Semiconductor Manufacturing Materials Market Overview

Semiconductor Manufacturing Materials mainly refer to various materials required in the process of processing silicon wafers or compound semiconductors into chips.

This report provides a deep insight into the global Semiconductor Manufacturing Materials market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Semiconductor Manufacturing Materials Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Semiconductor Manufacturing Materials market in any manner.

Semiconductor Manufacturing Materials Market Analysis:

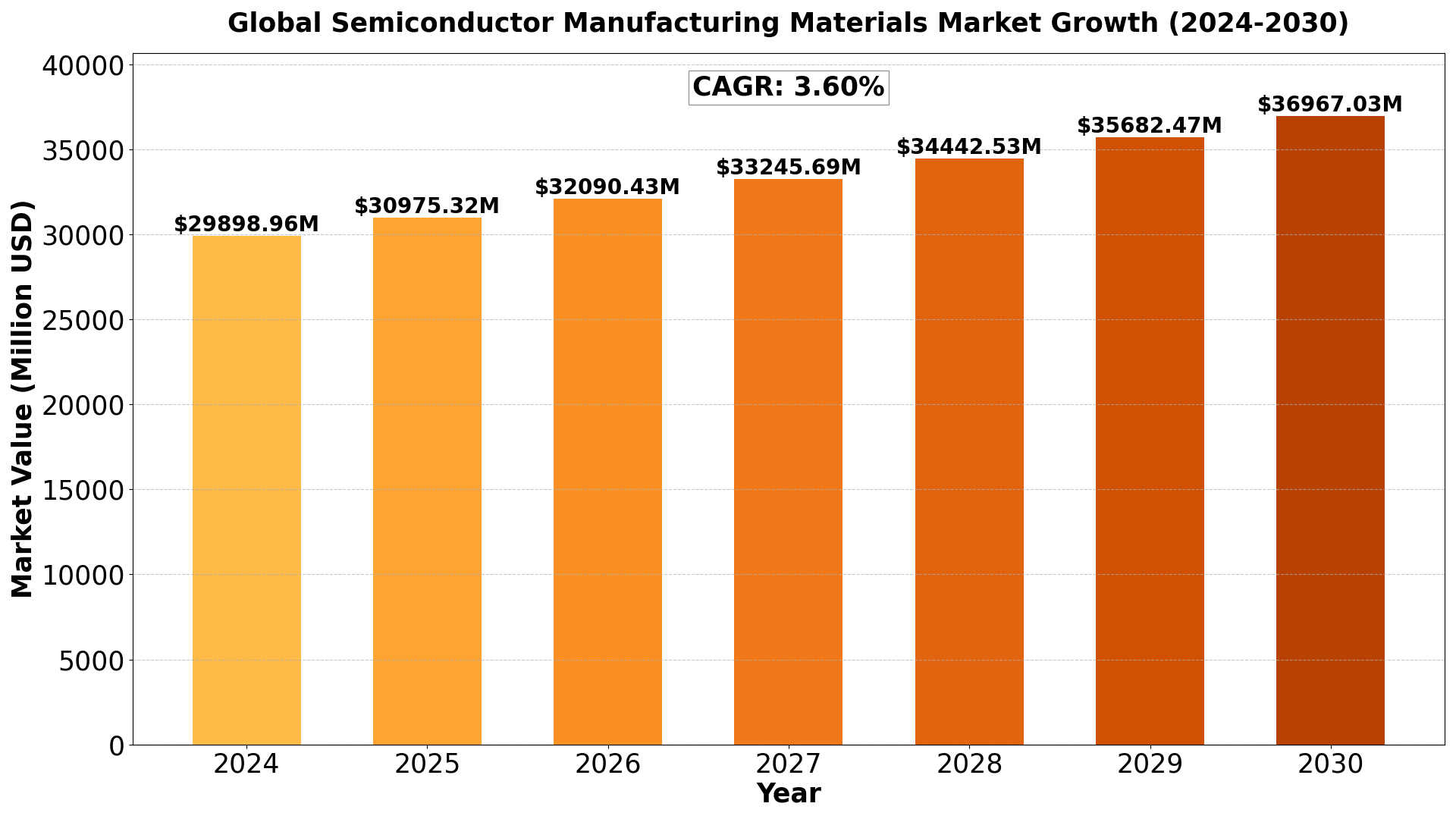

The Global Semiconductor Manufacturing Materials Market size was estimated at USD 28860 million in 2023 and is projected to reach USD 36967.03 million by 2030, exhibiting a CAGR of 3.60% during the forecast period.

