GaN Power Electronics Market Insights

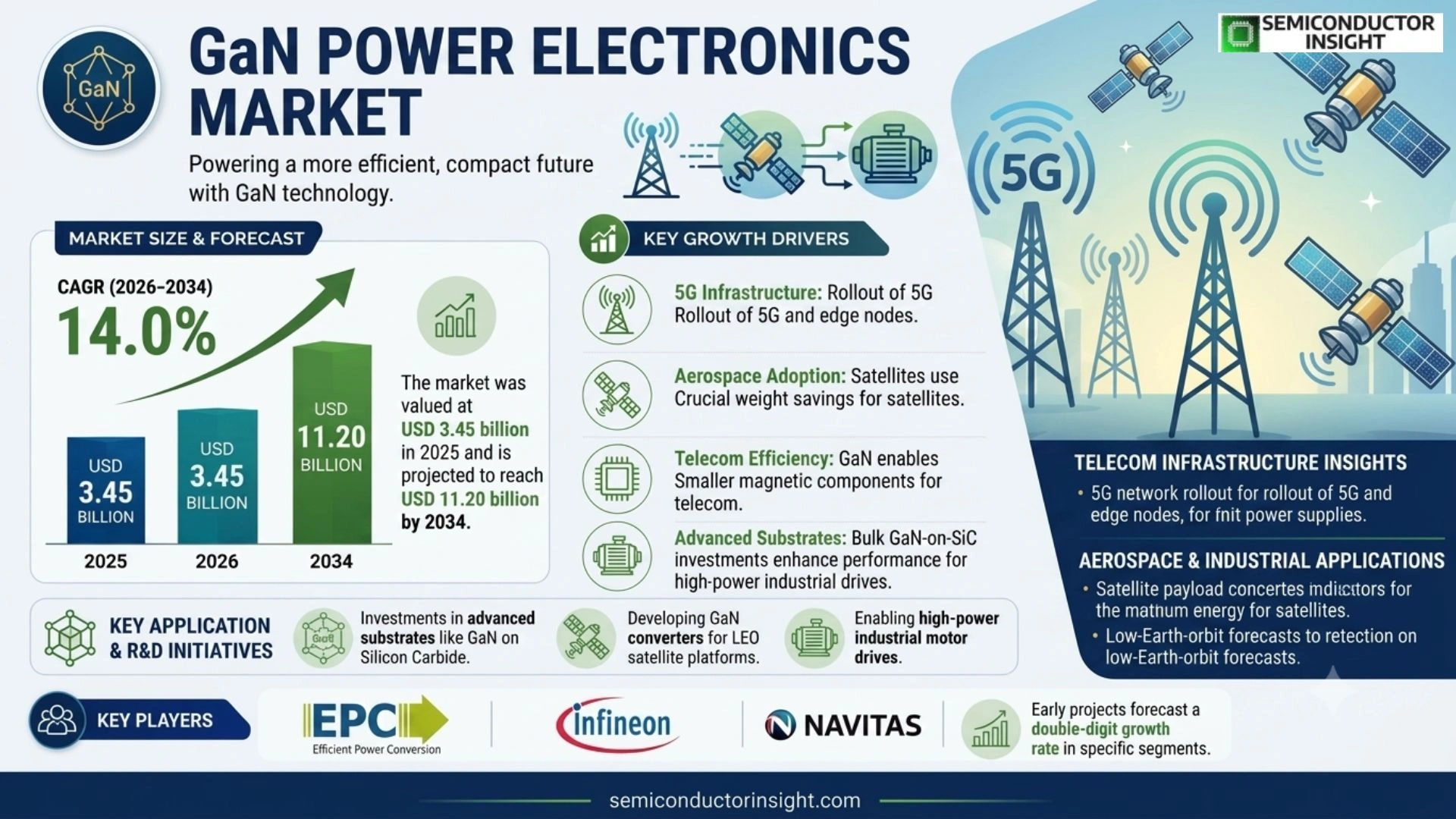

GaN Power Electronics Market size was valued at USD 3.10 billion in 2025. The market is projected to grow from USD 3.45 billion in 2025 to USD 11.20 billion by 2034, exhibiting a CAGR of 14% during the forecast period.

