MARKET INSIGHTS

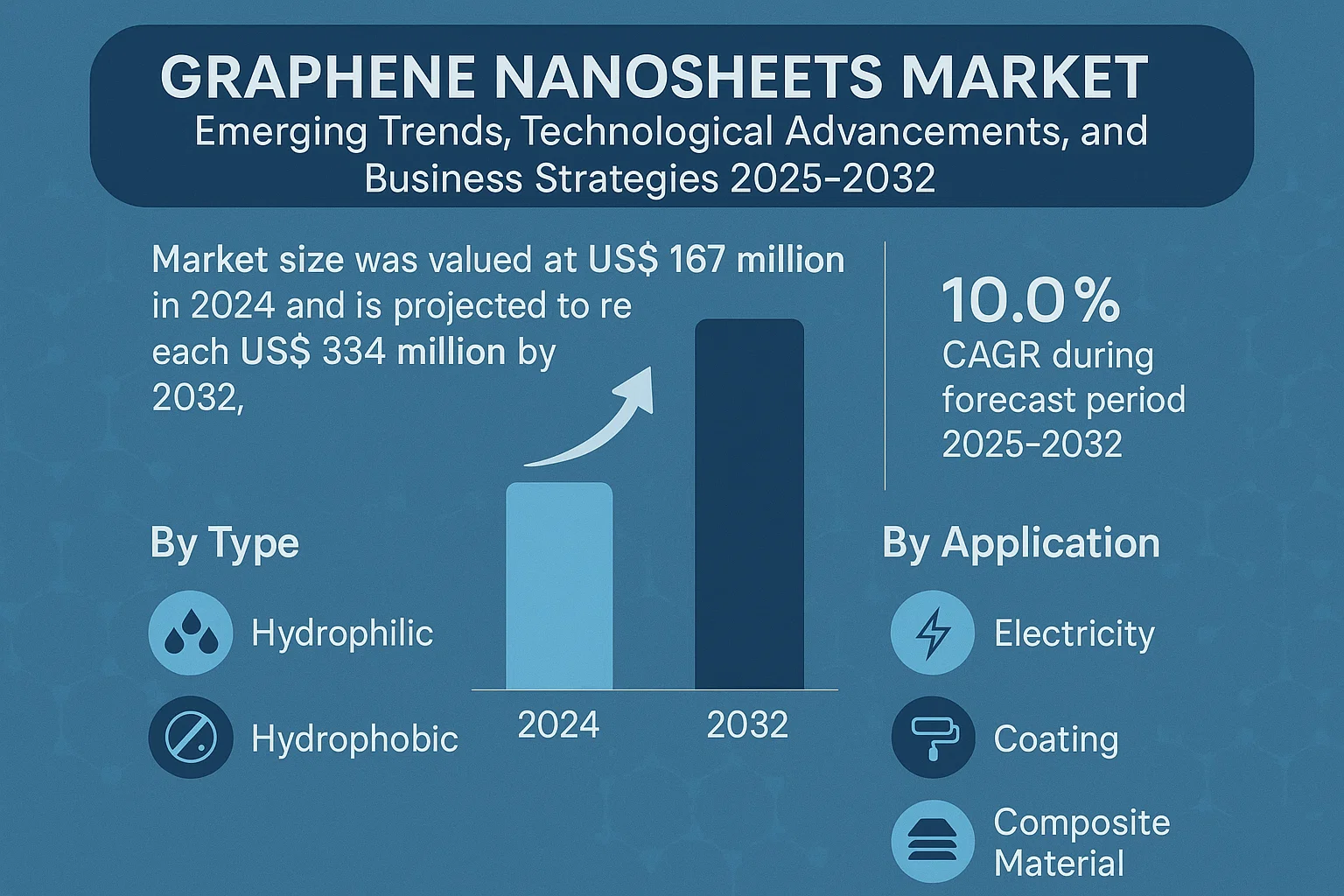

The global Graphene Nanosheets Market size was valued at US$ 167 million in 2024 and is projected to reach US$ 334 million by 2032, at a CAGR of 10.0% during the forecast period 2025-2032. The U.S. market size is estimated at USD 42.1 million in 2024, while China is projected to reach USD 98.3 million by 2032.