North America Semiconductor Manufacturing Materials market size was USD 7520.09 million in 2023, at a CAGR of 3.09% during the forecast period of 2024 through 2030.

Semiconductor Manufacturing Materials Key Market Trends :

1. Rising Demand for Advanced Semiconductor Technologies

As semiconductor manufacturers move towards smaller process nodes (e.g., 7nm, 5nm, and even 3nm), the demand for specialized materials has increased. Advanced materials such as high-quality photoresists, deposition chemicals, and etching gases are required to produce smaller and more powerful chips that meet the growing performance and power efficiency demands of industries like AI, data centers, and consumer electronics. This transition to advanced semiconductor technologies is driving the need for innovative manufacturing materials that support these next-generation production processes.

2. Increasing Application of Semiconductors in Automotive Electronics

The automotive sector is becoming one of the largest consumers of semiconductor components, particularly with the rise of electric vehicles (EVs) and autonomous driving technologies. Automotive electronics require semiconductors for power management, in-vehicle networking, infotainment systems, and advanced driver-assistance systems (ADAS). As automotive manufacturers increase their reliance on semiconductor chips, the demand for high-quality manufacturing materials that ensure reliability, performance, and safety in these applications is growing. Materials that can withstand harsh automotive environments (e.g., high temperatures, vibrations, and exposure to chemicals) are particularly sought after.

3. Focus on Sustainability and Environmental Compliance

The semiconductor industry is increasingly focusing on sustainability, driven by both regulatory pressures and a commitment to reducing environmental impact. Manufacturers are seeking materials that are more eco-friendly, energy-efficient, and compliant with environmental regulations. The development of green technologies, such as low-emission chemicals and recyclable materials, is becoming a key focus. Additionally, the increasing push for energy-efficient chips and processes is prompting the adoption of materials that minimize waste and reduce the carbon footprint of semiconductor manufacturing.

4. Growth of 5G Networks and IoT

The rollout of 5G networks and the proliferation of IoT devices are driving substantial demand for semiconductors, as these technologies require high-performance chips that can handle large volumes of data at faster speeds. The production of such advanced semiconductors requires specialized materials, including high-quality substrates, packaging materials, and specialized chemicals for etching and deposition processes. As the adoption of 5G and IoT expands, the need for semiconductor manufacturing materials will continue to rise, supporting the growth of the market.

5. Technological Advancements in Semiconductor Manufacturing

As semiconductor manufacturing processes evolve, new materials and processes are being developed to enable even more precise and efficient production techniques. The adoption of Extreme Ultraviolet (EUV) Lithography, for example, is revolutionizing the production of smaller nodes, and it requires highly specialized materials, such as advanced photoresists and mask blanks. The rise of 3D IC packaging and heterogeneous integration is also fueling demand for innovative materials that support these advanced packaging solutions. As these technologies mature, the market for semiconductor manufacturing materials will continue to expand, with an increasing emphasis on precision, quality, and performance.

