MARKET INSIGHTS

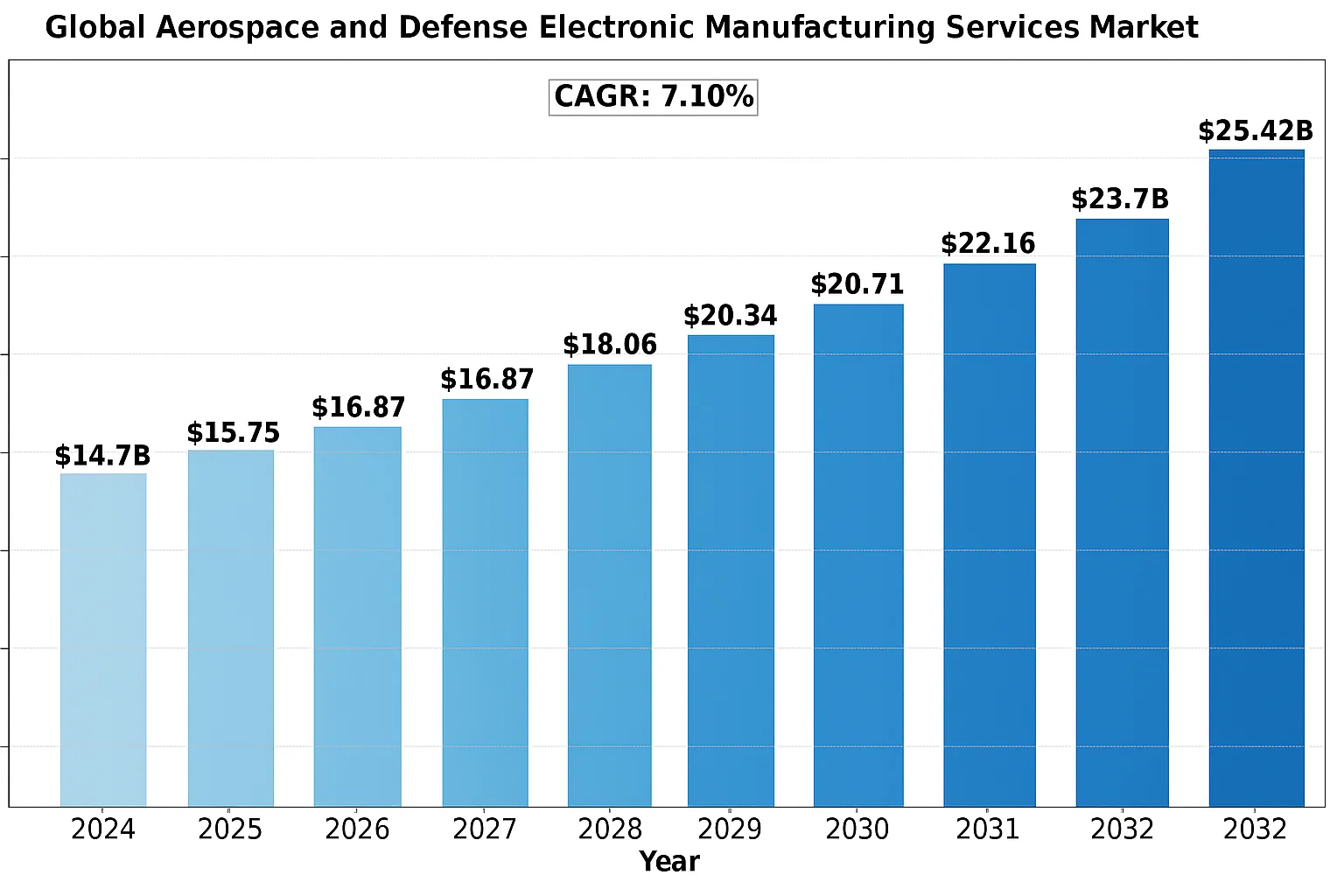

The Global Aerospace and Defense Electronic Manufacturing Services Market size was valued at US$ 14.7 billion in 2024 and is projected to reach US$ 23.8 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032.

Aerospace and defense electronic manufacturing services (EMS) encompass specialized outsourcing solutions for designing, testing, manufacturing, and assembling electronic components used in aircraft, spacecraft, and military systems. These services include printed circuit board assembly (PCBA), cable/wire harness production, avionics integration, and rigorous testing protocols compliant with stringent industry standards like AS9100 and MIL-STD-883.

