MARKET INSIGHTS

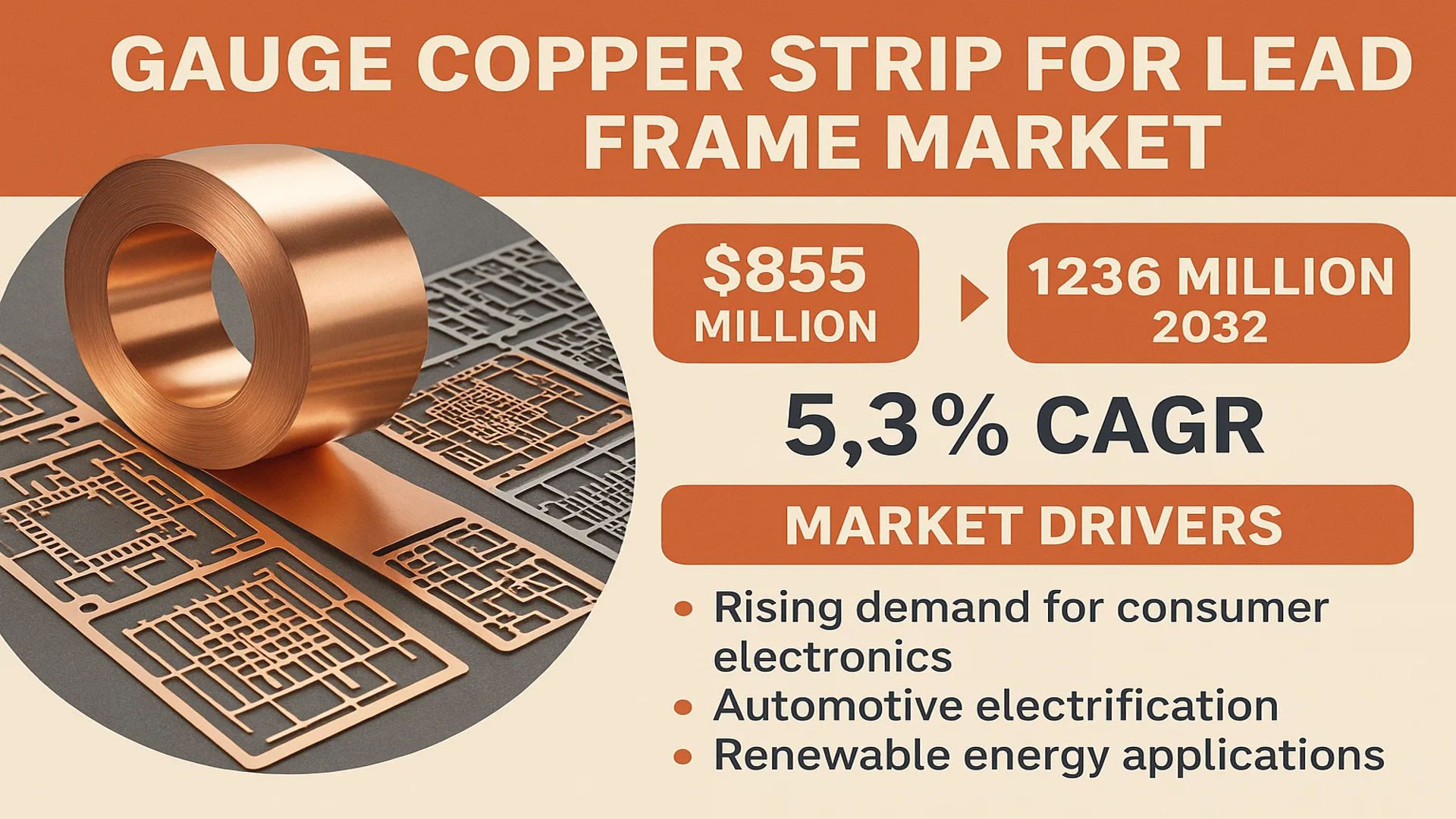

The global Gauge Copper Strip for Lead Frame Market was valued at 855 million in 2024 and is projected to reach US$ 1236 million by 2032, at a CAGR of 5.3% during the forecast period.

