MARKET INSIGHTS

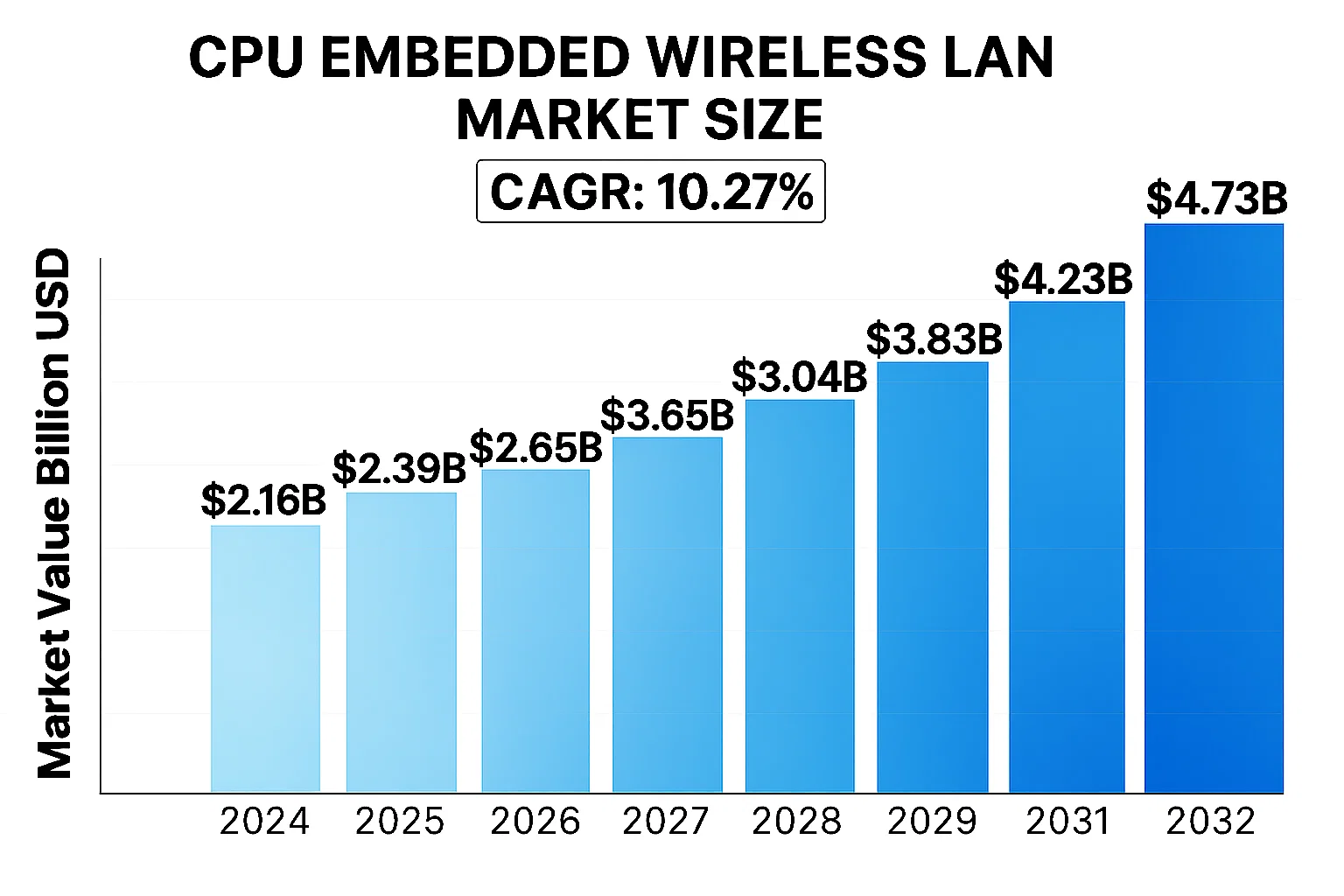

The global CPU Embedded Wireless LAN Market was valued at US$ 2.16 billion in 2024 and is projected to reach US$ 4.73 billion by 2032, at a CAGR of 10.27% during the forecast period 2025-2032. The Asia-Pacific region accounted for over 42% of global market share in 2023, driven by rapid IoT adoption in manufacturing and smart city projects.

