Semiconductor CVD and PVD Equipment Market Overview

Semiconductor CVD (Chemical Vapor Deposition) and PVD (Physical Vapor Deposition) equipment are integral to the manufacturing of semiconductor devices and integrated circuits. These processes are used to deposit thin films of various materials onto semiconductor wafers, allowing the creation of intricate layers with specific properties required for the functionality of electronic components.

This report provides a deep insight into the global Semiconductor CVD and PVD Equipment market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Semiconductor CVD and PVD Equipment Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Semiconductor CVD and PVD Equipment market in any manner.

Semiconductor CVD and PVD Equipment Market Analysis:

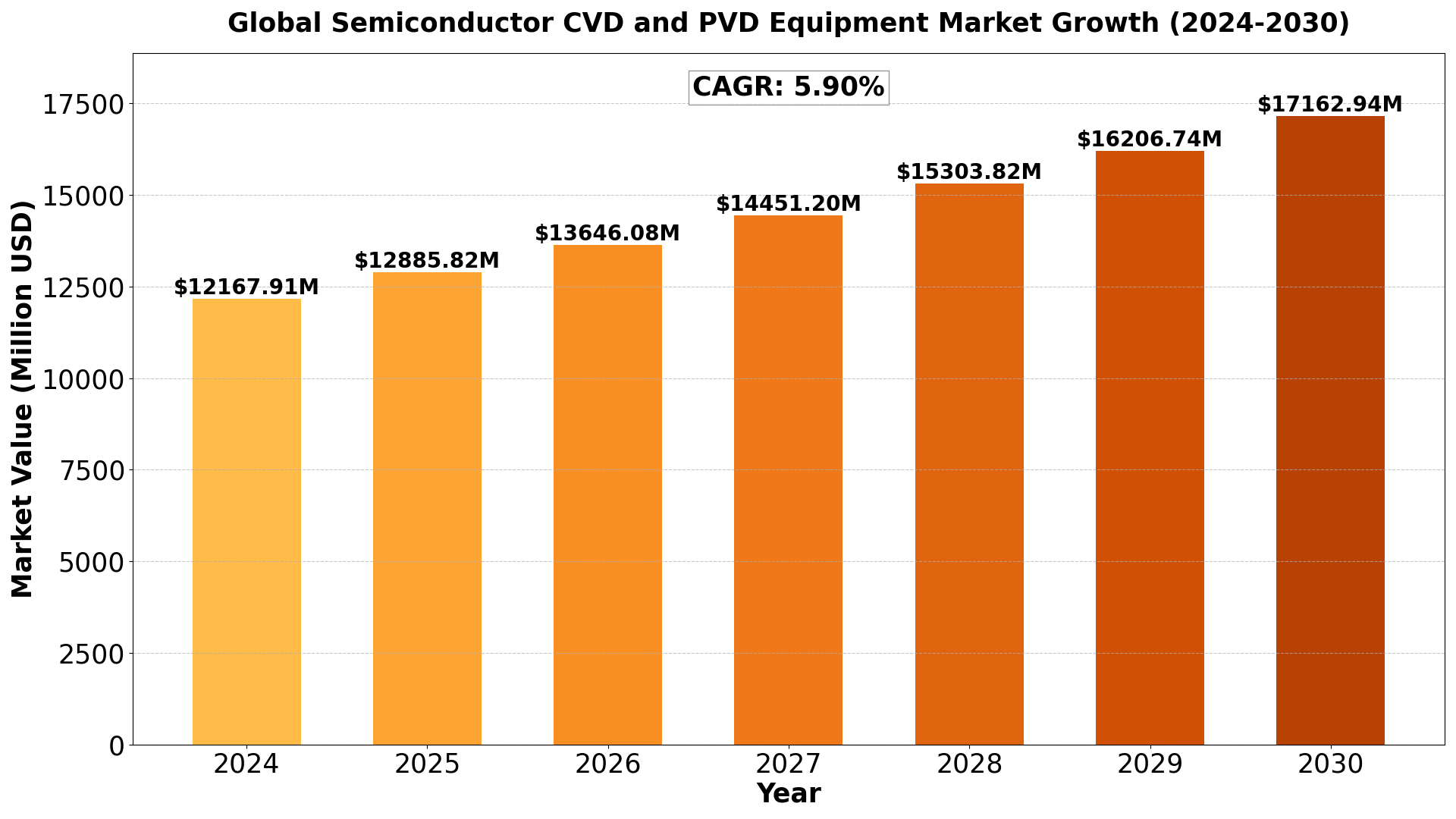

The Global Semiconductor CVD and PVD Equipment Market size was estimated at USD 11490 million in 2023 and is projected to reach USD 17162.94 million by 2030, exhibiting a CAGR of 5.90% during the forecast period.

