MARKET INSIGHTS

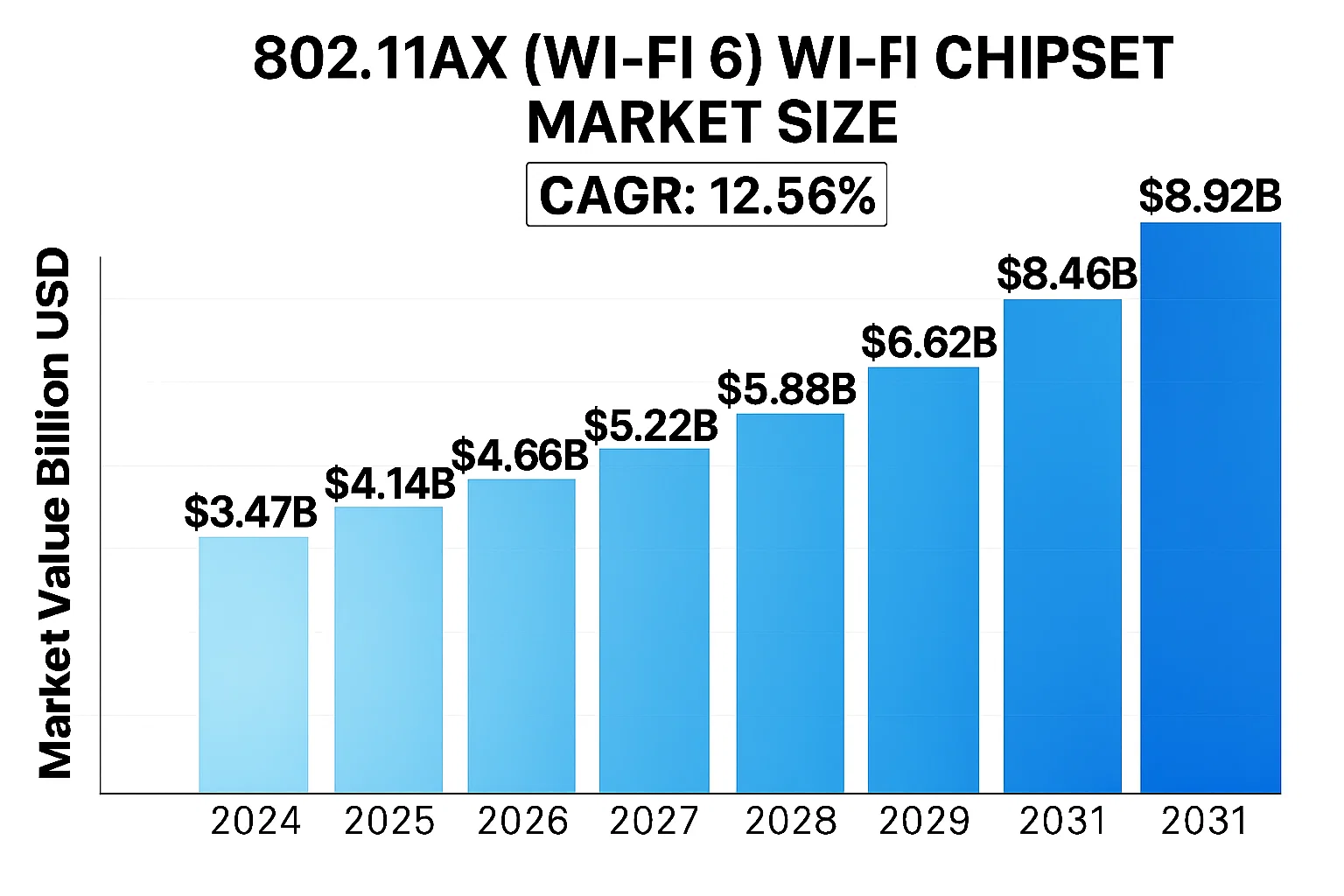

The global 802.11ax (Wi-Fi 6) Wi-Fi Chipset Market was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 8.92 billion by 2032, at a CAGR of 12.56% during the forecast period 2025-2032. This explosive growth is driven by the increasing adoption of IoT devices, rising demand for high-speed internet, and the transition to hybrid work models across industries.