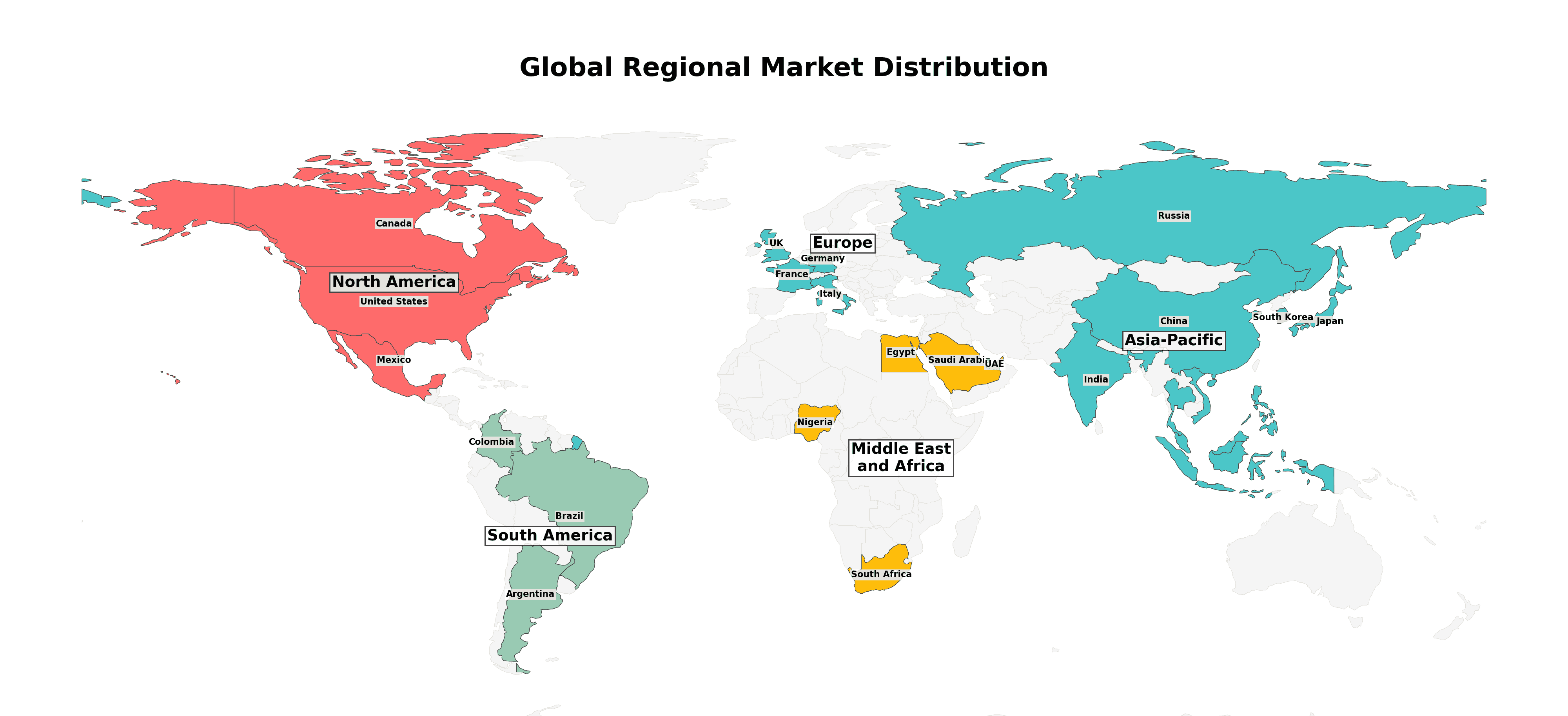

Semiconductor Manufacturing Materials Market Regional Analysis :

1. North America (USA, Canada, Mexico)

- USA: The largest market in the region due to advanced infrastructure, high disposable income, and technological advancements. Key industries include technology, healthcare, and manufacturing.

- Canada: Strong market potential driven by resource exports, a stable economy, and government initiatives supporting innovation.

- Mexico: A growing economy with strengths in automotive manufacturing, agriculture, and tourism, benefitting from trade agreements like the USMCA.

2. Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Germany: The region’s industrial powerhouse with a focus on engineering, automotive, and machinery.

- UK: A hub for financial services, fintech, and pharmaceuticals, though Brexit has altered trade patterns.

- France: Strong in luxury goods, agriculture, and aerospace with significant innovation in renewable energy.

- Russia: Resource-driven economy with strengths in oil, gas, and minerals but geopolitical tensions affect growth.

- Italy: Known for fashion, design, and manufacturing, especially in luxury segments.

- Rest of Europe: Includes smaller yet significant economies like Spain, Netherlands, and Switzerland with strengths in finance, agriculture, and manufacturing.

3. Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- China: The largest market in the region with a focus on technology, manufacturing, and e-commerce. Rapid urbanization and middle-class growth fuel consumption.

- Japan: Technological innovation, particularly in robotics and electronics, drives the economy.

- South Korea: Known for technology, especially in semiconductors and consumer electronics.

- India: Rapidly growing economy with strengths in IT services, agriculture, and pharmaceuticals.

- Southeast Asia: Key markets like Indonesia, Thailand, and Vietnam show growth in manufacturing and tourism.

- Rest of Asia-Pacific: Emerging markets with growing investment in infrastructure and services.

4. South America (Brazil, Argentina, Colombia, Rest of South America)

- Brazil: Largest economy in the region, driven by agriculture, mining, and energy.

- Argentina: Known for agriculture exports and natural resources but faces economic instability.

- Colombia: Growing economy with strengths in oil, coffee, and flowers.

- Rest of South America: Includes Chile and Peru, which have strong mining sectors.

5. The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Saudi Arabia: Oil-driven economy undergoing diversification with Vision 2030 initiatives.

- UAE: Financial hub with strengths in tourism, real estate, and trade.