GaN power electronics refer to devices built on gallium nitride semiconductor material that enable high‑efficiency switching and operation at higher voltages and frequencies than traditional silicon counterparts.

These components,such as transistors, diodes and integrated modules,are essential for modern power conversion systems used in data centers, electric vehicles, renewable energy interfaces and aerospace applications.

The market is experiencing rapid growth because automotive electrification, data‑center power density demands and aggressive energy‑efficiency regulations are driving adoption.

Furthermore, continued R&D investment from leading manufacturers,including Infineon Technologies, Texas Instruments, NXP Semiconductors, ON Semiconductor and STMicroelectronics,has accelerated cost reductions and expanded product portfolios.

As supply chains mature and design tools improve, end‑users are increasingly replacing silicon‑based solutions with GaN technology, reinforcing the upward trajectory of the sector.

MARKET DRIVERS

Growing Adoption in Automotive Applications

GaN Power Electronics Market is being propelled by the rapid electrification of vehicles, where GaN devices enable higher efficiency converters for on‑board chargers and electric drive inverters. Analysts estimate that automotive GaN components will account for nearly 30% of total unit shipments by 2028.

Expansion of Renewable Energy Infrastructure

Renewable energy systems, especially solar‑plus‑storage, demand lightweight, high‑frequency power converters. GaN technology reduces thermal losses by up to 40%, allowing smaller inverter footprints and lower balance‑of‑system costs, which drives market uptake across utility‑scale and distributed projects.

➤ “GaN devices are expected to capture a 15% CAGR globally through 2032, outpacing traditional silicon solutions.”

Additional momentum comes from data‑center power‑management strategies that prioritize energy‑saving architectures. GaN Power Electronics Market benefits from policy incentives targeting energy efficiency, reinforcing a virtuous cycle of technology adoption and cost reduction.

MARKET CHALLENGES

Manufacturing Yield and Scale‑Up Issues

Despite performance advantages, GaN Power Electronics Market faces challenges in achieving high‑volume yields. Current epitaxial growth processes can result in defect densities that affect device reliability, limiting large‑scale adoption in cost‑sensitive segments.

Other Challenges

Cost Sensitivity

The higher material and processing costs of GaN compared with silicon translate to premium pricing. OEMs in consumer electronics often defer migration until economies of scale lower total cost of ownership, slowing market penetration.

Supply‑chain constraints for high‑purity substrates further complicate scaling efforts, prompting manufacturers to invest in domestic production capabilities to mitigate lead‑time risks.

MARKET RESTRAINTS

Regulatory and Certification Barriers

Stringent safety and electromagnetic compatibility certifications required for automotive and aerospace applications add time and cost to GaN product launches. Compliance cycles can extend product‑to‑market timelines, restraining rapid market expansion.

The lack of unified global standards for GaN power modules creates fragmented testing requirements, compelling manufacturers to maintain multiple certification dossiers, which strains resources.

Furthermore, legacy infrastructure in many industrial plants remains optimized for silicon‑based converters. Retrofitting these facilities for GaN integration entails capital expenditure that many operators deem non‑essential in the short term.

MARKET OPPORTUNITIES

Emerging 5G and Edge Computing Power Supplies

The rollout of 5G networks and edge‑computing nodes elevates demand for compact, high‑efficiency power supplies. GaN’s ability to operate at higher switching frequencies enables smaller magnetic components, opening a sizable niche for GaN Power Electronics Market in telecom infrastructure.

Additionally, the aerospace sector is exploring GaN‑based power converters for satellite payloads, where weight savings directly impact launch costs. Early‑stage projects forecast a double‑digit growth rate for GaN solutions in low‑Earth‑orbit platforms.

Investment in advanced substrate technologies, such as bulk GaN on silicon carbide, promises to further reduce on‑resistance and enhance thermal performance, unlocking new application spaces in high‑power industrial drives.