Gauge copper strip is a precision-engineered material used in semiconductor lead frames, offering high conductivity, thermal efficiency, and mechanical strength. These strips are critical for stabilizing chips, conducting signals, and dissipating heat in electronic components such as power transistors, LEDs, and automotive inverter modules. The material is characterized by excellent electroplatability and dimensional accuracy, making it indispensable in miniaturized and high-performance electronics.

The market growth is driven by rising demand for consumer electronics, automotive electrification, and renewable energy applications. China dominates global consumption with a 48% revenue share, followed by Taiwan (19%) and Japan (18%). Leading manufacturers include Mitsubishi Materials, Wieland, and Proterial Metals, with the top five players holding approximately 45% of the market. While Asia-Pacific remains the production hub, technological advancements in copper alloys are expanding applications in next-generation semiconductors.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Electronics Manufacturing to Fuel Copper Strip Demand

The global surge in electronics production, particularly in Asia-Pacific regions, is driving substantial growth in the gauge copper strip market. With China accounting for 48% of global consumption and electronics manufacturing projected to grow at 6.2% annually through 2030, the demand for high-quality lead frame materials has intensified. Copper strips offer unparalleled conductivity and thermal management properties essential for modern semiconductor packaging. Recent advancements in 5G infrastructure and IoT devices have particularly increased requirements for precision copper components in power transistors and LED applications, where material performance directly impacts device efficiency and longevity.

Automotive Electrification Emerges as Key Growth Catalyst

The automotive industry’s rapid transition toward electric vehicles (EVs) is creating unprecedented demand for specialized copper materials. EV power systems require 3-4x more copper content than traditional vehicles, with critical applications in inverters, motor controllers and battery management systems. As global EV production is forecast to reach 40 million units annually by 2030, manufacturers are increasingly adopting high-performance copper alloys that can withstand higher current loads while maintaining dimensional stability. This sector’s growth directly benefits lead frame producers, particularly in China where both automotive production and copper strip manufacturing are concentrated.

Miniaturization Trends Driving Technical Material Innovation

Semiconductor packaging continues advancing toward smaller form factors with higher power densities, mandating improved material solutions. The market for ultra-thin (0.15-0.3mm) copper strips is growing at 7.1% annually as manufacturers develop alloys with enhanced strength-conductivity ratios. Leading producers have introduced proprietary copper-tin-phosphorus formulations that maintain 85% IACS conductivity while achieving 40% greater tensile strength compared to conventional materials. These innovations enable thinner lead frames that meet the rigorous reliability requirements of advanced chip packing technologies while resisting thermal fatigue in high-temperature applications.

MARKET RESTRAINTS

Volatile Copper Prices Create Supply Chain Uncertainties

The copper strip market remains vulnerable to raw material price fluctuations, with LME copper prices experiencing 23% annual volatility since 2020. This instability complicates long-term contracting and inventory management for both producers and end-users. Manufacturers must balance material cost risks against the need to maintain strict alloy composition standards, particularly for specialized lead frame grades requiring 99.99% pure copper feedstocks. The situation is compounded by increasing energy costs in primary copper production, which account for 35-40% of smelting operational expenses in major producing regions like China and Japan.

Technical Barriers Limit Material Adoption in Advanced Applications

While copper offers superior conductivity, performance limitations in extreme environments restrain some high-end applications. Certain power semiconductor packages require operating temperatures exceeding 200°C where copper’s thermal expansion properties become problematic. The industry continues working to develop composite and alloy solutions, but these often involve trade-offs in conductivity or processability. Additionally, maintaining sub-micron surface finishes across large production runs presents ongoing quality control challenges, particularly for ultra-thin gauges where material defects can critically impact downstream assembly yields.

