MARKET INSIGHTS

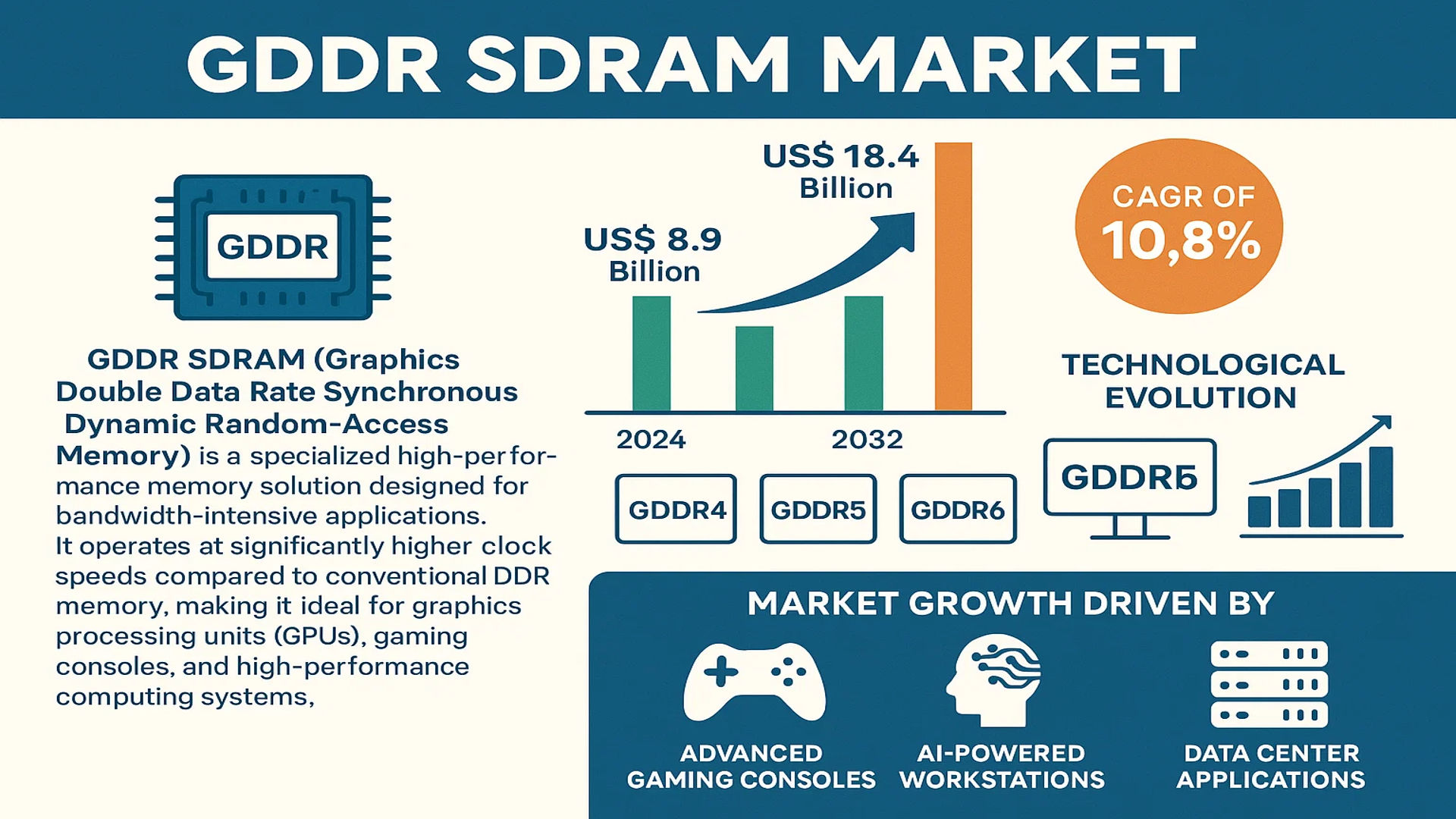

The global GDDR SDRAM Market size was valued at US$ 8.9 billion in 2024 and is projected to reach US$ 18.4 billion by 2032, at a CAGR of 10.8% during the forecast period 2025-2032.

