Glass Core Substrate for AI Processors Market Insights

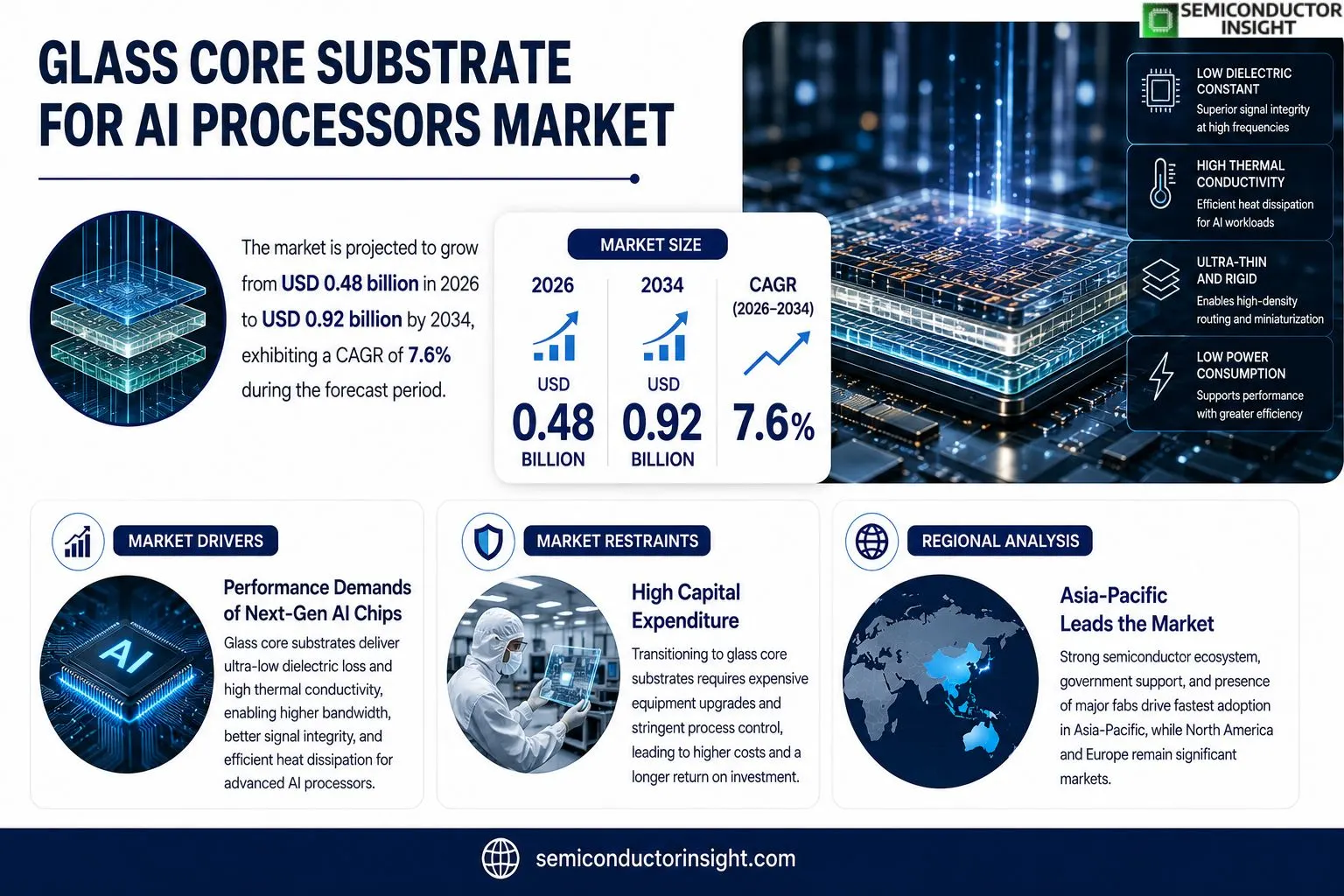

Glass Core Substrate for AI Processors market size was valued at USD 0.45 billion in 2025. The market is forecasted to expand from USD 0.48 billion in 2026 to USD 0.92 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

Glass core substrates are ultra‑thin glass plates that serve as carriers for high‑density interconnects within AI processors. Their low dielectric constant and superior thermal conductivity enable tighter routing and more efficient heat dissipation compared with traditional silicon interposers, making them suitable for next‑generation neural‑network accelerators.The upward trajectory reflects several dynamics: mounting demand for edge‑AI devices pushes manufacturers toward higher bandwidth packaging; the inherent rigidity of glass reduces signal loss at terahertz frequencies; recent collaborations such as Corning’s partnership with TSMC on advanced packaging solutions have accelerated adoption; and major semiconductor firms are allocating capital toward redesigning processor stacks around glass cores because they promise lower power consumption while maintaining performance.

