Thermopile Sensors Market MARKET INSIGHTS

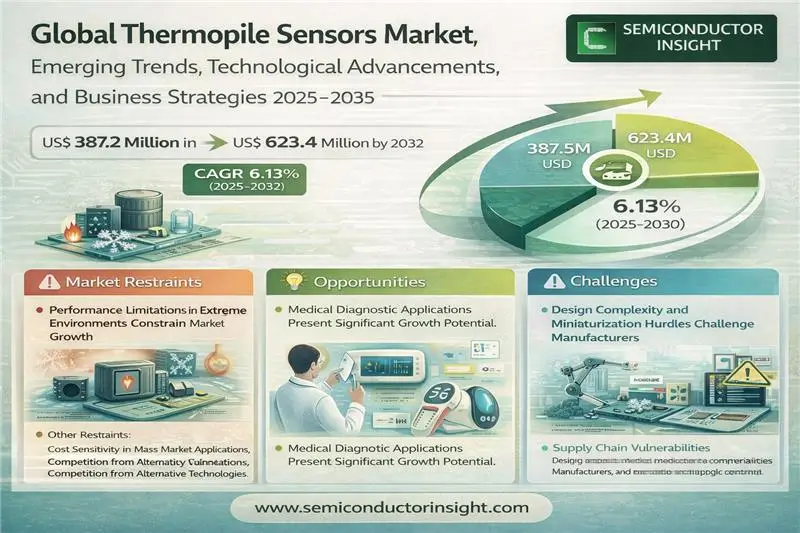

Global Thermopile Sensors Market was valued at USD 387.2 million in 2024 and is projected to reach USD 623.4 million by 2032, at a CAGR of 6.13% during the forecast period 2025-2032.

Thermopile sensors are infrared detection devices that convert thermal energy into electrical signals through series-connected thermocouples. These passive components measure temperature differences without direct contact, making them ideal for applications requiring non-invasive thermal monitoring. The technology is widely used in medical thermometers, industrial process control, automotive climate systems, and smart home devices.

The market growth is driven by increasing adoption in automotive HVAC systems, where demand rose 12% year-over-year in 2023. The healthcare sector accounts for 28% of total market share, propelled by contactless temperature measurement needs post-pandemic. Recent developments include Murata’s 2024 launch of ultra-thin thermopile arrays for wearable medical devices, while Texas Instruments expanded production capacity by 15% to meet growing IoT demand. Key players like Excelitas Technologies and FLIR Systems dominate the competitive landscape with advanced MEMS-based solutions.

Thermopile Sensors Market MARKET DYNAMICS

Thermopile Sensors Market MARKET DRIVERS

Growing Adoption in Consumer Electronics and Smart Home Applications Accelerates Market Expansion

Thermopile Sensors Market is experiencing robust growth driven by their increasing integration in consumer electronics and smart home devices. With the rising demand for touchless interfaces and energy-efficient solutions, thermopile sensors have become critical components in products like smart thermostats, motion detectors, and HVAC systems. Global smart home market, projected to surpass D 338 billion by 2030, creates substantial demand for these sensors which enable features like occupancy detection and temperature monitoring without physical contact.

Stringent Safety Regulations in Industrial Sector Fuel Market Demand

Industrial automation and workplace safety mandates are significantly driving thermopile sensor adoption. These sensors play a crucial role in predictive maintenance systems and equipment monitoring, helping prevent overheating in machinery and electrical systems. Regulatory requirements in oil & gas, manufacturing, and energy sectors increasingly mandate continuous temperature monitoring, creating sustained demand for reliable thermopile solutions that can operate in harsh environments.

Furthermore, the automotive industry’s shift toward advanced driver-assistance systems (ADAS) and cabin comfort features provides additional growth avenues. Thermopile sensors enable critical functions like occupant detection for airbag deployment and climate control personalization.

Thermopile Sensors Market MARKET RESTRAINTS

Performance Limitations in Extreme Environments Constrain Market Growth

While thermopile sensors offer numerous advantages, their performance limitations in extreme conditions present significant challenges. These sensors demonstrate reduced accuracy and reliability when subjected to rapid temperature fluctuations or operating outside specified ranges. In industrial applications where equipment may reach temperatures exceeding 150°C, traditional thermopile sensors often require additional shielding and cooling mechanisms, increasing system complexity and cost.

Other Restraints

Cost Sensitivity in Mass Market Applications

The relatively high production costs of precision thermopile sensors make price-sensitive applications challenging. Consumer product manufacturers often opt for cheaper alternatives when high accuracy isn’t critical, limiting market penetration in cost-driven segments.

Competition from Alternative Technologies

Emerging temperature sensing technologies like MEMS-based sensors and advanced RTDs are gaining traction in applications where thermopile sensors traditionally dominated, particularly in medical and scientific instrumentation where precision requirements continue to escalate.

Thermopile Sensors Market MARKET CHALLENGES

Design Complexity and Miniaturization Hurdles Challenge Manufacturers

As applications demand smaller form factors, thermopile sensor manufacturers face significant engineering challenges in maintaining performance while reducing size. The inherent physics of thermopile arrays requires careful thermal management that becomes exponentially more difficult as package sizes shrink below 5mm x 5mm. This creates barriers for integration into wearable devices and compact IoT endpoints.