The market growth is primarily driven by increasing defense budgets globally, particularly in North America and Asia-Pacific, where countries are modernizing their military aircraft fleets. For instance, the US Department of Defense allocated USD 842 billion for fiscal year 2024, with significant portions directed toward electronic warfare systems and communication upgrades. Furthermore, commercial aerospace demands are rebounding post-pandemic, with Boeing and Airbus reporting record order backlogs exceeding 8,000 aircraft collectively, all requiring advanced avionics and in-flight entertainment systems. However, supply chain vulnerabilities for semiconductors and geopolitical tensions pose challenges to consistent market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growing Defense Budgets Worldwide to Accelerate Market Expansion

The global aerospace and defense electronics manufacturing services market is experiencing significant growth driven by increasing defense expenditures across major economies. Governments are allocating substantial budgets to modernize military equipment and strengthen national security infrastructure, creating robust demand for advanced electronic components. Recent geopolitical tensions have further accelerated defense spending, with major allocations directed toward avionics, communication systems, and unmanned technologies. This trend is particularly evident in regions facing heightened security challenges, where militaries are prioritizing electronic warfare capabilities and next-generation defense systems.

Commercial Aviation Sector Rebound to Fuel Demand

Following the pandemic-induced slowdown, the commercial aviation sector is witnessing a strong rebound, driving demand for aircraft avionics and in-flight entertainment systems. Airlines worldwide are investing heavily in fleet modernization programs to improve fuel efficiency and passenger experience. This resurgence is creating significant opportunities for electronic manufacturing service providers specializing in aviation-grade components. The increasing adoption of connected aircraft technologies and advanced navigation systems is further propelling market growth, with aircraft OEMs expanding their supply chain partnerships to meet the rising demand.

Furthermore, the growing emphasis on predictive maintenance in aviation is driving the integration of advanced sensor networks and IoT-enabled monitoring systems throughout aircraft. These technological advancements require sophisticated electronic manufacturing capabilities, creating new revenue streams for EMS providers specializing in aerospace applications.

MARKET RESTRAINTS

Stringent Certification Requirements to Limit Market Entry

The aerospace and defense electronics sector faces significant barriers to entry due to rigorous certification processes and quality standards. Meeting AS9100 and other industry-specific certifications requires substantial investments in quality control systems and employee training. Many smaller manufacturers find it challenging to comply with these stringent requirements, limiting their ability to compete in this high-stakes market. The certification process can extend over several years, delaying time-to-market for new entrants and significantly increasing operational costs.

Additionally, the defense sector’s strict security protocols and ITAR regulations create further complications for international supply chains. Manufacturers must navigate complex export control laws and implement secure data management systems, adding layers of compliance burdens that impact operational efficiency and profitability.

MARKET CHALLENGES

Supply Chain Vulnerabilities to Impact Production Stability

The aerospace and defense electronics manufacturing sector continues to face significant supply chain disruptions, particularly for specialized semiconductor components. The industry’s reliance on a limited number of suppliers for radiation-hardened and high-reliability electronic components creates vulnerabilities in production stability. Recent geopolitical conflicts and trade restrictions have exacerbated these challenges, leading to extended lead times for critical components. Many manufacturers are struggling to maintain inventory levels while meeting demanding defense contract schedules, resulting in production delays and cost overruns.

Compounding these issues, the increasing complexity of electronic systems requires specialized manufacturing equipment and testing facilities. The capital-intensive nature of these investments makes it difficult for manufacturers to quickly scale production capacity in response to market demand fluctuations.

MARKET OPPORTUNITIES

Emerging Space Sector to Create New Growth Frontiers

The rapidly expanding commercial space industry is creating unprecedented opportunities for aerospace electronic manufacturers. Private space companies and government space agencies are investing heavily in satellite constellations, space exploration vehicles, and orbital infrastructure. This growth is driving demand for specialized electronic components that can withstand extreme environmental conditions while maintaining reliable operation. Manufacturers with expertise in radiation-hardened electronics and space-qualified components are particularly well-positioned to capitalize on this burgeoning market segment.

Moreover, the increasing deployment of small satellites and mega-constellations for communication and Earth observation applications is reshaping the supply chain dynamics. This shift favors agile EMS providers capable of delivering high-reliability components at commercial production volumes rather than traditional low-volume aerospace manufacturing approaches.

AEROSPACE AND DEFENSE ELECTRONIC MANUFACTURING SERVICES MARKET TRENDS

Increased Defense Budgets Worldwide Fueling Market Growth

The global aerospace and defense electronic manufacturing services market is experiencing robust growth, primarily driven by increased military spending across major economies. Over the past five years, defense budgets have grown at an average annual rate of 3.7%, with countries like the United States allocating over $800 billion for defense in 2023 alone. This surge in funding is accelerating the modernization of military aircraft, communication systems, and surveillance technologies, creating substantial demand for sophisticated electronic manufacturing services. The growing adoption of modular open systems architecture (MOSA) in defense applications is further stimulating market expansion by enabling more efficient upgrades and interoperability across platforms.