GaN Power Electronics Market Trends

Automotive Electrification Driving Adoption

Automotive manufacturers are rapidly integrating GaN power devices into electric‑vehicle drivetrains to meet stricter efficiency standards and reduce overall vehicle weight. GaN transistors can switch at higher voltages and frequencies than silicon, enabling compact converters that improve power‑train efficiency and extend range. Recent product launches indicate that more than 30 % of new EV models introduced in 2024 feature GaN‑based power stages, a clear signal that the industry is moving away from legacy silicon solutions. In parallel, leading semiconductor firms such as Infineon and Texas Instruments have expanded their GaN portfolios, lowering component costs and accelerating design cycles. This convergence of regulatory pressure, performance advantage, and cost reduction is a primary catalyst for GaN Power Electronics Market.

Other Trends

Data‑Center Power Density

Data‑center operators are turning to GaN modules to address rising power‑density demands and tighter energy‑efficiency regulations. The high switching speed of GaN reduces conduction and switching losses in server power supplies, delivering up to 20 % higher efficiency compared with traditional silicon converters. As a result, modern rack designs can accommodate more compute capacity per unit of power, directly cutting operating expenses. Industry observations show a steady migration toward GaN‑enabled power stages in new data‑center builds, with design teams citing smaller thermal footprints and simplified cooling as decisive factors. Continued R&D investment from companies such as NXP Semiconductors and ON Semiconductor is further expanding the range of GaN products available for high‑performance computing environments.

Renewable Energy Interface Expansion

GaN power electronics are increasingly embedded in renewable‑energy inverters and grid‑tie converters, where high voltage handling and low thermal loss are critical. The ability of GaN devices to operate at higher frequencies allows inverter designers to reduce the size of magnetic components, resulting in more compact and lighter solar‑farm installations. Market observations indicate that a growing share of new solar and wind projects specify GaN‑enabled converters, driven by the twin goals of space efficiency and compliance with increasingly stringent grid‑code standards. As supply‑chain maturity improves and design tools become more sophisticated, system integrators are replacing silicon‑based solutions with GaN, reinforcing the upward trajectory of the sector.

COMPETITIVE LANDSCAPE

Key Industry Players

GaN Power Electronics Market Competitive Overview

GaN Power Electronics market is currently led by a handful of large semiconductor firms that have leveraged extensive R&D budgets and mature manufacturing capabilities to drive cost reductions and broaden product portfolios. Infineon Technologies, Texas Instruments, and STMicroelectronics dominate the high‑volume segments, supplying GaN transistors and integrated modules for data‑center converters, electric‑vehicle chargers, and aerospace power supplies. Their scale enables a tiered market structure where Tier‑1 providers set pricing benchmarks and define performance standards, while downstream system integrators adopt their components to meet stringent efficiency targets.

Beyond the Tier‑1 leaders, a vibrant cohort of specialist companies enriches the ecosystem with niche innovations and application‑specific solutions. GaN Systems, Efficient Power Conversion (EPC), Qorvo, Analog Devices, and NXP Semiconductors focus on high‑frequency switching devices for automotive and renewable‑energy interfaces. Smaller players such as Microchip Technology, Skyworks Solutions, Wolfspeed (Cree), and Renesas Electronics contribute differentiated architectures, including GaN‑on‑silicon and vertical power devices, expanding the market’s technical depth and fostering healthy competition.

List of Key GaN Power Electronics Companies Profiled

- Infineon Technologies

- Texas Instruments

- STMicroelectronics

- GaN Systems

- Efficient Power Conversion (EPC)

- Qorvo

- Analog Devices

- NXP Semiconductors

- Microchip Technology

- Skyworks Solutions

- Wolfspeed (Cree)

- Renesas Electronics

- ON Semiconductor

- MagnaChip Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Switching Devices

|

| By Application |

|

Data Center Power Supplies

|

| By End User |

|

Original Equipment Manufacturers (OEMs)

|

| By Voltage Range |

|

Medium Voltage

|

| By Integration Level |

|

Monolithic Integrated Circuits

|

Regional Analysis: North America

The automotive industry is undergoing a rapid transformation with the increasing electrification of vehicles. GaN power electronics are playing a critical role in enabling higher voltage and current capabilities for EV chargers and onboard power management systems. The demand for GaN in automotive is expected to grow significantly as EV adoption rates continue to rise, emphasizing efficiency and performance.