Additionally, achieving consistent manufacturing yields at smaller geometries presents technical obstacles. The precision alignment required between thermocouple junctions and optical filters becomes increasingly difficult to maintain during high-volume production, potentially leading to higher unit costs and supply constraints.

Supply Chain Vulnerabilities

The specialized materials required for thermopile sensor manufacturing, including rare earth elements for infrared filters and high-purity semiconductor substrates, create potential bottlenecks. Recent geopolitical tensions and trade restrictions have highlighted vulnerabilities in the supply of these critical components.

Thermopile Sensors Market MARKET OPPORTUNITIES

Medical Diagnostic Applications Present Significant Growth Potential

The healthcare sector offers substantial opportunities for thermopile sensor expansion, particularly in non-contact temperature measurement applications. Global medical infrared thermometer market alone is projected to grow at nearly 8% CAGR through 2030, driven by infection control protocols and telehealth adoption. Thermopile sensors enable precise, hygienic temperature monitoring without patient contact, making them ideal for hospitals, clinics, and home healthcare settings.

Advancements in AI-Enabled Predictive Maintenance Create New Use Cases

The integration of thermopile sensors with artificial intelligence and machine learning platforms is creating innovative industrial applications. By combining thermal imaging data with predictive analytics, these systems can identify equipment faults before they cause failures. Major industrial automation providers are increasingly incorporating thermopile-based condition monitoring into their service offerings, representing a high-value market segment growing at approximately 15% annually.

Furthermore, smart city initiatives leveraging thermopile sensors for building efficiency and traffic management present additional growth avenues. Municipalities worldwide are investing in intelligent infrastructure that utilizes thermal sensing for applications ranging from pedestrian flow analysis to building heat loss detection.

THERMOPILE SENSORS MARKET TRENDS

Expanding Applications in Automotive and Smart Home Devices Driving Market Growth

Global Thermopile Sensors Market is experiencing robust growth, primarily fueled by increasing integration in automotive climate control systems and smart home devices. As vehicles evolve toward electrification and autonomous operation, demand for precise temperature monitoring in battery management and cabin comfort systems has surged. The smart home sector, valued at over D 100 billion globally, relies heavily on thermopile sensors for HVAC optimization and presence detection in intelligent thermostats. Industry data suggests that shipments for consumer-grade infrared temperature sensors grew by approximately 18% year-over-year in 2023, with thermopiles representing nearly 40% of this segment.

Other Trends

Miniaturization and Energy Efficiency Innovations

Technological advancements are enabling the development of smaller, lower-power thermopile sensors without compromising accuracy. Recent innovations in MEMS (Micro-Electro-Mechanical Systems) technology have produced sensors with footprints under 3x3mm while achieving sub-0.1°C resolution. These improvements are critical for wearable medical devices and IoT applications where space and power constraints are paramount. Furthermore, the adoption of advanced materials like silicon-germanium alloys has enhanced thermal response times by up to 30% compared to conventional designs.

Growing Demand in Industrial Automation and Safety

Industrial sectors are increasingly deploying thermopile sensors for predictive maintenance and equipment monitoring. The ability to perform non-contact temperature measurements in hazardous environments makes them ideal for manufacturing plants and energy facilities. Market analysis indicates that the industrial segment accounted for over 25% of global thermopile sensor revenue in 2023, with particularly strong adoption in semiconductor fabrication and chemical processing. Moreover, stricter workplace safety regulations worldwide are accelerating the replacement of traditional thermocouples with more reliable thermopile-based solutions in high-risk applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in Thermopile Sensors

Global Thermopile Sensors Market features a dynamic competitive landscape, characterized by the presence of established players and emerging innovators. Leading companies such as Excelitas Technologies and FLIR Systems dominate the market, leveraging their strong R&D capabilities and diverse product portfolios. Excelitas, for instance, holds a substantial market share due to its high-performance infrared thermopile sensors, widely used in automotive and industrial applications.

Meanwhile, Hamamatsu Photonic and Nippon Ceramic have strengthened their positions through continuous technological advancements. Hamamatsu’s expertise in photonics has enabled it to develop ultra-sensitive thermopile sensors, particularly for medical and scientific applications, contributing to its growing market influence.

The market also sees intense competition from mid-sized players like Heimann Sensor GmbH and TE Connectivity, which focus on niche applications such as smart home devices and consumer electronics. These companies are rapidly expanding their geographic footprint, particularly in Asia-Pacific, where demand for smart sensors is surging.

Recent strategic moves, such as Murata’s acquisition of smaller sensor manufacturers and Texas Instruments’ investment in MEMS-based thermopile technology, highlight the market’s evolution. Such initiatives not only enhance product offerings but also consolidate market positions, ensuring long-term competitiveness.

List of Key Thermopile Sensor Companies Profiled

- Excelitas Technologies (U.S.)

- FLIR Systems (U.S.)