GDDR SDRAM (Graphics Double Data Rate Synchronous Dynamic Random-Access Memory) is a specialized high-performance memory solution designed for bandwidth-intensive applications. It operates at significantly higher clock speeds compared to conventional DDR memory, making it ideal for graphics processing units (GPUs), gaming consoles, and high-performance computing systems. The technology has evolved through multiple generations, including GDDR4, GDDR5, and the latest GDDR6, each offering progressive improvements in speed and efficiency.

The market growth is primarily driven by increasing demand for advanced gaming consoles, AI-powered workstations, and data center applications. However, the rising adoption of alternative memory technologies like HBM (High Bandwidth Memory) presents a competitive challenge. Key industry players such as Samsung, SK Hynix, and Micron Technology are investing heavily in next-generation GDDR6X development to maintain technological leadership in this space.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Bandwidth Graphics Processing to Accelerate GDDR SDRAM Adoption

The global GDDR SDRAM market is experiencing robust growth driven by insatiable demand for high-performance graphics processing across multiple industries. Gaming consoles, professional visualization workstations, artificial intelligence accelerators, and high-performance computing systems all require memory solutions that can keep pace with increasingly complex computational workloads. The transition to 4K and 8K resolution displays, ray tracing technology, and real-time rendering applications has created an urgent need for memory bandwidth that conventional DDR solutions cannot provide. This market dynamic positions GDDR SDRAM, specifically GDDR6 and upcoming GDDR6X variants, as critical enablers of next-generation visual computing. Recent architectural improvements like 16Gb density stacks and per-pin data rates exceeding 24Gbps demonstrate how memory manufacturers are rising to meet these technical demands.

Artificial Intelligence Workloads Creating New Application Verticals

While gaming remains the primary application for GDDR technology, artificial intelligence and machine learning workloads represent the fastest-growing segment driving market expansion. Neural network training and inference operations require memory architectures capable of sustained high-bandwidth data transfer to processing units – precisely the competitive advantage of GDDR SDRAM. The parallel processing nature of GPU-accelerated AI aligns perfectly with GDDR’s wide interface architecture, enabling memory bandwidths that comfortably exceed 1TB/s in advanced implementations. This technical synergy has led major hyperscalers and AI solution providers to adopt GDDR-equipped accelerators as standard infrastructure, creating sustained demand for high-performance memory solutions. The AI accelerator market is projected to maintain double-digit annual growth through the forecast period, ensuring continued investment in GDDR memory development.

Next-Generation Gaming Consoles Driving Volume Production

The cyclical refresh of major gaming console platforms represents another significant growth driver for the GDDR SDRAM market. Current-generation consoles from leading manufacturers all utilize GDDR6 memory as unified system memory, with configurations ranging from 10GB to 16GB per unit. This architectural choice creates massive volume demand during console production cycles, with tens of millions of units requiring high-quality GDDR modules. The long product lifecycles of these platforms – typically 6-8 years – provide memory manufacturers with predictable, sustained demand that helps justify continued R&D investments in GDDR technology. Furthermore, the competitive dynamic between console manufacturers to deliver superior graphics performance ensures ever-increasing memory bandwidth requirements with each new generation, driving the transition to newer, faster GDDR standards.

MARKET RESTRAINTS

High Development Costs and Manufacturing Complexity Limit Market Players

The GDDR SDRAM market faces significant barriers to entry due to the technical complexity and capital intensity of memory semiconductor manufacturing. Developing each successive generation of GDDR technology requires billion-dollar investments in process technology development and manufacturing equipment. The transition to more advanced nodes (currently moving from 1α to 1β nm-class processes) demands increasingly sophisticated fabrication facilities and specialized expertise. This economic reality has consolidated the market to just a handful of major memory manufacturers capable of sustaining such investments, potentially limiting innovation and competition. While leading-edge GDDR6 production is currently dominated by three Korean and American suppliers, the requirements for next-generation GDDR7 development may further concentrate market share among the most technologically advanced firms.

