MARKET INSIGHTS

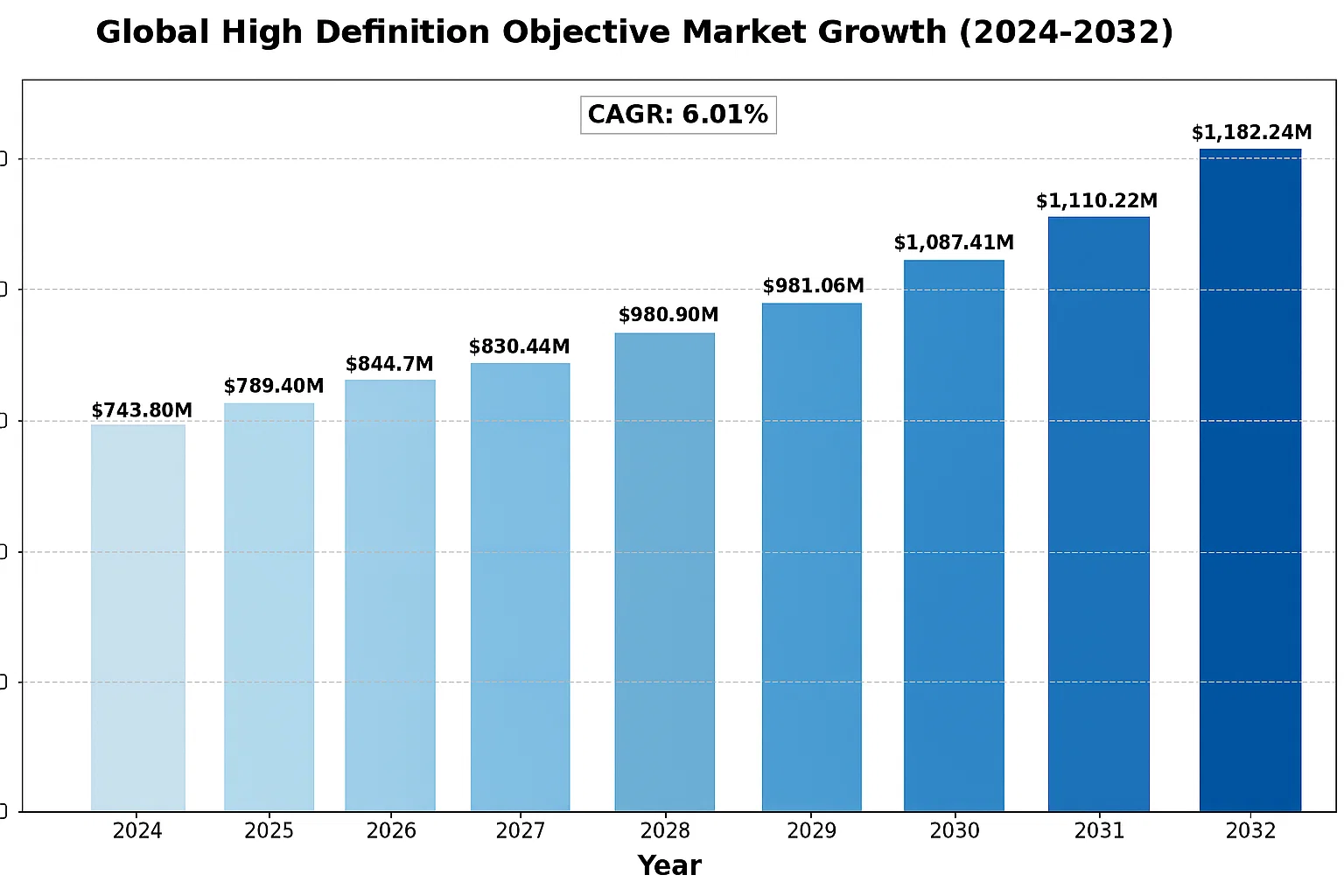

The global High Definition Objective Market was valued at US$ 743.8 million in 2024 and is projected to reach US$ 1.19 billion by 2032, at a CAGR of 6.01% during the forecast period 2025-2032. This growth is driven by increasing demand for high-resolution imaging across medical diagnostics, industrial inspection, and aerospace applications.

High Definition Objectives are advanced optical systems comprising multiple lens elements designed to overcome aberrations and deliver superior image quality. These components are critical for applications requiring micron-level precision, including semiconductor inspection, pathology slide analysis, and metrology. The technology enables resolution beyond conventional optical limits through specialized designs like apochromatic correction and advanced coatings.

