MARKET INSIGHTS

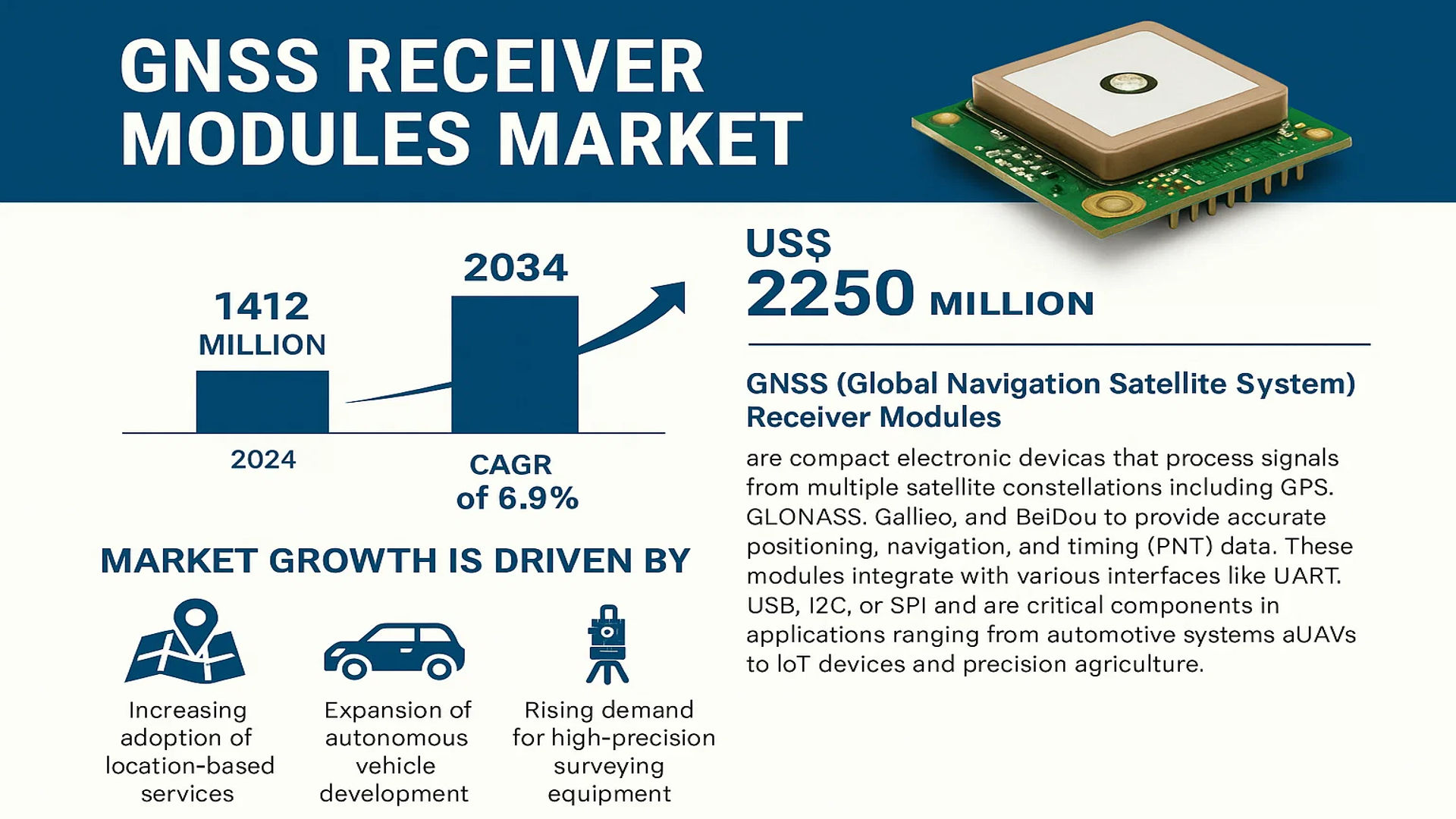

The global GNSS Receiver Modules Market was valued at 1412 million in 2024 and is projected to reach US$ 2250 million by 2032, at a CAGR of 6.9% during the forecast period.