Other Trends

Miniaturization of Avionics Components

The relentless push toward lighter and more compact aircraft systems is transforming avionics manufacturing. Aerospace manufacturers are increasingly demanding high-density interconnect (HDI) PCBs and advanced packaging solutions to reduce weight while maintaining performance. This trend is particularly evident in next-generation fighter jets and unmanned aerial vehicles (UAVs), where space constraints are critical. The miniaturization wave has prompted EMS providers to invest heavily in precision manufacturing technologies, with the global aerospace PCB market projected to exceed $3.2 billion by 2026.

Growing Adoption of Additive Manufacturing for Aerospace Electronics

Additive manufacturing is revolutionizing the production of complex aerospace components, with the technology now being extended to electronic systems. Leading EMS providers are developing 3D-printed antennas and embedded electronics that reduce part counts while improving reliability. The ability to manufacture conformal electronics that fit the unique contours of aircraft structures is creating new opportunities across both commercial and defense segments. Furthermore, additive processes are significantly shortening development cycles for prototype electronics—a critical advantage in defense applications where rapid fielding of new capabilities provides strategic advantages.

COMPETITIVE LANDSCAPE

Key Industry Players

Defense Electronics Giants Invest in Innovation to Secure Long-Term Contracts

The global aerospace and defense electronic manufacturing services (EMS) market exhibits a moderately competitive landscape characterized by the presence of established OEMs and specialized EMS providers. Jabil Circuit currently leads the segment with a 12.3% market share (2023 estimates), leveraging its vertically integrated supply chain and certified manufacturing facilities meeting stringent defense standards like AS9100D.

While the market remains dominated by U.S. firms due to high defense spending, European players like eolane are gaining traction through strategic partnerships with Airbus and Thales. The France-based EMS provider reported 9.2% YoY growth in aerospace segment revenue for FY2023, demonstrating the industry’s shift toward regional supply chain diversification.

Meanwhile, mid-sized specialists such as Absolute EMS and Sonic Manufacturing Technologies are capturing niche opportunities in ruggedized electronics and avionics testing. Their ability to deliver low-volume, high-mix production runs gives them an edge in prototyping and legacy system sustainment programs.

The competitive intensity is further amplified by defense contractors increasingly outsourcing electronics manufacturing to reduce operational costs. This has prompted EMS providers to obtain ITAR registrations and security clearances – with NEO Tech Inc. becoming one of only seven commercial manufacturers certified for Category XI (electronics) under the U.S. Defense Production Act in 2023.

List of Key Aerospace & Defense EMS Providers Profiled

- Jabil Inc. (U.S.)

- NEO Tech Inc. (U.S.)

- Sonic Manufacturing Technologies (U.S.)

- Absolute EMS, Inc. (U.S.)

- Asteelflash (France)

- Ducommun Incorporated (U.S.)

- Neways Electronics International (Netherlands)

- eolane (France)

- TT Electronics (UK)

Segment Analysis:

By Type

Electronic Manufacturing Segment Holds Major Share Due to Rising Demand for Advanced Avionics Systems

The market is segmented based on type into:

- Electronic Manufacturing

- Subtypes: PCB Assembly, Cable & Harness Assembly, Box Build Assembly

- Test Development & Implementation

- Logistics Services

- Subtypes: Supply Chain Management, Aftermarket Support

- Others

By Application

Military Aircraft Segment Leads Owing to Increasing Defense Budgets Worldwide

The market is segmented based on application into:

- Civil and Commercial Aircraft

- Military Aircraft

- Space Systems

- Unmanned Aerial Vehicles

- Others

By Service Type

Contract Manufacturing Dominates with Major OEMs Outsourcing Production Activities

The market is segmented based on service type into:

- Contract Manufacturing

- Design & Engineering Services

- Component Manufacturing

- Testing & Certification

- Others

By Technology

Integrated Systems Gain Traction Due to Need for Compact Avionics Solutions

The market is segmented based on technology into:

- Avionics

- Communication Systems

- Navigation Systems

- Surveillance Systems

- Others

Regional Analysis: Global Aerospace and Defense Electronic Manufacturing Services Market

North America

The North American market dominates global aerospace and defense EMS, driven by heavy defense spending and technological leadership. The U.S. Department of Defense’s FY2024 budget request of $842 billion prioritizes modernization programs requiring advanced avionics and communication systems. Major OEMs increasingly outsource to EMS providers like Jabil and Ducommun to meet stringent MIL-SPEC requirements while controlling costs. Key challenges include ITAR compliance complexities and supply chain vulnerabilities exposed during recent semiconductor shortages. The region is witnessing accelerated adoption of additive manufacturing and AI-driven testing to reduce lead times for mission-critical components.