MARKET DRIVERS

Performance Demands of Next‑Gen AI Chips

The push for ever‑higher compute density forces AI processor designers to seek substrates that can sustain gigahertz‑class signaling without compromising integrity. Glass core substrates deliver ultra‑low dielectric loss, enabling tighter clock margins and reduced power overheadattributes that are becoming non‑negotiable for advanced neural‑network accelerators.

Material Efficiency and Miniaturization

Thin‑film architectures benefit from the inherent rigidity and thermal stability of glass, allowing manufacturers to thin the stack while preserving mechanical strength. This translates into smaller form factors, a critical advantage for data‑center modules that must balance space constraints with cooling efficiency.

➤ Designers cite glass core substrates as a decisive factor in achieving signal integrity at unprecedented densities.

Beyond technical merits, the supply chain for high‑purity glass has matured, reducing lead times and price volatility. Companies that adopt Glass Core Substrate for AI Processors Market solutions can therefore lock in a cost structure that competes favorably with traditional ceramic or organic alternatives.

MARKET CHALLENGES

Manufacturing Yield Variability

Glass processing demands precise temperature control and defect‑free polishing. Even minor contaminants can generate micro‑cracks that propagate during high‑temperature bonding, pulling overall yields beneath acceptable thresholds and inflating per‑unit cost.

Other Challenges

Supply‑Chain Concentration

The majority of ultra‑low‑expansion glass is produced in a handful of facilities located in a limited geographic corridor. Any disruptionwhether logistical or regulatorycreates a bottleneck that reverberates through the AI processor value chain.Regulatory scrutiny over hazardous chemicals used in glass etching adds another layer of complexity. Compliance audits often require additional documentation and process adjustments, extending the time to market for new substrate designs.

MARKET RESTRAINTS

High Capital Expenditure for Equipment Upgrades

Transitioning from conventional organic laminates to glass core platforms necessitates substantial investment in new furnaces, precision grinders, and inspection tools. The payback horizon stretches over multiple product cycles, discouraging smaller players from entering the space.Environmental compliance also imposes constraints. The energy intensity of glass melting combined with stringent emissions standards raises operating costs, prompting manufacturers to evaluate the sustainability of large‑scale adoption.Finally, the ecosystem of design‑automation tools tailored to glass substrates remains limited. Engineers often resort to manual workarounds, slowing development timelines and increasing the risk of design errors.

MARKET OPPORTUNITIES

Emerging Edge‑AI Deployments

Edge devicesranging from autonomous sensors to portable inference unitsrequire substrates that marry compactness with thermal resilience. Glass core technology fits this niche, opening a revenue stream that complements traditional data‑center‑focused offerings.Photonics‑integrated AI processors are gaining traction, and the optical transparency of glass creates a seamless pathway for embedding waveguides directly within the substrate. This synergy positions glass core platforms as a natural bridge between electronic and photonic domains.Strategic alliances between glass manufacturers and semiconductor fab houses are beginning to surface, aimed at co‑developing turnkey solutions. Such collaborations can accelerate time‑to‑market and dilute the upfront cost burden, making Glass Core Substrate for AI Processors Market more accessible to a broader set of customers.

Glass Core Substrate for AI Processors Market Trends

Edge‑AI Bandwidth Pressure Elevates Glass Core Substrate Adoption

Glass Core Substrate for AI Processors Market recorded a valuation of roughly USD 0.45 billion in 2025. By the close of 2026 the estimate rose modestly to USD 0.48 billion, and projections show the market reaching about USD 0.92 billion by 2034, reflecting a compound annual increase near 7.6 percent. This trajectory is anchored in the surge of edge‑AI applications that demand higher I/O density and tighter latency budgets. Glass‑based carriers, with their ultra‑thin profile and low dielectric constant, enable designers to route more signals within a confined footprint while preserving signal integrity at terahertz frequencies. The thermal conductivity advantage also lets processors shed heat more efficiently, reducing the need for aggressive cooling solutions and, consequently, lowering system‑level power draw. Manufacturers that switch from silicon interposers to glass cores can therefore deliver thinner, lighter modules without compromising performancea competitive lever in markets such as autonomous sensors and portable inference devices.