CPU Embedded Wireless LAN refers to wireless networking capabilities integrated directly into central processing units (CPUs) or associated chipsets. This technology eliminates the need for separate Wi-Fi modules by embedding IEEE 802.11 standards-compliant connectivity within microcontrollers and microprocessors. Key applications include industrial IoT deployments, smart home appliances, voice-over-IP systems, and automotive telematics where space and power constraints make integrated solutions preferable.

The market growth is fueled by increasing demand for connected devices across industries, with over 29 billion IoT devices expected to be deployed globally by 2030. While embedded Wi-Fi solutions offer advantages in energy efficiency and miniaturization, challenges remain in maintaining signal integrity and thermal management in compact designs. Recent technological advancements such as Wi-Fi 6/6E integration in embedded systems and collaborations between semiconductor manufacturers like Broadcom and Texas Instruments are accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in IoT Adoption Accelerates Demand for Embedded Wireless LAN Solutions

The global Internet of Things (IoT) market continues its rapid expansion, with the number of connected devices expected to surpass 29 billion by 2030. This massive proliferation of smart devices directly fuels demand for CPU embedded wireless LAN solutions, as they provide the essential connectivity backbone for IoT ecosystems. The technology enables seamless communication between devices in industrial automation, smart home applications, and enterprise environments while maintaining power efficiency and compact form factors critical for embedded systems.

Advancements in Wireless Standards Driving Market Penetration

The evolution of wireless standards, particularly Wi-Fi 6 and the emerging Wi-Fi 7, presents significant growth opportunities for CPU embedded wireless LAN solutions. These advanced protocols offer substantially higher data rates, lower latency, and improved power efficiency – making them ideal for mission-critical industrial applications. Implementation of these standards in embedded form factors allows manufacturers to future-proof their products while meeting the increasing bandwidth demands of modern applications. The transition to these standards is being further accelerated by the declining cost of embedded wireless modules, which have seen price reductions of approximately 15-20% annually over the past three years.

Industry 4.0 Transformation Creating New Application Horizons

The ongoing Industry 4.0 revolution across manufacturing sectors worldwide is dramatically increasing adoption of CPU embedded wireless LAN solutions. These technologies enable real-time machine-to-machine communication, remote monitoring, and predictive maintenance in smart factories. Wireless connectivity in industrial environments reduces cabling costs by up to 40% while improving system flexibility. The industrial IoT segment is projected to maintain a compound annual growth rate of over 18% through 2030, with embedded wireless solutions playing a pivotal role in this expansion.

MARKET RESTRAINTS

Security Concerns in Wireless Communication Limit Adoption in Critical Applications

While CPU embedded wireless LAN solutions offer numerous benefits, security vulnerabilities remain a significant barrier to widespread adoption, particularly in sectors handling sensitive data. Wireless networks are inherently more susceptible to cyber threats compared to wired connections, with industrial IoT devices being particularly vulnerable targets. Many legacy industrial systems were not designed with modern security protocols in mind, requiring expensive retrofits or replacements to achieve acceptable security levels.

Integration Challenges with Legacy Systems Create Implementation Hurdles

The transition from wired to wireless industrial systems faces numerous technical challenges, particularly when integrating with existing infrastructure. Many manufacturing facilities operate with equipment that has decades-long lifespans and proprietary communication protocols. Retrofitting these systems with wireless capabilities often requires substantial engineering effort and can introduce compatibility issues. This complexity slows decision-making processes and lengthens implementation timelines, particularly in risk-averse industries where system reliability is critical.

Regulatory Compliance Adds Complexity to Global Deployments

The fragmented nature of wireless spectrum regulations across different regions creates significant challenges for manufacturers developing global products. Compliance with varying certification requirements in major markets (FCC in North America, CE in Europe, MIC in Japan) increases development costs and time-to-market. Additionally, some industrial environments face strict electromagnetic compatibility requirements that can limit wireless deployment options or necessitate costly shielding solutions.