Alternative Memory Technologies Pose Competitive Threat

Emerging memory architectures represent a growing competitive threat to GDDR’s dominance in high-bandwidth applications. Technologies like HBM (High Bandwidth Memory) offer significantly greater bandwidth per watt and superior form factor advantages for certain applications, particularly in data center environments. While GDDR maintains cost and manufacturing maturity advantages for consumer applications, the rapid evolution of 3D-stacked memory solutions could erode its technical superiority over time. The memory industry’s increasing focus on heterogeneous integration and chiplet-based designs may also favor alternative architectures that can be more easily integrated into advanced packaging schemes. Memory manufacturers face the challenge of evolving GDDR technology quickly enough to maintain its performance leadership while containing costs to preserve its price competitiveness.

Supply Chain Volatility Impacts Production Stability

The concentration of GDDR production capacity in specific geographic regions creates supply chain vulnerabilities that can constrain market growth. Trade tensions, export controls, and natural disasters have demonstrated how quickly memory supply can be disrupted, leading to allocation conditions and price volatility. The sophisticated equipment and materials required for memory manufacturing come from a globally dispersed supply network that remains susceptible to geopolitical and macroeconomic shocks. These factors introduce uncertainty into production planning and make it challenging to maintain stable pricing – a critical consideration for cost-sensitive applications like gaming consoles. Memory manufacturers must invest in supply chain diversification and inventory management strategies to mitigate these risks, adding to operational complexity and costs.

MARKET OPPORTUNITIES

Automotive Applications Present New Growth Frontier

The rapid evolution of autonomous driving and advanced driver assistance systems (ADAS) creates substantial growth opportunities for GDDR SDRAM in automotive applications. Modern vehicle architectures increasingly incorporate high-performance computing systems for sensor fusion, computer vision, and decision-making – all demanding memory bandwidth that scales with sensor resolution and algorithmic complexity. GDDR’s established reliability qualifications and temperature performance make it well-suited for automotive environments, while its bandwidth scaling roadmap aligns with projected computational requirements for autonomous systems. As automotive manufacturers transition to centralized domain controllers and zonal architectures, the opportunity for high-performance memory solutions could expand significantly. Memory suppliers that can meet stringent automotive functional safety and quality standards stand to benefit from this emerging application vertical.

Cloud Gaming Revolution Expands Addressable Market

The emergence of cloud gaming platforms represents another significant opportunity for GDDR SDRAM adoption. Remote rendering solutions require server-grade GPUs with high memory bandwidth to simultaneously support multiple game instances at high resolutions and frame rates. This application profile favors the use of GDDR memory in datacenter environments traditionally dominated by other memory architectures. As cloud gaming services expand their subscriber bases and improve visual fidelity to compete with local gaming hardware, demand for high-performance memory in deployment infrastructure will increase correspondingly. The ability to deliver consistent, low-latency gaming experiences to thousands of concurrent users creates a strong value proposition for GDDR’s bandwidth advantages, potentially opening a substantial new market segment.

Specialized Industrial Applications Driving Custom Solutions

Beyond traditional markets, specialized industrial applications are emerging as notable opportunities for GDDR technology. Medical imaging systems, scientific instrumentation, and defense/aerospace applications increasingly require the real-time processing capabilities enabled by high-bandwidth memory architectures. These segments often prioritize reliability and longevity over pure performance metrics, creating demand for customized GDDR solutions with extended product lifecycles and specialized qualifications. Memory suppliers that can support low-volume, high-value applications with dedicated engineering resources and long-term supply commitments can develop profitable niche markets. The ability to modify standard GDDR architectures for extreme environmental conditions or radiation hardening could further differentiate offerings in these specialized sectors.

GDDR SDRAM MARKET TRENDS

High-Performance Computing Demand Accelerates GDDR SDRAM Adoption

The growing demand for high-performance computing (HPC) applications in artificial intelligence (AI), machine learning (ML), and data centers is driving the global GDDR SDRAM market. These applications require ultra-fast memory bandwidth to process large datasets efficiently—a key strength of GDDR memory. With AI workloads expanding at a compound annual growth rate (CAGR) exceeding 35%, memory solutions like GDDR6 are increasingly preferred for their ability to handle parallel processing. Furthermore, the rise of AI-powered gaming consoles and professional visualization systems is intensifying demand for high-bandwidth memory technologies.

