competitive landscape, dominated by established electronics and semiconductor manufacturers primarily headquartered in the United States, Europe, and Japan. Allegro MicroSystems leads the market with an estimated 22% revenue share in 2024, owing to its comprehensive product portfolio covering both analog and digital output sensors for automotive and industrial applications.

European semiconductor giants Infineon Technologies and NXP Semiconductors collectively hold approximately 30% of the market, benefiting from their strong foothold in automotive electronics. Both companies are actively expanding their product lines to include more integrated solutions combining Hall Effect sensing with advanced signal processing capabilities, particularly for electric vehicle applications where reliability and precision are critical.

Meanwhile, Japanese competitors TDK Corporation and Asahi Kasei Microdevices continue to strengthen their positions through technological differentiation. TDK’s recent introduction of ultra-low power Hall sensors for IoT devices demonstrates this strategic emphasis, while Asahi Kasei has been focusing on high-temperature resistant variants for industrial automation systems.

The competitive environment is intensifying as Chinese manufacturers like Suzhou Novosense Microelectronics and Shanghai Orient-Chip Technology aggressively expand their market presence. These companies are gaining traction in domestic markets and starting to compete internationally through cost-competitive offerings for consumer electronics applications.

List of Key Hall Effect Sensor IC Companies Profiled

- Allegro MicroSystems (U.S.)

- Infineon Technologies (Germany)

- TDK Corporation (Japan)

- Asahi Kasei Microdevices (Japan)

- NXP Semiconductors (Netherlands)

- Melexis (Belgium)

- ams OSRAM (Austria)

- Texas Instruments (U.S.)

- Diodes Incorporated (U.S.)

- Suzhou Novosense Microelectronics (China)

- Honeywell (U.S.)

- TE Connectivity (Switzerland)

Segment Analysis:

By Type

Analog Output Hall Sensors Hold Significant Market Share Owing to Wide-Ranging Industrial Applications

The market is segmented based on type into:

- Analog Output Hall Sensor

- Subtypes: Linear output, ratiometric output, and others

- Digital Output Hall Sensor

- Subtypes: Bipolar, unipolar, omnipolar, and others

By Application

Automotive and Transportation Sector Dominates Due to Rising Adoption in EVs and ADAS Systems

The market is segmented based on application into:

- Consumer Electronics

- Industrial and Energy

- Automotive and Transportation

- Others

By Technology

Bipolar Technology Gaining Traction for Precision Current Sensing Applications

The market is segmented based on technology into:

- Bipolar Hall Effect Sensors

- Unipolar Hall Effect Sensors

- Omnipolar Hall Effect Sensors

Regional Analysis: Hall Effect Sensor ICs Market

Asia-Pacific

Asia-Pacific dominates the Hall Effect Sensor ICs market, accounting for over 40% of global demand in 2024. China’s robust electronics manufacturing sector, Japan’s precision engineering expertise, and India’s growing automotive industry drive this leadership. The region benefits from concentrated production facilities of key players like Asahi Kasei Microdevices and TDK, along with aggressive adoption in electric vehicles and industrial automation. Smartphone manufacturers increasingly integrate Hall sensors for flip/cover detection, while government initiatives supporting Industry 4.0 and renewable energy create sustained demand. Chinese suppliers like Suzhou Novosense Microelectronics are gaining traction with cost-competitive solutions, though quality differentiation remains a challenge compared to established international brands.

North America

North America’s market thrives on technological innovation and stringent automotive safety standards. The U.S. accounts for nearly 75% of regional demand, with Allegro MicroSystem and Texas Instruments leading development of high-reliability sensor ICs for electric vehicles and aerospace applications. The Infrastructure Investment Act has accelerated smart grid deployments utilizing Hall-based current sensors, while robotics adoption in manufacturing pushes demand for precision position sensors. Cybersecurity concerns in automotive applications are driving demand for tamper-resistant sensor designs with embedded encryption—a key differentiator for North American suppliers. The region maintains premium pricing power due to its focus on high-performance, application-specific integrated solutions.

Europe

Europe’s strong automotive OEM base and renewable energy focus sustain demand for specialized Hall sensor ICs. Germany’s industrial sector accounts for 30% of regional consumption, integrating sensors into Industry 4.0 automation systems. Companies like Infineon and NXP dominate the automotive segment with AEC-Q100 qualified sensors for ADAS and powertrain systems. The EU’s strict electromagnetic compatibility (EMC) directives compel manufacturers to develop low-noise sensor architectures. However, recent energy price volatility has pressured mid-tier industrial adopters to delay sensor upgrades. The region shows growing interest in spin-Hall effect sensors for next-generation memory applications, though commercialization remains limited to niche research projects.

South America

Market growth in South America remains constrained by economic instability, though Brazil’s automotive resuscitation program shows promise. Most demand stems from aftermarket automotive parts and basic industrial equipment, favoring cost-sensitive analog Hall sensors from Asian suppliers. Local assembly of consumer electronics in Mexico has spurred some regional demand, but import dependency on finished sensor ICs persists. The lack of domestic semiconductor fabrication limits technological advancement, with applications largely confined to basic speed sensing and position detection. Recent trade agreements may improve access to advanced sensor technologies, particularly for Argentina’s renewable energy sector.

Middle East & Africa

This emerging market shows potential through infrastructure-led growth, particularly in smart city projects across the UAE and Saudi Arabia. While current adoption focuses on basic building automation and HVAC systems, planned EV manufacturing hubs in Morocco could drive future demand. South Africa’s mining sector utilizes ruggedized Hall sensors for equipment monitoring, though political uncertainty hampers long-term investments. The region heavily depends on imports, with distribution channels dominated by European and Asian suppliers. Localized testing and calibration services are emerging as value-added differentiators to overcome the technical support gap in the region.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Hall Effect Sensor ICs markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Hall Effect Sensor ICs market was valued at USD 1664 million in 2024 and is projected to reach USD 2226 million by 2032, growing at a CAGR of 3.9%.

- Segmentation Analysis: Detailed breakdown by product type (Analog Output Hall Sensor, Digital Output Hall Sensor), application (Consumer Electronics, Industrial and Energy, Automotive and Transportation, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates with 45% market share, followed by Europe and North America.

- Competitive Landscape: Profiles of leading market participants including Allegro MicroSystem, Infineon, TDK, NXP, and Asahi Kasei Microdevices, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies including higher integration, low-power designs for IoT devices, smarter functionalities with digital output and self-calibration, and enhanced reliability for extreme conditions.

- Market Drivers & Restraints: Evaluation of factors driving market growth including demand from automotive electronics and industrial automation, along with challenges such as supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the Hall Effect Sensor ICs market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Hall Effect Sensor ICs Market?

-> Hall Effect Sensor ICs market was valued at 1664 million in 2024 and is projected to reach US$ 2226 million by 2032, at a CAGR of 3.9% during the forecast period.

Which key companies operate in Global Hall Effect Sensor ICs Market?

-> Key players include Allegro MicroSystem, Infineon, Asahi Kasei Microdevices, TDK, NXP, Melexis, ams OSRAM, Texas Instruments, and Honeywell, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand from automotive electronics (EVs, motor control), industrial automation (BLDC motors, robotics), and expanding applications in consumer electronics and renewable energy sectors.

Which region dominates the market?

-> Asia-Pacific is the largest market with 45% share, driven by electronics manufacturing in China, Japan, and South Korea, while Europe and North America lead in automotive and industrial applications.

What are the emerging trends?

-> Emerging trends include higher integration with embedded signal processing, low-power designs for IoT, digital output with self-calibration, and enhanced reliability for automotive and industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...