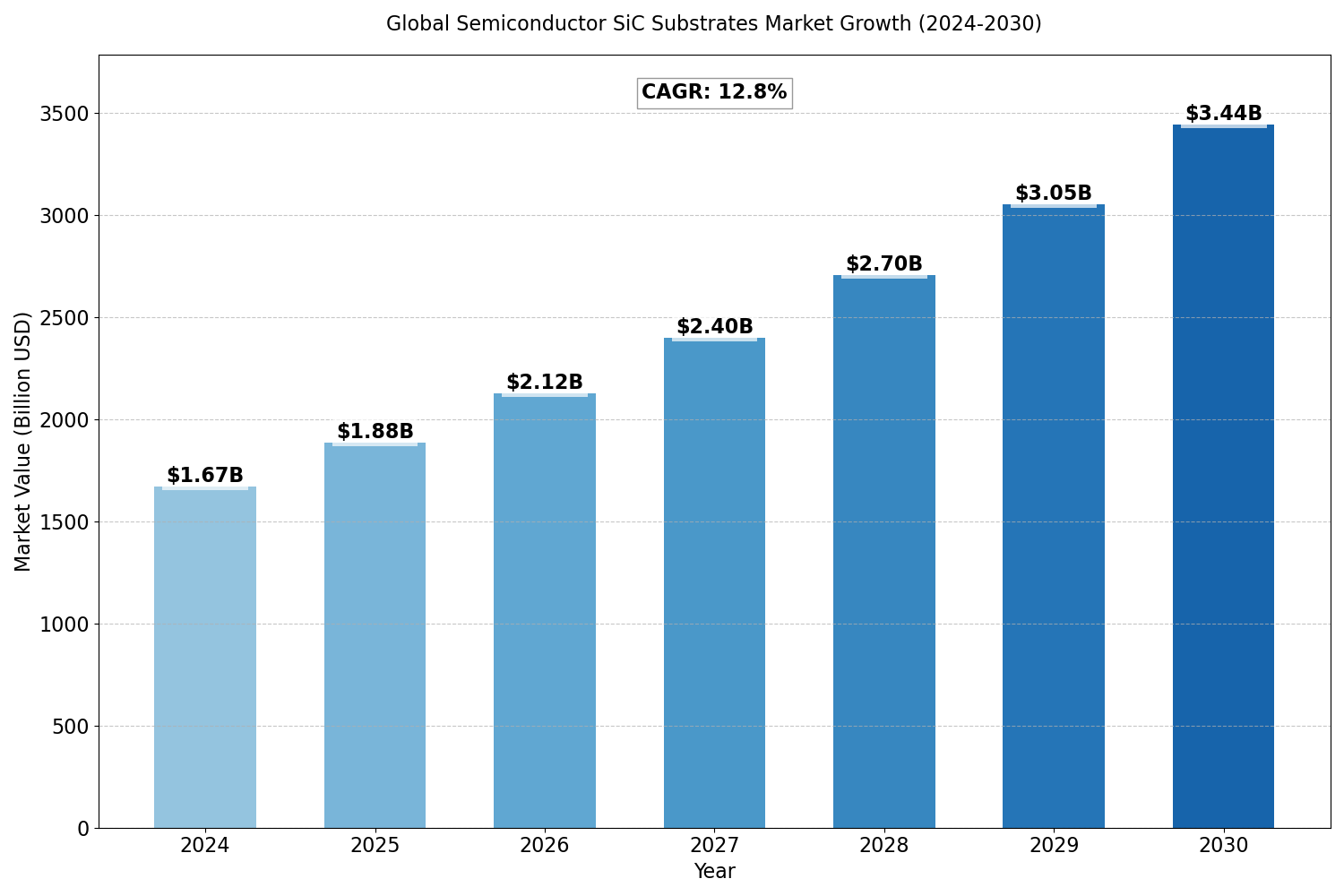

The Global Semiconductor SiC Substrates Market size was valued at US$ 1.67 billion in 2024 and is projected to reach US$ 3.44 billion by 2030, at a CAGR of 12.8% during the forecast period 2024-2030.

The United States Semiconductor SiC Substrates market size was valued at US$ 437.5 million in 2024 and is projected to reach US$ 876.4 million by 2030, at a CAGR of 12.3% during the forecast period 2024-2030.

Silicon carbide substrate materials for power semiconductor devices.

Report Overview

This report provides a deep insight into the global Semiconductor SiC Substrates market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Semiconductor SiC Substrates Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Semiconductor SiC Substrates market in any manner.

