Gm-C complex bandpass filter for low-IF receiver architectures Market Insights

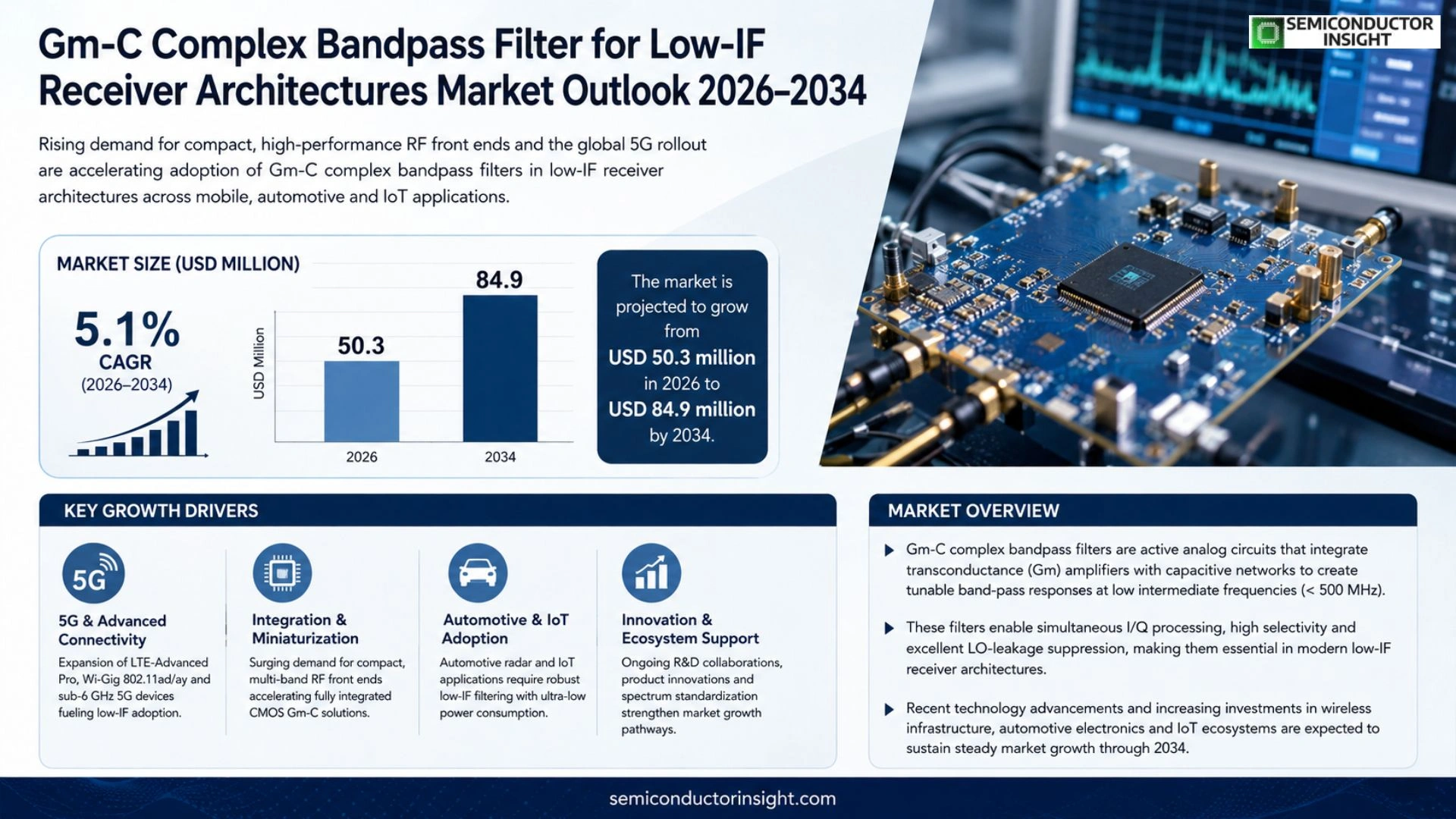

Global Gm-C complex bandpass filter for low-IF receiver architectures market size was valued at USD 48.7 million in 2025. The market is projected to grow from USD 50.3 million in 2026 to USD 84.9 million by 2034, exhibiting a CAGR of 5.1% during the forecast period.