MARKET CHALLENGES

Intense Competition Pressures Manufacturer Margins

The concentrated nature of the lead frame copper strip market, where the top five producers control 45% share, creates persistent pricing pressures. Asian manufacturers particularly face squeezed profitability as regional capacity expansions outpace demand growth in certain segments. With production costs varying significantly by region – Chinese producers operate at approximately 15-20% lower cost basis than Japanese counterparts – the market has seen increased consolidation efforts. However, the capital-intensive nature of precision rolling and finishing operations makes strategic repositioning challenging for mid-tier suppliers.

Other Challenges

Regulatory Compliance Complexities

Environmental regulations governing copper processing continue evolving, particularly regarding wastewater treatment and energy consumption standards. The EU’s recent inclusion of copper production in its carbon border adjustment mechanism may impact trade flows, while China’s tightening emissions standards require significant facility upgrades from domestic producers.

Supply Chain Vulnerabilities

Geopolitical factors and trade policies increasingly influence material availability, with some regions stockpiling strategic metal reserves. The industry’s reliance on a few major copper producing nations creates potential bottlenecks, as demonstrated during recent pandemic-related disruptions that caused 12-18 week lead time extensions for specialty alloys.

MARKET OPPORTUNITIES

Advanced Packaging Technologies Open New Application Frontiers

Emerging semiconductor packaging approaches like fan-out wafer-level packaging (FOWLP) and 3D IC integration are creating demand for innovative copper material solutions. These technologies require ultra-thin, high-strength conductors with exceptional planar uniformity – specifications aligning perfectly with gauge copper strip capabilities. Early adopters developing tailored alloys for these applications are achieving 20-30% premiums over conventional products. The market for advanced packaging materials is projected to grow at 9.4% CAGR through 2032, offering substantial opportunities for technological differentiation.

Sustainability Initiatives Drive Circular Economy Potential

Growing emphasis on sustainable manufacturing is accelerating copper recycling infrastructure development. The metal’s inherent recyclability – retaining 95% of original properties through repeated processing – positions it favorably in circular economy models. Several lead frame manufacturers have implemented closed-loop recycling programs achieving 85-90% material recovery rates from production scrap. As regulatory pressures and consumer preferences increasingly favor sustainable sourcing, these initiatives provide both environmental and economic benefits while differentiating suppliers in competitive markets.

GAUGE COPPER STRIP FOR LEAD FRAME MARKET TRENDS

Growing Demand for High-Strength Copper Alloys in Semiconductor Manufacturing

The global gauge copper strip for lead frame market is experiencing significant growth due to the increasing adoption of high-strength copper alloys in semiconductor packaging. As integrated circuits continue to advance toward miniaturization and higher performance, lead frame materials must meet stringent requirements for conductivity, thermal management, and mechanical stability. Copper strips with thicknesses between 0.15mm to 4mm dominate the market, accounting for over 70% of production, particularly in applications like power transistors and LED packaging. The shift toward electric vehicles and renewable energy technologies has further intensified demand, with automotive inverter modules alone contributing nearly 25% of lead frame copper usage in 2024.

Other Trends

Asia-Pacific as the Dominant Production and Consumption Hub

Asia-Pacific, led by China, Taiwan, and Japan, currently accounts for approximately 85% of global gauge copper strip production and consumption. China’s market revenue share stands at 48%, driven by expanding electronics manufacturing and government support for semiconductor self-sufficiency. Japan remains a technological leader in high-precision copper alloys, with key players like Mitsubishi Materials and Kobelco pioneering advanced formulations that combine conductivity exceeding 90% IACS with tensile strengths above 500 MPa. Meanwhile, Taiwanese manufacturers are focusing on thinner gauge strips (below 0.2mm) to support the latest chip packaging technologies.