- Hamamatsu Photonic (Japan)

- Nippon Ceramic (Japan)

- TE Connectivity (Switzerland)

- Heimann Sensor GmbH (Germany)

- Texas Instruments (U.S.)

- Panasonic (Japan)

- Fuji Ceramics Corporation (Japan)

- Murata (Japan)

Segment Analysis:

By Type

Thermopile Infrared Sensors Lead the Market with Rising Demand in Non-Contact Temperature Measurement

The market is segmented based on type into:

- Thermopile Infrared Sensors

- Thermopile Laser Sensors

- Dual-band Thermopile Sensors

- Matrix Thermopile Sensors

- Others

By Application

Medical Science Segment Shows Strong Growth Potential Due to Increased Use of Thermopile Sensors in Diagnostic Equipment

The market is segmented based on application into:

- Medical Science

- Military and Defense

- Automobile Industry

- Intelligent Furnishing

- Others

By Operating Wavelength

Long-Wave Infrared (LWIR) Sensors Dominate With Widespread Use in Thermal Imaging

The market is segmented based on operating wavelength into:

- Short-Wave Infrared (SWIR)

- Mid-Wave Infrared (MWIR)

- Long-Wave Infrared (LWIR)

- Others

By End User

Industrial Sector Accounts for Significant Market Share Due to Process Control Applications

The market is segmented based on end user into:

- Industrial

- Healthcare

- Consumer Electronics

- Automotive

- Others

Regional Analysis: Global Thermopile Sensors Market

North America

The North American Thermopile Sensors Market is driven by strong demand from key industries such as defense, automotive, and medical technology. The region benefits from significant R&D investments in sensor technology, with the U.S. accounting for over 40% of global spending in infrared and thermal sensing applications. Regulatory requirements mandating safety and efficiency in automotive emissions monitoring and smart HVAC systems are accelerating adoption. Major players like Excelitas Technologies and Texas Instruments dominate the landscape, leveraging advanced manufacturing capabilities. However, high production costs and competition from cheaper Asian suppliers pose challenges. The growing shift toward Industry 4.0 and IoT integration in manufacturing presents long-term opportunities.

Europe

Europe maintains steady growth in thermopile sensors, primarily due to stringent industrial safety standards and rapid advancements in automotive ADAS (Advanced Driver Assistance Systems). Germany, France, and the UK lead adoption in medical diagnostics and energy-efficient building automation. EU directives on CO2 monitoring and non-contact temperature measurement in public spaces post-pandemic have further boosted demand. European manufacturers like Heimann Sensor GmbH excel in precision thermopile solutions for aerospace and healthcare. However, supply chain disruptions caused by geopolitical tensions and reliance on external semiconductor suppliers create vulnerabilities. Sustainability-focused innovations, particularly in renewable energy applications, are key growth drivers.

Asia-Pacific

As the fastest-growing regional market, Asia-Pacific benefits from mass production capabilities in China and Japan, with Shenzhen emerging as a major sensor manufacturing hub. Japan’s Nippon Ceramic and China’s Winsensor lead in cost-competitive thermopile modules for consumer electronics and automotive uses. India’s expanding medical device sector and Southeast Asia’s smart city initiatives drive incremental demand. Price sensitivity remains a challenge, with local manufacturers prioritizing affordability over high-end specifications. The region’s dominance in electronics manufacturing ensures sustained growth, though intellectual property protection issues occasionally disrupt market dynamics.

South America

The South American market shows moderate growth, concentrated in Brazil’s industrial automation and Argentina’s agricultural monitoring sectors. Limited local manufacturing capabilities result in heavy reliance on imports from North America and Asia. Economic instability and fluctuating currency values hinder large-scale adoption, though mining and oil/gas applications provide stable demand pockets. Governments are increasingly investing in infrared-based security systems for public safety, creating opportunities. The lack of standardized regulations compared to Europe or North America slows market maturation, but Brazil’s automotive sector shows promising uptake for driver monitoring systems.

Middle East & Africa

This emerging market is gaining traction through infrastructure modernization in Gulf Cooperation Council (GCC) countries, particularly for smart building technologies in UAE and Saudi Arabia. South Africa leads in mining safety applications, while North African nations are adopting medical thermopiles for pandemic preparedness. The market suffers from fragmented distribution networks and low awareness of advanced sensing solutions outside oil/gas sectors. However, megaprojects like NEOM in Saudi Arabia are expected to drive demand for environmental monitoring sensors. Price competition from Asian suppliers and delayed technology transfer remain barriers to widespread implementation.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Thermopile Sensors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermopile Sensors Market?

-> Thermopile Sensors Market was valued at USD 387.2 million in 2024 and is projected to reach USD 623.4 million by 2032, at a CAGR of 6.13% during the forecast period 2025-2032.

Which key companies operate in Global Thermopile Sensors Market?

-> Key players include Excelitas Technologies, Flir Systems, Texas Instruments, Hamamatsu Photonic, TE Connectivity, and Murata, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for non-contact temperature measurement, increasing adoption in automotive applications, and growing IoT deployments.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 40% share, driven by manufacturing growth in China and Japan, while North America leads in technological advancements.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for predictive maintenance, and development of MEMS-based thermopile sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...