Other Trends

Thermal Management Benefits

Thermal performance has become a decisive factor as AI accelerators pack more transistors per square millimeter. Glass core substrates conduct heat away from active regions faster than conventional polymer‑based laminates, which translates into a measurable drop in hotspot temperature during sustained inference workloads. This advantage enables chipmakers to operate near the silicon speed limit while staying within safe thermal envelopes, extending product lifespans and reducing warranty claims. Companies are now allocating engineering resources to co‑design processor stacks that exploit the substrate’s conductivity, integrating heat spreaders directly onto the glass layer. The resulting architecture not only improves reliability but also opens the door for higher clock frequencies without incurring additional cooling costs.

Strategic Alliances Accelerate Ecosystem Maturation

Recent industry moves underscore the importance of collaboration in scaling Glass Core Substrate for AI Processors Market. A notable partnership between a leading glass manufacturer and a major foundry has yielded a joint development roadmap that aligns substrate specifications with next‑generation node requirements. By synchronizing design rules, the alliance shortens time‑to‑market for AI chips that rely on glass interposers, while also standardizing testing protocols across the supply chain. Parallel to this, several semiconductor firms have announced capital commitments to redesign their processor architectures around glass cores, citing anticipated reductions in power envelope and improvements in signal fidelity. These coordinated investments indicate a maturing ecosystem where material suppliers, fabs, and chip designers move in lockstep, accelerating broader adoption across data‑center and edge segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Glass Core Substrate for AI Processors – Competitive Overview

The substrate arena is increasingly dominated by firms that have already invested in thin‑glass processing lines and have established relationships with leading foundries. Corning remains the benchmark supplier, leveraging its Gorilla® Glass platform to deliver ultra‑low‑dielectric plates that accommodate the tight pitch required by modern AI accelerators. Its collaboration with TSMC on advanced packaging has created a de‑facto standard for high‑frequency interconnects, compelling other manufacturers to align their material specifications to this emerging norm. Intel’s recent internal push to redesign processor stacks around glass cores signals a shift from silicon interposers, prompting a cascade of design‑win opportunities for glass vendors that can meet the exacting thermal‑conductivity targets demanded by data‑center GPUs.Beyond the obvious market leaders, a cluster of specialist players is carving out niches through differentiated glass chemistries or value‑added services. Samsung Electronics has begun offering proprietary borosilicate formulations that improve yield on large‑wafer panels, while ASE Technology Holding and Amkor Technology are expanding their backend capabilities to integrate glass substrates directly into their packaging lines. Smaller entrants such as Sumitomo Chemical, Taiwan Glass Corporation, and DuPont’s Kapton®‑related glass business are pursuing focused R&D programs to reduce coefficient‑of‑thermal‑expansion mismatches, a critical factor for reliability in edge‑AI devices. The collective effect of these efforts is a multi‑tiered supply chain where platform providers, packaging specialists, and material innovators each exert influence over pricing, lead times, and technology road‑maps.

List of Key Glass Core Substrate Companies Profiled

- Corning Inc.

- Taiwan Semiconductor Manufacturing Co. (TSMC)

- Intel Corporation

- Samsung Electronics

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Sumitomo Chemical Co., Ltd.

- Taiwan Glass Industry Corporation

- DuPont de Nemours, Inc.

- Foundries Inc.

- SK Hynix Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Applied Materials, Inc.

- 3M Company

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Photonic Glass Core continues to dominate because its ultra‑low dielectric constant minimizes signal attenuation, enabling higher frequency operation. • Provides a rigid platform that maintains precise alignment for densely packed interconnects. • Facilitates superior thermal pathways, allowing processors to sustain performance under intensive AI workloads. • Aligns well with emerging wafer‑level packaging strategies, reducing assembly complexity. |

| By Application |

|

Edge‑AI Accelerators emerge as the leading application because they demand compact, high‑bandwidth interconnects that glass cores excel at delivering. • Enables thinner form‑factors ideal for mobile and IoT devices. • Supports rapid data movement, critical for latency‑sensitive inference at the edge. • Enhances power efficiency by reducing parasitic losses, extending battery life in portable AI gadgets. |

| By End User |

|

AI Device OEMs drive the market forward as they prioritize packaging solutions that can handle escalating compute density. • Favor glass cores for their ability to sustain high‑frequency signals without excessive crosstalk. • Leverage the thermal advantages to keep device temperatures manageable in confined enclosures. • Appreciate the material’s transparency for advanced inspection during manufacturing, improving yield. |

| By Integration Approach |

|

2.5D Interposer Integration is the most attractive pathway, offering a balance between design flexibility and performance. • Allows heterogeneous components to be combined on a single glass substrate, simplifying routing. • Preserves the low‑loss advantage of glass while enabling high‑density I/O placement. • Facilitates rapid iteration for designers seeking to prototype next‑generation AI processors. |

| By Performance Requirement |

|

High Bandwidth remains the critical differentiator, as AI models increasingly demand massive data movement. • Glass substrates support ultra‑wide signal paths with minimal attenuation, enabling faster training and inference cycles. • Their inherent rigidity curtails signal distortion at terahertz frequencies, a key factor for future generative AI workloads. • Combined with superior thermal conductivity, they ensure that high‑throughput operation does not degrade reliability. |

