MARKET INSIGHTS

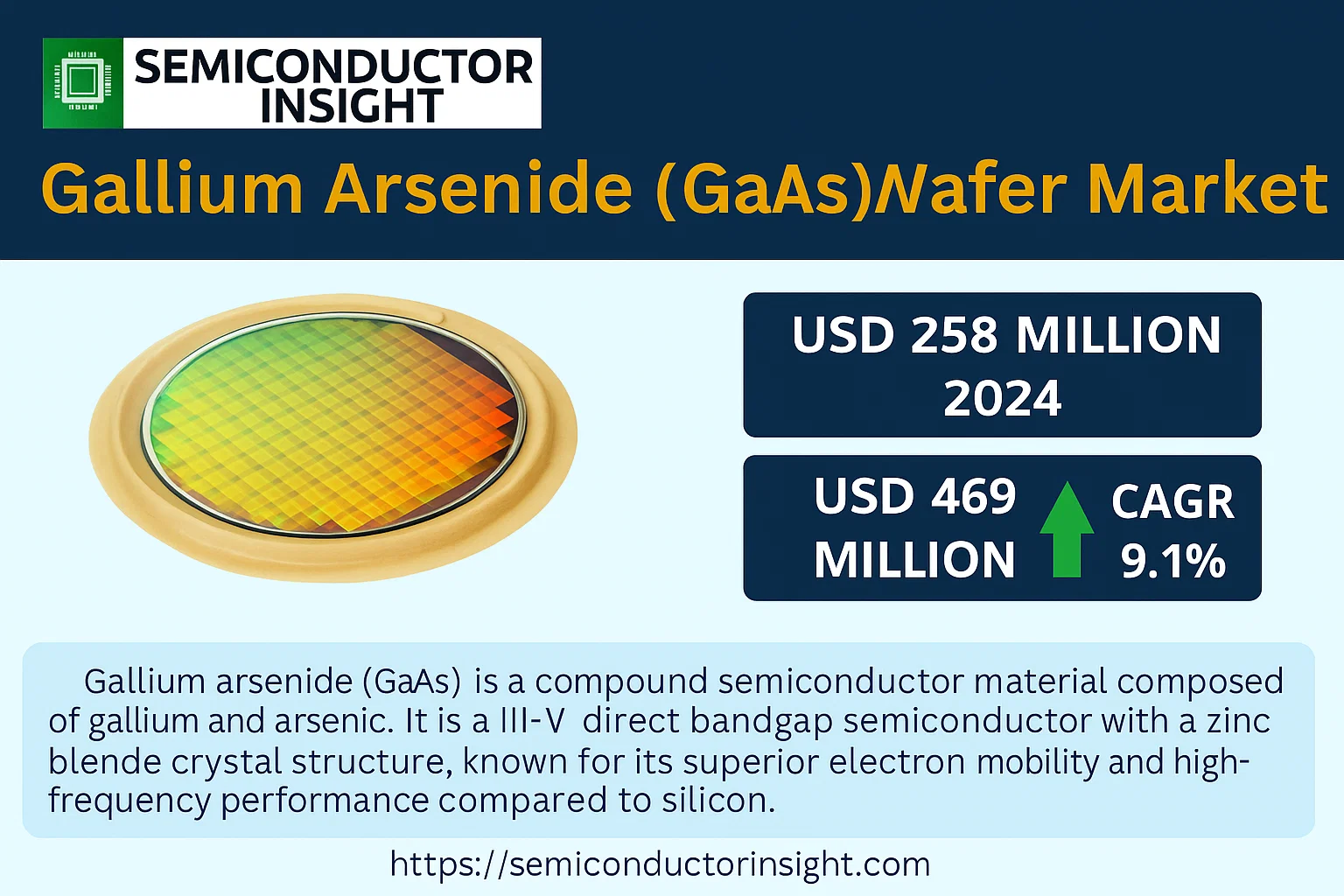

Global Gallium Arsenide (GaAs) Wafer Market size was valued at USD 258 million in 2024. to USD 469 million by 2032, exhibiting a CAGR of 9.1% during the forecast period.