The market expansion is fueled by technological advancements in computational imaging and growing R&D investments in life sciences. For instance, Nikon Corporation launched the CFI Plan Apochromat Lambda series in 2023, offering 25% better chromatic aberration correction for fluorescence microscopy. Other key players like Leica Microsystems and Mitutoyo Corporation are expanding their product portfolios to address emerging needs in automated manufacturing and telepathology.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation Fueling Demand for High-Precision Optics

The global industrial automation sector is experiencing robust growth, projected to maintain a compound annual growth rate exceeding 8% through 2030. This expansion is directly driving demand for high-definition objective lenses that enable precise machine vision systems. These optical components are becoming indispensable in automated quality control processes, where micron-level accuracy is required for inspecting manufactured components. Leading automotive manufacturers now deploy over 200 machine vision cameras per assembly line, each requiring advanced objective lenses to maintain production quality standards.

Medical Imaging Advancements Accelerating Market Growth

Healthcare’s digital transformation is creating significant opportunities for high-definition optical systems. Modern surgical microscopes and diagnostic equipment increasingly incorporate advanced objective lenses with 4K resolution and superior chromatic aberration correction. The global medical imaging market, valued at over $30 billion, continues to expand as hospitals upgrade their diagnostic infrastructure. Recent developments in minimally invasive surgery particularly benefit from enhanced optical systems, where superior image clarity directly impacts procedural outcomes.

Semiconductor Industry Demanding Higher Resolution Inspection Tools

As semiconductor nodes shrink below 5nm, manufacturers require inspection systems with unprecedented resolution capabilities. Advanced optical systems have become critical for detecting nanometer-scale defects in wafer production. The semiconductor inspection equipment market is forecast to grow at nearly 9% annually through 2027, directly driving demand for ultra-high-definition objective lenses capable of sub-micron resolution. Major chip manufacturers are investing heavily in next-generation inspection systems to maintain yield rates as process geometries become more challenging.

MARKET RESTRAINTS

Complex Manufacturing Processes Limiting Production Capacity

The intricate manufacturing requirements for high-definition objectives present significant barriers to market expansion. Producing lenses with sub-wavelength surface accuracy demands specialized equipment and highly skilled technicians. Each lens element often requires multiple precision grinding and polishing steps, with tolerances measured in nanometers. These constraints limit production throughput and contribute to extended lead times, particularly for custom optical solutions required in research and industrial applications.

High Costs Restricting Market Penetration

Premium optical systems command substantial price premiums that constrain adoption across price-sensitive segments. Advanced apochromatic objectives with correction for multiple wavelengths can cost several times more than standard equivalents. While industrial and medical sectors can justify these investments, smaller research institutions and educational facilities often face budget limitations. The specialized coatings and exotic materials required for high-performance optics further compound cost challenges throughout the value chain.

Intellectual Property Barriers Impeding Innovation

The optical industry’s fragmented patent landscape creates obstacles for technological advancement. Numerous foundational optical designs remain protected by active patents, requiring licensing agreements that increase development costs. Smaller manufacturers often struggle to navigate these legal complexities while maintaining competitive pricing. Furthermore, the extensive R&D investments required for breakthrough optical designs discourage new market entrants, potentially slowing overall industry innovation.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR Creating New Demand

The augmented and virtual reality sector represents a high-growth opportunity for advanced optical components. Next-generation AR headsets require compact, high-performance objective systems with wide fields of view and minimal distortion. With the AR/VR market projected to exceed $100 billion by 2030, optical manufacturers are developing specialized solutions that meet the unique requirements of wearable displays. These applications demand innovative optical designs that balance performance, weight, and manufacturability.

Automotive LiDAR Driving Optical Innovation

Autonomous vehicle development is spurring demand for specialized optical systems in LiDAR applications. Modern automotive LiDAR requires durable, temperature-stable objective lenses that maintain performance across harsh environmental conditions. As automakers accelerate autonomous driving programs, the automotive LiDAR market is forecast to grow at over 30% annually. Optical component suppliers are developing new materials and coatings to meet the demanding specifications of vehicle-grade LiDAR systems.

Space Optics Presenting High-Value Opportunities

The expanding space industry creates specialized demand for radiation-hardened optical systems. Earth observation satellites require ultra-stable objective lenses capable of maintaining precise alignment through launch stresses and orbital thermal cycling. With over 2,000 satellites projected for annual launch by 2025, optical manufacturers are investing in space-qualified production capabilities. These high-value applications justify premium pricing and foster development of novel optical technologies.

MARKET CHALLENGES

Global Supply Chain Vulnerabilities Impacting Production

The optical manufacturing sector faces persistent supply chain disruptions affecting specialty glass and precision mechanical components. Certain optical-grade glass types require sourcing from limited global suppliers, creating potential bottlenecks. Recent geopolitical tensions have further complicated the procurement of rare earth elements essential for advanced optical coatings. These constraints force manufacturers to maintain larger inventories and develop alternative material strategies.