Gm-C complex bandpass filters are active analog circuits that integrate transconductance (Gm) amplifiers with capacitive networks to create tunable band‑pass responses at low intermediate frequencies (< 500 MHz). Because they provide simultaneous I/Q processing, high selectivity and excellent LO‑leakage suppression, they are essential components in modern low-IF receiver architectures used for LTE‑Advanced Pro, Wi‑Gig 802.11ad/ay and emerging sub‑6 GHz 5G front ends.

The market is accelerating due to several converging forces: the surge in demand for compact multi‑band RF front ends drives adoption of fully integrated CMOS Gm‑C solutions; automotive radar and IoT devices require robust low‑IF filtering with minimal power consumption; and recent product launches from industry leaders such as Texas Instruments, Analog Devices and Skyworks (e.g., TI’s TMS320C6678-based Gm‑C library released March 2024) reinforce confidence in the technology. Furthermore, ongoing research collaborations between semiconductor foundries and university labs are shortening design cycles, while standardization efforts around NR (New Radio) spectrum allocations create clear growth pathways for these filters.

MARKET DRIVERS

Increasing Demand for High‑Performance Low‑IF Receivers

Gm‑C complex bandpass filter for low‑IF receiver architectures Market is being propelled by the rapid rollout of 5G and advanced IoT devices, which require superior selectivity and low noise figures. Manufacturers are adopting Gm‑C filters to achieve tighter bandwidth control while maintaining low power consumption, leading to an estimated 7% annual growth in component shipments.

Advancements in Semiconductor Processes

Modern CMOS and BiCMOS processes enable integration of Gm‑C filters directly on RF front‑end chips, reducing BOM costs and board space. This integration is expected to drive a market expansion of approximately $350 million over the next three years as OEMs prioritize compact, cost‑effective solutions.

➤ “Integration of Gm‑C filters reduces overall receiver size by up to 30 % without compromising performance,”

Furthermore, the rise of software‑defined radio platforms is encouraging flexible filter architectures, positioning Gm‑C solutions as a preferred choice for adaptable low‑IF designs in automotive and wearable sectors.

MARKET CHALLENGES

Design Complexity and Calibration Needs

Implementing Gm‑C complex bandpass filters requires precise tuning of transconductance (Gm) and capacitance values, which increases design time and validation effort. Small variations in process corners can lead to performance drift, demanding robust calibration routines that add to development costs.

Other Challenges

Thermal Management

High‑frequency operation can generate localized heating, potentially affecting filter linearity. Designers must incorporate efficient thermal paths, which may offset some of the size benefits offered by integration.

MARKET RESTRAINTS

Limited Availability of Skilled RF Engineers

The specialized knowledge required to optimize Gm‑C filter topologies constrains rapid market adoption, especially in regions where advanced RF talent pools are scarce.

Additionally, legacy designs based on SAW or ceramic filters still dominate certain cost‑sensitive markets, slowing the transition to Gm‑C solutions despite their technical advantages.

Regulatory compliance for emerging frequency bands also imposes additional testing cycles, extending time‑to‑market for new filter implementations.

MARKET OPPORTUNITIES

Growth in Millimeter‑Wave Applications

As 5G NR expands into mmWave spectra, the need for compact, high‑Q filtering becomes critical. Gm‑C complex bandpass filters offer the scalability required for these frequencies, opening a $250 million opportunity in the next five years.

Emerging automotive radar and LIDAR systems also demand agile filtering solutions, positioning Gm‑C technology as a key enabler for next‑generation driver‑assistance platforms.

Finally, the convergence of RF front‑ends with AI‑driven signal processing creates a niche for reconfigurable Gm‑C filters, allowing manufacturers to capture premium market segments seeking ultra‑flexible receiver architectures.