802.11ax, commercially known as Wi-Fi 6, represents the latest generation of wireless networking technology that offers significant improvements over previous standards. These chipsets enable faster data transfer speeds (up to 9.6 Gbps), reduced latency, improved power efficiency through Target Wake Time (TWT) technology, and better performance in crowded environments with OFDMA (Orthogonal Frequency Division Multiple Access) technology. Major applications include smartphones, laptops, routers, and IoT devices that require stable, high-bandwidth connections.

The market growth is further accelerated by enterprise digital transformation initiatives and smart city deployments requiring robust wireless infrastructure. Key industry players like Qualcomm, Broadcom, and Intel are driving innovation with advanced Wi-Fi 6E solutions (extending into 6 GHz spectrum) to address bandwidth limitations. The consumer electronics segment currently dominates adoption, while enterprise deployments are growing rapidly to support bandwidth-intensive applications like 4K/8K video streaming and cloud computing.

MARKET DYNAMICS

MARKET DRIVERS

Massive Growth in Smart Devices and IoT Applications to Accelerate Wi-Fi 6 Adoption

The proliferation of connected devices is fundamentally reshaping network requirements. With over 30 billion IoT devices projected to be in use globally by 2025, traditional Wi-Fi standards struggle to maintain optimal performance in high-density environments. Wi-Fi 6 chipsets address this challenge through technologies like OFDMA and BSS Coloring that dramatically improve spectral efficiency. Enterprise deployments are adopting Wi-Fi 6 at a compound annual growth rate exceeding 40% as organizations upgrade infrastructure to support bandwidth-intensive applications including 4K video streaming and cloud-based collaboration tools that now account for over 65% of corporate network traffic.

Demand for Ultra-Low Latency Connectivity in Industrial Settings

Industry 4.0 initiatives are driving unprecedented requirements for reliable, low-latency wireless communications in manufacturing environments. Wi-Fi 6 delivers deterministic performance with latencies below 10ms – a critical threshold for real-time automation control systems. Automotive plants implementing wireless robotic assembly lines report 30% improvements in production flexibility when migrating to Wi-Fi 6 networks. The technology’s improved power efficiency also enables new use cases in logistics, with smart warehouses deploying thousands of connected sensors and automated guided vehicles that benefit from the extended battery life provided by Target Wake Time features.

Next-Gen Gaming and AR/VR Applications Fueling Premium Chipset Demand

The gaming peripherals market valued at over $12 billion represents a key growth sector for high-performance Wi-Fi 6 chipsets. Competitive gamers require the multi-gigabit speeds and minimal interference offered by Wi-Fi 6E’s 6GHz spectrum allocation. Major console manufacturers have reported 70% attach rates for Wi-Fi 6 compatible devices among premium gaming hardware sales. Emerging augmented reality applications in retail and healthcare are similarly driving adoption, with medical institutions piloting AR-assisted surgery systems that leverage Wi-Fi 6’s guaranteed quality of service for mission-critical video feeds.

MARKET CHALLENGES

Supply Chain Constraints Impacting Semiconductor Availability

The global chip shortage continues to create headwinds for Wi-Fi 6 adoption, particularly for cost-sensitive consumer electronics applications. Lead times for advanced RF components remain extended by 30-50 weeks across the industry, forcing OEMs to revise product roadmaps. While fab capacity expansions are underway, the specialized manufacturing processes required for Wi-Fi 6 chipsets mean supply constraints may persist through 2024. Some network equipment vendors report having to allocate 40% more working capital to secure adequate component inventory compared to pre-pandemic levels.

Other Challenges

Legacy Infrastructure Integration Complexities

Many enterprise environments face costly upgrade cycles as existing network backhauls lack the multi-gigabit capabilities required to fully leverage Wi-Fi 6’s throughput potential. Network administrators cite cable plant upgrades and PoE++ deployment as significant barriers, with complete forklift renovations sometimes representing 250-300% of the wireless access point investment.