Technology Advancements in Processing and Surface Treatment

Recent developments in rolling mill technologies and surface treatment processes are enhancing the performance characteristics of gauge copper strips. Precision cold rolling now achieves thickness tolerances within ±0.001mm, while new electroplating techniques improve corrosion resistance without compromising conductivity. The market is seeing increased adoption of copper-nickel-silicon alloys, which demonstrate superior stress relaxation resistance at elevated temperatures – a critical property for automotive and power electronics applications. These material innovations coincide with the industry’s transition toward smaller lead frame pitches, now reaching below 0.1mm in advanced packaging solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Expansion to Maintain Dominance

The global Gauge Copper Strip for Lead Frame market features a semi-consolidated competitive landscape, with key players leveraging technological advancements and regional presence to capture market share. Mitsubishi Materials and Wieland currently dominate the market, accounting for a combined revenue share of approximately 25% in 2024. Their stronghold is primarily due to vertically integrated production capabilities and extensive R&D investments in high-performance copper alloys, critical for precision semiconductor applications.

Asian manufacturers like Xinke New Materials and Tongling Nonferrous Metals Group are rapidly gaining traction, supported by China’s 48% consumption share of global gauge copper strips. These players benefit from proximity to electronics manufacturing hubs and government incentives supporting domestic material production. Recent expansions by Chinese manufacturers into high-end copper alloys suggest increasing competition with established Japanese and European suppliers.

Meanwhile, Kobelco and Proterial Metals (formerly Hitachi Metals) are countering Asian growth through strategic collaborations with automotive and power electronics manufacturers. These partnerships focus on developing lead frame materials with enhanced thermal conductivity (>380 W/m·K) and tensile strength (>600 MPa) to meet evolving industry demands.

List of Key Gauge Copper Strip Manufacturers Profiled

- Mitsubishi Materials Corporation (Japan)

- Wieland-Werke AG (Germany)

- Proterial, Ltd. (Japan)

- Kobe Steel, Ltd. (Japan)

- Poongsan Corporation (South Korea)

- Jinchuan Group (China)

- Xinke New Materials Co., Ltd. (China)

- Tongling Nonferrous Metals Group (China)

- Chinalco Luoyang Copper Processing Co., Ltd. (China)

- CNMC Albetter Albronze Co., Ltd. (China)

The market’s technological evolution is driving consolidation, with top five players expected to increase their combined share from 45% to over 50% by 2032. Recent developments include Mitsubishi Materials’ 2023 acquisition of a European copper alloy specialist, while Chinese players are expanding production capacity by 15-20% annually to meet surging domestic demand from electric vehicle and renewable energy sectors.

Segment Analysis:

By Type

Thickness 0.15-3mm Segment Holds Dominance Due to Widespread Use in Miniaturized Electronic Components

The market is segmented based on type into:

- Thickness 0.15-3mm

- Thickness 3-4mm

- Others

By Application

Power Transistors Segment Leads Owing to Increasing Demand for High-Performance Semiconductor Devices

The market is segmented based on application into:

- Power Transistors

- LEDs

- Automotive Inverter Modules

- Others

By Material Composition

Copper Alloys are Preferred for Their Superior Thermal and Electrical Conductivity Properties

The market is segmented based on material composition into:

- Pure Copper

- Copper Alloys

- Subtypes: Copper-Iron, Copper-Nickel-Silicon, and others

- Others

Regional Analysis: Gauge Copper Strip for Lead Frame Market

Asia-Pacific

Asia-Pacific is the undisputed leader in the global gauge copper strip for lead frame market, accounting for over 70% of market share by production and consumption. China dominates with its massive 48% revenue share of global demand, driven by the country’s thriving electronics manufacturing sector. The growth of automotive electrification, 5G infrastructure, and renewable energy systems has created unprecedented demand for high-precision copper strips used in semiconductor packaging. Japan follows with an 18% consumption share, maintaining its position through technological superiority in precision engineering. While cost-sensitive manufacturers initially favored conventional copper alloys, there’s a growing preference for high-performance C19400 and C7025 copper alloys as the region’s semiconductor industry moves toward miniaturization.