Gallium arsenide (GaAs) is a compound semiconductor material composed of gallium and arsenic. It is a III-V direct bandgap semiconductor with a zinc blende crystal structure, known for its superior electron mobility and high-frequency performance compared to silicon. GaAs wafers serve as the foundational substrate for manufacturing various high-performance electronic and optoelectronic devices.

The Market growth is primarily driven by the escalating demand for high-speed data transmission in telecommunications, the proliferation of smartphones and connected devices, and the expansion of fiber optic networks. Additionally, the adoption of GaAs in advanced applications such as vehicle radar systems in autonomous driving and high-efficiency photovoltaic cells is contributing to Market expansion. The competitive landscape is concentrated, with the top two players holding a combined Market share of approximately 50%. Key manufacturers include Freiberger Compound Materials, AXT, Inc., and Sumitomo Electric Industries, Ltd., who are actively investing in capacity expansion to meet rising demand from sectors like radio frequency (RF) components, which dominates application segments with over a 50% share.

MARKET DRIVERS

5G Network Expansion and Smartphone Demand

Global rollout of 5G infrastructure is a primary driver for the Gallium Arsenide (GaAs) wafer Market. GaAs-based power amplifiers and RF switches are essential components in 5G base stations and next-generation smartphones, offering superior high-frequency performance and power efficiency compared to silicon. The increasing adoption of 5G-enabled devices, with smartphone shipments projected to exceed 1.5 billion units annually, directly fuels demand for high-quality GaAs wafers.

Growth in Automotive Radar and LiDAR

The automotive industry’s shift toward Advanced Driver-Assistance Systems (ADAS) and autonomous vehicles is generating significant demand for GaAs wafers. These wafers are used in high-frequency radar and LiDAR systems, which are critical for collision avoidance and object detection. The automotive radar Market is expected to grow at a compound annual growth rate of over 15%, driving substantial consumption of GaAs substrates.

➤ GaAs wafers are pivotal in photonics, with the optoelectronics segment accounting for a major share of the Market revenue.

Additionally, the expanding applications in aerospace and defense for radar and electronic warfare systems, alongside the steady demand from the optoelectronics sector for LEDs and laser diodes, further consolidate the Market’s growth trajectory.

MARKET CHALLENGES

High Manufacturing Costs and Competition from Alternative Materials

The production of Gallium Arsenide wafers involves complex and expensive processes, including high-purity raw material sourcing and demanding epitaxial growth techniques. This results in a significantly higher cost per wafer compared to silicon. Furthermore, the Market faces growing competition from semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) in specific high-frequency and high-power applications, challenging GaAs’s Market share.

Other Challenges

Supply Chain Constraints

The supply of raw gallium and arsenic is geographically concentrated and subject to potential disruptions, creating volatility in material prices and availability for wafer manufacturers.

Technical Complexity and Yield

Achieving high yields of defect-free, large-diameter GaAs wafers remains technically challenging, limiting production scalability and impacting overall profitability.

MARKET RESTRAINTS

Environmental and Regulatory Hurdles

Gallium Arsenide contains arsenic, a toxic material, which subjects its production, handling, and disposal to stringent environmental regulations worldwide. Compliance with regulations such as REACH and RoHS increases operational costs and poses a significant barrier to Market entry for new players. The costs associated with waste management and workplace safety measures further restrain Market expansion.

High Initial Investment and R&D Costs

The capital expenditure required for establishing state-of-the-art GaAs wafer fabrication facilities is substantial. Continuous investment in research and development is also necessary to keep pace with technological advancements and performance requirements, creating a high barrier for small and medium-sized enterprises and acting as a major Market restraint.

MARKET OPPORTUNITIES

Emerging Applications in Photovoltaics and Quantum Computing

Gallium Arsenide is gaining traction in high-efficiency, multi-junction solar cells used in space satellites and concentrated photovoltaic systems, where its superior conversion efficiency is critical. The nascent quantum computing sector also presents a significant opportunity, as GaAs is explored for hosting spin qubits due to its excellent electronic properties, opening a new frontier for the wafer Market.