GNSS (Global Navigation Satellite System) Receiver Modules are compact electronic devices that process signals from multiple satellite constellations including GPS, GLONASS, Galileo, and BeiDou to provide accurate positioning, navigation, and timing (PNT) data. These modules integrate with various interfaces like UART, USB, I2C, or SPI and are critical components in applications ranging from automotive systems and UAVs to IoT devices and precision agriculture.

The market growth is driven by increasing adoption of location-based services, expansion of autonomous vehicle development, and rising demand for high-precision surveying equipment. Technological advancements such as multi-frequency support and Real-Time Kinematics (RTK) are enabling centimeter-level accuracy, further accelerating adoption. The U.S. holds a significant market share, while China is emerging as a high-growth region due to its expanding BeiDou satellite infrastructure. Key players like Trimble, u-blox, and Qualcomm are investing in advanced chipset designs to enhance performance while reducing power consumption for IoT applications.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Autonomous Vehicle Technology to Propel GNSS Receiver Modules Demand

The rapid development of autonomous vehicle technology is significantly driving the adoption of GNSS receiver modules. These modules provide critical positioning data required for navigation and obstacle avoidance in self-driving cars. The automotive sector is witnessing substantial investments, with major manufacturers increasingly integrating multi-frequency GNSS solutions to enhance accuracy. High-precision modules with Real-Time Kinematic (RTK) capabilities are becoming standard in advanced driver assistance systems (ADAS) and fully autonomous platforms. Industry adoption rates continue to rise as regulatory frameworks evolve to accommodate autonomous vehicle testing and deployment across major markets. This growing acceptance is creating sustained demand for reliable positioning solutions that only GNSS modules can provide. Recent advances in module miniaturization and power efficiency further expand their suitability for automotive integration.

Growth of IoT and Smart City Infrastructure to Accelerate Market Expansion

The proliferation of IoT devices and smart city initiatives is creating substantial opportunities for GNSS receiver module manufacturers. Smart infrastructure projects increasingly rely on location-based services for asset tracking, environmental monitoring, and urban planning applications. GNSS modules are becoming essential components in connected devices, with demand increasing significantly across industries such as logistics, agriculture, and utilities. Municipalities globally are investing heavily in intelligent transportation systems that utilize GNSS technology for traffic management and public transit optimization. Meanwhile, the industrial IoT sector is adopting GNSS-enabled solutions for fleet management and supply chain visibility. Deployment numbers continue to show robust year-over-year growth as connectivity infrastructure expands and module costs decline due to economies of scale.

Military and Defense Modernization Programs Driving High-Precision Requirements

Global increases in defense spending and modernization programs are creating strong demand for ruggedized GNSS receiver modules with enhanced security features. Military applications require modules that maintain functionality in challenging environments while resisting jamming and spoofing attempts. Governments worldwide are investing in next-generation navigation systems for defense applications, with particular focus on secure positioning in GPS-denied environments. This has led to development of hybrid solutions combining GNSS with alternative positioning technologies. The defense sector’s emphasis on unmanned systems for surveillance and reconnaissance further amplifies the need for reliable GNSS modules capable of precise positioning in dynamic operational scenarios.

MARKET RESTRAINTS

Signal Interference and Obstruction Challenges to Limit Market Potential

GNSS receiver modules face significant technical limitations related to signal availability and reliability in urban and indoor environments. High-rise buildings create urban canyons that frequently disrupt satellite signals, while indoor applications often prove problematic due to signal attenuation. These limitations become particularly acute for applications requiring continuous positioning, such as autonomous mobile robots or indoor navigation systems. While augmentation systems and sensor fusion techniques can mitigate some issues, they often increase system complexity and cost. The growing prevalence of unintentional RF interference from various electronic devices further compounds these challenges, potentially limiting market adoption in certain applications.