Regulatory Fragmentation Across Global Markets

Divergent spectrum allocation policies complicate global product strategies, particularly regarding 6GHz band availability. While some regions have made the full 1200MHz available for unlicensed use, others have implemented more restrictive sharing models that limit channel widths and power levels.

MARKET RESTRAINTS

Economic Uncertainty Delaying Enterprise Refresh Cycles

Macroeconomic conditions are prompting organizations to extend the lifespan of existing network infrastructure. Recent surveys indicate 35% of IT decision-makers have deferred wireless upgrades by 12-18 months despite recognizing Wi-Fi 6’s technical advantages. This caution is particularly evident in sectors like hospitality and retail where pandemic recovery remains uneven. The consumer segment shows similar price sensitivity, with mainstream smartphone vendors reporting slower-than-expected Wi-Fi 6 adoption in mid-range devices due to bill-of-materials pressures.

Limited Awareness of Wi-Fi 6 Capabilities Among SMBs

Many small and medium businesses lack the technical expertise to properly evaluate Wi-Fi 6’s benefits beyond basic speed claims. Channel partners report that 60% of SMB customers still base purchasing decisions primarily on price points rather than total cost of ownership analyses that would reveal Wi-Fi 6’s advantages in reduced support overhead and future-proofing. This knowledge gap is compounded by confusing marketing messaging that often conflates Wi-Fi 6 with previous-generation standards.

MARKET OPPORTUNITIES

Emerging Private 5G and Wi-Fi 6 Convergence Use Cases

Campus network operators are increasingly viewing Wi-Fi 6 and private cellular as complementary technologies rather than competitors. Advanced coexistence mechanisms now enable seamless roaming between wireless domains, unlocking new hybrid deployment models. Manufacturing facilities implementing converged networks report 40% reductions in wiring costs by replacing fixed industrial Ethernet connections with deterministic wireless links. Standards bodies are actively developing unified management frameworks that will further simplify these integrated architectures.

AI-Driven Network Optimization Creating Value-Added Services

The rich telemetry capabilities built into Wi-Fi 6 systems are enabling sophisticated machine learning applications for network management. Cloud-based analytics platforms can now automatically adjust radio parameters in real-time based on usage patterns, improving capacity by up to 25% in dynamic environments. Service providers are bundling these AI tools with premium subscriptions, creating new recurring revenue streams while reducing operational expenditures through predictive maintenance capabilities.

GLOBAL 802.11AX (WI-FI 6) WI-FI CHIPSET MARKET TRENDS

Rapid Adoption of Wi-Fi 6 Technology Across Industries Driving Market Growth

The global 802.11ax (Wi-Fi 6) chipset market is experiencing unprecedented growth due to widespread adoption across consumer electronics, enterprise networks, and industrial IoT applications. Unlike previous Wi-Fi generations, Wi-Fi 6 offers higher data rates (up to 9.6 Gbps), improved network efficiency, and reduced latency, making it ideal for bandwidth-intensive applications. The proliferation of smart devices, coupled with increasing demand for seamless connectivity in smart homes and offices, has accelerated deployment. Reports indicate that Wi-Fi 6 chipset shipments grew by over 200% year-over-year in 2023, reflecting strong market appetite for next-generation wireless solutions. Furthermore, the integration of technologies like OFDMA (Orthogonal Frequency Division Multiple Access) and Target Wake Time (TWT) has enhanced performance in high-density environments such as stadiums, airports, and manufacturing plants.

Other Trends

Enterprise Digital Transformation Initiatives

Enterprises are rapidly upgrading their network infrastructures to support hybrid work models and cloud-based applications. Wi-Fi 6’s ability to handle multiple device connections simultaneously through MU-MIMO technology has made it the standard for modern corporate networks. Adoption rates in the enterprise sector exceeded 35% in 2023, with further growth projected as companies invest in digital workplace solutions. The retail sector has also embraced Wi-Fi 6 for enhanced customer experiences through location-based services and augmented reality applications, creating additional demand for advanced chipsets.