- Egypt: Growing infrastructure development and tourism.

- Nigeria: Largest economy in Africa with strengths in oil and agriculture.

- South Africa: Industrialized economy with strengths in mining and finance.

- Rest of MEA: Includes smaller yet resource-rich markets like Qatar and Kenya with growing infrastructure investments.

Semiconductor Manufacturing Materials Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Shin-Etsu Chemical

- Kanto Denka

- Tokyo Ohka Kogyo

- HOYA Corporation

- DNP Fine Chemicals

- JSR Corporation

- Fujifilm

- Dow

- KMG Chemicals

- Merck

- Photronics

- Air Products

- Dongjin Semichem

- S&S Tech

- Linde

- Air Liquide

Market Segmentation (by Type)

- Photoresists

- Wet Chemicals

- Sputtering Targets

- Polishing Materials

- Photomasks

- Gases

- Others

Market Segmentation (by Application)

- Semiconductors

- Photovoltaic Cells

- Flat Panel Displays

- Others

Drivers:

- Increasing Demand for Semiconductor Devices: The global demand for semiconductor devices has been rising rapidly due to the proliferation of smart devices, IoT technologies, 5G infrastructure, automotive applications, and industrial automation. As more electronic devices are integrated into everyday life, the need for semiconductors has surged. This, in turn, drives the demand for the raw materials required to manufacture these semiconductors, including silicon wafers, rare earth metals, gases, and chemicals.

- Technological Advancements in Semiconductor Manufacturing: As semiconductor technology continues to evolve, with advancements like extreme ultraviolet (EUV) lithography and smaller process nodes, the need for highly specialized materials is increasing. These materials must meet stricter requirements for purity, performance, and precision, thus driving the demand for high-quality and advanced manufacturing materials.

- Growth in Automotive and Electric Vehicle Markets: The automotive industry is increasingly relying on semiconductors for power management, ADAS (advanced driver-assistance systems), electric vehicle (EV) batteries, and autonomous driving systems. The shift towards electric and autonomous vehicles presents a significant opportunity for semiconductor material suppliers. This includes materials used for power semiconductors, sensors, and memory chips used in automotive electronics.

- Advances in Data Centers and High-Performance Computing: The expansion of data centers, driven by cloud computing, artificial intelligence (AI), big data, and high-performance computing (HPC), is driving the demand for high-performance semiconductors. These advanced chips require specialized materials for production, including high-quality silicon wafers, copper interconnects, and advanced packaging materials.

- Growth of 5G Networks and Telecommunications: The deployment of 5G networks worldwide is one of the major drivers of semiconductor demand. The creation of 5G infrastructure and the need for high-frequency, low-latency devices such as smartphones, IoT devices, and networking equipment require advanced semiconductor materials, particularly in areas such as radio frequency (RF) components and power amplifiers.

Restraints:

- High Cost of Semiconductor Manufacturing Materials: The production of semiconductor materials, especially those that meet the stringent standards required for advanced nodes (like 7nm, 5nm, and 3nm), can be costly. The high prices of raw materials such as rare earth metals, advanced silicon wafers, and specialty chemicals can drive up the overall production costs for semiconductor manufacturers. This may, in turn, result in higher prices for end-products, which can affect demand.

- Supply Chain Vulnerabilities: The semiconductor materials market is heavily dependent on global supply chains for raw materials, which can be susceptible to disruptions. Natural disasters, geopolitical tensions, trade restrictions, and other disruptions can impact the availability and cost of key materials, including rare earth metals, gases, and chemicals. Such supply chain challenges can delay production timelines and increase costs for semiconductor manufacturers.

- Environmental and Regulatory Challenges: The production and disposal of semiconductor materials can have environmental implications. Semiconductor manufacturing involves the use of hazardous chemicals and gases, which require strict adherence to environmental and safety regulations. Companies must ensure that their materials and processes comply with environmental standards, which can increase costs and operational complexity.

- Complexity of Advanced Materials Development: As semiconductor technologies advance, the materials required for production become more complex and specialized. For example, new materials such as graphene, gallium nitride (GaN), and silicon carbide (SiC) are being researched for use in next-generation semiconductor devices, but their development and integration into manufacturing processes are still in relatively early stages. The complexity of developing and scaling these materials poses a challenge to material suppliers and semiconductor manufacturers.