Regulatory Complexities and Export Controls to Impact Market Dynamics

The GNSS technology sector operates under stringent international regulations that can constrain market expansion. Export controls on sensitive positioning technologies affect manufacturers’ ability to serve certain geographic markets. Different regional certification requirements for wireless and navigation devices create additional compliance burdens that may delay product launches. The regulatory landscape is particularly complex for dual-use technologies with both civilian and military applications. Compliance with evolving spectrum allocation policies and privacy regulations regarding location data adds further operational complexity for module manufacturers. These factors collectively influence product development cycles and may slow innovation in some market segments.

MARKET OPPORTUNITIES

Emergence of Centimeter-Level Precision Solutions to Open New Application Areas

Developments in high-precision GNSS technologies are creating unprecedented opportunities across multiple industries. Centimeter-level accuracy solutions using RTK and PPP techniques are enabling new applications in precision agriculture, construction automation, and surveying. The agriculture sector is rapidly adopting these technologies for autonomous equipment guidance and variable-rate application systems. Construction firms are implementing GNSS-based machine control systems to improve accuracy and efficiency in earthmoving operations. These high-precision applications command premium pricing and demonstrate strong growth potential as their operational benefits become increasingly recognized across industries.

Integration with 5G Networks to Enhance Hybrid Positioning Capabilities

The global rollout of 5G infrastructure presents significant opportunities for GNSS receiver module manufacturers. Network operators are developing hybrid positioning solutions that combine GNSS with 5G-based localization to improve accuracy and reliability. This convergence is particularly valuable for indoor positioning and urban navigation applications where traditional GNSS performance is limited. The telecommunications industry’s push for location-based services is driving innovation in integrated positioning architectures. Module manufacturers collaborating with network equipment providers can capitalize on this trend by developing solutions optimized for 5G-network assisted positioning.

MARKET CHALLENGES

Increasing Threat of Signal Spoofing and Cybersecurity Risks

The GNSS industry faces growing security challenges as sophisticated spoofing and jamming techniques become more prevalent. These threats are particularly concerning for critical infrastructure and transportation applications where location integrity is paramount. Recent incidents have demonstrated vulnerabilities in various GNSS-dependent systems, raising awareness of the need for enhanced security measures. Developing robust anti-spoofing and anti-jamming technologies while maintaining cost-effectiveness presents an ongoing challenge for module manufacturers. The industry must balance security enhancements with power consumption and form factor considerations to meet diverse application requirements.

Intense Price Competition and Commoditization Pressures

The GNSS receiver module market is experiencing increasing price pressures as basic positioning functionality becomes standardized. Intense competition among manufacturers, particularly in consumer-grade modules, is eroding profit margins. Many industry participants are responding by differentiating their offerings through enhanced features or specialized certifications. However, the trend toward commoditization in certain market segments makes it challenging to maintain premium pricing. Manufacturers must carefully balance cost reduction efforts with investments in innovation to remain competitive in this evolving landscape.

GNSS RECEIVER MODULES MARKET TRENDS

Integration of Multi-Constellation Support to Emerge as a Dominant Market Trend

One of the most transformative trends reshaping the GNSS receiver modules market is the widespread adoption of multi-constellation support. Modern receivers increasingly integrate compatibility with multiple satellite systems, including GPS (U.S.), GLONASS (Russia), Galileo (Europe), and BeiDou (China), enabling enhanced positioning accuracy and reliability. This multi-frequency capability is critical in urban canyons, dense foliage, and other challenging environments where satellite signals may be obstructed. The global deployment of high-precision BeiDou-3 satellites has further expanded coverage, particularly in Asia-Pacific, intensifying the demand for receivers that leverage this constellation. Additionally, advancements in Real-Time Kinematic (RTK) and Precise Point Positioning (PPP) technologies are refining sub-meter to centimeter-level accuracy, positioning these modules as vital components in autonomous vehicles, drones, and precision agriculture.