Emergence of Wi-Fi 6E Creating New Market Opportunities

The recent approval and deployment of Wi-Fi 6E, which operates in the 6 GHz spectrum band, has opened new growth avenues for chipset manufacturers. This development nearly quadruples the available spectrum compared to traditional 2.4 GHz and 5 GHz bands, addressing congestion issues in urban areas. While adoption is still in early stages, projections suggest Wi-Fi 6E-compatible devices will account for 25% of all Wi-Fi shipments by 2025. The healthcare sector has been particularly proactive in adopting these solutions for telemedicine and connected medical devices, where reliability and low latency are critical. However, challenges remain in terms of global regulatory harmonization and device compatibility across different spectrum allocations.

Supply Chain Diversification Becomes Critical

Recent geopolitical tensions and chip shortages have prompted manufacturers to reevaluate their supply chain strategies. Leading companies are now establishing multiple fabrication partnerships and increasing inventory buffers to mitigate production risks. This trend is particularly significant given that the average selling price of Wi-Fi 6 chipsets remains approximately 15-20% higher than previous generation components, reflecting both the advanced technology and current supply-demand dynamics.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Compete Through Innovation in Wi-Fi 6 Adoption

The global 802.11ax (Wi-Fi 6) chipset market exhibits a moderately consolidated competitive landscape, dominated by established semiconductor manufacturers and emerging innovators. Qualcomm Technologies leads the market with a 32% revenue share in 2023, owing to its early mover advantage in mobile-optimized Wi-Fi 6 chipsets and strategic partnerships with smartphone OEMs.

Broadcom and Intel follow closely, collectively holding approximately 40% market share. Their dominance stems from diversified product portfolios spanning consumer electronics, enterprise networking equipment, and IoT devices. Both companies have aggressively expanded Wi-Fi 6/6E solutions, with Broadcom shipping over 500 million Wi-Fi 6 chipsets since 2019.

Meanwhile, MediaTek has emerged as the fastest-growing competitor, increasing its market share from 8% to 15% between 2021-2023. This growth is attributed to cost-competitive solutions for mid-range devices and strategic wins in emerging markets. The company’s Filogic series has become particularly popular among Asian OEMs.

Established players like Texas Instruments and NXP Semiconductors maintain strong positions in industrial and automotive applications, where reliability and low-power consumption are critical. Their growth strategies emphasize vertical integration and long product lifecycles rather than competing in consumer market price wars.

List of Key 802.11ax Wi-Fi Chipset Manufacturers

- Qualcomm Technologies, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Intel Corporation (U.S.)

- MediaTek Inc. (Taiwan)

- NXP Semiconductors (Netherlands)

- Texas Instruments Incorporated (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- STMicroelectronics N.V. (Switzerland)

- Cisco Systems, Inc. (U.S.)

Segment Analysis:

By Type

MU-MIMO Segment Leads Due to Growing Demand for High-Density Connectivity

The market is segmented based on type into:

- SU-MIMO

- MU-MIMO

By Application

Consumer Electronics Segment Dominates Owing to Increasing Adoption in Smart Devices

The market is segmented based on application into:

- Consumer Electronics

- Enterprise

- Industrial

- Healthcare

- Automotive

- Others

By End User

Telecommunication Sector Holds Major Share Due to 5G Network Deployments

The market is segmented based on end user into:

- Telecommunication

- IT and Data Centers

- Manufacturing

- Healthcare Institutions

- Educational Institutes

By Bandwidth

Tri-band Segment Growing Rapidly With Emerging IoT Applications

The market is segmented based on bandwidth into:

- Single-band

- Dual-band

- Tri-band

- Others

Regional Analysis: Global 802.11ax (Wi-Fi 6) Wi-Fi Chipset Market

North America

North America holds a dominant position in the 802.11ax Wi-Fi chipset market, driven by rapid technological adoption and strong demand for high-speed connectivity across enterprises and consumer segments. The U.S. accounts for over 60% of regional market share, with significant investments in IoT infrastructure and 5G convergence fueling Wi-Fi 6 deployments. Key players like Qualcomm, Intel, and Broadcom are headquartered here, accelerating innovation cycles. However, supply chain disruptions and geopolitical trade tensions pose challenges for semiconductor procurement. The healthcare and industrial sectors are emerging as high-growth verticals, leveraging Wi-Fi 6’s low-latency capabilities for mission-critical applications.