North America Semiconductor CVD and PVD Equipment market size was USD 2993.97 million in 2023, at a CAGR of 5.06% during the forecast period of 2024 through 2030.

Semiconductor CVD and PVD Equipment Key Market Trends :

- Advancements in Deposition Technology: As semiconductor manufacturers continue to push for smaller, more efficient chips, there’s an increasing demand for advanced CVD and PVD technologies that offer better precision, uniformity, and control over thin film deposition. This trend is pushing companies to innovate and develop new equipment to meet the exacting standards of modern semiconductor fabrication.

- Increased Demand for 5G and AI: The widespread adoption of 5G technology and artificial intelligence (AI) applications is driving the demand for more sophisticated semiconductor devices. These technologies require advanced materials and components that can only be produced with high-performance CVD and PVD equipment, boosting the overall market.

- Miniaturization of Semiconductor Devices: As semiconductor devices become smaller and more compact, the need for equipment capable of working at nanometer scales is increasing. This trend pushes the development of CVD and PVD equipment with higher precision and the ability to handle ultra-thin layers.

- Focus on Sustainable and Energy-Efficient Solutions: There’s a growing emphasis on sustainability within the semiconductor manufacturing process. Companies are looking for CVD and PVD solutions that not only offer high throughput but also reduce energy consumption and waste. This is driving innovation in equipment design to make the process more environmentally friendly.

- Growth in Emerging Markets: The expansion of semiconductor manufacturing in regions such as Asia-Pacific, particularly in countries like China, South Korea, and Taiwan, is fueling demand for CVD and PVD equipment. As these regions continue to invest in semiconductor production capacity, the market for deposition equipment is expected to see robust growth.

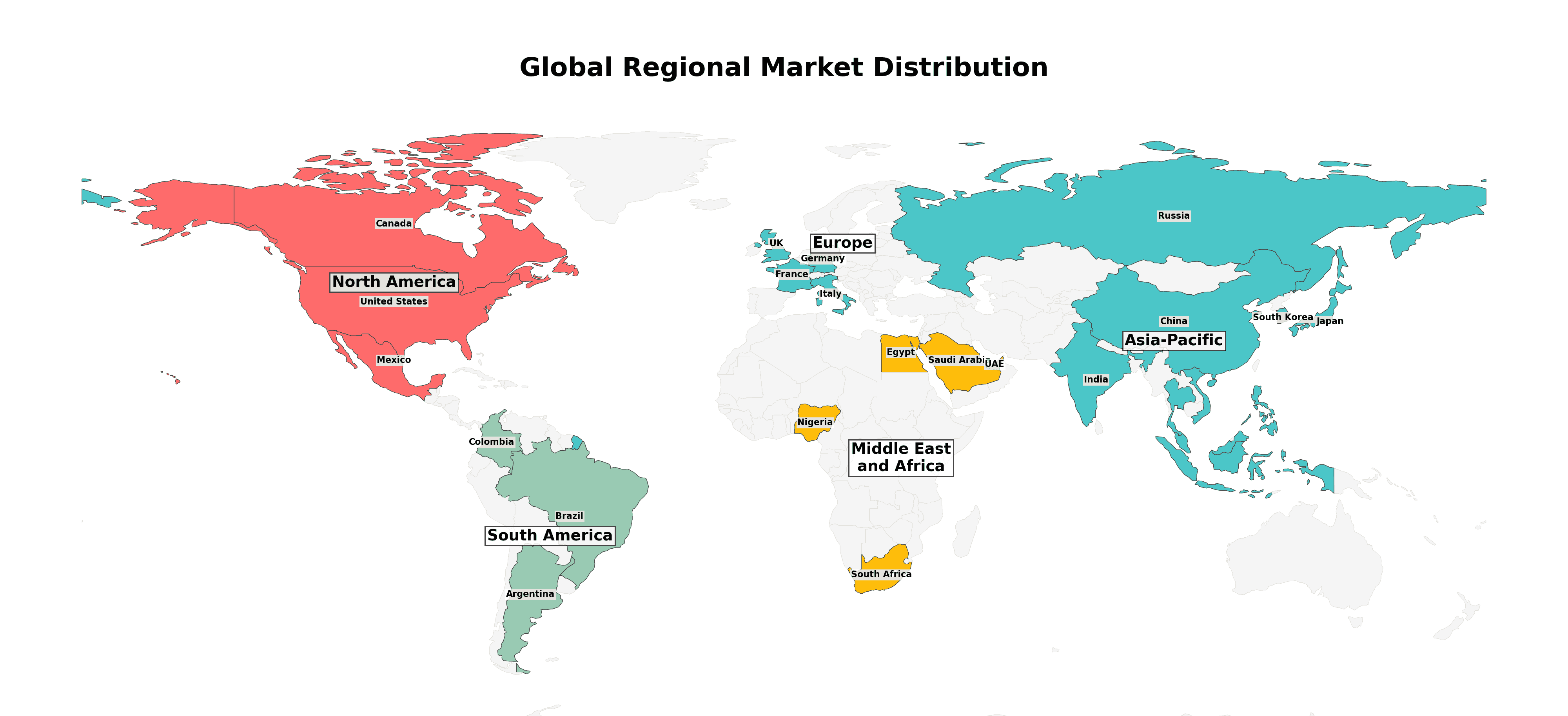

Semiconductor CVD and PVD Equipment Market Regional Analysis :