Other Trends

Rise of Low-Power, Small Form Factor Modules for IoT Applications

The exponential growth of the Internet of Things (IoT) has fueled demand for compact, energy-efficient GNSS modules tailored for asset tracking, wearables, and smart city infrastructure. Manufacturers are prioritizing ultra-low-power designs with integrated inertial sensors to maintain location accuracy during signal loss, a common challenge in indoor or underground applications. Innovations like u-blox’s M10 platform demonstrate the shift toward chipsets that consume under 10mW while delivering extended battery life—critical for edge devices operating on limited power. Concurrently, the proliferation of 5G and LPWAN networks is driving convergence between cellular and GNSS technologies, enabling seamless global tracking solutions.

Expanding Applications in Autonomous Navigation Systems

The automotive and robotics sectors are accelerating the adoption of high-integrity GNSS modules to support Level 4 and Level 5 autonomous vehicles. With the global autonomous vehicle market projected to surpass 800,000 units by 2030, receiver modules must now meet stringent safety standards like ISO 26262 (ASIL-B/D) while resisting signal jamming and spoofing. Companies such as Trimble and Septentrio are pioneering dual-antenna configurations for attitude determination, enabling precise lane-level navigation. Meanwhile, marine and UAV applications are leveraging GNSS/INS (Inertial Navigation Systems) fusion to ensure uninterrupted positioning in GPS-denied environments, unlocking new potentials in drone delivery and offshore surveying.

COMPETITIVE LANDSCAPE

Key Industry Players

GNSS Module Providers Accelerate Innovation to Capture Emerging Positioning Tech Demand

The global GNSS receiver modules market exhibits a moderately fragmented competitive environment, with established technology providers competing alongside specialized navigation solution developers. u-blox leads the market through its comprehensive portfolio of multi-constellation modules, holding approximately 18% revenue share in 2024. The Swiss company’s strength stems from its early adoption of Galileo/BeiDou compatibility and energy-efficient designs for IoT applications.

Trimble and Septentrio maintain strong positions in high-precision GNSS segments, leveraging their RTK and PPP technologies for surveying, agriculture, and autonomous systems. Both companies have recently expanded their compact module offerings to address drone and robotics markets, with Trimble launching its AGM5 series and Septentrio introducing AsteRx-m3 in 2024.

Meanwhile, semiconductor giants Qualcomm and Broadcom are gaining traction through integrated GNSS solutions for consumer electronics and automotive applications. Qualcomm’s dual-frequency GNSS integration in Snapdragon platforms has particularly strengthened its position in smartphone positioning markets.

The competitive landscape continues evolving with strategic moves—Telit Cinterion merged positioning and cellular IoT capabilities through its SE868K series, while Quectel captured significant market share in Asia through cost-optimized modules for fleet management and asset tracking applications.

List of Key GNSS Receiver Module Companies

- u-blox (Switzerland)

- Trimble Inc. (U.S.)

- Septentrio (Belgium)

- Qualcomm Technologies (U.S.)

- Broadcom Inc. (U.S.)

- Hemisphere GNSS (Canada)

- STMicroelectronics (Switzerland)

- Telit Cinterion (U.K.)

- Topcon (Japan)

- Quectel (China)

Segment Analysis:

By Type

Multi-Frequency Modules Segment Drives Market Growth with Enhanced Precision Across Applications

The market is segmented based on type into:

- Single-Frequency Modules

- Subtypes: GPS L1, GLONASS L1, Galileo E1, and others

- Multi-Frequency Modules

By Application

Autonomous Vehicles Lead the Market with Increasing Demand for Precise Navigation Solutions

The market is segmented based on application into:

- Autonomous Vehicles

- Marine Navigation

- UAVs & Drones

- Surveying & Mapping

- Internet of Things (IoT)

- Others

By Technology

RTK Technology Gains Traction for Centimeter-Level Accuracy Requirements

The market is segmented based on technology into:

- Standard Precision

- Real-Time Kinematics (RTK)

- Precise Point Positioning (PPP)

- Others

Regional Analysis: GNSS Receiver Modules Market

Asia-Pacific

The Asia-Pacific region dominates the global GNSS Receiver Modules market, driven by rapid adoption in automotive and industrial IoT applications. China is the largest contributor due to government-backed infrastructure projects and heavy investments in autonomous vehicle development. India follows closely, with increasing demand for precision agriculture and smart city initiatives. Japan leads in high-precision GNSS modules for robotics and construction, while South Korea excels in consumer electronics integration. The region benefits from strong semiconductor manufacturing ecosystems and proximity to key module producers like Quectel and MediaTek. However, market fragmentation and intense price competition among local manufacturers challenge profit margins for global players.