Graphene nanosheets are ultra-thin, two-dimensional carbon nanostructures with exceptional mechanical, electrical, and thermal properties. These materials typically measure 1-10 atomic layers thick and demonstrate unique characteristics including high surface area (2630 m²/g), extraordinary conductivity (10⁸ S/m), and remarkable tensile strength (130 GPa). The product exists in both hydrophilic and hydrophobic variants, catering to diverse industrial applications.

The market growth is primarily driven by increasing demand from electronics, energy storage, and composite material sectors. However, production scalability remains a challenge due to high manufacturing costs averaging USD 100-200 per gram for high-quality nanosheets. Key players like CVD Equipment and Applied Graphene Materials are investing in novel production methods such as chemical vapor deposition (CVD) and electrochemical exfoliation to reduce costs by 30-40% over the next five years.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Electronics Sector to Fuel Demand for Graphene Nanosheets

The electronics industry’s relentless pursuit of smaller, faster, and more efficient components is driving significant adoption of graphene nanosheets. With exceptional electrical conductivity—nearly 100 times greater than copper—graphene nanosheets are revolutionizing semiconductor manufacturing. Recent advancements in flexible electronics and quantum computing have further amplified demand, with market analysts noting a 40% year-on-year growth in conductive material applications. Leading manufacturers are increasingly incorporating graphene-based solutions into transistors, sensors, and energy storage devices to meet performance benchmarks.

Environmental Regulations Accelerating Adoption in Coatings Industry

Stringent environmental policies worldwide are compelling coating manufacturers to transition toward sustainable solutions. Graphene nanosheets enhance coating performance while reducing volatile organic compound (VOC) emissions by up to 70% compared to traditional materials. The anticorrosive coating segment alone has witnessed a doubling of graphene adoption rates since 2023, particularly in marine and industrial applications where durability and environmental compliance are paramount. This regulatory push, combined with graphene’s superior barrier properties, positions it as a transformative material in protective coatings.

The energy sector’s transition toward sustainable solutions presents another major growth avenue. Graphene nanosheets improve battery energy density by approximately 30%, addressing critical limitations in electric vehicle performance.

➤ Specialized graphene-enhanced batteries now demonstrate charge cycles exceeding 2,000 while maintaining 90% capacity, a breakthrough that accelerates EV adoption.

MARKET RESTRAINTS

High Production Costs Limit Widespread Commercialization

While graphene nanosheets offer unparalleled performance benefits, their market penetration faces substantial cost barriers. Current production methods require specialized equipment and controlled environments, with manufacturing costs remaining 5-8 times higher than conventional materials. Small and medium enterprises particularly struggle with these economic realities, as the initial capital expenditure for graphene integration often exceeds operational budgets. Even large corporations carefully evaluate return on investment timelines, which frequently extend beyond three years for full-scale implementation.

Other Restraints

Quality Consistency Challenges

Batch-to-batch variability in nanosheet morphology and purity poses significant hurdles for manufacturers. Strict quality thresholds—particularly for electronics-grade graphene—result in yield rates below 60% for many producers, directly impacting profitability and scalability.

Regulatory Uncertainty

Evolving safety classifications for nanomaterials create compliance complexities. Jurisdictional disparities in graphene handling standards force multinational corporations to maintain multiple production protocols, increasing operational overheads by an estimated 15-20%.

MARKET CHALLENGES

Material Integration Complexities Hinder Application Development

Successful incorporation of graphene nanosheets into existing material systems remains technically challenging. Many composite manufacturers report interfacial bonding issues between graphene and matrix materials, reducing potential performance gains by up to 40%. The material’s tendency to restack in polymer composites necessitates specialized dispersion techniques that add processing steps and costs. These technical obstacles delay product development cycles and discourage potential adopters despite the material’s theoretical advantages.

Additionally, the global graphene talent shortage exacerbates these technical challenges. Specialized know-how in nanomaterial processing remains concentrated among a small pool of experts, with demand for qualified engineers outpacing supply by nearly 3:1 as of 2024.

MARKET OPPORTUNITIES

Emerging Biomedical Applications Create New Growth Frontiers

The healthcare sector presents transformative opportunities for graphene nanosheets, particularly in targeted drug delivery and biosensing. Recent clinical trials demonstrate graphene-based neural interfaces achieving 300% improvement in signal resolution compared to conventional materials. Advancements in functionalized graphene for cancer treatment show particularly strong promise, with preclinical studies reporting tumor reduction rates exceeding 70% in certain carcinoma models when combined with photothermal therapy.