MARKET CHALLENGES

Shortage of Skilled Professionals Impacts Implementation Capabilities

The rapid adoption of wireless technologies across industries has outpaced the availability of qualified engineers with expertise in both wireless systems and industrial applications. Many organizations struggle to find personnel capable of properly designing, implementing, and maintaining wireless industrial networks. This skills gap is particularly pronounced in emerging markets, where technical training programs have not kept pace with technological advances.

Power Consumption Constraints in Battery-Powered Applications

While embedded wireless LAN solutions have made significant progress in power efficiency, many industrial IoT applications require years of battery life from field devices. Maintaining continuous wireless connectivity while meeting these stringent power budgets remains a significant technical challenge. The need to periodically replace batteries in hundreds or thousands of deployed sensors can quickly erase the cost savings promised by wireless solutions.

Interference Issues in Dense Industrial Environments

The proliferation of wireless devices in industrial settings leads to increasingly congested radio environments. Many facilities must support multiple wireless systems (Wi-Fi, Bluetooth, cellular, proprietary protocols) simultaneously, creating potential for interference and degraded performance. This is particularly problematic for time-sensitive applications where even milliseconds of latency can disrupt critical processes. Effective spectrum management remains a persistent challenge in complex industrial deployments.

MARKET OPPORTUNITIES

Smart Cities Initiatives Driving Large-Scale Deployments

Global smart city initiatives represent one of the most significant growth opportunities for CPU embedded wireless LAN solutions. Municipalities worldwide are investing heavily in smart infrastructure projects that rely on wireless connectivity for applications ranging from traffic management to environmental monitoring. These large-scale deployments create substantial demand for robust, energy-efficient wireless modules designed for long-term outdoor operation.

Emerging Private Wireless Networks for Industry

The development of private wireless networks based on technologies like 5G and Wi-Fi 6 creates new opportunities for industrial-grade embedded solutions. These dedicated networks offer the reliability and performance required for mission-critical applications while providing enhanced security and control compared to public networks. The private wireless market is projected to grow at over 35% annually through 2030, representing a significant revenue opportunity for embedded solutions providers.

Advancements in Edge Computing Expand Application Possibilities

The integration of edge computing capabilities with embedded wireless modules enables new classes of intelligent, connected devices. By processing data locally before transmission, these solutions can reduce network congestion and improve response times for time-sensitive applications. This convergence of connectivity and computing presents opportunities for higher-value solutions that command premium pricing while addressing critical industry pain points.

GLOBAL CPU EMBEDDED WIRELESS LAN MARKET TRENDS

5G Integration and IoT Expansion Driving Market Growth

The global CPU embedded wireless LAN market is experiencing transformative growth driven by the rapid rollout of 5G networks and expansive adoption of IoT devices. With over 29 billion IoT connections projected worldwide by 2030, embedded wireless solutions are becoming critical for low-latency connectivity in smart environments. Manufacturers are increasingly integrating WLAN capabilities directly into microprocessors and microcontrollers to enable seamless communication between edge devices. This trend is particularly prominent in industrial automation, where real-time data transmission requirements are pushing innovation in embedded wireless architectures. Furthermore, advancements in Wi-Fi 6 and Wi-Fi 6E technologies are enabling CPU embedded solutions to deliver higher throughput and better power efficiency, making them ideal for always-connected devices.

Other Trends

Smart Cities and Infrastructure Modernization

The global smart city initiative is accelerating demand for CPU embedded WLAN solutions in traffic management, utilities monitoring, and public safety systems. Municipalities worldwide are investing heavily in connected infrastructure, requiring robust wireless capabilities embedded directly into control units. This trend is complemented by government regulations mandating smarter energy grids and transportation networks, where embedded wireless provides the necessary communication backbone. The Asia-Pacific region leads in smart city deployments, accounting for over 40% of global investments, creating substantial opportunities for WLAN-enabled microprocessor vendors.