Advancements in Wafer Reclaim and Large-Diameter Substrates

Technological advancements in wafer reclaim processes are reducing costs and improving sustainability, making GaAs more accessible. The ongoing development and commercialization of larger diameter GaAs wafers (e.g., 6-inch and 8-inch) offer the potential for greater economies of scale and higher throughput in device manufacturing, creating substantial growth opportunities for foundries and substrate suppliers.

Gallium Arsenide (GaAs) Wafer Market Trends

Strong Market Growth Fueled by RF and Optoelectronic Demand

Global Gallium Arsenide (GaAs) Wafer Market is experiencing robust expansion, projected to grow from a valuation of USD 258 million in 2024 to USD 469 million by 2032, representing a compound annual growth rate (CAGR) of 9.1%. This significant growth is primarily attributed to the increasing demand for high-frequency communication devices and advanced optoelectronic components. GaAs wafers, a III-V direct bandgap semiconductor, are critical for manufacturing components that outperform traditional silicon in high-frequency and high-power applications.

Other Trends

Dominance of VGF Production Method

Vertical Gradient Freeze (VGF) method for producing GaAs wafers holds a dominant position in the Market, accounting for over 60% of production. This method is preferred for its ability to produce high-quality, low-defect crystals suitable for demanding applications. The preference for VGF-grown wafers underscores the industry’s focus on quality and performance, particularly for high-volume manufacturing of RF components and LEDs.

RF Applications as the Primary Driver

Radio Frequency (RF) applications constitute the largest Market segment for GaAs wafers, holding a share exceeding 50%. The proliferation of smartphones, the ongoing rollout of 5G infrastructure, and the expansion of wireless networks are key drivers. GaAs-based power amplifiers and switches are essential for enabling the high-speed data transmission and improved signal integrity required by modern communication standards, solidifying RF as the cornerstone of Market demand.

Regional Market Concentration and Competitive Landscape

Geographically, China is the largest Market for GaAs wafers, commanding approximately 28% of the global share, followed by Europe and Japan. This concentration reflects China’s strong electronics manufacturing base. The competitive landscape is characterized by a high level of consolidation, with the top two players, including Freiberger Compound Materials and AXT, Inc., collectively holding about 50% of the Market share. This dynamic influences pricing, innovation cycles, and supply chain strategies globally as companies navigate a concentrated supplier base.

COMPETITIVE LANDSCAPE

Key Industry Players

Concentration of Production Capacity Among a Handful of Global Leaders

Global Gallium Arsenide (GaAs) Wafer Market is characterized by a high degree of consolidation, with the top two players, Freiberger Compound Materials and AXT, Inc., commanding approximately 50% of the Market share. These established leaders possess significant manufacturing scale, deep technical expertise in crystal growth techniques like the Vertical Gradient Freeze (VGF) method, and longstanding relationships with major downstream device manufacturers. Their dominance is underpinned by extensive intellectual property portfolios and a focus on producing high-purity, low-defect wafers essential for high-performance applications in radio frequency (RF) devices and photonics. The Market structure necessitates substantial capital investment and rigorous quality control, creating significant barriers to entry and solidifying the position of these incumbents.

Beyond the dominant duopoly, the Market includes several other significant players who compete by specializing in niche applications or specific geographic regions. Companies like Sumitomo Electric Industries and DOWA Electronics Materials Co., Ltd. are key players from Japan with strong technological capabilities. Chinese manufacturers, such as Vital Materials and China Crystal Technologies Co., Ltd., have been rapidly expanding their production capacity to serve the growing domestic Market, which is the largest globally with a share of about 28%. Other notable participants focus on specialized wafer specifications for applications including light-emitting diodes (LEDs), vertical-cavity surface-emitting lasers (VCSELs), and photovoltaic cells, creating a competitive environment where technological innovation and cost-effectiveness are critical differentiators.

List of Key Gallium Arsenide (GaAs) Wafer Companies Profiled

- Freiberger Compound Materials

- AXT, Inc.

- Sumitomo Electric Industries, Ltd.