Global Semiconductor SiC Substrates Market: Market Segmentation Analysis

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Cree

- II-VI Advanced Materials

- TankeBlue

- SICC Materials

- CENGOL

- Showa Denko (NSSMC)

- Synlight

- Norstel

- SK Siltron

- ROHM

- 4 Inches

- 6 Inches

- Others

- Power Component

- RF Device

- Others

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- South America (Brazil, Argentina, Columbia, Rest of South America)

- The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Semiconductor SiC Substrates Market

- Overview of the regional outlook of the Semiconductor SiC Substrates Market:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Drivers

- Growing Demand for Electric Vehicles (EVs)

The rapid rise in EV adoption has spurred the need for advanced power electronics, particularly for EV charging systems and motor drives. Silicon carbide (SiC) substrates, with their superior performance in high-voltage and high-temperature environments, are crucial for these applications. SiC-based power devices offer improved efficiency, faster switching, and reduced energy losses, making them highly sought after in the EV market. - Advancements in Renewable Energy and Power Conversion Systems

SiC substrates are essential for the energy-efficient conversion of renewable energy, such as solar and wind. In power conversion systems, SiC devices can handle high-power and high-frequency operations, improving energy efficiency and reliability. This has led to increased demand in sectors like grid management, power supplies, and inverters. - Wide Temperature and Voltage Tolerance

SiC substrates have a high thermal conductivity and can withstand higher temperatures and voltages compared to traditional silicon. This makes SiC ideal for applications requiring high power and thermal efficiency, such as power electronics, aerospace, and industrial motor drives. This broadens the market for SiC substrates across diverse sectors. - Miniaturization of Electronic Devices

SiC’s ability to operate at higher frequencies and handle higher power in a smaller form factor is driving its adoption in compact electronic devices. As consumer electronics and industrial applications demand more compact, efficient, and robust power components, SiC substrates are increasingly being used.

Restraints

- High Production Costs

The production of SiC substrates is expensive compared to traditional silicon substrates. The cost of manufacturing SiC wafers, especially at larger diameters and higher purity levels, can significantly impact the cost of devices, limiting the adoption of SiC technologies in price-sensitive applications. - Limited Availability of Large-Diameter Wafers

While SiC technology has advanced, there is still a shortage of large-diameter wafers, particularly above 6 inches. This restricts scalability for mass production and increases the cost per wafer, limiting the widespread use of SiC in some industries, particularly consumer electronics. - Challenges in Material Quality and Yield

Achieving consistent material quality and high yields in SiC wafer production remains a challenge. Impurities and defects in SiC wafers can lead to lower device performance, which increases costs and reduces the reliability of SiC-based products.

Opportunities

- Expansion in Automotive Industry

As electric vehicles (EVs) and hybrid vehicles become more common, the demand for high-efficiency power electronics in automotive applications continues to rise. SiC substrates are highly effective in automotive power systems, particularly in electric drive systems, charging stations, and energy recovery systems, offering significant growth opportunities in this sector. - Development of 200mm Wafers

Significant research and development are focused on expanding the size of SiC wafers beyond the current 150mm diameter. The adoption of 200mm wafers could drastically lower manufacturing costs and improve yields, making SiC-based solutions more affordable for a wider range of applications, particularly in consumer electronics and renewable energy sectors. - Government Incentives for Green Technologies

As governments worldwide continue to push for greener, more energy-efficient technologies, there are numerous opportunities for SiC substrates in renewable energy, electric vehicles, and other power electronics applications. Incentives and subsidies for green technologies could further boost the adoption of SiC in these areas. - Integration with 5G and Telecommunications

SiC substrates can play a crucial role in next-generation telecommunications equipment, including 5G base stations, by supporting high-frequency and high-power components. As the global rollout of 5G continues, the demand for SiC power devices is expected to rise, creating new market opportunities.

Challenges

- Technical Hurdles in Scaling Production

While the potential for SiC in high-power and high-temperature applications is clear, scaling up production to meet global demand remains a significant hurdle. Increasing the size and volume of SiC wafers without compromising on material quality is a critical challenge for manufacturers. - Competition from Alternative Materials

While SiC offers several advantages, it faces stiff competition from other wide-bandgap materials, such as gallium nitride (GaN). GaN is also being used in power electronics and telecommunications applications and is considered by some to be a more cost-effective alternative for certain use cases. The competition from these materials could limit the growth potential for SiC substrates in some segments. - Slow Adoption in Some Industrial Segments

Despite the growing interest in SiC, its adoption in some industrial applications, particularly where silicon-based devices are well-established, is slow. The transition from silicon to SiC in power electronics and other areas requires significant investments in infrastructure and training, which could delay broader market penetration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...