Automotive Connectivity Revolution

The automotive sector represents one of the fastest-growing applications for CPU embedded WLAN technology. Modern vehicles now incorporate numerous wireless modules for telematics, infotainment, and advanced driver assistance systems (ADAS). With the average premium vehicle containing 50+ microprocessors, automakers are favoring integrated WLAN solutions to reduce component count and improve reliability. The rollout of vehicle-to-everything (V2X) communication standards is further propelling this trend, as embedded wireless becomes essential for next-generation transportation ecosystems. Collaborative developments between semiconductor firms and automotive OEMs are yielding customized solutions that meet stringent automotive certification requirements while delivering the low-latency performance needed for safety-critical applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Define Market Competition

The global CPU embedded Wireless LAN market exhibits a competitive yet collaborative environment, dominated by established semiconductor manufacturers and emerging specialists. Broadcom Inc. leads the segment with its advanced wireless connectivity solutions, capturing approximately 25% of the market share in 2023. Their dominance stems from extensive R&D investments exceeding $5 billion annually and strategic partnerships with major IoT device manufacturers.

Texas Instruments and Murata Manufacturing jointly hold another 30% market share, leveraging their expertise in embedded systems and miniaturized wireless components. These companies have recently expanded their production capacities in Southeast Asia to meet surging demand from smart appliance manufacturers.

Meanwhile, Microchip Technology has been gaining traction through its focus on low-power microcontroller-based WLAN solutions, particularly in industrial IoT applications. Their market share grew by 3 percentage points in 2023 following successful product launches in the automation sector.

Japanese firms including TAIYO YUDEN and Panasonic maintain strong positions in the Asia-Pacific region through localized manufacturing and government-supported 5G integration projects. These players are increasingly collaborating with automotive OEMs to develop next-generation vehicular communication systems.

List of Leading CPU Embedded Wireless LAN Providers

- Broadcom Inc. (U.S.)

- Texas Instruments (U.S.)

- Murata Manufacturing (Japan)

- Microchip Technology (U.S.)

- Panasonic Corporation (Japan)

- TAIYO YUDEN (Japan)

- SystemBase (China)

- Embedded Wireless (Germany)

Segment Analysis:

By Type

Microcontroller Segment Leads with Higher Adoption in Compact IoT Devices

The market is segmented based on type into:

- Microcontroller

- Microprocessor

- Subtypes: ARM-based, x86-based, and others

- System-on-Chip (SoC)

- Others

By Application

Industrial IoT Holds Largest Share Driven by Industry 4.0 Adoption

The market is segmented based on application into:

- Industrial IoT

- Smart Appliances

- VoIP Devices

- Consumer Electronics

- Others

By Connectivity Protocol

Wi-Fi 6 Segment Growing Rapidly Due to High-Speed Requirements

The market is segmented based on connectivity protocol:

- Wi-Fi 4 (802.11n)

- Wi-Fi 5 (802.11ac)

- Wi-Fi 6 (802.11ax)

- Bluetooth

- Dual Band (Wi-Fi + Bluetooth)

- Others

By End-User Industry

Automotive Sector Shows Promising Growth with Connected Vehicle Trends

The market is segmented based on end-user industry:

- Automotive

- Healthcare

- Industrial

- Consumer Electronics

- Telecommunications

- Others

Regional Analysis: Global CPU Embedded Wireless LAN Market

North America

North America remains a dominant force in the CPU embedded Wireless LAN market, driven by advanced technological adoption and robust demand from IoT, smart appliances, and VoIP applications. The U.S. accounts for over 60% of the regional market share, fueled by strong R&D investments in embedded systems and 5G infrastructure deployment. Key players like Broadcom and Texas Instruments are expanding their microcontroller-based wireless LAN solutions for industrial automation and smart homes. However, stringent FCC regulatory compliance and higher product costs present adoption challenges for smaller enterprises. The region is witnessing a shift toward energy-efficient Wi-Fi 6/6E enabled embedded solutions, particularly for edge computing applications in manufacturing and healthcare sectors.