Regional Analysis: Glass Core Substrate for AI Processors Market

Asia‑Pacific

Taiwan’s Hsinchu Science Park integrates glass‑core substrate R&D directly with advanced packaging lines, creating a seamless path from prototype to high‑volume production. The co‑location reduces lead times and aligns engineering roadmaps across the value chain.

Korean conglomerates are expanding their materials portfolios to include low‑coefficient‑of‑thermal‑expansion glass, limiting reliance on traditional silicon‑based interposers and mitigating geopolitical supply risks.

Regional design consortia are publishing open‑source thermal‑management guidelines that specifically reference glass‑core substrates, accelerating adoption among emerging AI accelerator developers.

Universities in Singapore and Japan have launched joint doctoral programs focusing on photonic‑glass integration, ensuring a steady flow of specialists who can bridge materials science and AI hardware engineering.

North America

The United States remains a strong purchaser of glass‑core substrates, driven by its leadership in AI software and custom accelerator design. However, the domestic supply chain lags behind Asian manufacturers, prompting major chipmakers to secure long‑term contracts with overseas glass providers. Recent policy shifts encouraging reshoring of semiconductor equipment have sparked early‑stage investments in substrate fabrication facilities, yet the capital intensity of glass processing suggests a gradual rollout. Consequently, the market in North America is characterized by high demand but modest local production capacity, creating a reliance on import channels that influences pricing dynamics.

Europe

European players leverage a tradition of precision optics to differentiate their glass‑core substrate offerings, emphasizing ultra‑low loss and high‑frequency performance for data‑center AI workloads. Collaborative research programs funded by the EU are exploring novel glass compositions that reduce dielectric loss, aligning with sustainability targets. While the region lacks the sheer volume of Asian fabs, its focus on niche, high‑value segments sustains a healthy demand environment. Companies are also positioning themselves as trusted suppliers for regulated industries, where quality certifications can command premium pricing.

South America

The South American landscape is still nascent, with most activity concentrated in Brazil’s emerging semiconductor clusters. Local universities are beginning to publish work on cost‑effective glass‑core prototypes, and a handful of start‑ups have attracted seed funding to pilot low‑volume production. The principal constraint is limited access to advanced lithography infrastructure, which forces developers to partner with overseas foundries. Nonetheless, growing digital‑infrastructure projects and governmental push for technology diversification hint at a longer‑term upside for glass‑core substrate adoption in the region.

Middle East & Africa

Investment interest in the Middle East & Africa centers on strategic partnerships with Asian substrate manufacturers, aiming to build downstream assembly capabilities rather than full‑scale glass fabrication. Gulf sovereign wealth funds have earmarked capital for AI‑focused hardware incubators, where glass‑core substrates feature as a key enabling technology. African markets, meanwhile, are witnessing early curiosity from telecom operators seeking cooling‑efficient AI edge solutions. The overall market tone is exploratory, with collaboration and knowledge transfer driving incremental progress rather than immediate scale.

Report Scope

This market research report provides a comprehensive analysis of the Glass Core Substrate for AI Processors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Glass Core Substrate for AI Processors Market?

-> Glass Core Substrate for AI Processors Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.92 billion by 2034 with a CAGR of 7.6% during the forecast period.

Which key companies operate in Glass Core Substrate for AI Processors Market?

-> Key players include Corning Inc., Taiwan Semiconductor Manufacturing Company (TSMC), and leading semiconductor packaging firms.

What are the key growth drivers?

-> Key growth drivers include rising demand for edge‑AI devices, need for higher‑bandwidth packaging, and superior thermal performance of glass substrates.

Which region dominates the market?

-> Asia‑Pacific shows the fastest adoption, while North America and Europe remain major markets.

What are the emerging trends?

-> Emerging trends include integration of glass core substrates in neural‑network accelerators, collaborations between glass manufacturers and semiconductor fabs, and development of ultra‑thin glass for terahertz‑frequency applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...