Other Trends

Advancements in Gaming and GPU Technologies

The gaming industry remains one of the largest consumers of GDDR SDRAM, with next-generation GPUs requiring significantly higher memory bandwidth for 4K and 8K gaming, real-time ray tracing, and VR applications. The transition from GDDR5 to GDDR6 and GDDR6X has been crucial in supporting these advancements, offering nearly doubled bandwidth and improved power efficiency. Leading graphics card manufacturers are innovating aggressively to integrate faster memory solutions, with GDDR6 adoption reaching over 60% of new GPU shipments in recent years. Cloud gaming platforms are also expanding, further driving the need for high-performance memory solutions.

Automotive and Embedded Applications Fuel Growth

Beyond traditional computing and gaming, automotive applications are becoming a key driver for GDDR SDRAM adoption, particularly in autonomous vehicles and advanced driver-assistance systems (ADAS). These systems require fast memory for real-time sensor processing, with demand expected to grow at over 20% annually as vehicle autonomy increases. Additionally, industrial applications, such as medical imaging, high-frequency trading systems, and edge computing devices, are leveraging GDDR memory for its low-latency performance. The market is also witnessing a push toward energy-efficient designs as environmental regulations tighten, with manufacturers optimizing their offerings for both performance and power consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership in GDDR SDRAM Sector

The global GDDR SDRAM market is characterized by a highly consolidated competitive landscape, dominated by a few key players with significant technological and manufacturing capabilities. Samsung Electronics leads the market with an estimated 35% revenue share in 2024, owing to its cutting-edge GDDR6 production and strong partnerships with GPU manufacturers. The company’s ability to scale production while maintaining quality has solidified its market dominance.

SK Hynix and Micron Technology closely follow, collectively holding approximately 40% of the global market. Both companies have intensified investments in next-generation GDDR6X development to cater to the growing demand for high-bandwidth memory in gaming and AI applications. While SK Hynix benefits from its vertical integration strategy, Micron has gained traction through its reliability-focused approach in the data center segment.

The competitive environment has seen accelerated product innovation as companies vie for market share in the lucrative gaming and HPC sectors. Recent launches like Samsung’s 24Gbps GDDR6 and Micron’s ultra-low-power GDDR6X variants demonstrate this trend. Meanwhile, emerging players such as Changxin Memory Technologies (CXMT) are making strategic inroads in the Chinese market through government-backed initiatives, though they currently account for less than 5% of global revenues.

Strategic alliances are reshaping market dynamics, with memory manufacturers increasingly forming direct partnerships with GPU developers and system integrators. Long-term supply agreements between GDDR producers and gaming console manufacturers have become particularly crucial, with Sony and Microsoft securing dedicated production lines for their next-generation platforms.

List of Key GDDR SDRAM Manufacturers Profiled

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- Micron Technology (U.S.)

- Winbond Electronics (Taiwan)

- Changxin Memory Technologies (China)

Segment Analysis:

By Type

GDDR6 Segment Leads the Market Due to High Bandwidth and Performance Requirements

The market is segmented based on type into:

- GDDR4

- GDDR5

- GDDR6

By Application

Graphics Application Segment Dominates Owing to Rising Demand for High-Performance GPUs

The market is segmented based on application into:

- High Performance Computing

- Graphics Application

- Game Console

- Others

By End-User

Consumer Electronics Segment Maintains Strong Position Due to Gaming and Multimedia Applications

The market is segmented based on end-user into:

- Consumer Electronics

- Data Centers

- Automotive

- Industrial

Regional Analysis: GDDR SDRAM Market

Asia-Pacific

The Asia-Pacific region, spearheaded by China, Japan, and South Korea, dominates the global GDDR SDRAM market, accounting for approximately 42% of the total revenue share in 2024. This leadership is driven by the concentration of semiconductor manufacturing giants like Samsung, SK Hynix, and Micron, which collectively hold over 65% of the global memory market. China’s aggressive push in GPU development and gaming console production, coupled with Japan’s established automotive and consumer electronics sectors, creates sustained high demand for GDDR6 and next-generation memory solutions. However, recent geopolitical tensions and export controls on advanced semiconductor technologies present challenges for regional supply chain stability.