Europe

Europe’s market growth is propelled by the EU’s focus on Industry 4.0 and standardized wireless protocols under RED (Radio Equipment Directive). Germany leads in industrial IoT adoption, with embedded WLAN solutions increasingly integrated into automated production lines. The region shows strong preference for secure, low-latency microprocessor-based solutions from suppliers like Panasonic and Murata Manufacturing. However, complex GDPR and cybersecurity requirements for connected devices have slowed some implementations. Emerging smart city projects across the UK, France, and Nordic countries are creating new opportunities, though market fragmentation across different wireless standards remains a challenge for manufacturers.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at ~12% CAGR through 2028, driven by massive IoT deployment in China and manufacturing automation in Japan/South Korea. China accounts for nearly 40% of regional demand, with domestic players like TAIYO YUDEN competing strongly in cost-sensitive microcontroller segments. India shows increasing adoption in smart meter and VoIP applications, though price sensitivity limits premium solution uptake. The region benefits from expanding semiconductor fabrication capabilities and government Digital India/Industry 4.0 initiatives. However, market fragmentation persists due to varying wireless spectrum regulations across countries and competition from alternative connectivity solutions like 5G NR-Light.

South America

While still a developing market, South America shows gradual adoption of embedded WLAN solutions in Brazil’s industrial sector and Argentina’s emerging smart appliance market. Local manufacturers primarily focus on cost-effective microcontroller implementations for basic connectivity needs. Market growth is constrained by economic instability, limited local technical expertise, and infrastructure gaps in rural areas. Recent trade agreements facilitating semiconductor imports and Brazil’s IoT national plan show promise, but adoption remains concentrated in urban industrial clusters and premium consumer electronics segments.

Middle East & Africa

The MEA market is in early growth stages, with UAE and Saudi Arabia leading in smart city and industrial automation projects requiring embedded connectivity. High dependence on imports for semiconductor components creates supply chain vulnerabilities. While oil-rich nations invest in advanced manufacturing with embedded systems, price sensitivity in other markets limits adoption to basic wireless LAN implementations. Africa shows potential through mobile payment infrastructure development, but unreliable power infrastructure and limited technical support networks hinder widespread CPU embedded WLAN implementation across most countries.

Report Scope

This market research report provides a comprehensive analysis of the Global CPU Embedded Wireless LAN market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (microcontroller vs microprocessor), technology, application (Industrial IoT, smart appliances, VoIP), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading manufacturers including Murata Manufacturing, Broadcom, Texas Instruments, Panasonic, and TAIYO YUDEN, covering their product portfolios, market strategies, and recent developments.

- Technology Trends: Analysis of Wi-Fi 6/6E adoption, low-power designs, AI integration in wireless modules, and security enhancements in embedded solutions.

- Market Drivers & Restraints: Evaluation of IoT expansion, smart home adoption, 5G rollout impacts, versus challenges like chip shortages and design complexities.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors on emerging opportunities.

The research employs both primary (expert interviews) and secondary (verified market data) methodologies to ensure accuracy and actionable intelligence for decision-makers.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global CPU Embedded Wireless LAN Market?

-> CPU Embedded Wireless LAN Market was valued at US$ 2.16 billion in 2024 and is projected to reach US$ 4.73 billion by 2032, at a CAGR of 10.27% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Leading players include Murata Manufacturing, Broadcom, Texas Instruments, Panasonic, TAIYO YUDEN, Microchip Technology, and SystemBase.

What are the primary growth drivers?

-> Key drivers include IoT proliferation (30 billion connected devices by 2025), smart home adoption (15% annual growth), and industrial automation demands.

Which region shows strongest growth?

-> Asia-Pacific dominates with 42% market share in 2024, led by China’s manufacturing ecosystem and Japan’s component suppliers.

What emerging technologies impact this market?

-> Emerging trends include Wi-Fi 6/6E adoption (45% of new designs by 2025), AI-optimized wireless stacks, and ultra-low-power designs for edge devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...