- Vital Materials

- China Crystal Technologies Co., Ltd.

- DOWA Electronics Materials Co., Ltd.

- WIN Semiconductors Corp.

- Visual Photonics Epitaxy Co., Ltd. (VPEC)

- IQE plc

- Advanced Wireless Semiconductor Company (AWSC)

- MTI Corporation

- AXT China

- PAM-XIAMEN

- UniversityWafer, Inc.

- DOWA Holdings Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

VGF GaAs wafers represent the leading segment, primarily due to their superior cost-effectiveness for producing large-diameter, high-quality crystals with excellent uniformity and lower defect densities compared to alternative methods. This production technique is highly favored for applications requiring consistent electrical properties, making it the dominant choice for commercial manufacturing. The process is well-established and scalable, which contributes to its widespread industrial adoption, particularly for radio frequency components and optoelectronic devices where material consistency is paramount. |

| By Application |

|

RF applications are the dominant segment, leveraging the inherent high electron mobility and saturated electron velocity of GaAs wafers, which are critical for high-frequency, low-noise performance in wireless communication systems, including smartphones, Wi-Fi, and radar. The material’s superior electronic properties over silicon make it indispensable for power amplifiers and switches in modern telecommunication infrastructure, driving sustained demand. The continuous global expansion of 5G networks and the increasing complexity of mobile devices further solidify the RF segment’s leadership position, demanding the unique performance characteristics that only GaAs can consistently provide. |

| By End User |

|

Telecommunications is the leading end-user segment, driven by the pervasive demand for GaAs-based components in network infrastructure such as base stations, satellite communications, and fiber-optic systems. The transition to higher-frequency bands for 5G and the need for efficient data transmission create a robust, continuous demand for high-performance semiconductors. This sector’s growth is underpinned by global investments in expanding and upgrading communication networks, making it the most significant consumer of GaAs wafers, as they are fundamental to enabling the high-speed, reliable connectivity that modern economies depend upon. |

| By Wafer Diameter |

|

4-inch wafers currently lead the Market as they offer an optimal balance between manufacturing throughput, cost-efficiency, and technical maturity for a wide array of commercial devices. This diameter is extensively used in the production of RF components and optoelectronic devices, providing a cost-effective solution without significant compromises on yield or performance. The extensive existing fabrication infrastructure for 4-inch wafers makes them the industry workhorse, although a gradual transition towards larger 6-inch diameters is observed for high-volume applications to achieve greater economies of scale in the long term. |

| By Product Grade |

|

Semiconductor Grade wafers are the dominant segment, characterized by extremely high purity and precise electrical properties required for active electronic components like transistors and integrated circuits. This grade demands stringent control over crystallographic defects and impurity levels to ensure device reliability and performance, especially in high-frequency and high-power applications. The vast majority of commercial production is dedicated to this grade to serve the massive telecommunications and consumer electronics industries, where consistent, high-quality material is non-negotiable for manufacturing success and product performance. |

Regional Analysis: Gallium Arsenide (GaAs) Wafer Market

The region possesses a mature and technologically advanced semiconductor manufacturing base. Foundries and IDMs have deep experience in epitaxial growth and wafer processing techniques specific to GaAs, enabling high-volume production with excellent yield and quality. This expertise is a significant barrier to entry for other regions and attracts global design houses seeking reliable manufacturing partners.

Unprecedented demand for 5G infrastructure and a relentless consumer electronics Market are the primary growth engines. The proliferation of 5G base stations and smartphones, both requiring high-performance GaAs RF components, ensures a sustained and growing Market. Local OEMs are major consumers, creating a tight-knit supply-demand loop within the region.

National initiatives across key countries actively promote self-sufficiency and leadership in semiconductors. Substantial funding, tax incentives, and strategic industrial policies are channeled towards compound semiconductor technologies, including GaAs. This top-down support accelerates R&D, encourages capacity expansion, and strengthens the entire value chain from raw materials to finished devices.

A highly integrated and efficient supply chain is a critical advantage. The region hosts everything from substrate suppliers and epitaxy growers to device fabricators and assembly/test facilities. This vertical integration reduces logistics costs, shortens time-to-Market, and fosters collaboration, making the ecosystem exceptionally resilient and responsive to Market fluctuations.