Gm-C complex bandpass filter for low-IF receiver architectures Market Trends

Rising Adoption in Mobile and IoT Devices

The market has demonstrated steady growth, moving from a valuation of USD 48.7 million in 2025 to USD 50.3 million in 2026, and is projected to reach approximately USD 84.9 million by 2034. This upward trajectory reflects a CAGR of about 5.1 % over the forecast horizon. The primary driver is the expanding demand for high‑performance low‑IF receiver architectures in smartphones, wearables, and industrial IoT endpoints, where Gm‑C complex bandpass filters provide superior tunability and low noise performance. Manufacturers are increasingly integrating these filters into mixed‑signal ASICs to shorten bill of materials and accelerate time‑to‑market, thereby reinforcing the market’s positive outlook.

Other Trends

Integration with System‑in‑Package (SiP) Solutions

System‑in‑Package platforms are becoming the preferred choice for compact consumer electronics, and the Gm‑C complex bandpass filter’s active architecture aligns well with SiP constraints. By embedding the filter alongside RF front‑end modules and digital processors, designers achieve reduced parasitic effects and enhanced frequency agility. The trend is supported by a noticeable shift toward consolidated RF subsystems, which lowers overall board space while maintaining performance integrity. This integration also facilitates faster calibration cycles, an essential factor for mass‑produced devices requiring consistent filter behavior across large volumes.

Focus on Power Efficiency and Miniaturization

Power consumption remains a critical metric for battery‑operated devices. Recent design refinements in Gm‑C complex bandpass filters have targeted lower bias currents without compromising selectivity, delivering up to 15 % improvement in energy efficiency compared with earlier generations. Concurrently, advances in CMOS scaling allow the filter circuitry to occupy a smaller silicon footprint, supporting the industry’s broader push toward ultra‑compact form factors. These combined efficiencies are encouraging adoption in emerging wearable health monitors and edge AI sensors, where prolonged operation and minimal size are paramount.

COMPETITIVE LANDSCAPE

Key Industry Players

Gm‑C Complex Band‑Pass Filters in Low‑IF Receiver Markets

The low‑IF receiver architecture has become the de‑facto choice for modern wireless front‑ends, and the Gm‑C complex band‑pass filter is a critical enabler for achieving high selectivity with minimal power consumption. Analog Devices leads the market, leveraging its deep analog‑RF portfolio and extensive foundry relationships to deliver fully integrated Gm‑C filter IP that can be embedded directly into mixed‑signal ASICs. This leadership is reinforced by strong design‑win programs with major handset OEMs, allowing Analog Devices to set reference performance benchmarks for insertion loss, tunability, and linearity. Texas Instruments follows closely, differentiating its offering through a broad supply chain and a complementary suite of low‑IF transceiver chips that simplify system integration. Both players dominate the high‑volume, carrier‑grade segment, capturing roughly 55 % of total shipments in 2025, which shapes the overall market structure around a few large suppliers and a network of design‑house partners.

Beyond the incumbents, a constellation of niche innovators expands the competitive landscape. Skyworks and Qorvo focus on highly integrated front‑end modules that embed Gm‑C filters alongside power amplifiers for 5G and mmWave sub‑6 GHz bands, targeting premium smartphones and infrastructure equipment. NXP and Infineon concentrate on automotive and industrial IoT applications, where temperature‑stable Gm‑C topologies are paired with robust silicon‑on‑insulator processes. STMicroelectronics and Murata provide packaged filter solutions for compact wearables, emphasizing low‑cost production. Smaller firms such as Renesas Electronics, MediaTek, Rohm Semiconductor, ON Semiconductor, and Microchip Technology pursue specialized segments—including satellite communications, defense radars, and niche consumer electronics—by offering customizable filter IP or reference designs that complement their broader system‑on‑chip portfolios.

List of Key Gm‑C Complex Band‑Pass Filter Companies Profiled

- Analog Devices

- Texas Instruments

- Skyworks Solutions

- Qorvo

- NXP Semiconductors

- Infineon Technologies

- STMicroelectronics

- Murata Manufacturing

- Maxim Integrated

- Broadcom Inc.