1. North America (USA, Canada, Mexico)

- USA: The largest market in the region due to advanced infrastructure, high disposable income, and technological advancements. Key industries include technology, healthcare, and manufacturing.

- Canada: Strong market potential driven by resource exports, a stable economy, and government initiatives supporting innovation.

- Mexico: A growing economy with strengths in automotive manufacturing, agriculture, and tourism, benefitting from trade agreements like the USMCA.

2. Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Germany: The region’s industrial powerhouse with a focus on engineering, automotive, and machinery.

- UK: A hub for financial services, fintech, and pharmaceuticals, though Brexit has altered trade patterns.

- France: Strong in luxury goods, agriculture, and aerospace with significant innovation in renewable energy.

- Russia: Resource-driven economy with strengths in oil, gas, and minerals but geopolitical tensions affect growth.

- Italy: Known for fashion, design, and manufacturing, especially in luxury segments.

- Rest of Europe: Includes smaller yet significant economies like Spain, Netherlands, and Switzerland with strengths in finance, agriculture, and manufacturing.

3. Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- China: The largest market in the region with a focus on technology, manufacturing, and e-commerce. Rapid urbanization and middle-class growth fuel consumption.

- Japan: Technological innovation, particularly in robotics and electronics, drives the economy.

- South Korea: Known for technology, especially in semiconductors and consumer electronics.

- India: Rapidly growing economy with strengths in IT services, agriculture, and pharmaceuticals.

- Southeast Asia: Key markets like Indonesia, Thailand, and Vietnam show growth in manufacturing and tourism.

- Rest of Asia-Pacific: Emerging markets with growing investment in infrastructure and services.

4. South America (Brazil, Argentina, Colombia, Rest of South America)

- Brazil: Largest economy in the region, driven by agriculture, mining, and energy.

- Argentina: Known for agriculture exports and natural resources but faces economic instability.

- Colombia: Growing economy with strengths in oil, coffee, and flowers.

- Rest of South America: Includes Chile and Peru, which have strong mining sectors.

5. The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Saudi Arabia: Oil-driven economy undergoing diversification with Vision 2030 initiatives.

- UAE: Financial hub with strengths in tourism, real estate, and trade.

- Egypt: Growing infrastructure development and tourism.

- Nigeria: Largest economy in Africa with strengths in oil and agriculture.

- South Africa: Industrialized economy with strengths in mining and finance.

- Rest of MEA: Includes smaller yet resource-rich markets like Qatar and Kenya with growing infrastructure investments.

Semiconductor CVD and PVD Equipment Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Applied Materials

- Lam Research Corporation

- Tokyo Electron Limited

- ASM International

- Kokusai Electric

- Wonik IPS

- Eugene Technology

- Jusung Engineering

- TES

- SPTS Technologies (KLA)

- Veeco

- CVD Equipment

- Piotech Inc.

- NAURA Technology Group Co.,Ltd.

- Evatec

- Ulvac

- KLA Corporation

- Semiconductor CVD Equipment

- Semiconductor PVD Equipment

- Foundry

- IDM Enterprise

Drivers

- Technological Advancements in Semiconductor Manufacturing:

- With the advent of more advanced semiconductor nodes (such as 7nm, 5nm, and 3nm), the need for precise and efficient deposition techniques like CVD and PVD has increased. These technologies enable the formation of ultra-thin, high-quality films required for modern semiconductors.

- Rising Demand for Consumer Electronics:

- The growing demand for smartphones, wearables, laptops, and other consumer electronics is a key driver. As these devices become more powerful, energy-efficient, and compact, the demand for high-performance semiconductors with advanced deposition coatings increases.

- Increasing Use in Automotive Electronics:

- The automotive sector is adopting advanced electronics, including semiconductors for electric vehicles (EVs), autonomous driving, and infotainment systems. This surge in demand for automotive semiconductors drives the need for CVD and PVD equipment.

- Growth in Data Centers and Cloud Computing:

- With the rise in cloud computing, big data, and AI applications, data centers require more efficient, high-capacity semiconductor devices. This is pushing for continuous improvements in semiconductor manufacturing processes, benefiting the CVD and PVD equipment market.

- Miniaturization of Electronics:

- The push for smaller and more efficient devices with better performance is leading to more sophisticated and fine-tuned deposition processes. CVD and PVD technologies are integral in meeting these demands.