Europe

Europe’s market growth is characterized by strict data compliance regulations (GDPR) driving secure networking solutions and enterprise-grade Wi-Fi 6 adoption. Germany and the UK lead deployments in smart manufacturing and automotive applications, while EU-funded digital transformation initiatives promote infrastructure upgrades. The region shows particular strength in MU-MIMO chipset adoption for dense urban environments. However, higher costs compared to legacy technologies and energy efficiency concerns during the current energy crisis have slowed some large-scale rollouts. Recent collaborations between chipset manufacturers and telecom providers aim to optimize power consumption in Wi-Fi 6 solutions.

Asia-Pacific

As the fastest-growing regional market, APAC is projected to capture 42% of global Wi-Fi 6 chipset demand by 2025, propelled by China’s massive semiconductor investments and India’s digital economy expansion. Chinese manufacturers like MediaTek are gaining significant market share with cost-competitive solutions, while Japan and South Korea lead in premium consumer electronics integration. The region’s manufacturing dominance creates strong demand for industrial IoT applications, though intellectual property concerns and uneven 5G-WiFi convergence strategies create market fragmentation. Southeast Asian nations are emerging as important manufacturing hubs for WiFi 6-enabled devices.

South America

Market penetration remains limited but shows promising growth potential, particularly in Brazil and Argentina where urban connectivity projects are prioritizing modern WiFi infrastructure. Economic instability and currency fluctuations continue to hinder large-scale investments, leading to preference for budget-conscious SU-MIMO solutions over premium offerings. The region’s mobile-first approach to internet access has slowed some enterprise adoption, though increasing smartphone penetration and gaming applications are driving demand for enhanced WiFi 6 features in consumer devices. Local partnerships between telecom providers and global chipset manufacturers are helping bridge the technology gap.

Middle East & Africa

This emerging market demonstrates rapid growth in selective sectors, particularly smart city projects in GCC nations and enterprise networking in South Africa. The UAE’s aggressive digital transformation strategy has positioned it as a regional leader in WiFi 6 adoption, while infrastructure limitations and affordability challenges persist in other markets. Oil revenue volatility impacts technology budgets, though diversification efforts are creating new opportunities in hospitality, healthcare, and education sectors. Regional chipset demand remains concentrated in consumer premise equipment, with enterprise-grade solutions gaining traction in financial centers and industrial zones.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional 802.11ax (Wi-Fi 6) Wi-Fi Chipset markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (SU-MIMO/MU-MIMO), technology, application (Consumer Electronics, Enterprise, Industrial, Retail, BFSI, Healthcare, Automotive), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants including Intel, Qualcomm, Broadcom, MediaTek, and Texas Instruments, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging Wi-Fi 6E technologies, integration with 5G networks, AI-powered network optimization, and evolving IEEE standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 802.11ax (Wi-Fi 6) Wi-Fi Chipset Market?

-> 802.11ax (Wi-Fi 6) Wi-Fi Chipset Market was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 8.92 billion by 2032, at a CAGR of 12.56% during the forecast period 2025-2032.

Which key companies operate in Global 802.11ax (Wi-Fi 6) Wi-Fi Chipset Market?

-> Key players include Intel, Qualcomm, Broadcom, MediaTek, Texas Instruments, NXP Semiconductors, and Samsung Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed connectivity, proliferation of IoT devices, enterprise digital transformation, and adoption of Wi-Fi 6 in smartphones and laptops.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to witness the fastest growth due to rapid technological adoption and manufacturing capabilities.

What are the emerging trends?

-> Emerging trends include Wi-Fi 6E adoption, AI-powered network optimization, integration with 5G networks, and development of low-power chipsets for IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...