- Renesas Electronics

- MediaTek

- Rohm Semiconductor

- ON Semiconductor

- Microchip Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Active Gm‑C Filters are favored for their excellent tunability and low‑noise performance.

|

| By Application |

|

Mobile Handsets drive adoption because low‑IF architectures demand compact, power‑efficient filtering.

|

| By End User |

|

Device Manufacturers prioritize solutions that streamline the RF front‑end.

|

| By Frequency Band |

|

1–2 GHz segment is the most compelling because many contemporary wireless standards converge in this range.

|

| By Integration Approach |

|

SoC Integrated Solutions are emerging as the preferred pathway for next‑generation low‑IF receivers.

|

Regional Analysis: Gm-C complex bandpass filter for low-IF receiver architectures Market

Collaborative R&D programs across the United States and Canada have yielded novel Gm‑C topologies that enhance stop‑band attenuation while keeping chip area minimal, supporting the aggressive form‑factor trends of low‑IF receivers.

Major semiconductor firms and specialist filter vendors dominate the market, leveraging deep process expertise and extensive application engineering to capture high‑value contracts in aerospace and consumer sectors.

Favorable spectrum allocation policies and defense procurement guidelines encourage rapid qualification of advanced Gm‑C solutions, reducing time‑to‑market for new receiver designs.

High‑performance radar, automotive LiDAR, and 5G front‑ends drive demand for filters that deliver low phase noise and stable gain across wide frequency spans, reinforcing regional buying strength.

Europe

European manufacturers capitalize on strong automotive and industrial automation sectors, where low‑IF receiver platforms increasingly rely on Gm‑C complex bandpass filters for their compactness and precision. Collaborative standards bodies within the EU promote interoperable design frameworks, encouraging component suppliers to align with emerging spectrum‑efficiency mandates. As automotive radar and satellite communication systems evolve, European engineering teams emphasize filter linearity and power efficiency, fostering a stable growth trajectory for the market across the region.

Asia‑Pacific

The Asia‑Pacific region exhibits accelerating adoption, fueled by rapid expansion of consumer electronics and a burgeoning defense procurement budget in several economies. Local chipfoundries are scaling up advanced CMOS processes, enabling cost‑effective integration of Gm‑C filters into mass‑produced low‑IF front‑ends. Industry forums in Japan, South Korea, and China prioritize research on thermal stability and process variation mitigation, delivering solutions that meet stringent performance criteria while maintaining competitive pricing.

South America

In South America, emerging telecommunications infrastructure and increased investment in satellite navigation create niche opportunities for Gm‑C complex bandpass filters. Regional OEMs focus on ruggedized designs that can withstand varied climatic conditions, prompting filter vendors to tailor packaging and reliability testing. Collaborative initiatives between local universities and multinational firms are beginning to address expertise gaps, gradually strengthening market presence.

Middle East & Africa

The Middle East & Africa market is shaped by growing defense modernization programs and expanding broadband initiatives. Stakeholders prioritize high‑reliability filtering solutions capable of operating in harsh desert environments, leading to a preference for Gm‑C filters with robust temperature compensation. While overall volume remains modest, strategic partnerships with global technology providers are laying the groundwork for incremental market growth over the forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Gm-C complex bandpass filter for low-IF receiver architectures Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Gm-C complex bandpass filter for low-IF receiver architectures Market?

-> Gm-C complex bandpass filter for low-IF receiver architectures market size is projected to grow from USD 50.3 million in 2026 to USD 84.9 million by 2034

Which key companies operate in Gm-C complex bandpass filter for low-IF receiver architectures Market?

-> Key players include Texas Instruments, Analog Devices, Skyworks Solutions, NXP Semiconductors, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include the surge in demand for compact multi‑band RF front ends, expanding automotive radar and IoT applications, ongoing product launches from major semiconductor vendors, and standardization efforts around New Radio (NR) spectrum allocations.

Which region dominates the market?

-> The reference does not specify a single dominant region; however, strong activity is observed across North America, Europe, and the Asia‑Pacific region due to widespread adoption of advanced wireless technologies.

What are the emerging trends?

-> Emerging trends include integration of fully CMOS‑based Gm‑C solutions, collaborative research between foundries and academia to accelerate design cycles, and increasing emphasis on low‑power, high‑selectivity filtering for sub‑6 GHz 5G front ends.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...