Opportunities:

- Development of Advanced Materials for Smaller Nodes: As semiconductor manufacturers continue to push toward smaller process nodes, there is an opportunity to innovate and provide materials that meet the needs of these advanced technologies. For example, materials that support extreme ultraviolet (EUV) lithography, advanced etching processes, and new transistor architectures like finFET and GAAFET will be in high demand. Companies that can develop new materials or improve existing ones to meet these requirements will have a significant competitive advantage.

- Rise of Semiconductor Materials for Automotive Electronics: The automotive industry’s increasing reliance on semiconductors, particularly for electric vehicles, autonomous driving, and smart sensors, presents a strong growth opportunity for semiconductor materials. Manufacturers can capitalize on the demand for power semiconductors, sensors, and memory chips designed specifically for automotive applications. This includes materials that offer durability, reliability, and high-performance capabilities in harsh automotive environments.

- Sustainability Initiatives and Green Technologies: As environmental concerns grow, there is increasing demand for sustainable and eco-friendly semiconductor manufacturing materials. Companies that can innovate in terms of reducing the environmental impact of material production, improving the recyclability of materials, or using greener alternatives for chemicals and gases in semiconductor processes will find increasing market opportunities.

- Increasing Investment in Semiconductor Production Capacity: Global investments in semiconductor manufacturing capacity are on the rise, especially in regions like the U.S., Europe, and Asia. These investments create opportunities for material suppliers to serve the growing demand for semiconductor components, as more fabs are built and upgraded to handle the next generation of semiconductor technologies.

- Next-Generation Semiconductor Materials: The ongoing development of next-generation materials such as gallium nitride (GaN), silicon carbide (SiC), and advanced polymers offers growth opportunities in areas such as power electronics, 5G technology, and electric vehicles. These materials are expected to play a key role in driving the efficiency and performance of power semiconductor devices and other high-performance applications.

Challenges:

- R&D and Innovation in Material Science: As semiconductor technology becomes more advanced, the demand for new and innovative materials increases. This requires significant investment in research and development (R&D) by material suppliers to develop and scale materials that meet the high-performance requirements of advanced semiconductor devices. The pace of technological innovation in semiconductor manufacturing materials is often a challenge for companies trying to stay competitive.

- Raw Material Shortages and Price Volatility: Some of the materials used in semiconductor manufacturing, such as rare earth metals (e.g., cobalt, lithium, tungsten), face supply constraints due to limited reserves, geopolitical factors, and mining challenges. These materials can experience price volatility, affecting production costs for semiconductor manufacturers and potentially leading to supply chain bottlenecks.

- High Capital Expenditure for New Facilities: The creation of new semiconductor manufacturing plants, or upgrading existing ones, requires substantial capital expenditure (CapEx) for new equipment, raw materials, and facilities. The cost of building fabs and the associated infrastructure can deter smaller players from entering the market and may put pressure on existing manufacturers to invest in maintaining their production capacity.

- Adherence to Stringent Standards and Compliance: Semiconductor manufacturing materials must meet stringent industry standards and specifications to ensure high performance, reliability, and safety. Maintaining compliance with regulatory requirements, particularly environmental and health safety standards, can be complex and costly for material suppliers.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Semiconductor Manufacturing Materials Market

- Overview of the regional outlook of the Semiconductor Manufacturing Materials Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q1. What is the Semiconductor Manufacturing Materials market?

A1. The Semiconductor Manufacturing Materials market involves the production and supply of raw materials used in the fabrication of semiconductor devices, including silicon wafers, photomasks, chemicals, gases, and other essential components for semiconductor production.

Q2. What is the current market size and forecast for the Semiconductor Manufacturing Materials market until 2030?

A2. The market size was estimated at USD 28,860 million in 2023 and is projected to reach USD 36,967.03 million by 2030, exhibiting a CAGR of 3.60% during the forecast period.

Q3. What are the key growth drivers in the Semiconductor Manufacturing Materials market?

A3. Key growth drivers include the growing demand for advanced semiconductor technologies, the rise of AI, 5G, and IoT applications, the increasing need for miniaturized chips, and the expansion of the semiconductor industry in emerging markets.

Q4. Which regions dominate the Semiconductor Manufacturing Materials market?

A4. Asia-Pacific leads the market, especially countries like Taiwan, South Korea, and China, which are major semiconductor manufacturing hubs. North America and Europe also contribute significantly due to strong semiconductor industries.

Q5. What are the emerging trends in the Semiconductor Manufacturing Materials market?

A5. Emerging trends include the development of advanced materials for next-generation semiconductor nodes, the use of eco-friendly and sustainable materials, and innovations in material solutions for advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...