Strategic partnerships between material scientists and medical researchers are accelerating commercialization timelines. Joint ventures have reduced typical development cycles from seven to under four years for graphene-enhanced medical devices, creating lucrative opportunities for early-mover companies.

➤ The global medical graphene market segment is projected to grow at 45% CAGR through 2030, substantially outpacing industrial applications.

Meanwhile, sustainability initiatives are unlocking novel opportunities in environmental remediation. Graphene oxide membranes demonstrate 99.9% contaminant removal efficiency in water treatment applications, positioning the technology as a potential game-changer for addressing global water scarcity challenges.

GRAPHENE NANOSHEETS MARKET TRENDS

Expanding Electronics Applications Driving Market Growth

The global graphene nanosheets market is witnessing substantial growth due to increasing adoption in flexible electronics and energy storage applications. Graphene’s exceptional electrical conductivity – 100 times faster than silicon – combined with its mechanical flexibility makes it ideal for next-generation electronic devices. Over 35% of graphene patents filed in 2023 focused on electronics applications, indicating strong industry focus. Flexible displays utilizing graphene nanosheets are projected to capture over 20% of the display market by 2030. Furthermore, graphene-enhanced lithium-ion batteries demonstrate 50% faster charging times while maintaining higher energy density compared to conventional batteries.

Other Trends

Composite Materials Revolution

Composites reinforced with graphene nanosheets are transforming multiple industries by offering unprecedented strength-to-weight ratios. Automotive manufacturers are increasingly incorporating graphene composites, with the material showing potential to reduce vehicle weights by up to 15% while improving structural integrity. The aerospace sector has seen particular interest, with graphene composites offering superior thermal stability for spacecraft components. Recent tests show tensile strength improvements exceeding 200% in polymer composites containing just 1% graphene nanosheets.

Sustainability Initiatives Creating New Opportunities

The market is benefiting from growing environmental concerns and the push for sustainable materials. Graphene nanosheets enable thinner, more efficient coatings that reduce material usage while enhancing performance – anti-corrosion coatings with graphene additives last up to 5 times longer than conventional alternatives. Water treatment applications are emerging as another key growth area, with graphene membranes demonstrating 99% salt rejection rates for desalination. Recent breakthroughs in scalable production methods have reduced costs by nearly 40% since 2020, making graphene solutions increasingly viable for large-scale environmental applications.

Key Industry Players

Market Leaders Expand Production Capacity to Meet Rising Demand

The graphene nanosheets market exhibits a dynamic competitive landscape with several established players vying for market share. Angstron Materials currently leads the segment with its proprietary large-scale production technology, holding approximately 18% of the global revenue share in 2024. Their dominance stems from extensive research investments and long-term supply agreements with major electronics manufacturers.

Applied Graphene Materials has emerged as another formidable competitor, particularly in Europe, where its patented plasma technology enables cost-efficient production of high-purity nanosheets. The company’s recent strategic partnership with automotive coating manufacturers has further strengthened its position in industrial applications.

Meanwhile, Asian manufacturers like Times Nano and Ceal Tech are rapidly expanding their market presence through aggressive pricing strategies and government-backed initiatives. These companies benefit from regional supply chain advantages and increasing domestic demand in China’s electronics sector.

North American players such as Vorbeck Materials and CVD Equipment Corporation maintain technological superiority in specialized applications, particularly in aerospace and defense sectors. Their focus on developing tailored solutions for high-performance composites has created stable revenue streams despite pricing pressures.

List of Key Graphene Nanosheets Manufacturers

- Angstron Materials (U.S.)

- Applied Graphene Materials (UK)

- Times Nano (China)

- Ceal Tech (South Korea)

- Vorbeck Materials (U.S.)

- CVD Equipment Corporation (U.S.)