North America

The North American market prioritizes high-end applications in aerospace, defense, and automotive electronics where premium-grade copper strips command significant value. Strict regulations governing material traceability and reliability requirements for military-grade semiconductors create a specialized niche. The U.S. leads regional demand, particularly for 0.15-3mm thickness strips used in advanced driver-assistance systems (ADAS). With reshoring efforts gaining momentum, domestic production of specialty copper alloys is expected to grow. However, higher production costs relative to Asian suppliers and limited upstream copper processing capacity remain key challenges.

Europe

Europe’s market is characterized by high-value, precision-engineered solutions for automotive and industrial applications. Germany and Italy lead in consumption, with stringent EU regulations on material composition driving innovation in lead-free and low-impurity copper alloys. The region has seen increasing adoption of C194 alloy strips for EV power modules, though dependence on imported raw materials impacts cost competitiveness. Recent investments in localized production of specialty copper strips aim to reduce reliance on Asian suppliers while meeting sustainability requirements. The focus on Industry 4.0 has also increased demand for precision-grade materials in sensor applications.

South America

The South American market remains relatively underdeveloped but shows potential for growth in Brazil’s expanding electronics sector. Currently, most demand is met through imports, primarily from China and Japan. Limited local processing capabilities and variable raw material quality constrain domestic production, though some Brazilian manufacturers are investing in upgraded rolling mills. The automotive sector presents the strongest growth opportunity, particularly for copper-nickel-silicon alloy strips used in hybrid vehicle components. However, economic volatility continues to impact capital investments in the region’s semiconductor supply chain.

Middle East & Africa

This emerging market is characterized by selective growth in Gulf Cooperation Council (GCC) countries, where economic diversification programs are fostering technology manufacturing ecosystems. The UAE and Saudi Arabia show particular promise with investments in semiconductor assembly and testing facilities creating opportunities for copper strip suppliers. Most demand is currently met through imports, though new copper processing facilities in Oman could support regional supply. Infrastructure limitations and the lack of established electronics manufacturing bases in most African nations currently restrict market development, but long-term growth potential exists as the continent’s technology sectors develop.

Report Scope

This market research report provides a comprehensive analysis of the global Gauge Copper Strip for Lead Frame market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 855 million in 2024 and is projected to reach USD 1,236 million by 2032, growing at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (Thickness 0.15-3mm, Thickness 3-4mm), application (Power Transistors, LEDs, Others), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. China dominates consumption with 48% market share, followed by Taiwan (19%) and Japan (18%).

- Competitive Landscape: Profiles of leading market participants including Mitsubishi Materials, Wieland, Proterial Metals, Kobelco, and Poongsan, with the top five players holding about 45% market share.

- Technology Trends & Innovation: Assessment of emerging semiconductor packaging technologies and the shift toward high-strength, high-conductivity lead frame materials.

- Market Drivers & Restraints: Evaluation of factors driving market growth including demand from automotive and renewable energy sectors, along with challenges like raw material price volatility.

- Stakeholder Analysis: Strategic insights for copper strip manufacturers, semiconductor companies, investors, and policymakers regarding market opportunities and challenges.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Gauge Copper Strip for Lead Frame Market?

-> Gauge Copper Strip for Lead Frame Market was valued at 855 million in 2024 and is projected to reach US$ 1236 million by 2032, at a CAGR of 5.3% during the forecast period.

Which key companies operate in Global Gauge Copper Strip for Lead Frame Market?

-> Key players include Mitsubishi Materials, Wieland, Proterial Metals, Kobelco, Poongsan, Jinchuan Group, and Xinke New Materials, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand from automotive electronics, renewable energy applications, and the miniaturization trend in semiconductor packaging.

Which region dominates the market?

-> Asia-Pacific dominates the market, with China accounting for 48% of global consumption, followed by Taiwan and Japan.

What are the emerging trends?

-> Emerging trends include development of advanced copper alloys, integration with smart manufacturing processes, and increasing adoption in power electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...