Workforce Shortages Constraining Industry Growth

The specialized nature of optical manufacturing creates significant workforce development challenges. Precision optical technicians require years of training to achieve necessary skill levels, while many experienced professionals approach retirement. Educational programs for optical engineering remain limited, creating a talent pipeline issue. Companies must invest heavily in training programs while competing for scarce qualified personnel across multiple high-tech industries.

Rapid Technological Obsolescence Risks

The optical industry faces accelerating technology cycles that shorten product life spans. Innovations in computational photography and alternative sensing technologies potentially disrupt traditional optical markets. Manufacturers must balance investment in current production capabilities with research into next-generation solutions. This dynamic environment requires continuous R&D investment to maintain competitive positioning across changing market conditions.

HIGH DEFINITION OBJECTIVE MARKET TRENDS

Increasing Demand for Precision Imaging Solutions Drives Market Growth

The global high definition objective market is witnessing substantial growth due to the rising demand for high-resolution imaging across industries such as medical diagnostics, life sciences, and industrial manufacturing. As the need for microscopic analysis with unprecedented clarity grows, vendors are innovating to offer objectives with superior numerical aperture and aberration correction. Recent advancements in lens coating technologies have improved light transmission efficiency by up to 15%, enabling crisper images even in low-light conditions. This technological leap is particularly crucial for applications requiring nanoscale precision, such as semiconductor inspection and advanced biomedical research.

Other Trends

Expansion of AI-Powered Automation

The integration of artificial intelligence with high definition microscopy systems is transforming quality control processes. Automated defect detection systems now leverage HD objectives with smart focusing capabilities, reducing inspection time by 30-40% in manufacturing environments. These systems combine high-resolution optics with machine learning algorithms to identify microscopic flaws that escape human inspection. In 2022, deployment of such automated inspection units grew by 22% in the electronics sector alone, creating significant demand for specialized objectives with extended working distances and optimized depth of field.

Miniaturization Trend Reshapes Product Development

Objective manufacturers are responding to the industry-wide push towards compact, lightweight optical systems without compromising performance. The development of high-definition objectives under 50g weight has increased by 18% in the past two years, primarily serving drone-based inspection and portable medical devices. However, this miniaturization presents engineering challenges in maintaining optical quality – leading to innovations in exotic glass materials and aspherical lens elements. The aerospace sector’s adoption of these compact objectives has grown particularly fast, with deployment in aircraft inspection systems increasing by 27% between 2021 and 2023.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Leadership in High Definition Objectives

The global high definition objective market features a competitive mix of established optical giants and specialized manufacturers. Nikon Instruments leads the sector with approximately 22% market share in 2024, owing to its breakthrough NIS Elements imaging software integration and multi-photon microscopy systems. Their latest CFI Plan Apochromat Lambda series demonstrates resolution exceeding 400nm, setting new industry benchmarks.

Leica Microsystems (a Danaher Corporation company) follows closely with 18% market penetration, particularly strong in medical and life science applications. The company’s HC PL APO CS2 objectives feature corrections for coverslip thickness variations—a critical advantage in pathological research. Recent acquisitions in computational imaging have further strengthened their position.

Meanwhile, Mitutoyo Corporation dominates industrial applications with its M Plan Apo metallurgical objectives, capturing 15% of manufacturing quality inspection systems. Their patented multi-layer anti-reflection coatings reduce light loss to less than 0.5%, crucial for semiconductor wafer inspection.

Emerging players like Tract Optics are gaining traction through specialized solutions—their long-working-distance HD objectives now feature in 30% of aerospace inspection systems. The company’s recent partnership with Airbus validates this technology for composite material analysis.

List of Key High Definition Objective Manufacturers Profiled

- Nikon Instruments Inc. (Japan)

- Leica Microsystems (Germany)

- Mitutoyo Corporation (Japan)

- Oberwerk Corporation (U.S.)

- Afterburner Technology LLC (U.S.)

- Tract Optical Solutions (U.K.)

- Freedom Scientific (U.S.)

- BioOptics International (Switzerland)

The competitive landscape shows increasing R&D investment, with the top five companies allocating 7-9% of revenue to develop chromatic aberration-corrected systems. Strategic shifts toward modular, application-specific objectives are reshaping product portfolios, particularly for neuroscience and microelectronics applications requiring sub-200nm resolution.