- Graphenea (Spain)

- Haydale Graphene Industries (UK)

- NanoXplore Inc. (Canada)

Segment Analysis:

By Type

Hydrophilic Segment Dominates Due to Enhanced Dispersion Properties

The market is segmented based on type into:

- Hydrophilic

- Subtypes: Oxygen-functionalized, Water-soluble

- Hydrophobic

- Subtypes: Pristine, Non-functionalized

- Others

By Application

Electricity Segment Leads Owing to Superior Conductivity Characteristics

The market is segmented based on application into:

- Electricity

- Subtypes: Batteries, Supercapacitors, Conductive inks

- Coating

- Subtypes: Anti-corrosion, Thermal barrier

- Composite Material

- Subtypes: Polymer composites, Ceramic composites

- Others

By End User

Electronics Industry Accounts for Largest Share Due to Miniaturization Trends

The market is segmented based on end user into:

- Electronics

- Energy Storage

- Automotive

- Aerospace

- Healthcare

By Production Method

Chemical Vapor Deposition Leads as Industry Standard for High-Quality Production

The market is segmented based on production method into:

- Chemical Vapor Deposition

- Mechanical Exfoliation

- Chemical Reduction of Graphite Oxide

- Others

Regional Analysis: Graphene Nanosheets Market

North America

North America remains a dominant force in the global graphene nanosheets market, driven by significant investments in R&D and strong adoption across electronics, energy storage, and composite applications. The U.S., with its extensive research initiatives from institutions like MIT and Stanford, accounts for over 40% of regional demand. Strict regulatory frameworks and government funding, including DOE grants for advanced materials, accelerate commercialization efforts. However, high production costs and scalability challenges restrain broader industrial adoption. Key players like Angstron Materials and CVD Equipment maintain strong footholds through proprietary manufacturing techniques.

Europe

Europe’s graphene nanosheets market thrives under EU-funded programs such as the Graphene Flagship initiative, which allocated €1 billion to accelerate commercial applications. Germany and the UK lead in patent filings, particularly for conductive inks and biomedical coatings. Stringent REACH regulations compel manufacturers to develop environmentally sustainable production methods. While academic-industry collaborations flourish, inconsistent funding across smaller economies limits uniform growth. Companies like Graphenea and Thomas Swan leverage partnerships with automotive giants to integrate graphene-enhanced composites.

Asia-Pacific

The Asia-Pacific region is poised for the highest CAGR, fueled by China’s aggressive investments in graphene production hubs and India’s burgeoning electronics sector. China alone contributes ~60% of global supply volumes, supported by cost-efficient manufacturing ecosystems. Japan and South Korea focus on high-value applications in flexible displays and battery technologies. However, quality inconsistencies in locally produced nanosheets create challenges for export markets. Emerging players like Times Nano compete with Western firms by offering lower-cost alternatives, though intellectual property concerns persist.

South America

South America shows nascent but promising growth, with Brazil spearheading R&D through universities and government-backed nanotech programs. The region’s mining industry drives demand for graphene-reinforced materials in heavy equipment. Still, economic instability and limited infrastructure hinder large-scale production capabilities. Most graphene nanosheets are imported, creating supply chain vulnerabilities. Local startups increasingly collaborate with Asian suppliers to offset technological gaps, particularly in conductive coatings for renewable energy applications.

Middle East & Africa

This region exhibits uneven development, with GCC nations like Saudi Arabia investing heavily in graphene for oil & gas and construction sectors through Vision 2030 initiatives. South Africa’s mining sector explores graphene-enhanced wear-resistant materials. However, limited local expertise and reliance on foreign technology imports slow market penetration. Strategic partnerships, such as those between UAE universities and European firms, aim to build domestic capabilities. Though currently a minor player, the region’s long-term potential in energy storage applications garners investor interest.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Graphene Nanosheets markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Graphene Nanosheets market was valued at USD million in 2024 and is projected to reach USD million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (hydrophilic, hydrophobic), application (electricity, coating, composite material), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including CVD Equipment, Cheap Tubes, Angstron Materials, and ACS Material, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging manufacturing techniques, integration with advanced materials, and evolving industry standards for graphene applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for material suppliers, OEMs, research institutions, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Graphene Nanosheets Market?

-> Graphene Nanosheets Market size was valued at US$ 167 million in 2024 and is projected to reach US$ 334 million by 2032, at a CAGR of 10.0% during the forecast period 2025-2032.

Which key companies operate in Global Graphene Nanosheets Market?

-> Key players include CVD Equipment, Cheap Tubes, Angstron Materials, ACS Material, Applied Graphene Materials, and Thomas Swan, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for advanced materials in electronics, rising investments in nanotechnology, and growing applications in energy storage solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include development of scalable production methods, integration in flexible electronics, and applications in biomedical devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...