Restraints

- High Capital Investment:

- The initial cost of acquiring CVD and PVD equipment can be prohibitively expensive for smaller companies or startups. This high capital expenditure can be a barrier to entry, limiting the expansion of the market.

- Complexity and Maintenance:

- Both CVD and PVD techniques are highly complex, requiring specialized skills for operation, maintenance, and troubleshooting. This complexity, along with the need for regular maintenance, can be a burden for manufacturers, especially when managing multiple machines.

- Environmental and Health Concerns:

- Some of the chemicals used in CVD processes can be hazardous to both the environment and the workforce. Stricter regulations and environmental policies may increase the cost of compliance and affect the market’s growth.

- Technological Obsolescence:

- The rapid pace of technological advancements means that existing equipment can quickly become outdated. Manufacturers may face challenges in keeping up with the latest innovations, leading to costly upgrades and replacements.

Opportunities

- Emerging Applications in 5G and IoT:

- The demand for semiconductors in 5G infrastructure and Internet of Things (IoT) devices is creating new opportunities for deposition equipment. As 5G networks expand globally, the need for specialized semiconductor materials and coatings will continue to rise.

- Advancements in Materials Science:

- New materials such as high-κ dielectrics, advanced semiconductors, and organic electronics are creating new possibilities for CVD and PVD. As the materials used in semiconductor devices evolve, there is an opportunity for the equipment market to innovate and create new solutions.

- Rise in Demand for Energy-efficient Devices:

- The growing need for energy-efficient and sustainable devices, such as low-power semiconductors for wearable technologies, opens up new growth avenues. CVD and PVD equipment manufacturers can capitalize on the development of thin films that are more energy-efficient.

- Regional Expansion:

- As the semiconductor industry expands in regions like Asia-Pacific, Latin America, and Eastern Europe, the demand for advanced deposition technologies increases. Companies in these regions may look to invest in CVD and PVD equipment to meet the growing demand for semiconductor devices.

- Increased Investment in R&D:

- Increased investments from semiconductor manufacturers in R&D to develop next-generation chips and devices create significant opportunities for CVD and PVD equipment makers. R&D-driven innovation leads to the development of more efficient, cost-effective, and precise deposition techniques.

Challenges

- Supply Chain Disruptions:

- The global semiconductor supply chain has faced disruptions due to factors such as the COVID-19 pandemic, geopolitical tensions, and raw material shortages. These disruptions can affect the availability of components needed for CVD and PVD equipment and slow down production timelines.

- Intense Competition:

- The semiconductor equipment market is highly competitive, with a few large players dominating the market. This intense competition puts pressure on companies to constantly innovate and reduce costs while maintaining quality.

- Scaling Challenges:

- As semiconductor manufacturing moves toward smaller nodes (e.g., below 5nm), scaling up deposition processes becomes increasingly challenging. The precision required for such advanced processes can strain existing CVD and PVD technologies, requiring substantial R&D investments to overcome these limitations.

- Regulatory Compliance:

- Stringent regulatory requirements related to environmental and safety standards can pose challenges for equipment manufacturers, adding complexity and cost to the development and deployment of CVD and PVD technologies.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Semiconductor CVD and PVD Equipment Market

- Overview of the regional outlook of the Semiconductor CVD and PVD Equipment Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q1: What are Semiconductor CVD and PVD Equipment?

A1: Semiconductor CVD (Chemical Vapor Deposition) and PVD (Physical Vapor Deposition) Equipment are used in the semiconductor manufacturing process to deposit thin films onto substrates. CVD involves chemical reactions to form films, while PVD uses physical processes like vaporization to deposit materials.

Q2: What is the current market size and forecast for the Semiconductor CVD and PVD Equipment market until 2032?

A2: The global Semiconductor CVD and PVD Equipment market size was valued at USD 11,490 million in 2023 and is projected to reach USD 17,162.94 million by 2030, with a CAGR of 5.90% during the forecast period.

Q3: What are the key growth drivers in the Semiconductor CVD and PVD Equipment market?

A3: Key growth drivers include the increasing demand for semiconductors in electronics, advancements in semiconductor manufacturing technology, rising demand for advanced devices like smartphones and 5G infrastructure, and the growing adoption of IoT and AI technologies.

Q4: Which regions dominate the Semiconductor CVD and PVD Equipment market?

A4: Asia-Pacific, particularly China, Japan, South Korea, and Taiwan, dominate the Semiconductor CVD and PVD Equipment market due to the presence of major semiconductor manufacturers.

Q5: What are the emerging trends in the Semiconductor CVD and PVD Equipment market?

A5: Emerging trends include the development of advanced materials, miniaturization of semiconductor devices, increased focus on energy-efficient equipment, and the adoption of automation and AI in semiconductor manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...