North America

North America remains a critical and technologically sophisticated region in the GaAs wafer Market, characterized by strong R&D capabilities and high-value applications. The United States is home to several leading GaAs wafer manufacturers and design companies that focus on cutting-edge applications, particularly in the defense and aerospace sectors, where the high-frequency and radiation-hardened properties of GaAs are essential. There is also significant activity in the automotive sector for advanced driver-assistance systems (ADAS) and in premium telecommunications infrastructure. While manufacturing volume may not match Asia-Pacific, the region excels in innovation, developing next-generation devices for specialized, high-performance Markets. The presence of major technology firms and a culture of venture capital investment in deep-tech startups continues to drive advancement in GaAs material science and device architectures.

Europe

The European GaAs wafer Market is defined by a strong focus on research, niche applications, and automotive electronics. The region benefits from collaborative research initiatives and the presence of several specialized foundries that cater to demanding sectors like aerospace, defense, and medical technology. European automotive manufacturers are significant drivers, integrating GaAs-based components into vehicle radar systems and other safety-critical electronic systems. There is also a notable presence in the optoelectronics segment, including applications for photonic integrated circuits. While the overall scale of production is more modest compared to leading regions, Europe maintains a competitive edge through high-quality engineering, stringent standards, and innovation in specialized, low-volume but high-margin Market segments supported by both public and private research funding.

South America

The GaAs wafer Market in South America is in a developing stage, with limited local manufacturing capabilities. The regional Market is primarily consumption-driven, relying on imports to meet the demand from its telecommunications and consumer electronics sectors. As countries gradually expand and modernize their mobile networks, demand for GaAs components is expected to grow, albeit from a relatively small base. The Market potential is linked to broader economic stability and increased investment in technological infrastructure. Currently, the region’s role is more that of an emerging Market with future growth potential rather than a significant production or innovation hub for GaAs wafers on the global stage.

Middle East & Africa

The Middle East & Africa region represents an emerging Market for GaAs wafers, with growth primarily fueled by telecommunications infrastructure development, especially in Gulf Cooperation Council (GCC) countries. Investments in 5G networks and a growing consumer base for smartphones are creating new demand. However, the region lacks a significant local manufacturing base for compound semiconductors, making it almost entirely import-dependent. Some countries are beginning to formulate strategic plans to develop technology hubs, which could, in the long term, include support for high-tech manufacturing. For now, the Market dynamics are characterized by growing end-use demand with supply chains heavily oriented towards imports from Asia and Europe.

Report Scope

This Market research report provides a comprehensive analysis of the Gallium Arsenide (GaAs) Wafer Market , covering the forecast period 2025–2032. It offers detailed insights into Market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current Market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and Market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into Market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading Market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving Market growth along with challenges, supply chain constraints, regulatory issues, and Market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time Market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current Market size of Gallium Arsenide (GaAs) Wafer Market?

-> Global Gallium Arsenide (GaAs) Wafer Market was valued at USD 258 million in 2024 and is projected to reach USD 469 million by 2032, exhibiting a CAGR of 9.1% during the forecast period.

Which key companies operate in Gallium Arsenide (GaAs) Wafer Market?

-> Key players include Freiberger Compound Materials, AXT, Inc., Sumitomo Electric Industries, Ltd., Vital Materials, China Crystal Technologies Co., Ltd., and DOWA Electronics Materials Co., Ltd., among others. The top 2 players hold a combined Market share of about 50%.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-frequency electronic devices, the proliferation of smartphones and wireless communication infrastructure, and the growing adoption of GaAs in photonic applications such as LEDs and laser diodes.

Which region dominates the Market?

-> China is the largest Market, with a share of about 28%, followed by Europe and Japan.

What are the emerging trends?

-> Emerging trends include advancements in VGF and LEC manufacturing methods, increasing use in RF applications which hold over 50% Market share, and the expanding application of GaAs wafers in VCSEL and photovoltaic devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...