Data centers are major consumers of power, and GaN power electronics offer a compelling solution for improving energy efficiency and reducing operating costs. The high efficiency of GaN components contributes to lower cooling requirements and reduced overall energy consumption within data center facilities. This is a key driver for adoption in this demanding sector.

The renewable energy sector, including solar and wind power, is leveraging GaN power electronics to enhance the efficiency and reliability of power inverters and grid connection systems. Improved power conversion efficiency directly translates to increased energy yields and reduced system losses, contributing to the overall economic viability of renewable energy projects. The integration of GaN contributes to more compact and readily deployable systems.

Industrial applications are increasingly adopting GaN power electronics for motor drives, power supplies, and other equipment where efficiency and performance are critical. The compact size and high power density of GaN components allow for the design of more efficient and space-saving industrial systems. This enhances operational flexibility and reduces overall system costs.

Europe

Europe represents a significant and rapidly growing market for GaN power electronics, driven by stringent energy efficiency regulations and a strong focus on sustainable technologies. Government initiatives promoting green energy and electrification are fueling demand across various sectors, including automotive, industrial, and renewable energy. The European Union’s emphasis on reducing carbon emissions is a key driver for the adoption of GaN power solutions. Innovation centers across Europe are actively involved in research and development, creating a dynamic ecosystem for GaN technology advancement. The region’s commitment to technological leadership positions it as a crucial market for the continued growth of GaN power electronics. Integration with smart grid initiatives is also a significant factor.

Asia-Pacific

Asia-Pacific is emerging as the largest and fastest-growing market for GaN power electronics. Rapid industrialization, increasing automotive production, and substantial investments in renewable energy infrastructure are driving significant demand. China, in particular, is a major consumer and producer of GaN power devices. Government support for domestic manufacturing and technological innovation is fostering a vibrant GaN ecosystem. The region’s focus on energy efficiency in manufacturing is a key contributing factor to market expansion. The increasing demand from electric vehicle manufacturers further reinforces Asia-Pacific’s position as a dominant market.

South America

South America is witnessing increasing adoption of GaN power electronics, primarily driven by the growing renewable energy sector and the expansion of electric vehicle infrastructure in select markets. The region’s abundant renewable energy resources, particularly solar and hydro, present opportunities for utilizing GaN power solutions in power conversion systems. While the market is currently smaller than North America and Asia-Pacific, it holds significant potential for future growth as infrastructure development progresses. Focus on energy access and grid stabilization are key considerations driving adoption.

Middle East & Africa

The Middle East & Africa represents a nascent but promising market for GaN power electronics. Significant investments in renewable energy projects, particularly solar power, are creating demand for efficient power conversion solutions. The region’s growing automotive sector and increasing focus on energy efficiency in buildings are also contributing to market growth. While challenges related to infrastructure and regulatory frameworks exist, the long-term growth potential for GaN power electronics in this region is substantial, particularly within the context of ambitious sustainability goals.

Report Scope

This market research report provides a comprehensive analysis of the GaN Power Electronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of GaN Power Electronics Market?

-> GaN Power Electronics Market was valued at USD 3.10 billion in 2025 and is expected to reach USD 11.20 billion by 2034, growing at a CAGR of 14% during the forecast period.

Which key companies operate GaN Power Electronics Market?

-> Key players include Infineon Technologies, Texas Instruments, NXP Semiconductors, ON Semiconductor, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include automotive electrification, data‑center power density demands, and stringent energy‑efficiency regulations.

Which region dominates the market?

-> The reference does not specify a single dominant region; market adoption is observed globally across major economies.

What are the emerging trends?

-> Emerging trends include increased integration of GaN devices in data‑center power supplies, electric vehicle powertrains, renewable energy converters, and aerospace applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...