North America

As the second-largest market, North America maintains technological leadership in high-end GNSS solutions, particularly for defense and aerospace applications. The U.S. government’s modernization of GPS infrastructure and strict accuracy requirements for autonomous driving systems fuel demand for multi-frequency modules. Canadian mining and forestry sectors increasingly adopt RTK-enabled receivers, while Mexico sees growth in fleet management solutions. Major players like Trimble and Qualcomm drive innovation, but regulatory hurdles for drone and autonomous vehicle operations temporarily hinder some deployments. The region maintains premium pricing power for advanced centimeter-level accuracy solutions.

Europe

Europe shows strong adoption of GNSS modules across automotive and marine applications, with strict regulations pushing embedded navigation system mandates. The Galileo satellite system’s completion enhances regional positioning accuracy, benefiting surveying and precision agriculture sectors. Germany leads in industrial IoT implementations, while Nordic countries pioneer cold-weather performance enhancements for modules. The EU’s focus on standardized vehicular telematics creates consistent demand, though lengthy certification processes slow time-to-market. Environmental durability requirements and cybersecurity concerns shape product development priorities for manufacturers like u-blox and Septentrio operating in the region.

Middle East & Africa

This emerging market shows accelerating GNSS module adoption, particularly in oil & gas exploration and smart city projects across Gulf Cooperation Council countries. Israel’s defense technology sector drives specialized high-accuracy demand, while African nations increasingly implement GNSS for wildlife tracking and mineral exploration. Challenges include harsh environmental conditions requiring ruggedized modules and intermittent satellite coverage in remote areas. The market shows potential for leapfrog adoption in IoT applications, though price sensitivity limits penetration of premium multi-frequency solutions currently favored in developed markets.

South America

Growth in South America remains steady but constrained by economic volatility, with Brazil and Argentina as primary markets. Precision farming adoption rises among large-scale agricultural operations, while urban transportation projects create opportunities for fleet tracking modules. Limited local manufacturing forces reliance on imports, subject to fluctuating import duties. However, developing satellite infrastructure partnerships with China’s BeiDou system may enhance coverage and spur future growth. The mining sector increasingly adopts GNSS for equipment tracking, though cost sensitivity favors single-frequency solutions over advanced RTK configurations prevalent elsewhere.

Report Scope

This market research report provides a comprehensive analysis of the Global GNSS Receiver Modules Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 1,412 million in 2024 and is projected to reach USD 2,250 million by 2032, growing at a CAGR of 6.9%.

- Segmentation Analysis: Detailed breakdown by product type (Single-Frequency and Multi-Frequency Modules), application (Autonomous Vehicles, Marine Navigation, UAVs & Drones, Surveying & Mapping, IoT), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for the U.S., China, Germany, Japan, and other key markets.

- Competitive Landscape: Profiles of leading market participants including Trimble, u-blox, Qualcomm, Broadcom, and STMicroelectronics, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies including multi-constellation support, RTK precision, and integration with AI/ML for enhanced positioning accuracy.

- Market Drivers & Restraints: Analysis of growth drivers like autonomous vehicle adoption and IoT expansion, along with challenges such as signal interference and regulatory constraints.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global GNSS Receiver Modules Market?

-> GNSS Receiver Modules Market was valued at 1412 million in 2024 and is projected to reach US$ 2250 million by 2032, at a CAGR of 6.9% during the forecast period.

Which key companies operate in Global GNSS Receiver Modules Market?

-> Key players include Trimble, u-blox, Qualcomm, Broadcom, STMicroelectronics, Septentrio, and Leica Geosystems, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of autonomous vehicles, expansion of IoT applications, and increasing demand for precision agriculture solutions.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of AI for enhanced positioning, development of low-power GNSS solutions for IoT, and increasing adoption of multi-constellation receivers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...