North America

North America, primarily the U.S., represents the second-largest market for GDDR SDRAM, fueled by thriving gaming, AI, and data center industries. The presence of NVIDIA, AMD, and Intel drives innovation, with GDDR6X adoption growing at 28% CAGR in high-end GPUs. The U.S. CHIPS Act’s $52 billion semiconductor manufacturing incentives are expected to bolster domestic production capabilities. While the region leads in technology adoption, dependence on Asian suppliers for memory chips creates vulnerability in the supply chain, prompting increased partnerships with Korean and Japanese manufacturers.

Europe

Europe shows moderate but steady growth in the GDDR SDRAM market, with Germany and the UK leading demand from automotive and industrial applications. The EU’s Chips Act aims to double Europe’s semiconductor market share to 20% by 2030, potentially reshaping local memory supply chains. Automotive-grade GDDR solutions for advanced driver-assistance systems (ADAS) are gaining traction, though the region remains largely dependent on imports from Asian manufacturers. Research initiatives in quantum computing and supercomputing applications present long-term growth opportunities for specialized high-bandwidth memory solutions.

South America

The South American GDDR SDRAM market remains niche but shows potential, particularly in Brazil and Argentina where gaming and cryptocurrency mining drive demand. However, economic instability and limited local manufacturing capabilities restrict market growth to primarily low-to-mid range GDDR5 products. Import tariffs averaging 18-25% on electronic components further constrain market expansion, though government initiatives to develop local tech hubs offer possibilities for future infrastructure investment in memory-intensive applications.

Middle East & Africa

This emerging market demonstrates increasing interest in GDDR technologies through data center developments in UAE and Saudi Arabia, plus gaming growth in Turkey and South Africa. While current adoption focuses mainly on legacy GDDR4/GDDR5 for consumer electronics, planned smart city projects and AI initiatives suggest future demand for advanced memory solutions. Challenges include underdeveloped semiconductor ecosystems and reliance on gray market imports, though sovereign wealth funds are beginning to invest in local technology manufacturing capabilities that may influence the regional memory market landscape by 2030.

Report Scope

This market research report provides a comprehensive analysis of the global GDDR SDRAM market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global GDDR SDRAM market was valued at US$ 8.9 billion in 2024 and is projected to reach US$ 18.4 billion by 2032, growing at a CAGR of 10.8%.

- Segmentation Analysis: Detailed breakdown by product type (GDDR4, GDDR5, GDDR6), application (High Performance Computing, Graphics Application, Game Console, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (USD 420 million in 2024), Europe, Asia-Pacific (USD 580 million in 2024), Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Samsung (28% market share), SK Hynix (22%), Micron Technology (19%), Winbond, and Changxin Memory Technologies, covering their product portfolios and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging memory technologies, AI integration in memory management, and advancements in semiconductor fabrication processes.

- Market Drivers & Restraints: Evaluation of factors driving market growth (gaming industry expansion, AI adoption) along with challenges (supply chain constraints, material shortages).

- Stakeholder Analysis: Insights for memory manufacturers, GPU producers, system integrators, and investors regarding market opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts and data from semiconductor trade associations, ensuring the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global GDDR SDRAM Market?

-> GDDR SDRAM Market size was valued at US$ 8.9 billion in 2024 and is projected to reach US$ 18.4 billion by 2032, at a CAGR of 10.8% during the forecast period 2025-2032.

Which key companies operate in Global GDDR SDRAM Market?

-> Key players include Samsung, SK Hynix, Micron Technology, Winbond, and Changxin Memory Technologies, with the top three companies holding approximately 69% market share.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance GPUs, expansion of gaming industry, and increasing adoption of AI/ML applications requiring high-bandwidth memory solutions.

Which region dominates the market?

-> Asia-Pacific is the largest market (48% share in 2024), driven by semiconductor manufacturing in South Korea and Taiwan, while North America leads in consumption.

What are the emerging trends?

-> Emerging trends include development of GDDR6X and GDDR7 standards, increasing memory densities (up to 24Gb), and integration with advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...