Europe

Europe maintains a robust aerospace EMS sector through Airbus supply chain networks and NATO defense collaborations. The EU’s ~€240 billion defense budget fuels demand for secure, sovereign manufacturing capabilities, with France and Germany accounting for 58% of regional EMS contracts. Regulatory pressures like EU REACH and conflict mineral reporting requirements have pushed providers toward full material declaration services. While labor costs remain high, investments in automated Industry 4.0 factories (particularly in Eastern Europe) are improving competitiveness. The Ukraine conflict has accelerated military EMS demand, though export controls on dual-use technologies present compliance hurdles.

Asia-Pacific

Asia-Pacific represents the fastest-growing EMS market, projected to expand at 6.3% CAGR through 2028. China’s military-civil fusion strategy drives domestic EMS capabilities (accounting for 42% of regional activity), while India’s $72.6 billion defense budget targets 70% indigenization – creating opportunities for local providers. Japan and South Korea focus on high-reliability electronics for next-gen fighters and missile systems. The region benefits from established electronics ecosystems in Taiwan and Singapore, though geopolitical tensions and U.S. export restrictions are forcing supply chain diversification. Cost advantages remain significant, with labor expenses 35-40% below Western counterparts.

South America

South America’s aerospace EMS market remains nascent but shows potential, particularly in Brazil where Embraer’s supply chain accounts for 68% of regional activity. Defense budgets average just 1.3% of GDP (vs 3.5% global median), limiting military EMS growth. Currency volatility and protectionist policies (like Brazil’s BNDES financing requirements) complicate foreign EMS provider operations. However, recent satellite program investments in Argentina and Chile are driving demand for radiation-hardened electronics manufacturing. The lack of advanced testing facilities means most complex assemblies still require final certification in North America or Europe.

Middle East & Africa

The MEA market is bifurcated between Gulf states investing in dual-use capabilities (UAE’s $23 billion Tawazun industrial program) and African nations reliant on imports. Israel dominates high-tech military EMS with specialized providers like Elbit Systems, while Saudi Arabia’s offset agreements compel technology transfers. Africa’s commercial aviation growth (projected 4.7% annual passenger increase) spurs MRO-related EMS demand. Infrastructure gaps persist, with only two MIL-STD-1553 compliant EMS facilities in the region. Political instability in North Africa continues to deter significant investment despite low labor costs of $2.8/hour versus $38 in the U.S.

Report Scope

This market research report provides a comprehensive analysis of the Global Aerospace and Defense Electronic Manufacturing Services market, covering the forecast period 2024–2030. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 28.5 billion in 2023 with a projected CAGR of 6.8% through 2030.

- Segmentation Analysis: Detailed breakdown by service type (electronic manufacturing, test development, logistics), platform (aircraft, UAVs, space systems), and end-user (OEMs, defense contractors) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis of major defense spenders.

- Competitive Landscape: Profiles of leading EMS providers including their capabilities in high-reliability manufacturing, ITAR compliance, and recent contract wins with major aerospace primes.

- Technology Trends & Innovation: Assessment of emerging technologies including 3D printing of electronic components, AI-based testing systems, and modular avionics architectures.

- Market Drivers & Restraints: Evaluation of defense budget increases, commercial aerospace recovery post-pandemic, and challenges in semiconductor supply chains.

- Stakeholder Analysis: Strategic insights for defense contractors, aerospace OEMs, and EMS providers regarding outsourcing strategies and supply chain resilience.

The analysis incorporates primary interviews with industry executives and utilizes data from defense procurement databases, regulatory filings, and verified market intelligence sources.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Aerospace and Defense Electronic Manufacturing Services Market?

-> The global Aerospace and Defense Electronic Manufacturing Services market size was valued at US$ 14.7 billion in 2024 and is projected to reach US$ 23.8 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Leading players include Jabil Circuit, Sanmina Corporation, Benchmark Electronics, Celestica, and TT Electronics, along with specialized providers like Ducommun and Esterline Technologies.

What are the key growth drivers?

-> Primary drivers include increasing defense electronics complexity, commercial aerospace production rates recovery, and outsourcing trends among OEMs to focus on core competencies.

Which region dominates the market?

-> North America holds the largest share (42% in 2023) due to major defense programs, while Asia-Pacific shows fastest growth with expanding indigenous aerospace capabilities.

What are the emerging trends?

-> Key trends include adoption of digital twin technologies, increasing use of additive manufacturing for electronics, and growing demand for secure supply chain solutions in defense applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...