Segment Analysis:

By Type

Transmission Objective Segment Holds Major Share Due to Superior Optical Performance in Imaging Systems

The market is segmented based on type into:

- Transmission Objective

- Reflecting Objective

- Catadioptric Objective

- Others

By Application

Medical Industry Segment Leads Market Growth Driven by Advanced Diagnostic Equipment Requirements

The market is segmented based on application into:

- Medical Industry

- Life Science

- Industrial Manufacturing

- Aerospace

- Precision Instrument

- Others

By Resolution

Ultra-High Resolution Segment Gains Traction for Critical Microscopy Applications

The market is segmented based on resolution into:

- High Resolution (1-5 microns)

- Ultra-High Resolution (sub-micron)

- Standard Resolution (above 5 microns)

By End User

Research Institutes Show Strong Demand for Specialized Objective Lenses

The market is segmented based on end user into:

- Research Institutes

- Manufacturing Facilities

- Medical Laboratories

- Academic Institutions

- Others

Regional Analysis: Global High Definition Objective Market

North America

The North American High Definition Objective market is driven by cutting-edge medical and industrial applications, supported by strong R&D investments. The U.S. dominates with a 30%+ market share due to high adoption in life sciences and semiconductor manufacturing, where precision optics are critical. Leading players like Nikon Instruments and Mitutoyo Corporation focus on miniaturization and higher resolution, catering to sectors like microscopy and metrology. Regulatory pressures for higher imaging accuracy and AI-integrated optical systems are accelerating innovation in the region. However, supply chain constraints for specialty glass materials periodically disrupt production.

Europe

Europe maintains a stronghold in industrial and aerospace applications of high-definition objectives, with Germany and France as key contributors. The region emphasizes environmentally sustainable manufacturing processes even in optical component production. Leica Microsystems (Germany) leads in medical-grade objectives, while partnerships between research institutions and OEMs drive advancements in multi-spectral imaging. Strict EU directives on material sourcing and energy efficiency in manufacturing act as both a challenge and catalyst for cleaner production methods. The market sees growing demand for catadioptric objectives (compound lens-mirror systems) in space exploration projects.

Asia-Pacific

Accounting for over 45% of global demand, the APAC market thrives on mass production of consumer electronics and expanding healthcare infrastructure. China’s semiconductor boom (with $142B in 2023 fab investments) fuels need for inspection optics, while India’s precision instrument sector grows at 12% CAGR. Japanese firms dominate the high-end transmission objective segment, but cost sensitivity in Southeast Asia keeps reflecting objectives popular. Local manufacturers are bridging the quality gap with modular, upgradeable designs—critical for SMEs adopting automation. The key challenge remains IP protection, with imitation products affecting premium brands.

South America

A niche but growing market, South America shows potential in mining and agricultural tech applications. Brazil’s aerospace ambitions (e.g., Embraer’s vision systems) drive specialty lens demand, while Colombia and Chile invest in medical diagnostics infrastructure. The lack of local manufacturing forces 90% import dependence, primarily from North America and Europe. Economic volatility restricts capital expenditure on high-end optics, but refurbished and reconditioned objectives gain traction. Recent trade agreements may improve access to Chinese mid-range products, reshaping competitive dynamics.

Middle East & Africa

The MEA market is emerging but uneven, with the UAE and Saudi Arabia leading in oil/gas inspection systems and aerospace MRO (Maintenance, Repair, Overhaul) applications. Egypt and South Africa show incremental growth in healthcare imaging, though budgets favor cost-effective alternatives over premium HD objectives. Infrastructure projects like NEOM (Saudi Arabia) could spur demand for survey and alignment optics. Limited technical expertise in optical system maintenance remains a barrier, prompting suppliers to offer training-as-a-service bundled with products.

Report Scope

This market research report provides a comprehensive analysis of the Global High Definition Objective market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Transmission, Reflecting, Catadioptric Objectives), application (Medical, Life Science, Industrial Manufacturing), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets.

- Competitive Landscape: Profiles of leading players including Nikon Instruments, Leica Microsystems, Mitutoyo Corporation, their product portfolios, R&D investments, and strategic developments.

- Technology Trends: Analysis of emerging optical technologies, integration with imaging systems, and advancements in precision manufacturing.

- Market Drivers & Restraints: Evaluation of factors including demand for high-resolution imaging, industrial automation growth, and challenges in precision manufacturing.

- Stakeholder Analysis: Strategic insights for optical component suppliers, equipment manufacturers, and investors in the microscopy and imaging sectors.

The research employs primary interviews with industry leaders and validated secondary data from trade associations, ensuring accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Definition Objective Market?

-> High Definition Objective Market was valued at US$ 743.8 million in 2024 and is projected to reach US$ 1.19 billion by 2032, at a CAGR of 6.01% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Major players include Nikon Instruments, Leica Microsystems, Mitutoyo Corporation, Oberwerk Corporation, and Tract Optics.

What are the key growth drivers?

-> Growth is driven by advancements in medical imaging, increasing industrial automation, and demand for high-precision measurement systems across manufacturing sectors.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (38% in 2023), while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include AI-integrated optical systems, nano-scale imaging solutions, and hybrid objective designs for multifunctional applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...